Written by: Yokiiiya

After finishing the conclusion of Agentic Payment last week, everyone has been talking about it, but the real difficulty lies in the journey in between. Afterwards, I chatted with some friends about this direction, but the more I talked, the more I felt that many of the most fundamental issues have yet to be clarified.

What exactly is Agentic Payment? How does it differ from automatic payments? What’s the difference with smart contracts? Why is it being discussed now? What problem does it really solve?

If these questions are themselves vague, then many discussions about "where the opportunities are," "who can do it," and "what the path looks like" will also feel a bit unfocused.

Therefore, in this article, I want to start with a very basic question: What is Agentic Payment, and how has it evolved step by step to this stage?

1. What is Agentic Payment?

Today, we are already quite accustomed to letting AI help us with many tasks: searching for information, writing emails, analyzing data, even making decisions. However, there is one process that still basically remains at the stage of "the last step must be manually confirmed"—payment. You can let AI help you choose a flight, compare prices, generate an order, but in the end, the moment you click "pay" still has to be done by you. AI has not yet truly become an actor that can "complete the task."

What Agentic Payment wants to change is exactly this point. In one sentence:

Agentic Payment refers to the ability of an AI Agent to autonomously decide and execute payment actions based on goals, context, and constraints, within the boundaries authorized by the user.

There are four key terms in this definition that need to be examined separately.

First is the AI Agent, as opposed to a script. It needs to understand goals, process information, invoke tools, and make judgments during the process, rather than executing a fixed procedure.

Second is real payment. It’s not just stopping at recommendations, redirects, or generating payment links, but rather the actual flow of funds. Third is autonomous decision-making. If payment is simply triggered by preset rules, it's closer to automatic payment; only when decisions are made based on goals and context during execution does it start to approach Agentic Payment.

Fourth is the authorization boundary. The "autonomous" here does not imply unlimited authority but operates under clear constraints. This boundary can be a monetary limit (no more than 500 yuan per transaction), a whitelist of recipients (payments only to specified suppliers), defined scenarios (only for travel-related payments), frequency control (no more than three transactions per day), or a combination of these rules. It is delineated by humans, and the system operates autonomously within this range.

So, to be more precise, Agentic Payment must meet at least four conditions simultaneously:

There is an intelligent agent, not just a simple script.

There is real payment, not just stopping at the recommendation stage.

There is a decision-making process, not just pure rule-triggering.

There is an authorized boundary, not an unlimited authority black box.

If any of these is lacking, it fundamentally does not count. Many things now referred to as Agentic Payment are essentially just: AI + recommendations, AI + automation, or AI + slightly more complex rule systems, but they have not yet touched on the core layer—allowing AI to participate in the decision of "whether to spend money."

