Eight years, two terms, spanning two presidents, a once-in-a-century global pandemic, and the most severe inflation in the United States in forty years.

Written by: Zhao Ying

Source: Wall Street Journal

「I won't see you next time」, with his term coming to an end, the countdown to Powell's era has begun.

On April 29, 2026, at the end of the Federal Reserve's regular press conference, Chairman Jerome Powell stepped off the podium and told the reporters present this seemingly understated yet profoundly meaningful phrase — 「Thank you very much, I won't see you next time.」

He then left the podium, exited the venue, and concluded his final press conference as Chairman of the Federal Reserve.

On May 15, 2026, Powell's chairmanship will officially come to a conclusion. On this day, his successor, Kevin Warsh, nominated by Trump, is expected to be confirmed through a voting by the Senate Banking Committee to take over this most powerful monetary policy position in the world.

Eight years, two terms, spanning two presidents, a once-in-a-century global pandemic, and the most severe inflation in the United States in forty years. What Powell leaves behind is a historical account interwoven with both achievements and controversies: under his leadership, the Federal Reserve successfully preserved the employment baseline, reducing the monthly average unemployment rate to 4.6%, lower than his predecessors Greenspan, Bernanke, and Yellen; but at the same time, the average inflation rate during his tenure reached 3.09%, far exceeding the Federal Reserve's 2% policy target and well above the average during the terms of previous chairs.

When discussing his policy legacy, Powell quoted a famous saying by Frank Sinatra, stating that he had a few regrets, but not many. This statement may be the most appropriate footnote for these eight years.

Atypical Central Bank President: From Princeton Liberal Arts Graduate to Federal Reserve Leader

In November 2017, then-President Trump announced the nomination of Jerome Powell to succeed Janet Yellen as the 16th Chairman of the Federal Reserve. This appointment, once announced, immediately caused a stir in academic circles.

The reason is simple: Powell is not an economist.

For the past thirty years, starting with Greenspan (in 1987), every past Chairman of the Federal Reserve has held a doctoral degree in economics, and has been a top scholar in the field of macroeconomics. In contrast, Powell's resume appears particularly unconventional on this elite track.

Powell graduated from Princeton University in 1975 with a Bachelor of Arts degree, then attended Georgetown University Law Center, earning a Juris Doctor degree. He started his career as an investment banker in New York, later entering the Treasury Department and serving as a Treasury official during the George H.W. Bush administration, handling domestic financial, debt, and tax policies.

From 1997 to 2005, he worked as a partner at the prominent Washington private equity firm Carlyle Group, and in 2008 he joined the private equity firm Global Environment Fund as a managing partner.

In 2011, then-President Obama nominated him to serve on the Board of Governors of the Federal Reserve. This move was widely interpreted at the time as an olive branch extended to Republicans. In 2012, the Wall Street Journal reported that Powell's personal assets ranged between $21.3 million and $72.2 million, making him one of the wealthiest members of the Federal Reserve Board at that time.

However, the accumulation of wealth on Wall Street cannot compensate for the lack of an academic background. Greg McBride, chief financial analyst at financial services company Bankrate.com, frankly stated: “Jerome Powell does not have a PhD in economics, but he will be entrusted with the heavy responsibility of guiding the world’s largest economy. Putting a non-economist at the helm of the Federal Reserve is a break from tradition.”

Critics voiced even sharper words. Josh Bivens, research director at the Economic Policy Institute, called for retaining Yellen and pointed out: “It is time for a true macroeconomic expert to steer the ship, not someone who may be beholden to the Board.”

Some commentators cited G. William Miller, the last non-economist to serve as Federal Reserve Chair, as a warning example, noting that Miller was forced to resign after only 17 months in office due to misjudgments regarding the inflation situation during the Carter administration, warning that history may repeat itself.

However, Aaron Klein, an economist at the Brookings Institution, held a different view. He argued that Powell's years of practical experience accumulated in the Treasury and the Federal Reserve fully qualified him for the position. More importantly, his unique background might precisely help the Federal Reserve break the long-standing “groupthink.”

