Author: Pink Brains

Compiled by: Jiahua, ChainCatcher

Market Landscape

Ask ten cryptocurrency users what digital banking is, and you may get the same answer: a card that lets you spend stablecoins. Ask ten developers, and the answers will quickly diverge. Some are developing non-custodial wallets with Visa payment functionality; others are forking Aave and calling it a savings account; a few are seeking full banking licenses.

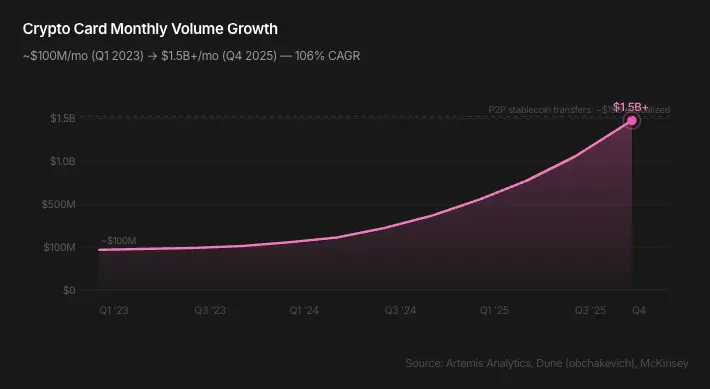

The monthly transaction volume of cryptocurrency cards has grown from around $100 million at the beginning of 2023 to over $1.5 billion by the end of 2025 (a compound annual growth rate of 106%). The current annualized scale of the market has surpassed $18 billion. By 2025, the consumption volume of bank cards linked to stablecoins is expected to reach $4.5 billion, a year-on-year increase of 673%.

