DeFi was once a power strip without sockets, RWA connected this circuit to the real external power grid.

Written by: Tiger Research

Translated by: AididiaoJP, Foresight News

The DeFi market has spent years compounding returns on returns, attracting a massive amount of capital through high-yield incentives. But now DeFi is connecting to real-world assets (RWA) as its true yield network.

Key Points

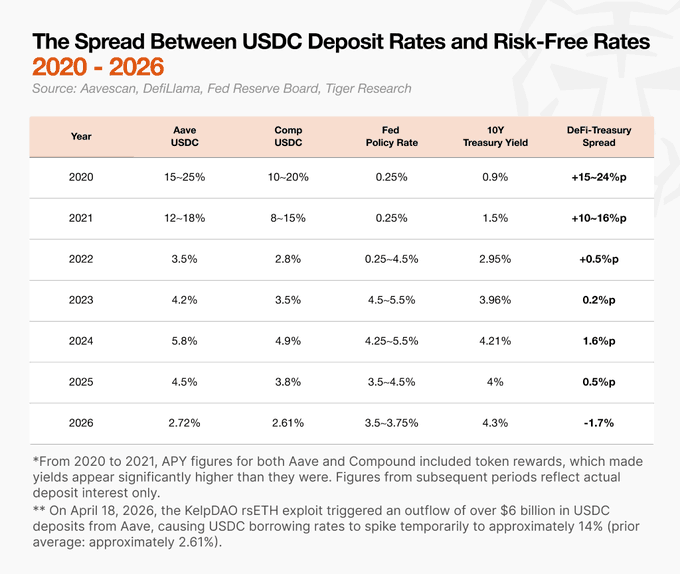

- Aave V3's USDC deposit rate is 2.7%, below the US 10-year treasury yield of 4.3%. The fundamental yields in DeFi are decreasing.

- The market is not dead; yields are down, but RWA and stablecoins have grown into a multi-hundred billion dollar market, evolving in a new direction.

- The failures of Compound, Curve, and Olympus share a common lesson: any structure supported by tokens that undergird other tokens will collapse once external capital stops flowing in.

- DeFi was once a power strip without sockets; RWA connected this circuit to the real external power grid.

- The market is maturing. It is anchoring on real underlying assets (RWA) and showing signs of coordinated accountability, as seen in the DeFi United initiative.

Declining Yields, Market Still Growing

DeFi is no longer a high-yield product.

Since 2022, the yield spread between DeFi and government bonds has narrowed to near zero, with inversions occurring at certain times. As of April 2026, Aave V3's USDC deposit rate is approximately 2.7%, lower than the Federal Funds Rate (3.5%) and the US 10-year treasury yield (4.3%).

In the past, taking on risk made clear sense.

On-chain yields were much higher than bank deposits. That is no longer the case. If the returns from DeFi—after absorbing all on-chain risks (like hacks and de-pegging events)—are lower than traditional finance, the reasons for retail users to engage in DeFi diminish.

However, the market itself is growing in different directions. While DeFi yields have decreased, the RWA and stablecoin markets are integrating with traditional finance, expanding to hundreds of billions in scale. Institutional participation has played a significant role in this shift.

However, institutions often overlook the history and existing community of DeFi, imposing traditional financial practices onto it. Before institutional involvement, DeFi was a market driven by incentives. Some protocols gained market recognition through incentive strategies and altered the market paradigm. This model persists in DeFi, with Aave, which rose during DeFi Summer, now acting as a benchmark rate provider for DeFi protocols.

Understanding the participants who remain in the market is essential groundwork for new institutional entrants. This article traces the protocols that have propelled defining narratives throughout DeFi's lifecycle and the lessons the market has learned from them.

The History of DeFi: From Experimentation to Collapse and Rebuilding

DeFi was initially not a market built on incentive promises. The starting point was simple: "Can we lend, swap, and use assets as collateral on the blockchain without intermediaries?"

