From Google to Stripe: Who Will Win the AI Agent Payment Standards Battle?

Written by: Tiger, Research

Translated by: AididiaoJP, Foresigh News

In the past year, global tech giants, card issuers, and exchanges have all unveiled their own Agent payment standards (hereinafter referred to as "Agent"). In 2025 alone, eight standard agreements have been released, with collaboration announcements still ongoing.

At a crucial moment of structural change, capturing payment standards carries the most weight. During the era of offline commerce, Visa and Mastercard locked in card payment standards and dominated the market. Every subsequent card transaction was routed through their networks.

As commerce shifted online, a new batch of players emerged. PayPal built its online payment service based on email-based remittances, followed by Stripe. The next payment market is Agent. With AI entering the mainstream, there is no doubt that the era of Agents is approaching.

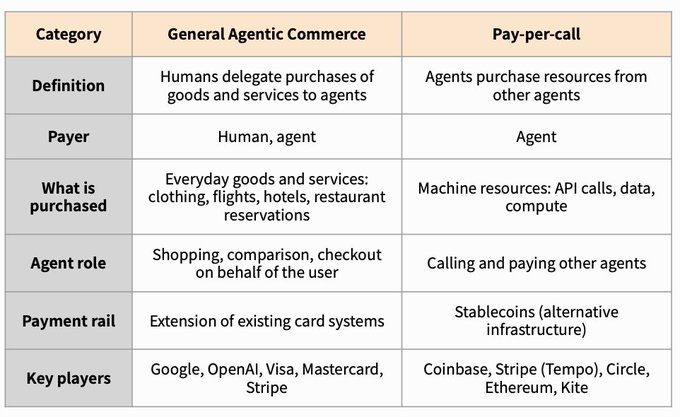

When people imagine AI Agent payments, two scenarios typically come to mind: one where the Agent finds and purchases products on behalf of the user, and another where Agents transact directly without human intervention.

The former is the nearer future, while the latter is more distant. Agents executing orders under user directives belong to "General Agentic Commerce," a field that is already taking shape. Direct payments between Agents fall under "Pay-per-call," which is a more remote future state.

These two categories seem opposed but are, in fact, different players tackling different problems. This report will examine how various groups of players establish standards within these two categories of the Agent payment industry.

General Agentic Commerce

In General Agentic Commerce, humans entrust shopping tasks to Agents. Within a given platform, users register a card and set the parameters of their delegation, after which the Agent performs actions within that platform.

For example, a user tells the Agent: "Prepare for my business trip to Tokyo next week, with a budget of 2 million won (approximately 1400 US dollars)." This single instruction grants the Agent conditional payment authority. Within the budget, the Agent will sequentially select and pay for flights, hotels, airport transfers, currency exchange, and travel insurance, using the user's card to complete the transactions.

To achieve this process, the Agent must first understand the user's intent and find suitable products, then securely complete the payment. The structure is divided into two layers:

- Discovery layer: Agents search for products on the platform on behalf of the user

- Payment layer: Agents complete payments within the parameters set by the user

Some leading players focus on a single layer, while others attempt to capture both layers simultaneously.

Alphabet Inc. (GOOG)

Core Technology

@Google is trying to capture both the discovery layer and the payment layer, focusing on two standards: UCP and AP2.

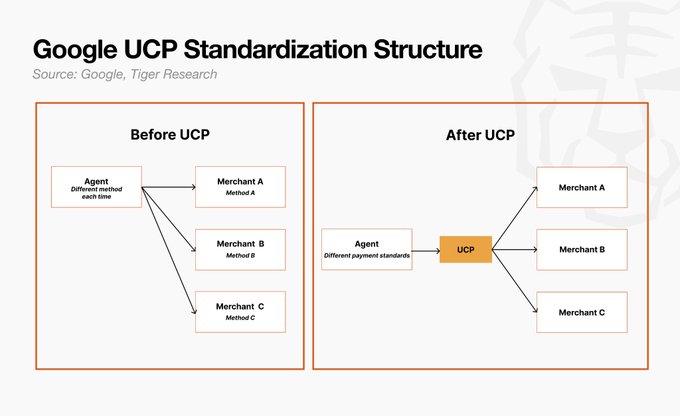

UCP (Universal Commerce Protocol) is the standard that specifies how Agents communicate with merchants.

For an Agent to complete shopping on behalf of the user, it must interact countless times with different services. The problem is that the structures of each service vary. Every time an Agent discovers a new service and initiates a transaction, integration needs to be done separately. Google hopes to eliminate this inefficiency through UCP.

Once merchants are configured according to the standard, any Agent can thereafter connect with that merchant in the same way.

