Author: Anthony Bowman

Translated by: Jiahua, ChainCatcher

There is a real demand for fixed-rate borrowing on-chain. The obvious response is to issue fixed-rate loans, but there is no corresponding demand for fixed-rate lending in the market.

The vast majority of on-chain funds are in pursuit of yield and desire immediate liquidity. Therefore, issuing fixed-rate loans only transfers the interest rate risk from the borrower to the lender. And when the lender is a treasury that commits to immediate liquidity, an asset-liability mismatch can occur.

In variable-rate borrowing, interest rates fluctuate with capital utilization and market conditions, and borrowers directly bear the cost of this volatility. This is a real cost, but it is clear and transparent, terminating upon liquidation.

Assuming a lender holds a fixed loan with an interest rate of 3% for 6 months. If the interest rate rises, the same loan yield will now be 5%. At market value (MTM), the value of the old loan has shrunk. There are new loans with higher yields available under the same risk, and no one would buy the old loan at its amortized value.

The market value loss of a standalone loan stays on the books as the lender can hold it to maturity and receive full repayment. It is only when this loan is placed within a system requiring continuous pricing that it becomes extremely risky.

Morpho's V2 treasury is currently the most representative design publicly available, integrating fixed-rate loans within a treasury system that commits to immediate liquidity.

Excerpt from: Morpho Fixed Rate Market: Unlocking the Potential of On-Chain Loans

According to public information, this design includes three components:

Morpho Blue: Existing variable-rate lending protocol. Lenders deposit funds into an isolated market, and borrowers pay a rate that fluctuates with capital utilization, positions can be opened and closed at any time.

Morpho Midnight: Fixed-rate, fixed-term lending realized through zero-coupon bonds (ZCBs). Borrowing parties are matched by an intent engine, and each loan is a bond with specific collateral, term, and rate. These zero-coupon bonds require no permission and support any solution of collateral, term, and parameter combinations.

Morpho V2 Treasury: A treasury managed by curators, which allocates deposits between Blue and Midnight based on yield. Depositors withdraw and deposit based on the treasury's share price.