The early stages were closer to financial experiments. The significance lies in the fact itself: no bank loans, no exchange trading, anyone with collateral could create liquidity. But after 2020, the market rapidly turned in another direction. Token incentives became the primary mechanism to attract capital. Countless protocols and ideas emerged, but only a few survived. The market learned lessons from each narrative and continuously adjusted its direction.

Compound integrated its native token (COMP) into yield incentives to attract massive liquidity. However, when other projects replicated the same playbook, new capital inflows dried up, revealing structural vulnerabilities.

@CurveFinance transformed governance voting into a competition over which pool could receive yields, turning yield competition into a war for control of the protocol. The market recognized that DeFi governance could also become a target for power and incentive monopolies.

@OlympusDAO is the most extreme case. It showcased the possibility of DeFi having its own liquidity without reliance on external capital through extremely high APY. However, its returns heavily depended on new token issuance and new capital rather than real cash flow. When inflows slowed, both the price of its governance token OHM and confidence in the protocol collapsed.

The lesson from these three is: "When the source of yield is the tokens of the protocol itself, this structure cannot sustain itself." This experience changed the way users, builders, and institutions view DeFi.

In this gap, a new movement began to emerge: EigenLayer, Pendle, YBS, and RWA.

Compound: A Bubble Built on Token Distribution

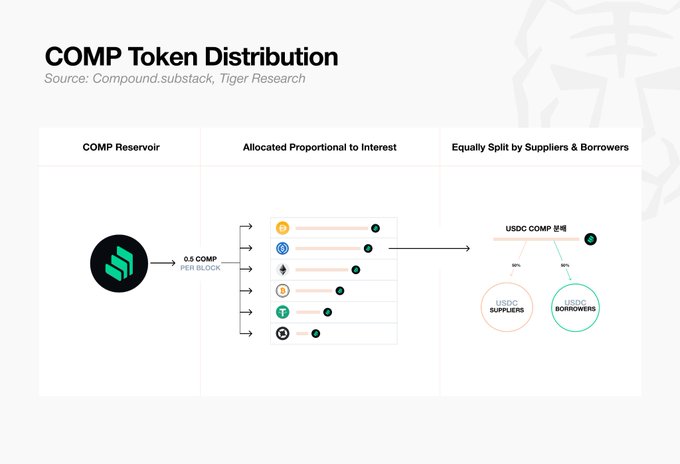

In June 2020, Compound began distributing its governance token COMP to users. Both depositors and borrowers could earn token rewards. At certain times, COMP rewards even exceeded borrowing costs, creating a scenario where "borrowing money actually earns you money."

This represented a new paradigm. With users flooding in, Ethereum gas fees soared, making it commonplace to pay tens of dollars for a single transfer. Depositing and borrowing were no longer straightforward financial actions but became tools for airdrop rewards, with capital chasing yield rapidly moving between protocols.

This period was dubbed DeFi Summer. Uniswap, Aave, and Yearn Finance all rose, solidifying on-chain finance as an independent market. However, Compound ultimately built a structure that attracted capital through token-dependent incentives, while that capital drove up token prices. Today's DeFi users' keen response to yields, liquidity, and reward structures was formed during this period.

Curve and veCRV: The Dawn of the Curve Wars

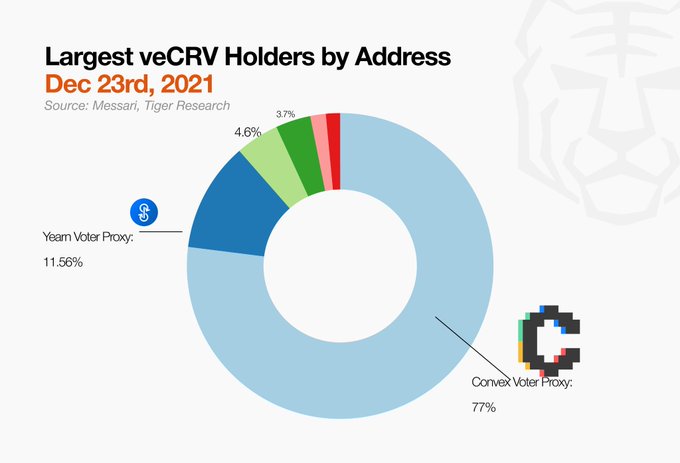

Curve initially resembled a stablecoin exchange. But the introduction of veCRV fundamentally changed its nature. The longer users locked up CRV, the more veCRV they received, and veCRV carried voting rights over gauge weight distribution, deciding how CRV rewards would be allocated among various pools.