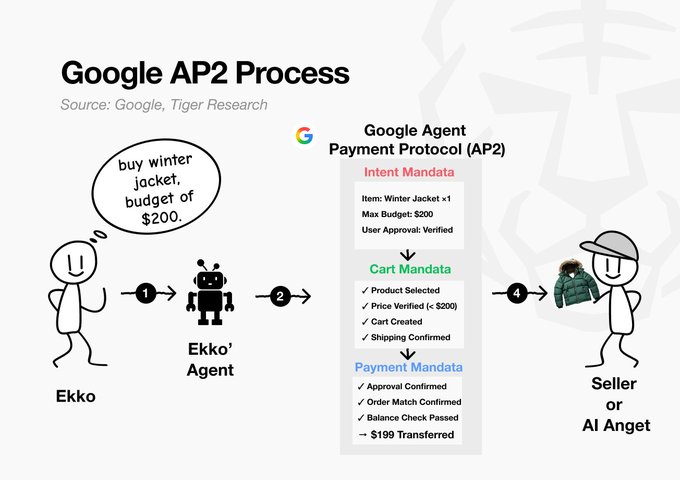

AP2 (Agent Payments Protocol) is the authoritative standard that ensures "who authorized what, and what the authorization limit is," occurring at the moment from discovery to payment.

When a person directly presses the payment button, the subject of action and responsibility are clear. When an Agent pays on behalf of the user, the boundaries of authorization and responsibility become vague. AP2 records the user's initial instruction as an immutable digital contract (Mandate). Agents can only act within the scope of the user's instructions, and after the transaction is completed, a traceable record is left showing who authorized what at what time.

In short, if UCP is the standard for discovery, then AP2 is the standard for writing responsibility into transactions.

Core Business

Google’s current revenue relies on two pillars: advertising and cloud services. In 2025, advertising revenue is projected at 262.7 billion USD, and cloud services revenue at 58 billion USD, making up a large portion of total revenue of about 400 billion USD.

The issue is that the landscape is changing. As consumers start delegating purchases to AI Agents instead of entering keywords into the search bar, the existing search advertising model is under threat. Google's investment in UCP and AP2 begins from here. It is preparing for the next step.

Google is evolving its AI Mode to be the next stage of search. Starting from the initial Q&A layer, it will gradually transform into an Agent that executes purchases on behalf of the user. Once merchants join UCP and list products, these products will become tradable within the Agents' reach.

Advertising: Advertising shifts from the discovery phase to the recommendation phase. Agents compare products based on user criteria and filter them; paying merchants appear at the forefront. It looks like a natural recommendation, but ads are now positioned in the recommendation phase. Advertisers spend less in the non-conversion phase; Google captures higher ad prices with each transaction.

Payments: The AP2-based Agentic Checkout completes payments with just one user approval. Google Pay becomes the payment channel, charging fees per transaction. Agent transactions are faster and more frequent than those by humans. Small fees compound at scale.

Cloud Services: A possibility that is not yet a revenue line. Merchants handling Agent transactions require AI reasoning, data storage, and API integration. If this demand flows to Google Cloud, cloud service revenue will grow in sync with the Agent ecosystem.

Outlook

Google’s differentiated advantage lies in its existing network.

Google led the internet age and now operates nearly complete payment infrastructure, including Google Pay and a vast merchant base. In the AI era, the company is at the forefront with Gemini, showing a high sensitivity to technological change. User touchpoints through Android and Chrome are already in place.

If UCP and AP2 establish a strong foothold, users will complete end-to-end purchases within Google’s infrastructure. Merchants will naturally join Google’s infrastructure. The existing systems are built around humans, while UCP and AP2 are designed for Agents. Merchants that fail to board the train will be at a competitive disadvantage against those that have.

For merchants, reaching buyers by joining UCP and AP2 represents the path of least resistance.

Google has done similar things before. In 2008, it open-sourced Android. Manufacturers joined, user numbers grew, and Google’s infrastructure such as Play Store and Google Pay followed. The result: Google became the largest beneficiary of the mobile market without producing a single phone.

Once Agent transactions truly form, Google is very likely to walk the same road again. Buyers and merchants move on its infrastructure, and Google can capture revenue at every stage of the transaction.

OpenAI Group PBC

Core Technology

@OpenAI developed ACP (Agentic Commerce Protocol) in partnership with Stripe, launching it on September 29, 2025.