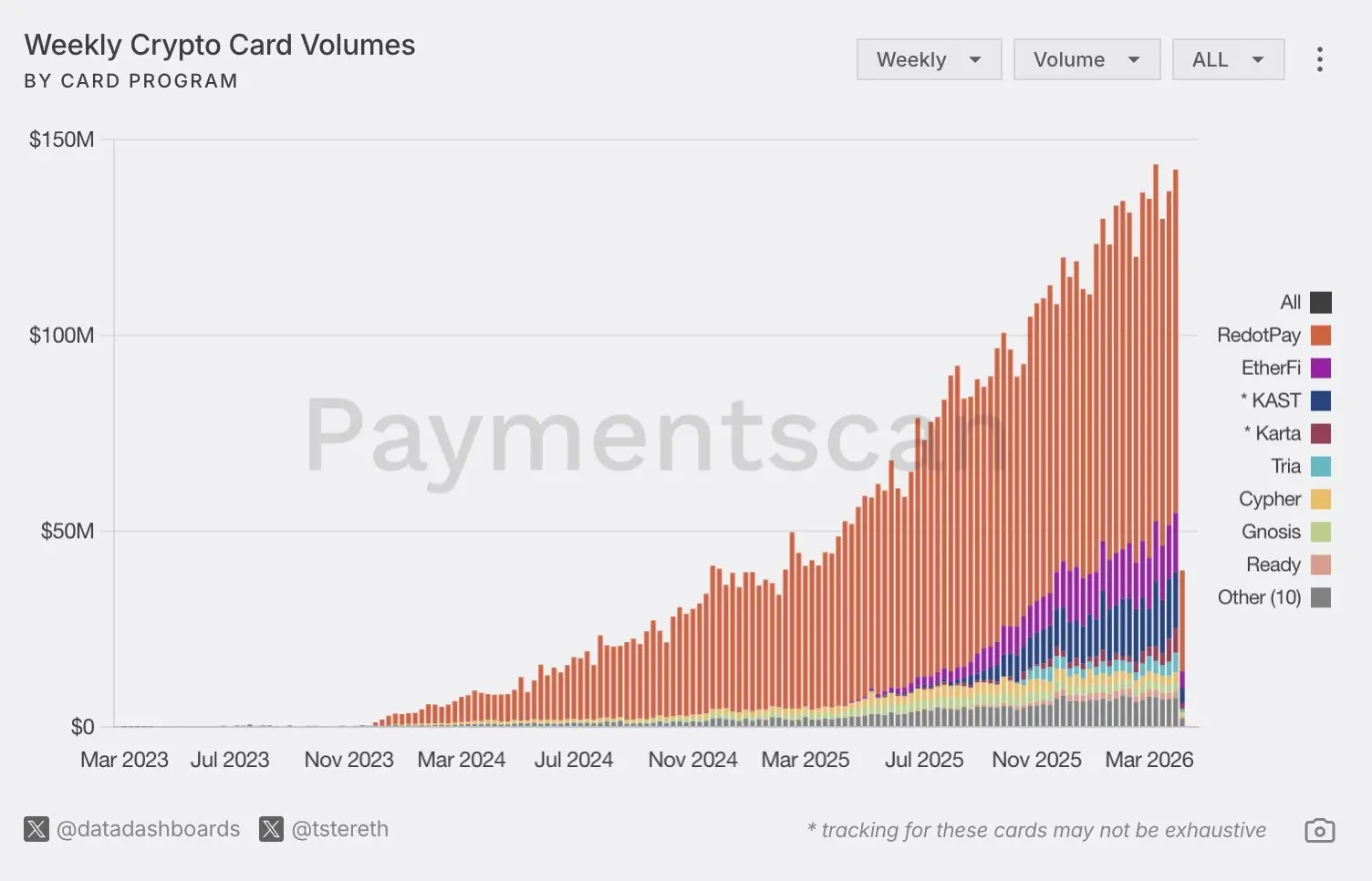

But let's see who is handling this transaction volume. On-chain bank card data shows that a custodial platform based in Asia, RedotPay, dominates 60% of the market share, with transaction volume approximately four times that of the next 13 competitors combined. In contrast, DeFi native, self-custodied digital banks appear to pale in comparison on the transaction volume charts.

However, a deeper story is unfolding with crypto-friendly giants converging. Between December 2025 and March 2026:

- Coinbase applied for a national trust license

- NuBank received conditional OCC (Office of the Comptroller of the Currency) approval for a national bank in the U.S.

- PayPal applied to create PayPal Bank

- Revolut obtained a full banking license in the UK and is seeking a license in the U.S.

- Kraken became the first crypto company to hold a primary account with the Federal Reserve

- 11 companies applied for OCC trust bank licenses in 83 days, including: Circle, Ripple, BitGo, Paxos, Fidelity, Bridge, Crypto.com, Morgan Stanley, Payoneer, Zerohash, Protego

More than 50 crypto digital banks have launched. It is expected that by 2026, the global digital banking market size will reach $552 billion (according to The Business Research Company data).

We are trying to depict the landscape of digital banking—not just who is developing what, but who has an economic model that survives.

Core Conflicts

Two central conflicts shape the competitive landscape of digital banking.

The first conflict is economic. 76% of traditional digital banks are not profitable. Those that have succeeded (Nubank, Revolut, SoFi) do not profit through card spending but through loan books and net interest income. Fees are just the entry point; credit is the real core business.

Now, crypto digital banks are joining the competition with fees and cash rewards, which is exactly the revenue model that led to the failure of the first generation of fintech companies. Stablecoins make things worse: they compress forex profit margins to near zero.

The second conflict concerns user choices. The crypto community praises self-custody, DeFi yields, and non-custodial wallets. But on-chain bank card transaction volumes tell a different story. The vast majority of crypto card spending flows through custodial platforms not because users are unaware of self-custody but because when you just want to buy a cup of coffee, a frictionless onboarding experience outweighs the pursuit of sovereign funds.

History always follows this pattern: just as webmail preceded encrypted email, Dropbox preceded self-hosted storage, and custodial exchanges preceded DeFi dominance—whether crypto digital banking will follow the same trajectory remains an open question.

Four Prototypes of Digital Banks

Instead of dividing them into "Web2 and Web3" (which only reflects technology and offers no insights into business models), a more useful perspective is to examine a digital bank's moat, unit economics, and ceiling.