From that moment on, the focus of competition shifted from yields themselves to the power to move those yields. Those with more veCRV could direct more incentives to their pools. Protocols naturally began to compete to accumulate veCRV, leading to the emergence of Curve Wars.

Initially, this structure appeared attractive to both retail users and builders. The longer retail users locked up their tokens, the higher their yields, while builders could reduce circulating supply and steer liquidity towards target pools. This is why similar models spread throughout the ecosystem, including Balancer’s veBAL and Frax’s veFXS.

However, over time, this power did not remain in the hands of individual users. Meta-protocols like Convex aggregate and lock up CRV on behalf of users to provide enhanced yields in exchange for accumulating veCRV voting rights. The Curve Wars expanded their scope with Convex as a new battleground.

Ultimately, veCRV proved to be more motivating than the control over yields themselves. Users did not directly hold that power but delegated it to more efficient intermediaries like Convex. Curve revealed that governance rights in DeFi itself can become an asset that generates yields, and that right is easily concentrated.

OlympusDAO: A Golden Age Built on Game Theory

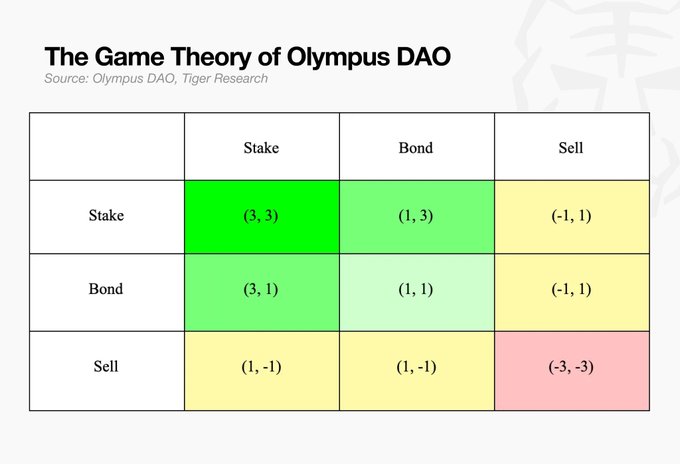

Even after the introduction of Curve’s veToken mechanism, liquidity remained DeFi’s most stubborn challenge. Once external sources of liquidity were offered better incentives, they would leave. This is mercenary capital.

OlympusDAO, which emerged in the second half of 2021, garnered attention as a solution. Its core consists of three elements: Protocol-Owned Liquidity, a (3,3) game theory framework (which posits that when all participants choose to stake, the best outcome will arise), and extreme APYs exceeding 200,000% at launch.

However, this structure did not last. The yields of OHM heavily depended on new token emissions rather than real cash flow. The mechanism gave rise to dozens of similar projects, but OHM's price ultimately fell by over 90%. Following this, builders began asking "how high can yields go?" before asking "where do these yields actually come from?".