Image from Morpho V2 Treasury documentation

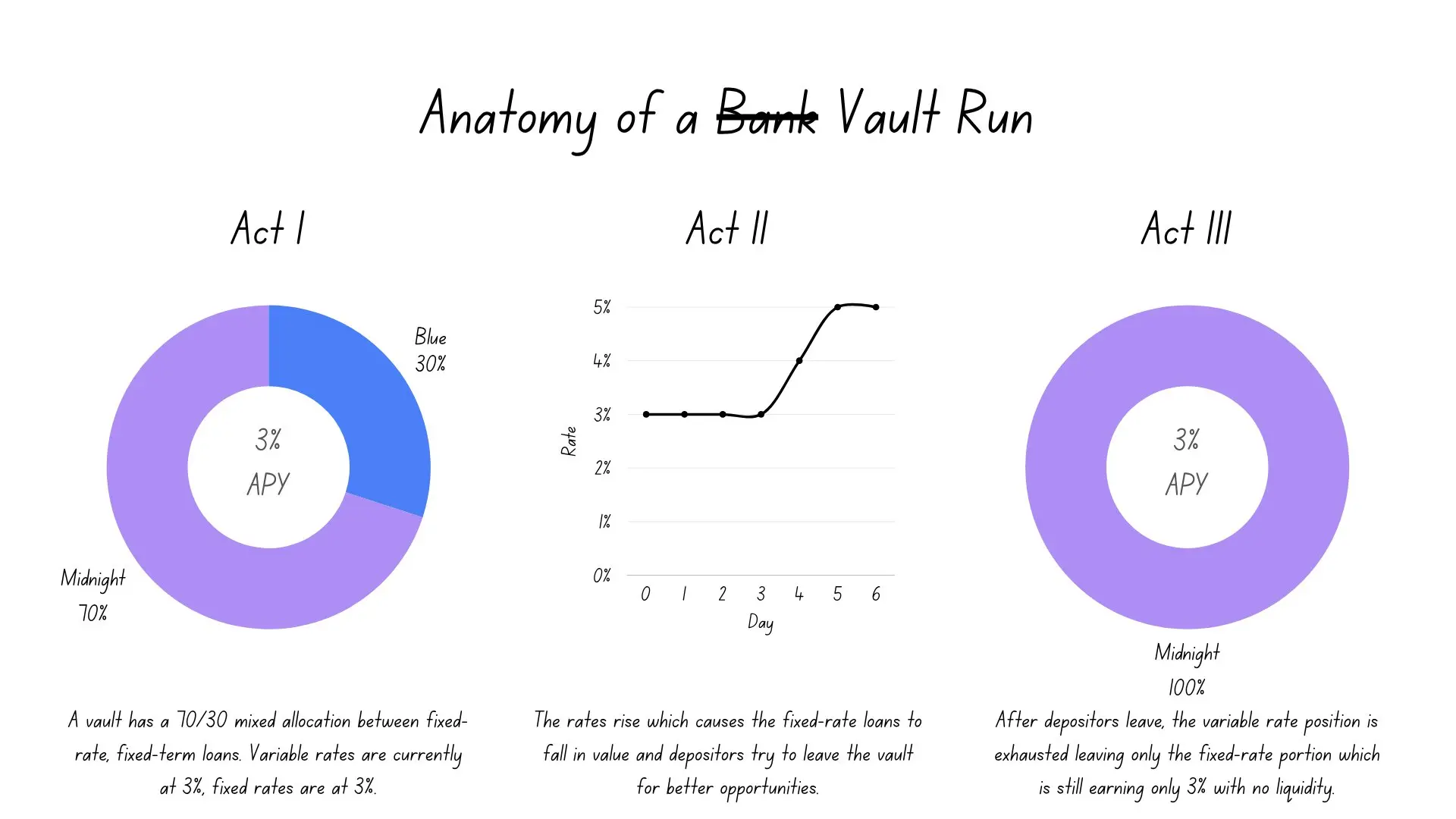

Envision two competing treasuries priced in USDC: Treasury A allocates funds to both Blue and Midnight, while Treasury B only allocates to Blue. Treasury A allocates 30% to Blue (variable, 3%) and 70% to Midnight (fixed, 3%).

A rate shock raises the variable rate to 5%, while Midnight's position remains locked at 3%. Treasury A's mixed yield rises to 3.6% (5%×30%+3%×70%). The purely variable-rate Treasury B rises to 5%. This 140 basis point gap creates conditions and incentives for treasury runs.

Depositors in Treasury A do not need to calculate market value losses, nor must they even know of their existence. The yield spread itself serves as the coordinating mechanism. Funds flow from A to B in pursuit of higher interest rates, and withdraw through A's uniquely liquid portion (the variable-rate module).

This will first drain the portion with the highest on-book yield, causing Treasury A's mixed yield to fall further and accelerate the run. What remains are illiquid fixed loans below market rates that can only wait until maturity.

Now the situation reverses. When interest rates decline, Treasury A's fixed position is above market levels, and depositors enjoy market value gains but cannot retain them. Depositors in Treasury B detect Treasury A's higher mixed yield and will rush to deposit for a share.

New funds enter at the current share price and are proportionately allocated to the existing book. This means that for positions above market rates, new money enjoys the same proportionate rights as the original depositors. This portion of yield is thus diluted.

Both sides lead to dead ends. Interest rates rise: depositors run away, treasury run. Interest rates fall: yields are diluted by newcomers.

The fundamental issue lies in the pricing mechanism of bonds. Although the accounting treatment of zero-coupon bond amortization varies, putting that aside, the real problem is that changes in external interest rates alter the actual value of the bonds, while amortization-based pricing fails to reflect this fact.

If bonds are priced at amortized value, the aforementioned asymmetry will follow. An evident solution is to create a secondary market, which would theoretically allow the treasury to price bonds at their real value.

However, the absence of permission zero-coupon bonds with arbitrary collateral, terms, and parameters cannot form a secondary market because every bond is effectively unique, lacking a liquid benchmark for valuation.

Taking a step back, even if a secondary market were formed, pricing the treasury through it would only cover one problem with a worse one. Share prices would be influenced by external trading data of customized, illiquid bonds. Anyone who can influence this data could manipulate share prices and arbitrage when entering and exiting the treasury.

The highly expressive zero-coupon bonds and the treasury that commits to immediate liquidity are structurally at odds. Perhaps there is some resolution within this framework, but I have yet to see a related description and am very curious whether Morpho has a countermeasure.

However, I personally believe that directly issuing fixed loans is not the solution, at least not in the current short-term outlook of over-collateralized lending. If borrowers want fixed rates while lenders desire immediate liquidity, then interest rate risk must be transferred to those willing to take on that directional risk exposure.

If the underlying variable-rate benchmark curve can become increasingly efficient and stable, buyers of interest rate risk can offer higher quality fixed rates. As I discussed in this article, we are far from reaching the final form of variable rate market design.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。