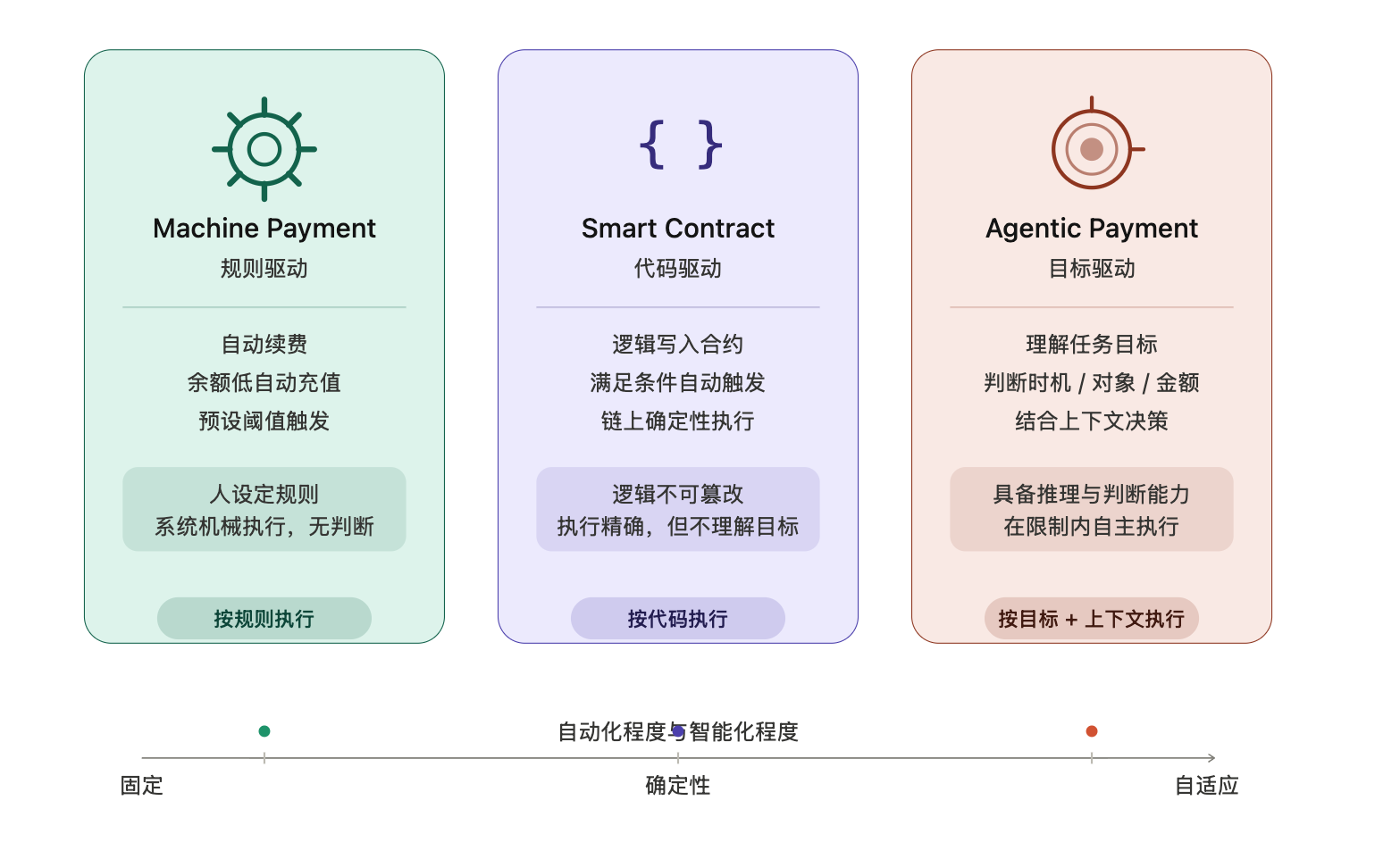

2. Why is Agentic Payment not just "more automated payment"?

When people first discuss Agentic Payment, many naturally interpret it as a matter of making payments a bit more automated, right? I think this intuition is quite normal. Because on the surface, it does seem similar. Over the past few years, payments have indeed been becoming increasingly automated: automatic renewals, password-free payments, scheduled deductions, and even on-chain conditional automatic settlements.

From an external view, the result is identical. Whether it’s rule-based automatic deductions or AI making judgments and proactively executing payments, what ultimately appears on the bill is the same transaction. The money has moved from Account A to Account B, the timestamp is at a certain moment, and the amount is what it is. There’s no trace indicating whether this money was executed based on rules or judged by AI.

The difference exists only in that invisible decision moment.

This is why the misunderstanding of "isn't it just more automation" is particularly stubborn—because you cannot perceive it by observing payment results; you can only see the difference by understanding what happens inside the system.

Once this difference is established, the nature of the whole issue changes. You are no longer just facing an execution system but a system that makes judgments during operation. These two things demand completely different requirements for risk control, authorization, and responsibility attribution. If we compare the three types of payments, the differences will become clearer:

Distinguishing in three sentences:

The decisions in the first two categories occur before execution—the rules are written by humans, and the code is written by humans, with the system merely executing. The decision for Agentic Payment happens during execution, made on the spot by the system.

This is also why Agentic Payment cannot be understood as an upgraded version of automatic payment. It is not about optimizing the original payment process a bit more or making it smoother but is gradually pushing payments from "execution-level capabilities" to "decision-level capabilities." And this step is precisely the hardest one: Are we willing to entrust the decision of "whether to pay" to machines?

3. Why is it essential to view Agentic Payment in layers?

If we discuss the term Agentic Payment without layering it, it’s easy to make it sound bigger and bigger until it can accommodate anything. If AI recommends a payment solution, it can be counted. If AI generates an order or jumps to the payment page, some may also count that. Automatic renewals, automatic deductions, and on-chain executions sometimes also get included. Going back a bit further, people have even started talking about direct transactions between Agents. While all these things are related, if they are all called Agentic Payment, the concept itself will begin to distort.