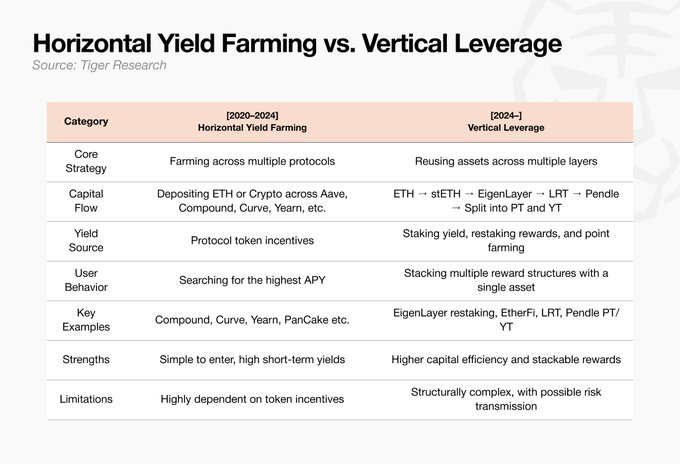

EigenLayer and Pendle: From Horizontal Deposits to Vertical Leverage

The collapse reshaped retail user behavior. The playbook from 2020 to 2022 was simple: first airdrop incentives, then exit. It became common for individual users to spread their funds across multiple protocols simultaneously. The airdrop yields of that era were horizontal. Capital moved between protocols, chasing higher APYs.

After 2022, this method lost efficiency. Token incentives proved unsustainable, and competition for airdrops intensified. Simply depositing across multiple venues led to diminishing returns. Capital began to shift from single asset stacking multi-layer yields: restaking stETH, redeploying LRT to DeFi, and splitting yield rights to capture points and future returns.

EigenLayer and @pendle_fi are at the center of this shift. Starting in 2024, EigenLayer launched a restaking structure that allows staked ETH and LST to generate additional rewards. EigenLayer’s TVL grew from under $400 million to $18.8 billion in about six months, clearly indicating capital is rapidly moving from simple deposits to restaking.

Pendle splits yield-bearing assets into PT and YT. PT represents a claim close to the principal, while YT captures all yields, rewards, and points prior to maturity. YT goes to zero at maturity but can extract maximized points and returns before that. Even without fully understanding the structure, purchasing YT has become an airdrop strategy that utilizes time and capital.

The strategy has shifted from spreading capital across multiple protocols to stacking multi-layer rewards from a single asset.

Reshaping Income Models: RWA and YBS

Builders used to focus on driving TVL through token incentives. As TVL grew, protocols appeared to expand, and token prices rose alongside. The issue was that liquidity never stayed long.

TVL remains an important metric. However, focus has shifted to revenue based on fees, real asset backing, and regulatory readiness. The reason is a new variable has emerged: institutions. Institutions will inquire more rigorously about where yields come from and which assets serve as backing.

Products are evolving to absorb both of these demands.

RWA: Institutions Enter the Market

Since 2024, traditional financial institutions including @BlackRock, @FTI_US, and @jpmorgan have begun entering the on-chain market under the banner of RWA. Their approach is to tokenize off-chain assets like government bonds, money market funds, private credit, gold, and real estate, and then distribute these tokens on-chain.

The on-chain RWA market has grown from billions in 2022 to hundreds of billions by April 2026. Tokenized government bonds and private credit are the main drivers of this growth.

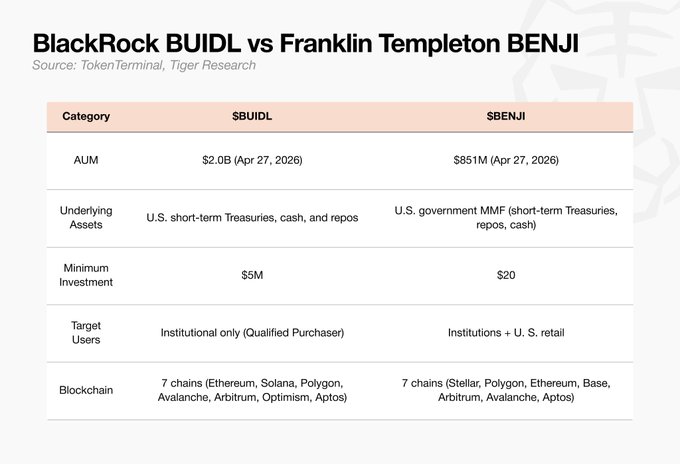

Currently, the leading institutional products in the market are BlackRock BUIDL and Franklin Templeton BENJI. BUIDL and BENJI cover similar types of assets but differ in their approaches. BUIDL is primarily aimed at institutions, while BENJI is open to US retail users starting from $20.