1. Crypto-Friendly & Banking Business First

The core profit point of a digital bank lies in credit income and traffic conversion, rather than being merely a payment channel.

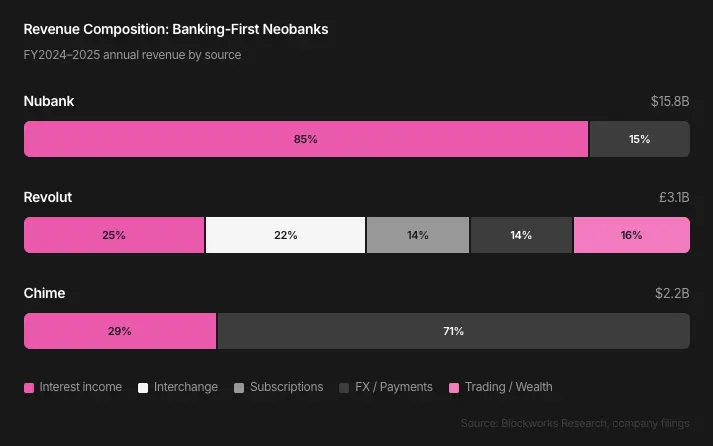

Nubank reported $15.8 billion in revenue for the 2025 fiscal year, with 85% coming from interest income. Credit card interest contributed $4.6 billion, while loan interest contributed $4.8 billion. Monthly revenue per active user reached $15, while service costs were only $0.80, yielding a 19-fold return. SoFi obtained a banking license in 2022, with quarterly net interest income growing from $94.9 million to $617 million over four years, and deposit costs being 181 basis points lower than warehouse financing costs, resulting in annual savings of approximately $680 million. Revolut achieved £3.1 billion in revenue across five business lines in 2024, with no single business line accounting for over 30%, and transaction/wealth business line growth of 298% year-on-year.

Licensed digital banks deliberately restrict stablecoins to the payment domain because loan books are the source of their economic benefits. Revolut has not introduced stablecoin yield; its participation in the UK FCA sandbox test in February 2026 is to use proprietary stablecoins as payment infrastructure, rather than savings products. SoFi's stablecoin (SoFiUSD, launched in December 2025) operates through the Mastercard network as a settlement channel.