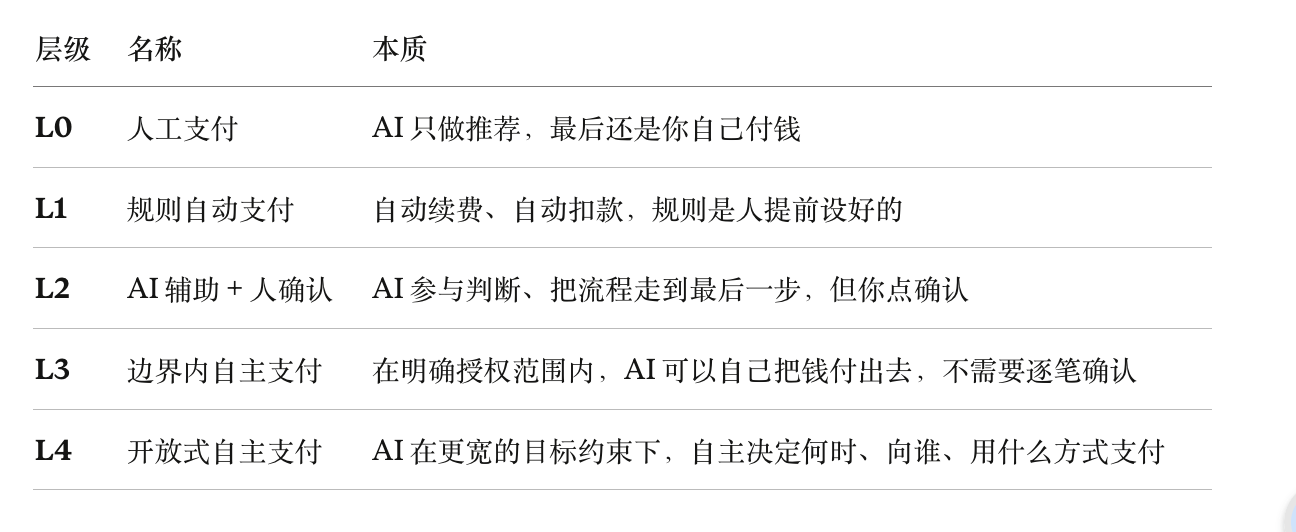

Therefore, an important approach to understanding this is not to continue quarreling over definitions, but rather to break down "the autonomy of payments." I would prefer to roughly divide it into five layers:

The significance of this layering is not to make a pretty model, but it helps you see many things clearly at once. The most direct point is: currently, most so-called Agentic Payments actually still remain at L2. AI is already capable of helping you a lot: filtering, comparing, preparing orders, and even walking through the entire process right up until the last step. But that last step is still up to you. On the surface, this seems like just missing a "confirm button." However, what is missing in between is not just a button, but a very significant gulf. Because moving from L2 to L3, the real change that occurs is that you start to hand over the final decision-making power of "whether to spend money" from humans to machines. Once this step is crossed, the entire question completely changes and suddenly becomes:

So it's not just about optimizing the product UI a bit more or enhancing the prompt. It’s a system-level issue. This is particularly similar to autonomous driving. The autonomous driving industry has insisted on layering from L1 to L5 because everyone quickly realized that "can it drive automatically" is not a binary question. The difference between assisted driving and truly autonomous driving is not about degree, but about responsibility, control, and system boundaries.

The same goes for Agentic Payment. In L1 and L2 stages, machines are primarily assisting you. Starting from L3, the machine begins to make decisions on your behalf under certain conditions. And the genuinely challenging aspect is precisely this step.

The endgame is actually easy to explain—AI helps you make decisions, AI helps you complete payments, and even in the future, Direct value exchanges between Agents, this scenario makes sense and is also very attractive to imagine. But the real difficulty has never been about articulating the endgame; it is rather the journey in between: moving from "assisted decision-making" to "bearing decision-making."

This journey cannot be crossed solely on the basis of improving model capabilities. It connects to engineering, product, risk control, compliance, responsibility attribution, and how much control users are willing to give up.

The core of Agentic Payment is not the degree of automation but the extent to which decision-making power has shifted. And this process of shifting is bound to not happen overnight.

