Author: Jae, PANews

When Aave faced a $10 billion withdrawal, Spark caught the massive liquidity.

The on-chain disaster triggered by Kelp DAO and LayzerZero's cross-chain vulnerability tore the DeFi lending market into two clearly defined worlds.

The "toxic" asset rsETH flooded into Aave, causing it to incur approximately $200 million in bad debts, leading to network-wide liquidity exhaustion and $10 billion fleeing in panic.

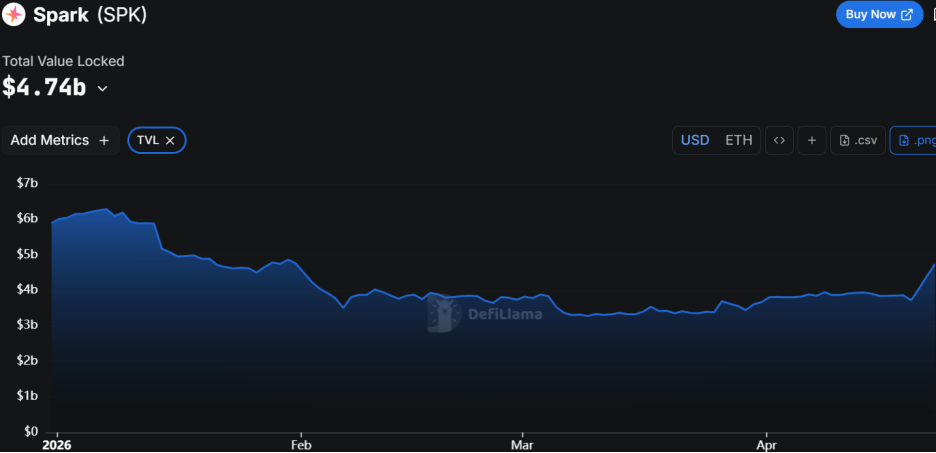

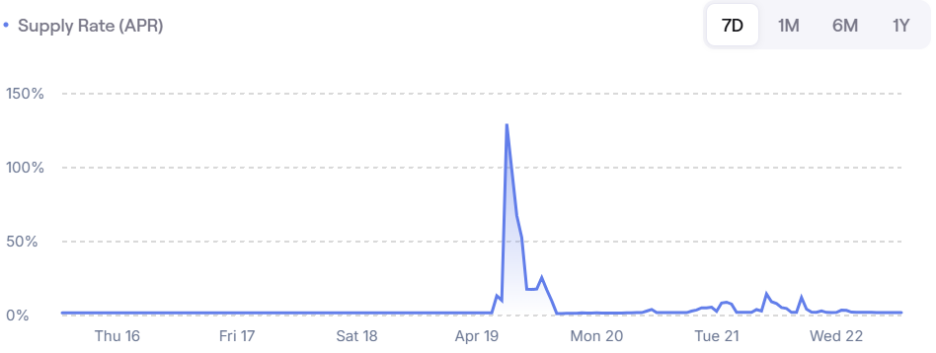

However, amidst the chaos, another lending protocol giant, Spark, welcomed its shining moment. TVL (Total Value Locked) skyrocketed by $1.3 billion, with ETH deposit rates once surging to 130%, becoming the preferred safe haven for whales to transfer assets.

A black swan event reassessed the rightful owner of the DeFi Iron Throne.

Aave Liquidity Crisis, Spark Seizes Opportunity to Attract $1.3 Billion

With the cross-chain bridge of rsETH broken, the entire Aave lending market was directly put on pause.

Hackers used illegally minted rsETH to borrow large amounts of WETH from Aave, draining clean assets and leaving a pool of bad debts.

For further reading: KelpDAO Cross-Chain Disaster, AAVE Becomes the "Payer," Industry Calls for Risk Repricing

Panic spread like a virus: in just over three days, Aave already lost $15.1 billion, with total deposits dropping from $48.5 billion to $30.7 billion, about one-third of the funds fleeing; WETH utilization rates across multiple chains reached 100%; depositors could not withdraw, and liquidators had no money to borrow.

The most notable operation came from Justin Sun, who quickly withdrew 65,584 ETH from Aave, worth approximately $154 million.

This "withdraw first, ask questions later" behavior created a herd effect in the market. For investors, the annualized yield, no matter how high, could not offset the panic of being unable to withdraw the principal.

As Aave became a liquidity outlet for hackers, Spark became a lifeline for users.

Spark's TVL not only did not fall but instead increased by $1.3 billion, reaching a total scale of $4.74 billion. This money represents a trust vote cast by the market with real capital.