ACP is an open-source protocol that allows Agents to call merchants' payment systems and purchase products on behalf of users. ACP grants permission through a four-party structure:

- Buyer

- Seller

- Agent

- Payment Provider

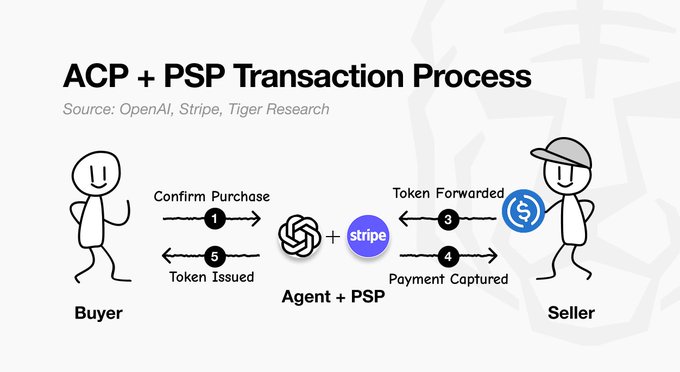

The core question of ACP is, "How much payment authority should be granted to Agents?" Directly giving the Agent the user's card information theoretically allows the Agent to pay at any merchant, any amount, at any time. However, insufficiently trained Agents may repeatedly purchase unnecessary items, and hijacked sessions may also be exploited.

ACP resolves this issue through Delegate Payment. The user's actual card information is never transmitted to the Agent. Instead, the PSP (e.g., Stripe) receives the card information and issues a one-time token, which the Agent only processes. This token carries four constraints:

- Which merchant it can be used at

- The maximum amount it can pay

- When it expires

- Which checkout session it is applicable to

Therefore, even if an Agent malfunctions or is hijacked, the damage cannot exceed "this single shopping transaction."

Core Business

OpenAI's current revenue comes from three major pillars. In 2025, annual recurring revenue (ARR) is around 20 billion USD, with ChatGPT subscription revenue accounting for approximately 85%. The rest comes from API usage fees and enterprise contracts. This is a subscription model that grows linearly with the number of users.

The problem is that the growth ceiling of this structure is becoming clear. As long as OpenAI competes for subscriptions with Claude and Gemini, growth is tied to how many new users it can attract. ACP is an attempt to break through this ceiling. It layers transaction fees on top of subscription fees. It adds transaction volume on top of user numbers. It adds growth on top of growth.

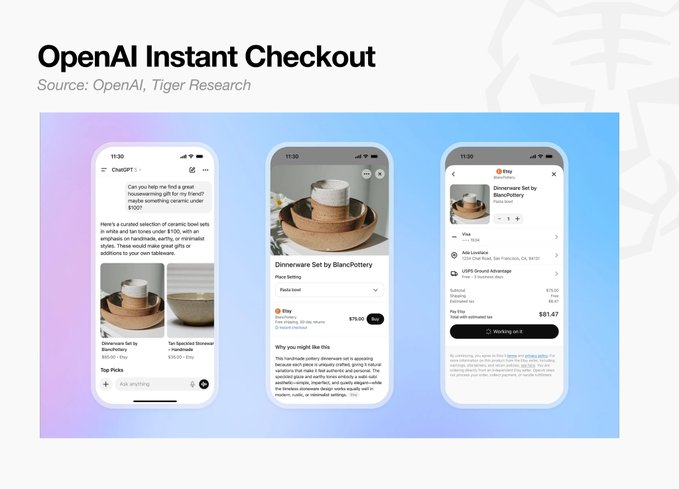

In September 2025, OpenAI launched Instant Checkout, completing payments within ChatGPT. It charged a 4% transaction fee to Shopify merchants. However, lack of real-time inventory synchronization, tax processing infrastructure, and low conversion rates hampered progress.

Merchants strongly opposed it, pointing out that directly handling complex variables like inventory status, tax processing, and price updates through ChatGPT was very challenging. Walmart specifically disclosed that the conversion rate through ChatGPT was only one-third of its official website.

OpenAI ultimately took down Instant Checkout in March 2026, returning payment to merchant applications and systems, while limiting ChatGPT's role to product discovery.

This was an adjustment, not a retreat. The acquisition of personal finance app Hiro Finance is expected to play a key role in this adjustment. The plan is to upgrade consumption pattern analysis, financial data management, and the inventory, tax, and fraud detection infrastructure that previously hampered Instant Checkout, and then re-enter the market with its own payment capabilities.

Once this ecosystem is in place, OpenAI will have achieved its original goal: ChatGPT mastering the starting point of every transaction, opening the door to a commission-based model.

Outlook

OpenAI's success depends on its ability to meet the needs of both merchants and buyers simultaneously. On the merchant side, cases like Walmart that integrate interests and payments deeply into ChatGPT must continue to increase. On the consumer side, ChatGPT's recommendations must convert into actual purchases. If one side fails, the other will stagnate. If there are too few merchants, product selection will diminish; if conversion rates are low, merchants will withdraw their investments.

OpenAI does not have the luxury, like Google, to buy time with other assets.