4. What problem does Agentic Payment ultimately solve?

Why is Agentic Payment necessary? If it’s just about making payments a bit faster and smoother, then it wouldn’t be worth discussing separately. For many years, the payment industry has been working on this: binding cards, password-free transactions, one-click payments, automatic renewals, fundamentally all aimed at reducing friction. Therefore, what Agentic Payment really aims to address is not "how to pay" but a more fundamental issue: in an increasingly complex digital world, the gap between decision-making and execution is beginning to widen.

Many past payment behaviors were actually quite straightforward. You see a product, make a judgment, click to pay, and the decision and execution are almost connected. But today, that’s not the case. Many times, the complexity lies not in "payment" itself but in the long string of judgments before payment:

The commonality of these tasks is that the money itself is not the focus; the judgment is the focus. And now there is an awkward reality: AI is becoming increasingly capable of making those preceding judgments. It can understand goals, process information, compare options, and provide recommendations. But as soon as it comes to real money transfers, the process breaks down again.

As a result, you often see a common scenario: AI analyzes, compares, and generates solutions, and then in the end, humans come back to click pay. On the surface, this only seems to lack the final step, but that last step precisely indicates one thing: AI has not yet truly become a system capable of completing the task loop. It can think, it can speak, it can plan, but it still cannot bear the consequences of actions in the real world.

From this perspective, what Agentic Payment needs to address is not the payment interface but the action loop. There’s another often-overlooked issue: many payment decisions actually do not warrant consuming human attention. Not because they are unimportant, but because they often tend to be low-value yet high-frequency.

These types of decisions don’t seem significant individually, but once the numbers add up, they can become massive management costs. This is precisely where Agents are best positioned to step in—they are essentially taking over a type of "low-value but high-frequency" small decision, freeing human attention from fragmented judgments. If you look one step further, Agentic Payment encounters an even deeper question: If in the future, more and more tasks are completed by Agents, can Agents become genuine economic participants?

The traditional payment system has always operated on the premise that the payer is a person, the decision-maker is a person, and the liable party is also a person. But if an Agent makes calls to models, purchases data, subscribes to tools, allocates computing power, and even settles with another Agent to complete tasks, then payment is no longer merely "humans buying things," but more like a system actively coordinating resources to achieve a goal. Payment is no longer just part of the consumption action; it will gradually become part of task execution itself.

Thus, what Agentic Payment truly solves is more fundamental: enabling AI to progress from "thinking" to "doing," and finally to "bearing the consequences of real-world actions."

5. Why is Agentic Payment starting to be frequently discussed now?

Automatic payments are not new, smart contracts are not new, and AI has not just appeared out of nowhere. So why is it that right now, everyone suddenly starts to discuss Agentic Payment intensely? The reason is not due to a sudden breakthrough in any single technology but rather that several lines, which were originally separate, are beginning to converge at the same time.

The first line is that AI has finally started to transition from “being able to speak” to “being able to do”.

In the past, people's understanding of AI was still largely focused on "answering questions" and "generating content." It could write copy, make a summary, or provide advice. But essentially, it was more like a powerful expression system rather than a true action system.

The biggest change in this round of Agents is that AI has begun to possess more complete task capabilities: understanding goals, breaking tasks down, invoking tools, adjusting based on feedback, and ultimately executing tasks. This brings about a fundamental shift: AI is beginning to transform from an "information system" into an "action system."

The second line is that payment capabilities themselves are being API-ed and modularized.

In the past, many payment capabilities were closed, heavy, and difficult to flexibly integrate into workflows. A noticeable change over the past few years is that payment capabilities are increasingly resembling infrastructure. Stripe has introduced a new payment interface design specifically for AI Agent scenarios around 2024, significantly reducing the costs of programmatic calls to payment capabilities; Visa has also launched the "Intelligent Commerce" plan, focusing on how to enable Agents to safely complete transactions on behalf of users; Coinbase has launched a lightweight wallet solution for Agents on the Base chain, allowing Agents to independently hold and schedule funds.

Receiving payments, making payments, subscription management, wallets, escrow accounts, and on-chain settlements are all being broken down into more standardized modules. Because only when payments become a capability that can be programmatically called can Agents truly start to incorporate "payment" into their task chains.

The third line is that the nature of "payment" itself is also changing.