“There is no magical secret formula that is exclusive to PhD economists,” Klein said, “Having a chair with a different background could be an advantage — provided he knows when to set aside the models and make judgments based on intuition.”

This debate will be dramatically tested over the next eight years.

2018 Transition: Inheriting a Start Filled with Hidden Dangers

On February 5, 2018, Powell was sworn in, officially taking over the helm of the Federal Reserve from Yellen.

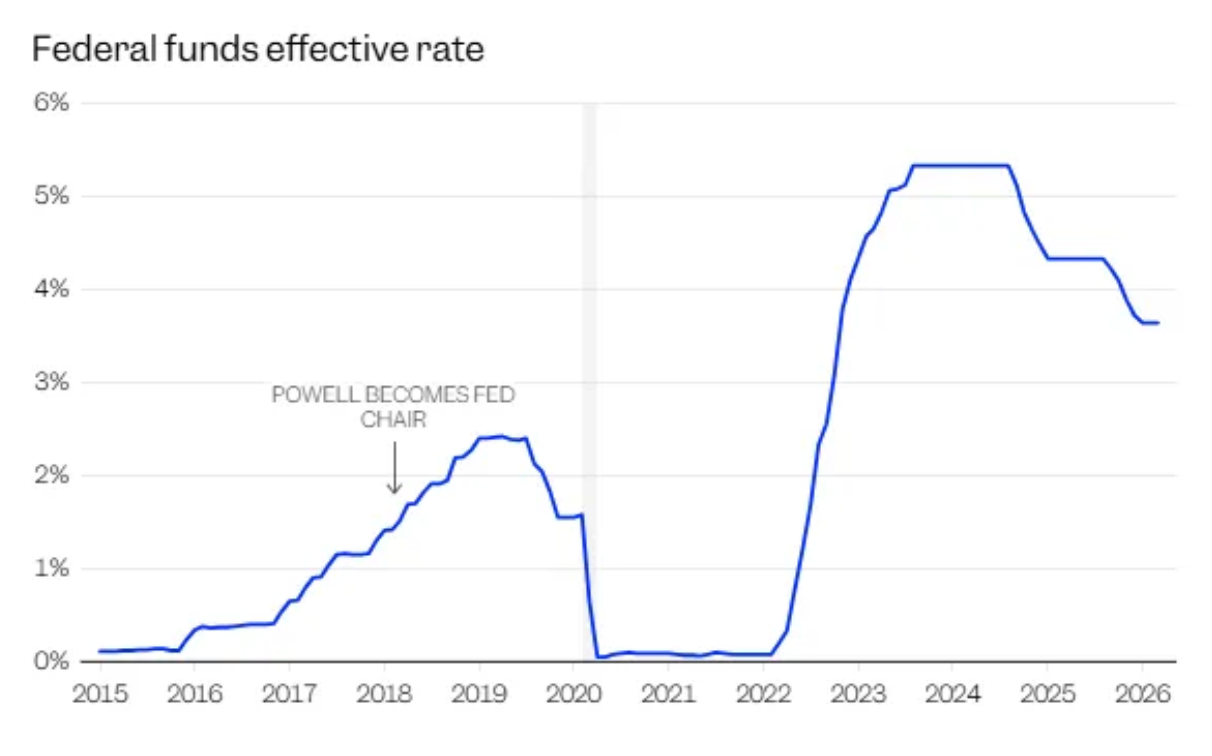

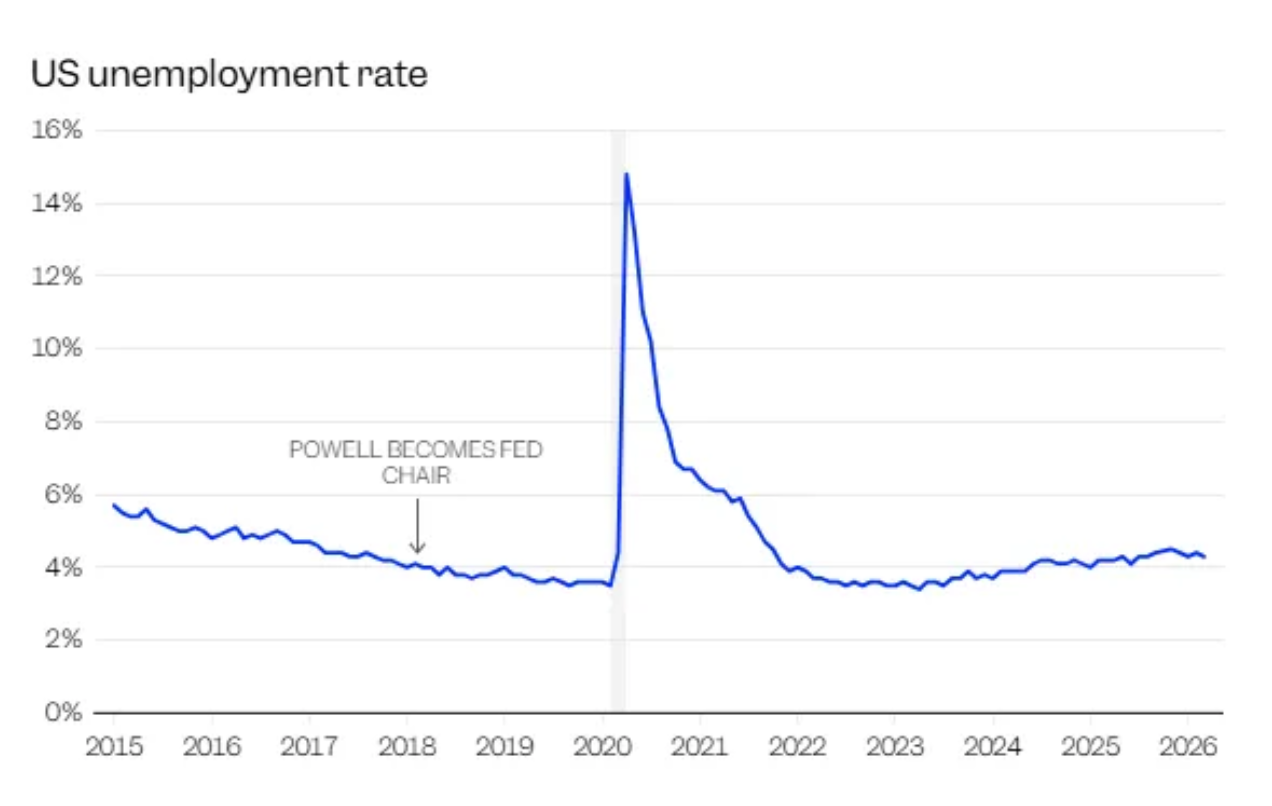

On the surface, he inherited quite a favorable situation: inflation was below the Federal Reserve's 2% policy target, operating at about 1.5%; the unemployment rate was at 4.1%, the lowest point in 17 years; the economy was regaining momentum after years of stagnation, the stock market was repeatedly hitting historical highs, and Trump's tax reform was providing fiscal stimulus to the economy.

However, hidden dangers had already quietly accumulated beneath the surface.

Veteran observer David Wessel pointed out at the time that Yellen left Powell not just a shiny report card, but also a series of thorny challenges: how to manage the pace of interest rate hikes before inflation pressure escalated? How to assess the impact of substantial tax cuts on an economy that was already near full capacity? When and how to employ unconventional monetary policy tools to respond to the next recession?

Some other critics were even more pessimistic. They believed that Yellen’s prolonged loose policy allowed U.S. stock market valuations to rise to levels that had only been seen three times in the past century, while global government bond yields fell to historical lows, with credit risk being systematically underestimated — all of which would become ticking time bombs left for Powell.

Even more complicated were the political variables. Just five months into Powell’s tenure, Trump publicly lambasted on CNBC: “I don’t like the effort we’re putting into the economy, then watching interest rates rise.”

Powell chose to ignore it. But this political struggle with Trump was just beginning.

In the fall of 2018, Powell stated in an interview that the Federal Reserve was “a long way” from the neutral level of interest rates, which triggered significant market volatility. In December of that year, he caused a new wave of market panic with a statement that the balance sheet reduction was “on autopilot.” Trump considered dismissing him at one point.