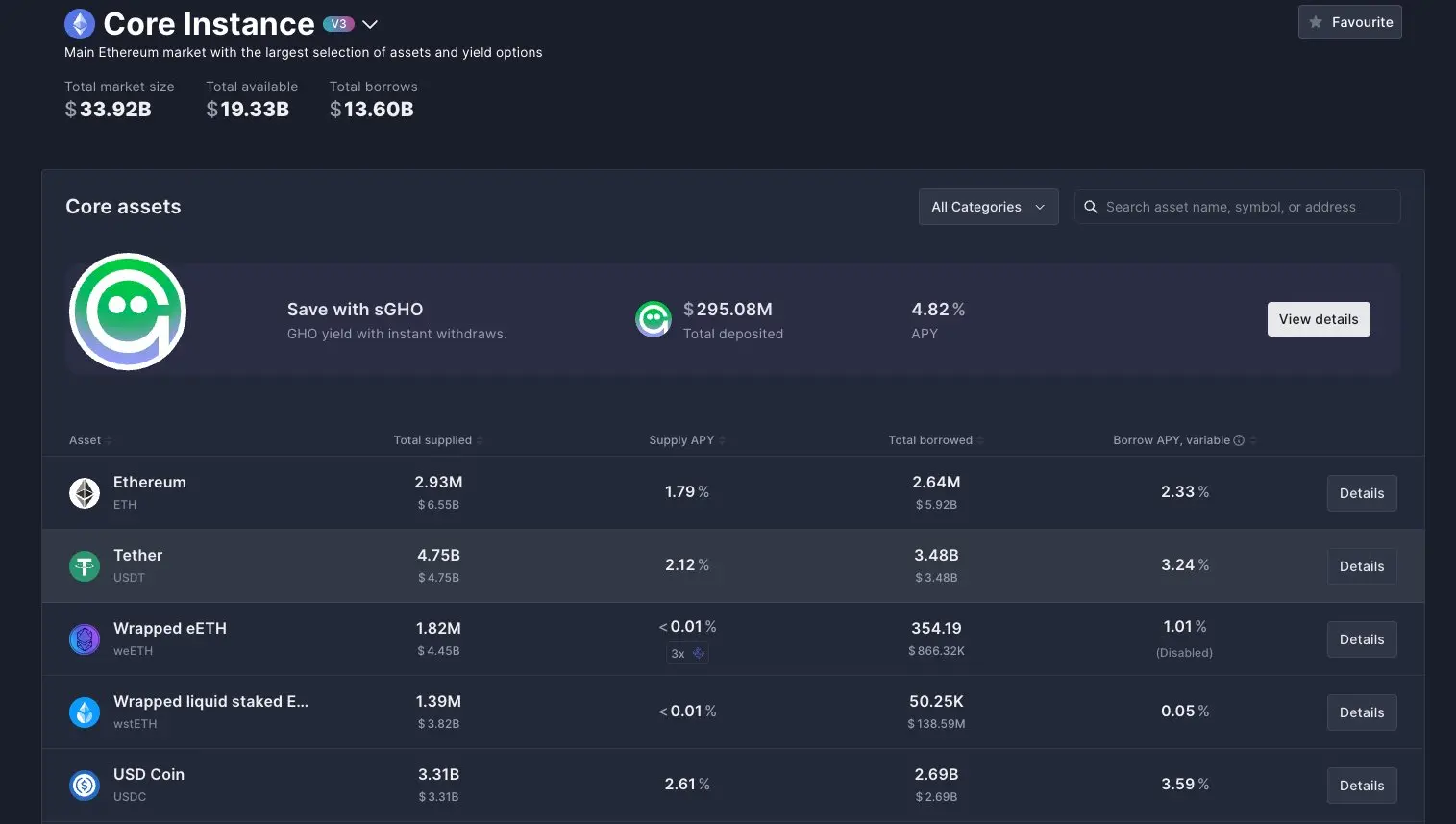

This restraint is built on a specific market condition: on-chain yields currently lack competitiveness. Recent yields for Aave v3's USDC have been about 2.6% APY, lower than SoFi's 3.3% savings APY and Revolut Ultra's 4.25%. However, on-chain yields are cyclical. During periods of active DeFi activity, Aave's USDC reached 8-10%, and Ethena's rate driven by funding costs was even higher. This gap is cyclical; when it widens again, the competitive dynamics will change accordingly.

This restraint is built on a specific market condition: on-chain yields currently lack competitiveness. Recent yields for Aave v3's USDC have been about 2.6% APY, lower than SoFi's 3.3% savings APY and Revolut Ultra's 4.25%. However, on-chain yields are cyclical. During periods of active DeFi activity, Aave's USDC reached 8-10%, and Ethena's rate driven by funding costs was even higher. This gap is cyclical; when it widens again, the competitive dynamics will change accordingly.

2. Commercial and Social Super Apps

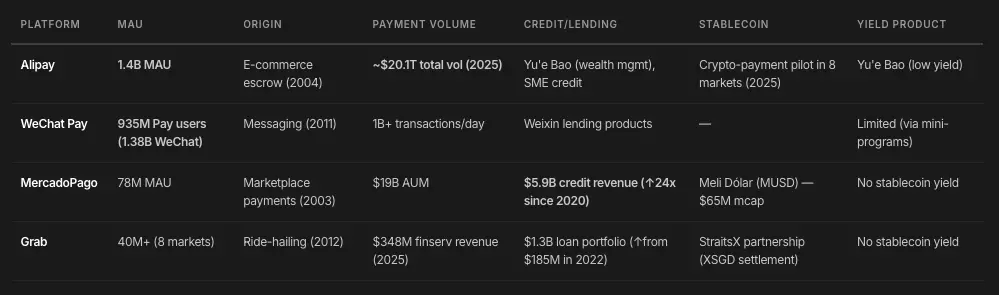

MercadoPago, Grab, WeChat, Alipay. They did not initially intend to establish banks but integrated finance into business applications. The moat is not the product itself but the distribution channels and behavioral data—enabling them to conduct credit assessments more accurately than any bank.