Ultimately, whether OpenAI can take the lead in shopping initiation depends on whether ChatGPT can replace the beginning of shopping like it did for search. As Google enters the same race with Gemini, this will be OpenAI's toughest battle.

Visa Inc. (V)

Core Technology

@Visa is a company determined to maintain its status as "the most widely used payment method," even in the era of Agents. To prepare for Agent payments, Visa has opted to open its existing payment network to Agents.

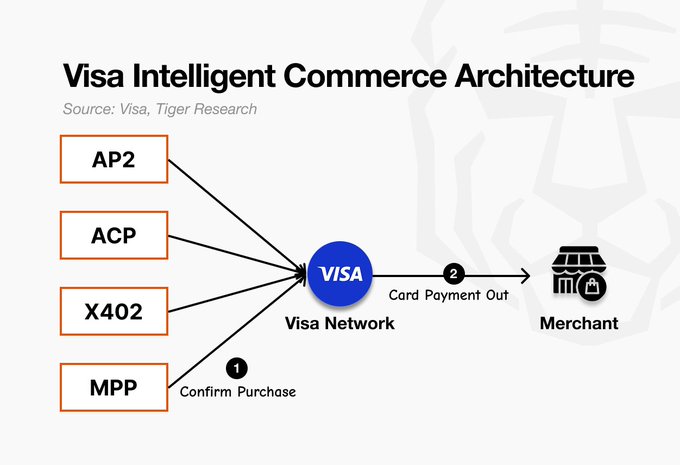

In April 2025, Visa launched the Visa Intelligent Commerce product suite. Visa Intelligent Commerce consists of four components that allow Agents to complete payments like humans.

The commonality among the four components is that Visa is not directly participating in the protocol race.

Agent APIs are Visa's own technology, activated when using Visa cards. Intelligent Commerce Connect is a strategy to accept competitive protocols.

Core Business

Visa’s current revenue comes from card payment fees. In 2025, revenue is projected at about 40 billion USD, with an annual transaction volume of 14 trillion USD. Visa Intelligent Commerce has not yet generated separate revenue. It serves as a strategic foundation built to preserve existing revenue structures when the Agent commerce era arrives.

The revenue paths remain unchanged.

First is payment fees. Whether an Agent presses the payment button on behalf of the user or a human operates directly, it makes no difference to Visa. As long as payments go through the Visa network, card fees will be generated. This is why Visa designed Intelligent Commerce Connect to accept competitive protocols.

No matter which protocol the transaction runs under, as long as payment is made with a Visa card, fees will be incurred.

Second are token infrastructure fees. Each time an AI-specific token issued by Tokenization (one of the five Agent APIs) is used for a transaction, Visa is responsible for credential conversion and authentication. When PSPs and AI platforms like Stripe use this token service, Visa charges network usage fees. The token layer built on cards becomes the new revenue axis in the Agent era.

Ultimately, Visa's strategy is not to win the protocol race but to charge fees to both winners and losers. On the buyer side, AI platforms like OpenAI, Anthropic, and Perplexity have lined up as partners. On the seller side, e-commerce platforms like Shopify and PSPs like Stripe are in place. Regardless of which direction Agent transactions grow, Visa sits at both ends.

Outlook

Visa's outlook can be summarized in one sentence: rather than competing with its own protocol, it aims to be the payment infrastructure that accepts all protocols.

This choice is significant, as Visa's positioning is fundamentally different from other players. Google, OpenAI, and Coinbase are all playing the game of "our own protocol must win." AP2, ACP, or x402 must become the standard of their respective ecosystems to maximize revenues. The protocol war itself is close to a zero-sum game.

In contrast, the game Visa plays is: whichever protocol wins, as long as payments go through its network, it can profit. For Visa, the winner of the protocol war does not matter. It attaches to the winning side to charge fees and can continue to charge even if the market shifts to other protocols.

This acceptance strategy is not a "concession" but is Visa's most advantageous position, a choice unique to Visa owing to its ownership of 4.8 billion cards and 150 million merchant assets.

However, there is one variable: stablecoins. If payments between Agents completely bypass the Visa network and settle directly on the blockchain, Visa will lose that layer of fees. Visa's acquisition of Bridge, introduction of stablecoin cards, and role as a validator for the stablecoin-specific chain Tempo are all responses to this risk.

For the acceptance strategy to work, payments must go through Visa’s infrastructure at some point. Stablecoins are the only path that could threaten this premise itself.