Additionally, Apollo, Hamilton Lane, and KKR are working with on-chain issuance platforms like Securitize to accelerate the tokenization of private funds and private credit.

For institutions, the on-chain market is less about a new frontier to explore and more about a new distribution channel. Thus, protocols serving institutions are building the necessary KYC and AML frameworks, custody infrastructures, legal jurisdiction coverage, and risk management frameworks.

Yield-bearing Stablecoins (YBS): Dollars with Built-in Yield

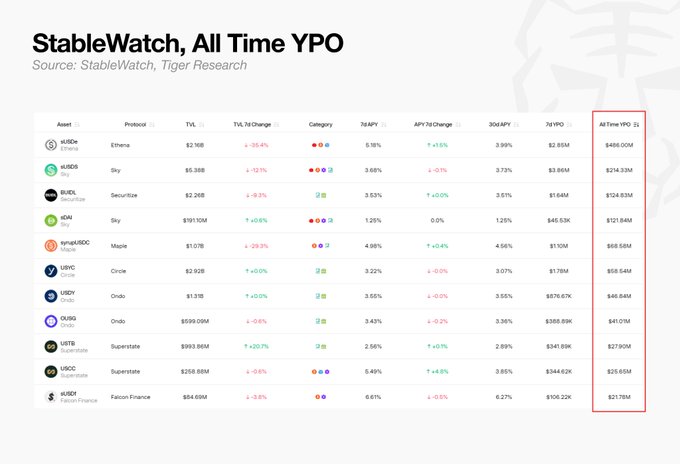

A noteworthy segment is YBS. Yield-bearing stablecoins (YBS) are stablecoins that embed yield directly within the token itself. Ondo USDY, Sky sUSDS, Ethena sUSDe, as well as the previously mentioned BlackRock BUIDL and Franklin BENJI all belong to this category.

Simply holding these assets will accumulate the yields generated by the underlying assets. The underlying assets include US treasury bonds, funding rates, staking interest, and money market funds. This structure closely resembles the migration of traditional financial MMFs onto the blockchain.

According to YPO data from @stablewatchHQ, Ethena sUSDe, Sky sUSDS, BlackRock BUIDL, and Sky sDAI rank among the top products paying accumulated yields. While the calculation methods vary across products, YBS has clearly evolved from a niche experiment into a category where real interest is being distributed.

However, simply transplanting MMFs onto the blockchain does not constitute differentiation. The real differentiation lies in composability. BUIDL constitutes 90% of Ethena USDtb reserves, while USDtb is used as collateral for Aave.

In other words, what was once a foundational product as real-world RWA tools has now become a stable structural component. This is no longer a market relying on a limited internal battery to operate. It has begun to draw power from external sources.

Players Building the RWA Network, Learning from Past Failures

Up to now, DeFi has been about plugging power strips into each other and calling it a flywheel.

Layer upon layer of power strips, ultimately connecting on leverage and derivatives, the problem is the current comes from the future externally. It was mainly token incentives generated by the protocols themselves, as Compound created loans with its tokens; Curve retained liquidity providers with its tokens.

It seems like each one is powering the other, but in reality, this is a structure running on a shared, limited battery. When the market shakes, the voltage starts to drop from the bottom, and the farthest products begin to extinguish. The load that self-referencing power strips can endure is limited.

RWA connects this structure to the real power network for the first time. Cash flow generated by the real economy—such as bond interest, real estate rental income, and trade receivables—becomes the current for on-chain finance. Interest rates are not determined by internal token incentives but by external market demand, interest rates, and credit risks.

Once the current begins to flow, financial functions such as issuance, custody, collateralization, lending, and settlement can be sequentially connected on top of it. Financial products that are difficult to design in traditional DeFi become viable on this power network. The issue is no longer how many power strips to plug in but how stable the current can be drawn from it.