MercadoPago's credit revenue grew from $246 million in 2020 to $5.9 billion in 2025, a 24-fold increase in five years. Grab's loan portfolio grew from $185 million in 2022 to $1.3 billion by the end of 2025, with financial service revenue reaching $348 million in the 2025 fiscal year.

Both have explored stablecoins. MercadoPago launched Meli Dólar (MUSD) in Brazil, expanding to Chile and Mexico, but MUSD's circulating market cap is only $65 million, less than 0.4% of its $19 billion AUM. Grab partnered with StraitsX for stablecoin settlements, allowing visitors to settle Singapore dollars instantly using the XSGD stablecoin at GrabPay merchants.

Neither has explored stablecoin yields. This is a breakthrough for crypto-native players and the most underestimated gap in this field.

Whop is worth noting here. It is currently not a digital bank but a creator marketplace. However, after Tether invested $200 million (valued at $1.6 billion), creators can accept USDT, hold stablecoins, and settle without a bank. The integration with Aave provides stablecoin yields catering to 18.4 million users and $3 billion in annual creator income. MercadoPago was also not a digital bank in 2003, just a third-party guarantee for the marketplace—financial relationships came with business. Whop is currently at that same starting point, and it is built on a crypto network from day one.

The implication for card-centric digital banks is that the most sustainable financial relationships may not begin with finance at all, but with e-commerce.

3. Transaction Focused

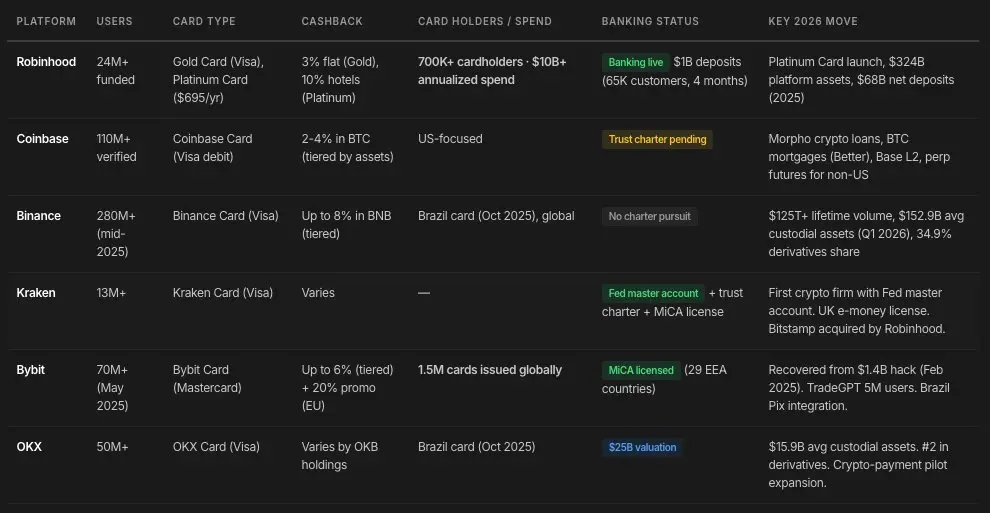

Robinhood, Coinbase, Binance, Kraken, Bybit, OKX—starting with centralized cryptocurrency trading and expanding into crypto banking. Each platform in this group is explicitly building a banking layer to generate income without relying on bull markets.