Mastercard Incorporated (MA)

Core Technology

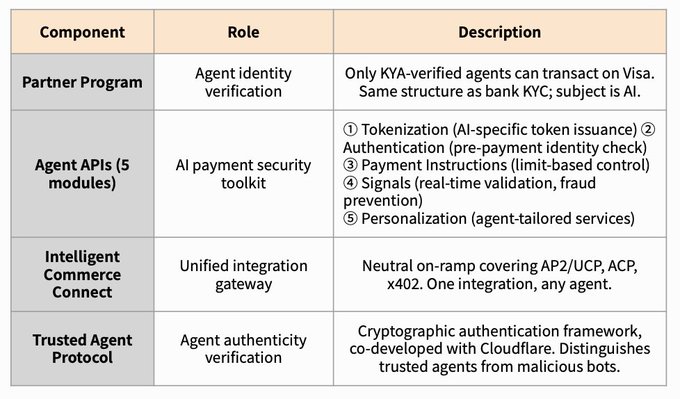

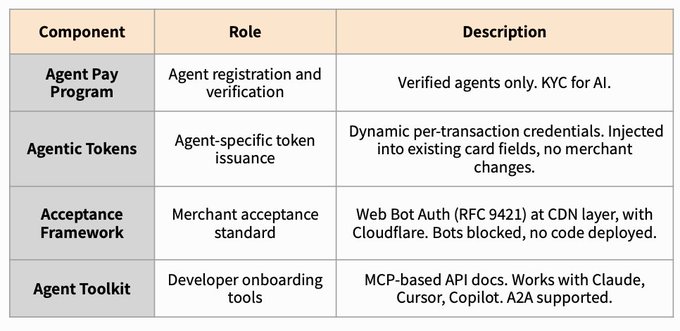

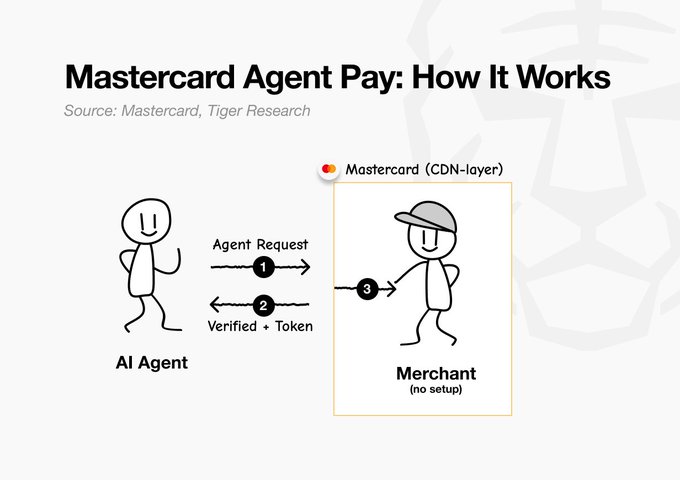

@Mastercard is playing the same game as Visa. It is a company that also aims to maintain its card network position even in the era of Agents. Mastercard's chosen strategy is to open its existing payment network, covering over 210 countries, to Agents while building architecture that enables merchants to easily integrate into its system.

In April 2025, Mastercard launched Mastercard Agent Pay, followed by developer tools in September and the Agent Pay Acceptance Framework in October, steadily building its Agent payment system.

The commonality among these components is that Mastercard does not attempt to dominate the market with its own protocol. Its strategy is to ensure that regardless of which direction the market moves, Mastercard can engage during payment and authentication moments. This is the same "payment layer neutrality" strategy as Visa's, but Mastercard focuses on merchant acceptance.

Mastercard's true battleground is to enable merchants to accept Agent payments without any operation. Typically, when merchants adopt a new payment method, they must embed code into their websites. Mastercard eliminates this burden.

By collaborating with Cloudflare, Mastercard has built a structure in front of merchant websites that can instantly differentiate “trusted Agent traffic from malicious bots,” only allowing trusted Agents to pass through to the merchant. Merchants can accept Agent transactions without touching a single line of code.

Another path is left for merchants wishing for deep integration. Merchants that wish to directly converse with Agents can connect through major Agent protocols such as MCP, A2A, and ACP. Ultimately, merchants have two choices: do nothing and accept default traffic; or connect protocols and build custom experiences. Either way, transactions will flow through Mastercard.

Core Business

Mastercard’s revenue structure is simple. Fees are incurred each time a payment goes through the Mastercard network. In the 2025 fiscal year, revenue is projected at approximately 32.8 billion USD, with transaction volume hitting 175.5 billion transactions. Whether the payment is made by an Agent or a human, the same fees apply as long as the transaction goes through the Mastercard network.

The problem is that Agent payments could completely bypass the card network. If direct settlement occurs on-chain via stablecoins, Mastercard loses its position. Agent Pay is specifically designed as a strategy to fill this gap.

Mastercard's chosen path is to lower the threshold for merchants. Adopting a new payment method typically requires merchants to embed new code into their systems. Mastercard eliminates this burden. By collaborating with Cloudflare, Mastercard has built a layer in front of merchant websites that automatically filters trusted Agent traffic.