In the past, most payments were essentially "humans buying things"—buying products, services, tickets. Payments were more of a consumption action. But now, more and more payments are starting to become a resource call in the execution of a task: invoking a paid API to complete a task, purchasing computing power to obtain results, and systems opting for the most appropriate path and settling in real time to optimize costs.

At this point, payment is no longer just a matter of "confirming one last time"; it gradually transforms into an action that occurs frequently, fragmented, and in real-time during the process. The traditional method wherein "each transaction waits for human confirmation" is increasingly unsuitable for these new scenarios—not because people cannot confirm but because that confirmation action itself is starting to slow down the entire system.

In essence, it’s not that something suddenly matured but that three lines are aligning for the first time. AI can think but cannot do. Payments can execute but do not understand goals. Automation can run processes but cannot handle dynamic judgments. For a long time, these things were separate. And now, AI is beginning to acquire task capabilities, payment capabilities are starting to modularize, and real scenarios are beginning to require systems to handle more and more fragmented payment decisions on behalf of people—these three things are slowly beginning to align for the first time.

Agentic Payment is not being discussed because it has "suddenly been invented"; it is because it has finally transitioned from an imagination to a "conditionally viable" direction. This is also why this stage is particularly likely to be lively. The endgame can already be described, but the path is still very early, and many boundaries have not yet been genuinely verified.

6. Where will Agentic Payment start to take root?

Where will it happen first? When people talk about this direction, they often jump directly to the endgame: Agents helping you make all decisions, completing all payments, and even completing transactions directly between Agents. This scenario is certainly plausible, but it is difficult to serve as a starting point. Because once real money transfers are involved, the system will immediately face three constraints: risks must be controllable, permissions must be clear, and responsibilities must be definable.

Therefore, from a realistic path perspective, it is almost impossible for Agentic Payment to enter the L4 "open autonomous payment" right away. It is more likely to gradually cut in from some clearly defined boundaries, smaller amounts, and relatively simple decision structures.

The first category, and the easiest to occur, is high-frequency, small-amount, clearly defined resource calls (corresponding to the early form of L3).

The characteristics of this type of scenario are: the amounts are not large, but the decision-making frequency is very high, and they already have clear boundaries. For example, API calls billed per request, model calls and computing power consumption, small renewals or usage-based fees for SaaS tools, and resource scheduling in automated workflows.

These scenarios are already driven by programs (not manually operated by humans), inherently existing demand for "automatic execution." Within a set budget, allowing the Agent to decide whether to invoke a certain paid API or choose a more optimal invocation path—the key here is not to "let it spend money freely," but to allow it to take over high-frequency small decisions within a very clear boundary.

The second category is "authorized within budget" corporate decision-making (also L3, but the boundaries come from corporate management structure).

Companies are accustomed to budget management and hierarchical permissions—some teams have fixed monthly tool budgets, and certain types of purchases can be automatically approved below a certain amount. This structure naturally possesses: goals + budget + authorization boundaries, aligning perfectly with the prerequisites needed for Agentic Payment.

For instance: an Agent responsible for marketing allocation dynamically selects channels and makes payments within budget; an Agent manages internal subscriptions and resource usage to automatically optimize costs. In these scenarios, funds are not subject to transaction-by-transaction approval but rather managed according to strategy and budget. Within this structure, handing over a portion of payment decisions to the Agent is more easily accepted.

The third category is clearly defined tasks and rules for execution payments (a high-certainty version of L3).

The tasks themselves are clear, and payment is merely a part of completing the task. For example, helping users complete travel bookings and making automatic payments within budget, or achieving a specific goal at the lowest cost. In this context, users are more likely to accept "you complete this for me" rather than confirming every step. However, the premise remains: clear budget, clear rules, traceability, and retrievability. It is still a "fenced autonomy," not a completely open one.

Why is it not starting directly from "personal consumption"? Many people believe that the most intuitive scenario for Agentic Payment should be "AI helping me buy things or pay." However, this category may actually take longer: users are more sensitive to spending money, the scenarios are more open, boundaries are challenging to define, decision preferences are more personalized, and once there’s an error, the cost of trust is very high. In personal consumption scenarios, you have to solve not only "can it be done," but also whether users are willing to give up control.

A more realistic path judgment: Agentic Payment is likely to start from L3 scenarios "where the machines are already making decisions + amounts are controllable + boundaries are clear," gradually expanding outwards, rather than immediately entering the completely open consumer world.