Robinhood is the most complete embodiment: the platform's total assets grew approximately 70% year-on-year to $324 billion, with net deposits reaching a record $68 billion. Coinbase is aggressively entering the digital banking sector: its own L2 blockchain (Base), a wallet with card functionality, cryptocurrency-backed loans based on Morpho, Bitcoin mortgages in partnership with Better, and an application for a trust license under review. Kraken holds both a trust license and a Federal Reserve primary account.

These platforms start with transaction income that already possess scale effects and layer their banking services on top. In contrast, stablecoin digital banks do the opposite: starting with meager fees, hoping to layer everything on top of that—which is much more difficult.

4. Stablecoin Priority (Crypto Native)

Ether.fi, Gnosis Pay, RedotPay, KAST, Holyheld, Bleap, Ready, Tria, Cypher, Payy, and dozens more. These platforms leverage the low operational costs of stablecoins and the composability of DeFi as backend product infrastructure. Their value proposition is clear: self-custody; DeFi yields (5-15% APY in active markets, traditional savings at 3-4%); near-instant cross-border payments based on stablecoins at very low forex costs; and global portability without geographic restrictions.

Stablecoin priority digital banks have the most obvious structural advantages in emerging markets and cross-border use cases. But weaknesses are also very real: no one has achieved breakthroughs in scaling unsecured loans; they compete on the thinnest profit layer (fees) while subsidizing user acquisition with token-funded cash rewards; stablecoins worsen the situation by compressing foreign exchange profits and settlement costs to near zero, eroding the sources of income that kept early digital banks alive.

Infrastructure

Most crypto digital banks are just front ends built on shared infrastructure. Understanding this tech stack is crucial for assessing their moat.

Bank card networks (Visa, Mastercard): although the number of projects is nearly equal (over 130 each), Visa captures more than 90% of on-chain bank card transaction volumes through early partnerships with crypto-native infrastructure providers. This is a single point of failure risk for the entire industry—if Visa changes its crypto project policies, slows down its expansion, or raises rates, the economic equations of the entire industry could change overnight.

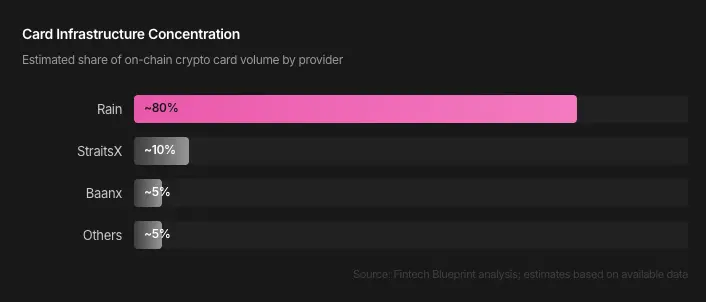

Issuing institutions (Rain, Reap, Baanx, StraitsX): a regulated bridge between the on-chain world and traditional finance. The most important structural development is the emergence of full-stack issuers—these companies hold primary memberships with Visa/Mastercard directly, bypassing traditional sponsoring banks.

Most crypto digital banks share the same backend. Rain supports Ether.fi, RedotPay, and Avalanche Card. If Rain encounters technical failures, regulatory issues, or strategic shifts, the entire industry will be impacted. A report by Solus Partners analyzing 19 platforms indicates that infrastructure concentration and vendor dependency pose systemic risks—this is the Synapse risk of crypto digital banks.

(Note: Synapse is a U.S. fintech infrastructure company that filed for bankruptcy in 2024 due to issues with segregated funds, freezing user funds from dozens of partnering platforms reliant on its services, serving as a landmark warning case for the risks of infrastructure concentration in the industry.)

The Threat of Wallet-Native Stablecoins

A frequently overlooked competitive dynamic: major wallet providers are issuing their own stablecoins specifically for funding card purchases, constructing closed-loop ecosystems to capture value that would otherwise be earned by independent digital banks.

By the end of Q3 2025, MetaMask launched mUSD, and Phantom launched CASH, both designed as funding mechanisms for their respective debit card products. These wallets do not rely on users holding USDC or USDT but construct a closed loop—users convert their assets to the wallet-native stablecoins to pay for card transactions. Early data shows sharply differing trajectories: Phantom's CASH steadily grew from about $25 million in September to approximately $100 million by late December; MetaMask's mUSD peaked at nearly $100 million in early October before declining to around $25 million, a drop of 75%.