The more merchants that connect to the network, the more transactions are conducted through Mastercard.

The revenue path remains unchanged. Each time an Agent completes a payment via the Mastercard network, fees will be incurred. The structure is identical to when a card is swiped. The difference is that Agent payments are faster and more frequent than human payments. As transaction volume grows, the speed at which fees accumulate will also increase.

For Mastercard, the growth of Agent transactions is a natural extension of fee revenue. This is not about opening up a new business, but about ushering existing structures into the Agent era.

Outlook

Mastercard's outlook can be summarized in one sentence: like Visa, it does not pick a winner in the protocol race but aims to dominate how merchants accept Agents.

The core of this strategy is enabling merchants to accept Agent payments without touching a line of code. By working with Cloudflare, Mastercard effectively removes barriers to entry for merchants.

Visa is also moving in this direction, but Visa is currently dealing with stablecoin variables at the same time. With the acquisition of Bridge and the involvement of Tempo validators, the frontline has expanded. In contrast, Mastercard can still focus all its energy on the merchant acceptance layer. Defending a single front is an advantage at present.

The question is how long this concentration can be maintained. If payments between Agents begin to settle directly on-chain with stablecoins, transaction volume through existing payment networks may decline. Visa has already begun to address this risk; Mastercard has not yet publicly acted.

Stripe, Inc.

Core Technology

@stripe is the company that has become the internet commercial payment standard over the past 15 years by developing developer-friendly APIs. To maintain this position in the Agent era, Stripe's strategy is to lay new Agent-ready payment tracks directly on top of existing infrastructure.

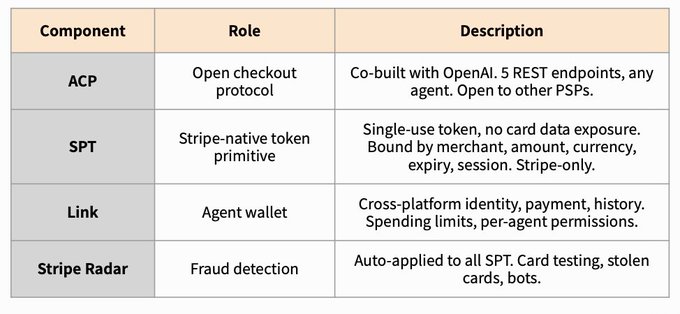

To this end, in September 2025, Stripe published ACP together with OpenAI as an open standard and announced its own payment primitive SPT (Shared Payment Token) in the same year.

Stripe's Agent payment stack consists of four components.

The commonality among the four components is that only ACP is an open standard; the others are proprietary technologies by Stripe. If ACP is the common language about "how Agents interact with merchants," then SPT is Stripe's proprietary payment token responsible for how money flows in that interaction.

The flow of SPT is as follows:

- The user says in ChatGPT, "Buy this."

- Stripe issues a one-time payment token (SPT).

- The Agent passes that token to the merchant.

- The merchant verifies the token and completes the payment.

The card number is never directly given to the Agent. Stripe issues a one-time token (SPT), which can only be used for this transaction, allowing the Agent to only pass that token to the merchant, thereby reducing the risk of card data theft. Moreover, any merchant already using Stripe needs only a single line of code to enable SPT payments.

In other words, this is the fastest path for merchants already integrated with Stripe, but merchants using other PSPs need separate integration.

Core Business

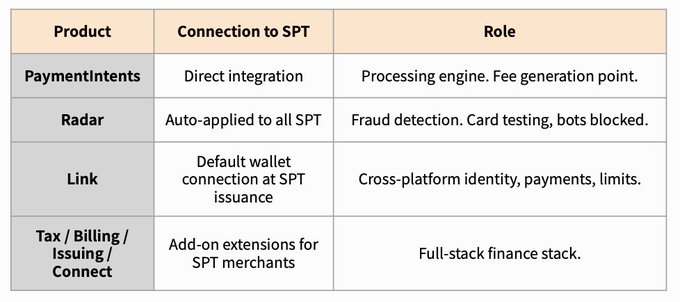

Stripe differentiates itself by designing SPT as the hub for Agent payments to enter the Stripe ecosystem rather than just a simple payment token. Once a merchant adopts SPT to accept Agent payments, adjacent Stripe products will follow as packages. Open one door, and four doors connect together.

Here's how it works: once a merchant adopts SPT to accept Agent payments, Stripe's adjacent services will follow as a bundled package.

Payment fees: Each Agent transaction through SPT carries the same fee structure as before. Agent payments are much faster and far more frequent. As more transactions occur, the speed at which fees are charged per transaction will accelerate. The payment method has changed; the fee structure has not.