This is the essence of on-chain RWA. Bringing assets with real underlying value onto the chain and connecting financial functions on top of the cash flows they generate. If traditional DeFi borrowed liquidity through token incentives as a temporary battery, today's RWA market is attempting to retain liquidity through the cash flows of the assets themselves.

The players in today's market are building this power network from their respective positions.

- Theo decides which assets to connect on-chain, choosing those that will serve as power sources.

- Plume builds the infrastructure for asset issuance and distribution, laying down the transmission lines and switch infrastructure that allows current to flow.

- Morpho uses these distributed assets as collateral to build lending and collateral markets. It is the first financial device to actualize power extraction on this power network.

No single player owns the entire power grid. Only when power sources, transmission networks, and points of usage are all connected does this new financial circuit named on-chain RWA become complete.

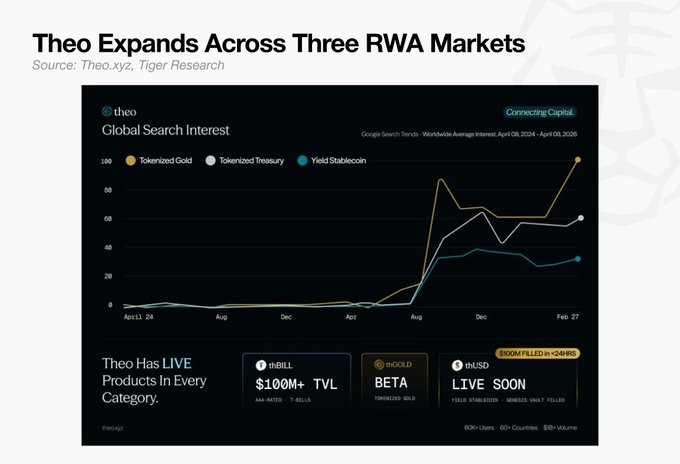

Theo: A Case Study in Repositioning the Customer Base

@Theo_Network serves as a case study of starting from asset selection and rebuilding its customer base from scratch.

Theo’s flagship product was once a strategy vault. However, as the market changed, the desires of retail users and those of institutions began to diverge. Theo recognized this shift and completely redefined its customer base.

The core product is thBILL. It is a basket of tokenized US short-term treasuries provided by regulated issuers, designed to produce stable income as a core asset in the Theo ecosystem. Subsequent roadmaps have added thGOLD, and thUSD (YBS backed by thGOLD) is also on its way.

What changed was not just the product. It signifies that a player starting from retail incentives can also be designed to speak the language that engages with institutions.

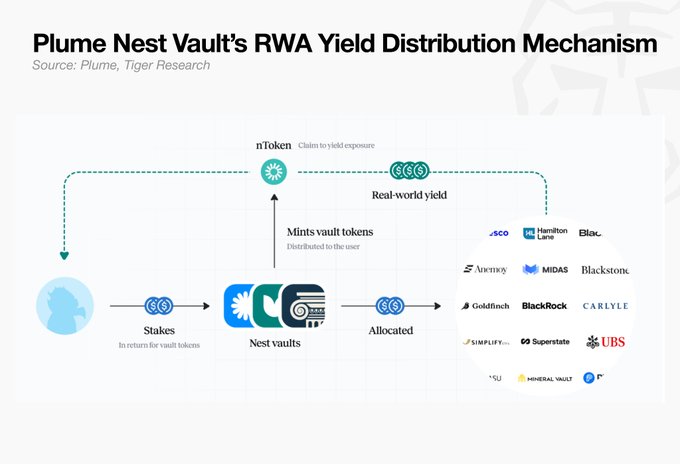

Plume: Creating the Environment for RWA Operations

@plumenetwork is a case that bundles asset distribution infrastructure with upper-layer demand.

For institutions, putting assets on-chain is not enough. What is needed is an end-to-end infrastructure that encompasses issuance, compliance, distribution, and yield productization. For on-chain users, accessing institutional-grade assets (like treasuries and funds) requires supporting product structures.