7. Many things that seem like Agentic Payment actually aren’t.

Once this concept starts to heat up, a common issue can arise: anything can be included. If AI participates a bit, it seems it can be counted. If there’s a bit more automation, that seems countable too. If there’s some on-chain execution, it appears that it can also be included. But if everything counts, eventually the concept itself will lose its meaning. So rather than continuing to amplify the imagination, it is more important to start discerning what is true.

AI recommendation + human clicking to pay doesn’t count. This is currently the most common type and indeed part of this path. But as long as the final decision of "to pay or not" still rests with humans for final confirmation, it does not yet represent full-fledged Agentic Payment—it is L2, not L3.

Automatic renewals and automatic deductions do not count. The system automatically pays the money, but there are no runtime judgments or understanding of goals involved. Ultimately, it's just humans setting rules in advance and the system executing based on those rules. It addresses the issue of execution automation, not the shift of payment decisions—that's L1.

Automatic execution of smart contracts also does not equal Agentic Payment. On-chain automatic revenue sharing, conditional triggers for settlements, rules are written into the code in advance, and the system executes based on deterministic logic. It can be very complex and verifiable but doesn’t really "understand" the goals and will not reassess whether this money should be paid during runtime. It’s robustly L1, not L3.

A payment interface with some AI also does not count. More intelligent payment assistants or AI interfaces that help you understand bills—these are advances in product experience, but if AI does not truly enter the "payment decision-making + fund execution" loop, it fundamentally remains payment experience optimization.

The real issue is not whether "there is AI," but whether AI has been granted some decision-making power regarding payments during execution.

It is not enough to simply have AI to call it Agentic Payment, nor is it sufficient for a system to automatically pay money to call it that. The truly critical aspect is: in a real payment scenario, does the system participate in the decision of "whether to pay" based on goals, context, and authorized boundaries during execution? If this layer is absent, it remains something else—it could be very important, but it is not the same thing.

8. Rather than jumping to conclusions, it is more important to continue clarifying the problems.

Before writing this article, I initially thought I was organizing a new concept. However, by the end, I increasingly feel that Agentic Payment may not be something already formed but rather a system capability that is being assembled gradually.

Many things are beginning to happen: AI is starting to acquire task execution capabilities, payments are becoming callable infrastructures, and some high-frequency, low-value, clearly defined scenarios are also starting to genuinely need systems to take over a portion of payment decisions.

But at the same time, many boundaries have yet to stabilize. What should count, what should not count. What can be done first, what cannot be done yet. Which scenarios are suitable for handing over to systems, and which are not worth handing over. These questions are still in the process of formation.

Therefore, I don’t want to rush to answer whether Agentic Payment will truly become a definitive direction.

More pressing at this stage is to continue asking under what conditions we would genuinely feel comfortable handing over the act of "spending money" to machines?

Is it when the budget is clear enough? Is it when the authorization boundaries are sufficiently well defined? Is it when risk control and responsibility mechanisms are sufficiently mature? Or is it only when payments themselves have devolved into a form of "low-value yet high-frequency micro decisions" that humanity is truly willing to let go?

If 2026 truly marks the beginning of a new era, it does not mean that Agentic Payment has matured; rather, it suggests that the first batch of genuinely L3 cases is starting to be validated in specific narrow scenarios. It could be on-demand payment for AI development tools, it could be an authorized Agent within a corporate procurement process, or it could be a platform genuinely granting the system the fund execution authority for specific tasks—small in scale, but genuinely executed.

The significance of a new era has never implied that something has become widespread, but instead signifies that it is no longer simply an imagination.

End of article

The content of this article represents personal observations and thoughts and does not constitute any investment or business advice. Readers are encouraged to rationally consider based on their own understanding and information sources.

For Web3 practitioners, the real problem has never been a lack of information, but rather too much noise. Therefore, I want to create a Stablehunter AI that can filter out more important and relevant signals from massive amounts of information. If you would like to apply for product internal testing, please visit Stablehunter.ai or scan the code to apply for internal testing.

Recommended content:

AI × Crypto

Agentic Finance

Stablecoin / Payment

On-chain Finance

Industry Analysis

Field Research

Field Observation | The Seen and Unseen of Stablecoin Payments in Latin America: Who is it Really Used By?

Global Stablecoin Payment Survey: Which Companies Have Already Taken the Lead?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。