Dan Sundheim restructured D1 Capital's short book from 8 names to 40 after being caught in the GME squeeze.

His reasoning was the short opportunity is larger than ever because retail is driving flows with emotions rather than fundamentals, and that inefficiency cuts both ways.

The opportunity is bigger, but so is the squeeze risk on any single name. The solution could be spreading the short leg wide enough that no single squeeze ends the trade.

Most crypto traders are still expressing short views through concentrated single-name positions, despite a market that spent the last year squeezing nearly every obvious fade. The view was often right but the expression was wrong.

A 40% squeeze on a single-name short is a 40% hit to the short leg. The same 40% squeeze inside a 20-name basket is a 2% hit. You could hold the same view and take a fraction of the damage.

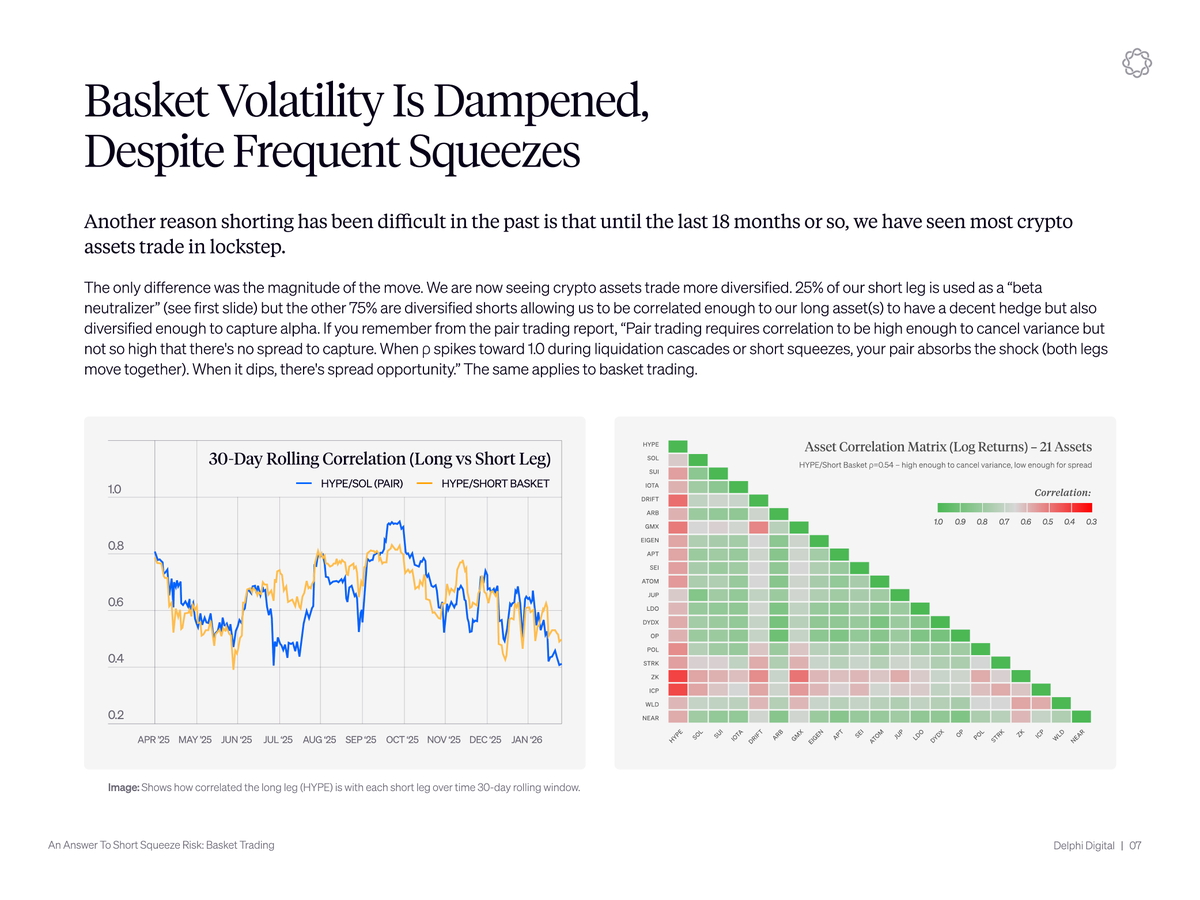

The result is a basket that runs at lower volatility than the HYPE/SOL pair trade, despite every one of its 20 short legs being individually squeezable. Max drawdown compresses to -15% on the basket versus -48% on naked HYPE.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。