These two media controversies made Powell deeply realize one truth: as Chairman of the Federal Reserve, every word has the power to shake the market.

Pandemic Impact: The "Rule Breaker" in Crisis

If the initial policy adjustment period at the beginning of his tenure was merely a warm-up, then the spring of 2020 was truly Powell's first major test.

At the beginning of 2020, the COVID-19 pandemic swept the globe, and the U.S. economy plummeted off a cliff within just a few weeks. In April 2020, the unemployment rate in the United States skyrocketed to 14.8%, setting a record high since modern unemployment statistics began in 1948, with tens of millions of Americans losing their jobs overnight.

In the face of this once-in-a-century crisis, Powell's rapid response and aggressive measures left Wall Street astonished.

The Federal Reserve, in an extremely short time, lowered the benchmark interest rate to near zero and re-launched with a dramatic expansion of quantitative easing, purchasing several trillion dollars in bonds within weeks; concurrently, Powell collaborated with the Treasury Department to launch a series of emergency credit tools that far exceeded the traditional boundaries of central banking.

He later admitted that these actions had far surpassed the territory of conventional monetary policy.

“We crossed many red lines,” Powell said at a Princeton University event in May 2020, “In such situations, you do the thing first, and then figure out how to remedy it later.”

This gamble ultimately paid off. The U.S. economy successfully avoided a second Great Depression, the labor market completed a journey from the severe impacts of the pandemic to the near full recovery in about two years — a process that took six years after the 2008 financial crisis. Powell received widespread praise for this, being seen as a leader showing Volcker-like courage in a time of crisis.

However, the phrase “then figure out how to remedy it later” also laid the groundwork for subsequent policy mistakes.

High Inflation Era: From "Transitory" Arrogance to "Volcker-like" Firmness

The cost of pandemic rescue became concentrated in the year 2021.

With a massive influx of fiscal stimulus funds into the market, consumer demand surged, while the restoration of global supply chains was much slower than expected; simultaneously, labor market supply remained tight, with costs such as energy, rent, and wages rising in succession. The dual imbalance from both demand and supply sides, along with the surge in energy prices triggered by the Russia-Ukraine war, collectively pushed U.S. inflation to the brink of uncontrollability.

In August 2021, faced with the significantly increasing inflation pressure, Powell made a fateful judgment at the annual Jackson Hole central bankers' conference — he labeled current inflation as “transitory,” believing that supply chain disruptions would eventually dissipate and prices would return to the right track.

This judgment became his biggest policy mistake during his tenure.

It turned out that inflation did not dissipate “transitorily” on its own, but instead continued to accelerate. By February 2022, the U.S. core CPI year-on-year increase had climbed to 6.4%, the highest level in forty years; by June of the same year, the comprehensive CPI year-on-year increase further peaked at 9.1%. This not only reflected the Federal Reserve's misjudgment, but also marked an indelible blemish in Powell’s historical evaluation.

During a Congressional hearing, senators directly questioned: why did the Federal Reserve misjudge the inflation situation so severely? Powell admitted that this wave of inflation escalated rapidly after mid-2021, surpassing the expectations of almost all mainstream macroeconomists; the speed of supply chain restoration also lagged far behind expectations, which was an unprecedented situation in history. He acknowledged, “We should have acted earlier.”

The delayed correction was unprecedented in its scope.

In March 2022, the Federal Reserve officially commenced this round of interest rate hikes. Over the following year, the series of aggressive rate hikes led by Powell shocked the market — within less than two years, the benchmark interest rate was raised by over 500 basis points from near-zero levels, a speed of rate hikes that is extremely rare in the modern history of the Federal Reserve.

In stark contrast to the crisis measures taken in 2020, this time Powell's intellectual inspiration shifted from Keynes to Volcker. At the Jackson Hole conference in 2022, he clearly warned that bringing “price stability back” would bring “some pain” to employment and growth, and declared he would “maintain price stability at all costs,” thereby conveying his determination to combat inflation with an iron fist to the market.