If wallets successfully make their native stablecoins the default funding source, channel fees, forex spreads, and reserves earnings will be retained by the wallet platforms themselves. MetaMask, Phantom, and Coinbase Wallet already have user relationships—adding digital banking functionalities is an extension of their product line, not a new product. Independent crypto digital banks may thus lose a significant portion of their value proposition.

Economic Dilemma

76% of traditional digital banks are unprofitable. Crypto-native digital banks inherit the same broken model—and stablecoins make matters worse, not better. The lessons from bank-preference players are clear: payments are just a distribution channel, not the core business. The 85% share of interest income in Nubank proves this; the net interest margin (NIM) expansion driven by SoFi's licenses demonstrates it. Treating card spending as the core revenue engine of crypto digital banks is akin to building on sand.

A sustainable model is to use bank cards as a channel to acquire users while monetizing through higher-margin on-chain finance: DeFi yields, exchange transactions, structured products, and lending.

Five Game-Changing Developments

1. On-Chain Credit Scoring

In the crypto world, a wallet's transaction history, DeFi usage patterns, repayment behavior on loan protocols, staking duration, trading frequency, and protocol diversity can all serve as inputs for credit assessments. No crypto digital bank has achieved this on a large scale yet. Those who can crack this will essentially replicate Nubank's strategy on a permissionless, on-chain infrastructure.

2. Crypto-Native Enterprises Obtaining Full Banking Licenses

Not trust licenses (limited to custody) but full licenses that allow for deposits and loans. This would enable crypto-native businesses to build loan books funded by stablecoin deposits at a lower cost than warehouse financing facilities.

3. Regulatory Clarification of Yield Legality

The regulatory direction in major markets is consistent: issuers of stablecoins are not allowed to pay yields. Both the U.S. and Europe have clearly defined this red line, and major Asian markets like Japan, Singapore, and Hong Kong have also taken similar conservative stances.

4. Agent-Driven Finance

AI agents execute financial operations on behalf of users—rebalancing portfolios, optimizing yields, managing payments, executing cross-protocol strategies. Mastercard had six crypto partners in 2024, which expanded to over 25 by 2025. Visa launched Smart Commerce Connect, allowing AI agents to shop on behalf of users at global merchants. Whoever can build the best agent infrastructure on top of the stablecoin network will capture the next wave of traffic in e-commerce.

5. Making On-Chain Operations Seamless

Crypto digital banks still rely on card networks, but the payment terminal technologies that bypass them already exist: QR code payments for stablecoin settlements, NFC touch payments without the intervention of Apple Pay or Google Pay, and on-chain settlement for physical card transactions. Projects like OpenPasskey (built on Base) are proving this path viable: having its own IIN issued by ISO, P-256 cryptography, and fully non-custodial crypto cards—three payment methods without Visa and without banks.

Who Will Win?

We do not know yet. But the key variables determining victory and defeat are already set in motion.

Licensed digital banks have proven their economic models, and in markets where loans drive user relationships, which is most developed countries, they hold the advantage. Stablecoin-priority digital banks provide globally portable dollars, local stablecoins for emerging markets, access to DeFi yields, and retroactive rewards, but current data shows users still prefer simplicity and ease of use over crypto-native ideals. Participants embedded in commerce may possess the deepest moats because they already control distribution channels—but overlaying crypto functionalities on top of mature infrastructure is costly, requires user education, and heavily relies on regulatory clarity.

The value captured by the infrastructure layer (issuing institutions, custody, fiat deposits and withdrawals, core banking systems, blockchain settlements, KYC/AML) will inevitably exceed that of any consumer brand. Over 40 stablecoin cards are competing on token-subsidized cash back without a real business moat, sharing the same set of infrastructure—most of which will not survive the next two years.

The landscape of crypto digital banking is at a turning point.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。