Visa and Mastercard charge a fee each time a payment goes through their networks and then move on. Stripe uses payments as an entry point, binding merchants to its complete financial services stack.

From a merchant’s perspective, connecting a single Agent payment ultimately bonds the merchant to the entire Stripe ecosystem.

Outlook

Stripe's outlook can be summarized in one sentence: an all-encompassing strategy that occupies every layer of Agent payments.

Stripe has positioned itself at every layer of Agent payments: protocol layer (ACP), payment token layer (SPT), and stablecoin (@tempo). While Visa and Mastercard view stablecoins as a defensive challenge, Stripe has locked in the bypassing of cards as an offensive asset.

But the core question is this: can Stripe transcend the card network?

Stripe's current revenue structure is still built on top of Visa and Mastercard networks. SPT, payment fees, and merchant bundling all depend on the card networks. Only when stablecoins truly replace card networks will the structure change, but no one knows when that moment will arrive.

Admittedly, Stripe is currently double betting. However, if Visa and Mastercard operate the highways, Stripe is the most successful logistics company on those highways. Being the top logistics company is different from owning the highways themselves.

First, there’s the relationship with OpenAI. While ACP is a jointly developed protocol, real-time payment through ChatGPT is essentially Stripe's monopoly. If OpenAI builds its own payment track or allies with another PSP after the traffic accumulates to a sizable scale, Stripe could lose its largest AI channel. This relationship is currently necessary for both parties, but no alliance is permanent.

Second, there’s the open nature of ACP. Because ACP is an open standard, competitive PSPs like Adyen and Worldpay can also produce compatible tokens. Today, Stripe's market share naturally leads merchants to choose SPT; once competitors launch equivalent tokens, the premium enjoyed by the protocol proposer will quickly dilute.

Pay-per-call

The Agentic Commerce discussed above is a model where humans decide payment, whereas Pay-per-call is a market where Agents themselves act as the payers. As long as there are funds in the account, the Agents will settle autonomously. This structure is activated when an Agent calls another Agent's API, data, or computations.

For example, an Agent is asked to write a market analysis report.

- The user requests the Agent to write a market analysis report.

- The Agent queries the OpenAI API and gets a response.

- To verify data, it requests information from Dune and Nansen APIs.

- The completed report is sent to another Agent for review.

A report involves dozens of payments. However, unlike Agentic Commerce, the amounts can be as low as fractions of a cent. In traditional payment systems, such structures lead to losses on each transaction due to fees. This is why Pay-per-call relies on stablecoins, which have extremely low fees.

Currently, there are three infrastructure standards for Pay-per-call:

- Protocol Layer: How Agents express payment intent through messages.

- Settlement Layer: On which chain and with which asset the payment is settled.

- Trust Layer: Who verifies who pays what and with what authority.

Coinbase Global, Inc. (COIN)

Core Technology

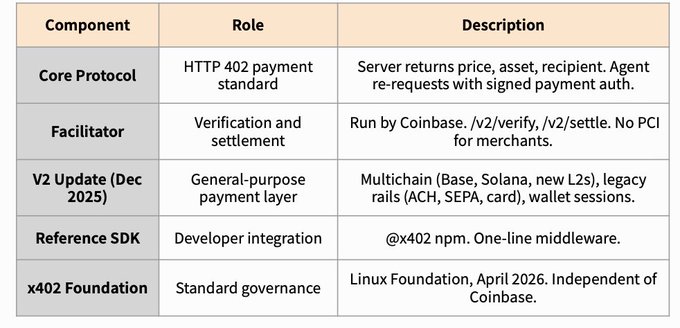

@coinbase is the company building x402, a standard that allows Agents to make payments without going through card networks.

In May 2025, Coinbase released the x402 protocol, activating the previously dormant HTTP 402 (Payment Required) status code. In the same year, Coinbase and Cloudflare jointly established the x402 Foundation to extend x402 into a universal payment layer.

x402 is an open payment protocol consisting of five elements.

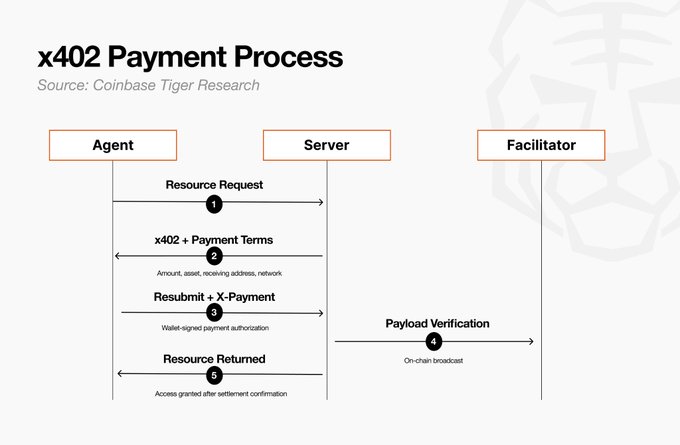

x402 works simply: when an Agent calls an API, the server returns an HTTP 402 response containing pricing, receiving address, asset, and network information. The Agent signs the payment with its own wallet, includes it in the header, and makes a re-request. The server verifies and settles the payment through the Facilitator, which broadcasts it on-chain.