Critics pointed out that this was a delayed shift, for which the Federal Reserve paid a heavy price — millions of American families suffered a significant loss of purchasing power during this period. However, some economists defended Powell, arguing that the main cause of this wave of inflation was supply-side disturbances brought about by the pandemic and geopolitical shocks, rather than a result that could solely be influenced by monetary policy.

The most surprising outcome was that this unprecedentedly aggressive rate hike did not trigger the widely anticipated economic recession.

By the end of 2024, the U.S. economy's annual growth rate remained at 2.5%, with inflation significantly falling without raising the unemployment rate, and the labor market maintained a state close to full employment. The recession that almost the entire economics community had predicted never materialized.

Powell himself admitted in Harvard's economics class that the nearly impossible “soft landing” was one of his proudest achievements.

A Legacy of Both Legacy and Controversy: Independence is the Greatest Legacy

The ultimate historical evaluation of Powell may not rest on any specific economic indicators but rather on a more fundamental question: he preserved the independence of the Federal Reserve.

Trump frequently criticized Powell for his reluctance to cut interest rates during his first presidential term and even considered dismissing him. After Trump returned to the White House in 2025, this political pressure escalated into open conflict — the White House instructed the Department of Justice to conduct a criminal investigation into Powell on the grounds of budget overruns in the renovation project of the Federal Reserve Board headquarters, a first in the 112-year history of the Federal Reserve.

Analysts generally believe that the real motive behind this investigation was to force the Federal Reserve to lower interest rates to align with Trump’s political agenda.

In the face of this unprecedented political pressure, Powell released a video statement in January 2026 openly countering it, defining it as “the Federal Reserve sets interest rates based on what is best for the public, not as a consequence of being subservient to presidential preferences.” This video quickly spread widely in the financial community, winning him support from both sides of Congress and allowing him to conclude his term in a historic manner on his own terms.

Historically, the last time a Chairman faced such intense political pressure dates back over fifty years: Nixon pressured then-chairman Arthur Burns to maintain loose monetary policy, ultimately resulting in uncontrollable inflation during that era. In contrast, Powell's ability to withstand pressure and refuse to compromise clearly places him in a significantly higher historical position than his yielding predecessor.

Full employment is another noteworthy legacy of Powell's tenure.

During Powell's term, the average monthly unemployment rate was 4.6%, lower than Greenspan (5.5%), Bernanke (7.3%), and Yellen (5.1%). Behind these figures are real improvements in people's livelihoods: the low unemployment rate disproportionately benefited the most vulnerable groups in the labor market — from 2019 to 2024, the cumulative increase in real wages for workers in the bottom 10% of the income distribution reached 15.3%; the Black unemployment rate dropped to 4.8% in 2023, setting a historic low.

Researcher Dean Baker wrote that Powell's serious execution of the full employment goal allowed millions of workers who could have been unemployed to retain their jobs, and tens of millions of people received wage increases that would not have otherwise occurred.

Powell's critics also have plenty of grounds for their arguments.

In terms of regulation, the sudden collapse of Silicon Valley Bank in 2023 exposed the Federal Reserve's laxity in bank regulation. Baker bluntly stated: “He has serious deficiencies in regulation, allowing the situation to reach a point where bailout of Silicon Valley Bank became necessary.”

Regarding inflation, the average inflation rate during Powell's term was 3.09%, exceeding the Federal Reserve's 2% target by more than one percentage point, and was higher than during the terms of Greenspan (2.5%), Bernanke (1.84%), and Yellen (1.17%). Upon leaving office, the Federal Reserve's balance sheet was still about $6.7 trillion, more than doubled since he took office, with his successor Kevin Warsh listing this “legacy burden” as a primary target for remediation.

The low unemployment rate and high inflation represent the two sides of this dual report card he presents to history.

He himself described the essence of this work with a single phrase: “We are building a dam, not preventing a hurricane.”

This is both a modest expression of the Federal Reserve's functional boundaries, and a self-annotation of his eight years — not to say he foresaw everything, nor to say he never made mistakes, but rather that in the most turbulent times, he tried to build this institution strong enough that it would not be completely destroyed by the political winds, the pandemic rains, and the floods of inflation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。