Nest is a yield protocol built on Plume infrastructure. It packages yields from institutional-grade RWA into a format accessible to users who deposit stablecoins. Each vault, including nBASIS, nTBILL, and nWisdom, provides returns backed by different real-world assets, and the vault tokens can move and circulate freely in DeFi.

WisdomTree has launched 14 tokenized funds, Apollo Global deployed a $50 million credit strategy, and Invesco has migrated a $6.3 billion senior loan strategy to Plume. Nest serves as the demand entrypoint for these institutional assets.

In addition to its own track, Plume also acts as an integrated infrastructure that creates distribution channels between institutional assets and on-chain demand.

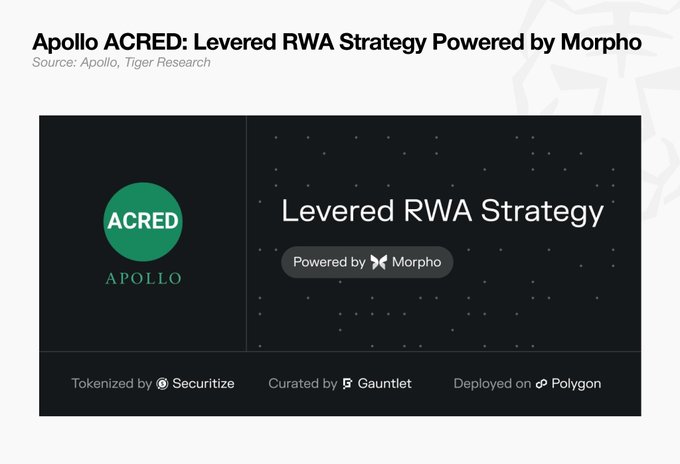

Morpho: Adding Financial Functionality to Institutional Assets

@Morpho is a case of transforming assets into collateral, loans, and liquidity.

For institutions, registering assets on-chain is just the beginning. The important question is whether these assets can be used as collateral, and whether liquidity can be derived from that basis. Lending terms and risk parameters must be clearly defined, and execution must be feasible within custody and compliance frameworks.

A leading example is Apollo ACRED. Apollo not only deployed its credit strategy on Plume but allowed ACRED to be used as collateral on Morpho, enabling holders to borrow stablecoins while maintaining fund positions. ACRED is a tokenized private credit fund based on the Apollo Diversified Credit Securitize Fund, issued on-chain through Securitize.

Only when institutional assets can serve as collateral, generate loans, and produce liquidity will they become usable materials for on-chain finance.

What Remains After Token Incentives Fade

Looking back, the golden age of decentralized finance (DeFi) was closer to a mirage built on token incentives and leverage.

Some corners of the market remain skeptical of DeFi’s revival potential, pointing to a series of hack incidents.

However, the recent Kelp DAO rsETH event and the establishment of DeFi United tell a rather surprising story, countering the aforementioned view. By April 28, 2026, Aave and DeFi United successfully raised over $300 million, surpassing the $190 million siphoned off in this vulnerability.

This indicates the market is forming trust infrastructures and more mature models of shared accountability.

DeFi’s history tells us it was once a market where no one took responsibility. Rapidly claiming high-yield tokens was the only goal for users, while builders designed yield mechanisms to match this demand, often exiting after reaching their fundraising goals.

But the market is now shifting towards a model that must deliberately design accountability into the system. It is not yet a complete financial system, but it is evident that a movement recognizing shared problems and distributing losses and responsibilities has emerged.

Many feel the market is no longer viable not only due to security issues, but also because of the disappearance of instant rewards and yields, as well as a lack of any new narratives or catalysts.

The term "DeFi" is losing power as time passes. The market has fragmented under more specific labels: lending, stablecoins, RWA, restaking, on-chain credit.

The words themselves are not important. The experiments that started from them are maturing into structures that can truly put more assets into productive motion.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。