Flow

- The Agent requests a resource from the server.

- The server returns an HTTP 402 with payment terms.

- The Agent signs the payment authorization with its own wallet and re-requests, carrying the signature in the X-PAYMENT header.

- The server passes the payload to the Facilitator (the validation and settlement service), which broadcasts on-chain.

- After settlement is confirmed, the server returns a 200 response and provides the resource.

The most fundamental difference between x402 and existing payment systems is that the payment itself serves as the authentication. Agents can autonomously discover, pay, and use new APIs without human intervention.

The V2 update expands x402 from a one-time call payment protocol to a universal layer that supports multiple types of authentication, sessions, and chains.

The most significant change is wallet-based sessions. V1 required a payment for each call; V2 introduces session-based payments (Sign-In-With-X), allowing for repeated use within a set time after a single payment. This change enables workloads (like LLM calls and multi-call Agents) that previously couldn't settle on-call due to being too slow or expensive to operate within x402.

Core Business

Coinbase's current revenue comes from exchange fees. In 2025, annual revenue is projected at around 7.2 billion USD, most of which is derived from cryptocurrency trading fees. x402 is currently unrelated to this revenue structure. But this is precisely why Coinbase has open-sourced x402: to release standards for free and then earn revenue based on the infrastructure operating that standard.

This strategy is similar to Google's: Open-source Android and then capture revenue through Play Store and Google Pay.

The market targeted by x402 is fundamentally different from that of Visa, Mastercard, and Stripe. Card payments charge 0.30 USD + 2.9%. However, micropayments like 0.01 USD API calls, 0.005 USD image classifications, or 0.50 USD for a minute of GPU time cannot exist on card networks.

The market opened by x402 lies in Agent payments to other Agents, or paying API providers, where the unit and frequency are factors that humans cannot trigger with a payment button.

When this distant future market opens, two revenue streams will flow to Coinbase.

Base transaction fees: the default settlement layer for x402 is Coinbase's Layer 2 chain Base. Every x402 payment generates transactions on Base, and Coinbase captures the sorting fee revenue. As x402 transaction volume increases, the transaction fees and locked assets on Base will also grow. The standard is released for free, but the chain operating that standard is run by Coinbase.

CDP infrastructure fees: each x402 payment requires a facilitator to verify "whether the payment is real" and actually move funds. The default facilitator is operated by Coinbase Developer Platform (CDP). Once developers start using x402, they will naturally pull in adjacent CDP tools: wallet creation, gas sponsorship, and data analytics.

However, since x402 V2, third-party facilitators can also participate. Thus, the locking power of facilitators is weaker than initially expected. Coinbase's true play lies elsewhere. The most affordable and fastest running x402 blockchain is Base, built by Coinbase, and its official white paper clearly states that x402 performs best on Base.

In simple terms: Stripe binds the payment moment to its own system. In contrast, Coinbase builds the highway for payments and lets travelers on that road naturally pull into Coinbase's rest area (CDP tools).

Outlook

Coinbase's outlook can be summarized in one sentence: not a game of defeating competitors, but a game of how quickly a yet-to-exist market will open.

This framework is important because x402 does not compete in the same domain as card networks. Credit cards charge a fee of 0.30 USD + 2.9%. Micropayments like 0.01 USD API calls, 0.005 USD image classifications, or 0.50 USD for a minute of GPU time simply can't exist on card networks.

Even if Visa and Mastercard accept Agent payments, that remains within the domain of Agents executing the buying behavior previously conducted by humans. The market that x402 opens lies at the next level: payments Agents make to other Agents or to payment service providers, in units and frequencies that humans can't press the payment button on.

The issue is that the trading market between Agents is still very small. For Agents to autonomously procure external resources from unspecified providers as part of their everyday workflows, these transactions must occur at a rate of dozens per second, with each transaction valued under 0.001 USD.

Only when the speed and unit price emerge that the existing subscription structure cannot handle does the proposition of "Pay-per-call being better than credit cards" hold true.

Ultimately, the expansion of this market follows a sequence. First, Agentic Commerce must grow; only through this process can trust and autonomy of Agents build up, validating the demand for the Pay-per-call market.

The winners of Agentic Commerce are already in competition. The winner of Pay-per-call will be determined at the moment the market opens.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。