Due to a surge in borrowing demand into Spark, combined with a significant scarcity of liquidity, the ETH deposit rates on Spark experienced a spectacular spike, reaching an annualized level of 130%, which directly reflected the extremely high premium on safe assets.

Spark's ability to absorb this wave of demand is attributed to its unique ecological structure. Unlike Aave, it is the lending engine of the Sky ecosystem, backed by a large reserve of USDS. As Sky's liquidity outpost, Spark not only relies on external deposits but can also obtain stablecoin supplies directly through Sky's credit lines.

This "central bank-level" liquidity support allows it to maintain an uninterrupted withdrawal channel even during market shocks.

Abandoning the Vanity of TVL, Spark Moves to Remove rsETH

Spark dodged the rsETH disaster thanks to a counter-cyclical decision made three months ago.

Different fates on the same day. On January 29, the two major lending platforms operated on the logic of re-collateralizing liquidity (LRT) in opposite directions.

Aave went all out. The protocol officially launched rsETH E-Mode, allowing users to leverage borrow at a high collateral rate (LTV) of 93%. Aave's goal was to attract an expected $1 billion in rsETH inflow to restore the utilization rate of WETH and sprint for TVL and revenue.

Spark chose a cautious retreat. The protocol completely stopped new supplies of rsETH through governance operations and began to gradually remove it from the asset list.

Spark's move sparked strong dissatisfaction among users of ETH recycled leverage, who typically used staking assets like stETH or rsETH to capture arbitrage, and Spark's removal forced them to migrate their positions, most of which flowed to Aave, which had more relaxed policies and lower rates.

At that time, the community questioned Spark's team as being "too conservative" or "abandoning growth." No one anticipated that this step might save the entire protocol later on.

In hindsight, Spark's strategic director monetsupply.eth pointed out that the decision to remove rsETH was based on a safety-oriented tightening mechanism.

- Marginal Cost vs Marginal Benefit: If the cost of maintaining a certain asset exceeds its risk-adjusted return to the protocol, such assets will be cleaned up;

- Risk Exposure Concentration: The utilization rate of rsETH on Spark was extremely low, almost monopolized by the same wallet address, making the risk difficult to disperse;

- User Preference Survey: The only whale user of rsETH expressed a willingness to actively migrate to more mature collaterals like wstETH or weETH, providing the protocol with an opportunity to smoothly clean up assets.

It is this "not blindly pursuing TVL" decision transparency and discipline that allowed Spark to avoid all potential losses that could arise from hackers exploiting rsETH.

Multi-layer Risk Control System: Rate Limits + Interest Rate Buffers + Isolated Architecture

PANews believes that even if rsETH had not been removed, Spark's architecture would still be sufficient to resist such risks. Compared to Aave, which pursued capital efficiency at the expense of safety redundancy, Spark has built a multi-layered deep defense system.

Spark implemented strict deposit and borrowing rate limits (Rate-Limited Caps), where the amount deposited and borrowed grows sequentially within a fixed time. Even if rsETH had not been removed, attackers would not have been able to deposit $290 million worth of collateral all at once like they did on Aave. This design forces limits on the maximum risk exposure of a single event and hard caps losses to bearable levels.

Spark maintains a relatively high interest rate cap over the long term. Under stable market conditions, higher borrowing rates discourage over-borrowing (if borrowing is expensive, people won’t borrow), while on the other hand, attract more people to save (those saving earn more). The result is that liquidity is always available in the pool, preventing it from being "exhausted" and making it impossible for everyone to withdraw when they want. Especially during market downturns, it won't be subject to a run due to liquidity exhaustion.

As the utilization rate of the funding pool rises, Spark's interest rate curve slope will be steeper than Aave's, leading to two significant consequences:

Forced De-leveraging: High interest costs will compel borrowers to actively seek liquidity to repay loans.

Attracting Supplemental Liquidity: High annualized deposit yields will quickly attract external arbitrage capital, unlocking the deadlock of 100% utilization.

Spark's modular isolated architecture has strong controllability over risk management. When dealing with high-risk synthetic assets like USDe, Spark also adopts a prudent attitude, isolating them in specific primary risk pools, ensuring that even if a particular segmented asset has problems, it will not affect the main lending pool on the platform.

The massive migration of liquidity from Aave to Spark signifies a shift in risk preferences from pursuing yield to seeking safety and stability.

Aave's $10 billion outflow has sounded the alarm for all protocols pursuing high capital efficiency. In situations where safety margins are compromised, even the tiniest external related risk can evolve into a systemic dilemma for the protocol.

Spark's rise proves that in uncertain market environments, cautious risk governance decisions and the implementation of a "risk-first" strategy is the more valuable long-term moat.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。