Dalio said we are standing on the eve of a reconstruction of the world order. Regardless of whether you agree with this judgment, one thing is becoming increasingly difficult to ignore: when war, sanctions, and blockades occur simultaneously, which channel will funds choose?

In the previous article, "Whose Dollar? USDT in Hormuz and the Disordered Dollar System", we tracked the path of the dollar in disorder—it remains the pricing currency of the world, but its authorization is being circumvented. USDT parasitizes on the dollar's price but does not go through the financial channels of the dollar. An unlicensed dollar is growing in the cracks.

In this article, we look at another path: the renminbi. It is not a shadow of the dollar, nor is it a parasite. It has its own channels, its own clearing system, and its own national backing. But it also faces a problem that the dollar never had—most people want it but cannot obtain it.

On a night in March 2026, a fully loaded tanker slowed down in the narrowest part of the Strait of Hormuz. A Persian instruction came over the radio: stop the ship, pay the fee, or no escort will be provided.

The rate is 1 dollar per barrel. A fully loaded VLCC, $2 million per trip. Accepts USDT, Bitcoin, and Renminbi. Does not accept dollars.

This waterway, which carries nearly one-third of global oil transportation, became a toll station that spring. Behind the anxious phone calls and encrypted messages, a previously rarely discussed issue suddenly became urgent:

If you can't settle in dollars, what else can be used?

A Greek shipowner running routes between the Mediterranean and the Persian Gulf just completed a toll payment with USDT—a dollar-pegged digital currency. $2 million, with on-chain transfer, received in ten minutes—an operation he was already familiar with. But immediately after, the partner sent a second message: next time, you could also try settling in Renminbi.

He stared at the screen for a long time. His company is registered in Athens, with clients across the Middle East and Europe. He has no Chinese clients, no Renminbi account, and is not even sure which bank in Greece could open one.

He asked a question that seemed very simple:How can I obtain Renminbi?

Most people are debating "Can Renminbi replace the dollar?" But maybe this question is wrong. A more practical question is: Can a person who wants to use Renminbi obtain it right now?

The answer to this question is far more complicated than he imagined.

1. The World's Largest Trading Nation and the Most Difficult Currency to Buy

An intuitively non-existent fact:

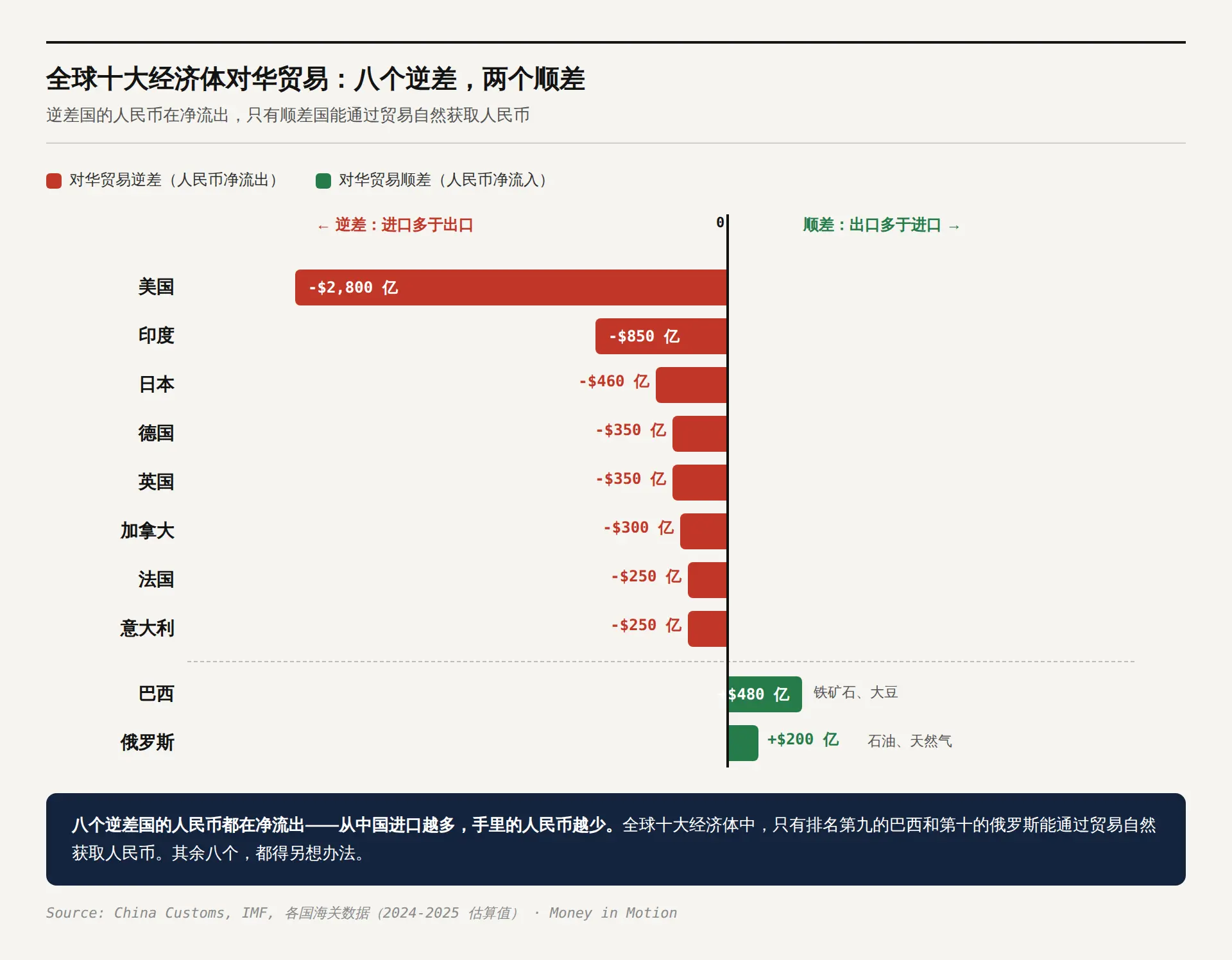

China is the world's largest trading nation, but the Renminbi is one of the most difficult major currencies to buy globally.

In 2025, China's trade surplus reached $1.19 trillion—China earns over a trillion dollars a year from the price differences of goods worldwide. However, in the statistics of global cross-border payments, the Renminbi only accounts for 3%. Money is made but spent less. The surplus remains in China, and the world cannot obtain it.

If you want to get Renminbi, there is only one normal path:Do business with China and earn Renminbi. However, among the top ten economies in the world, only Brazil and Russia have a trade surplus with China. The other eight all have trade deficits—America has an annual deficit of $280 billion, while Japan, Germany, India, the United Kingdom, France, Italy, and Canada are all net buyers. Renminbi flows out of your hands, not into them.

So what about buying in the financial market? The world's largest offshore Renminbi pool is in Hong Kong, approximately 80% of offshore Renminbi payments pass through there. But the pool is surprisingly shallow—the total Renminbi deposits in the global offshore market amount to about 1.6 trillion, while China's annual trade surplus exceeds 8 trillion Renminbi. The entire pool is not enough to cover the surplus.

Moreover, the pool is being drained. Three years ago, only 20% of the Renminbi deposited in Hong Kong banks was loaned out. By mid-2025, this ratio skyrocketed to over 90%—almost all the money that came in was lent out.

At the Canton Fair in autumn 2025, a manager from an electric tricycle company in Jiangsu stated to reporters, "Many foreign customers are now actively choosing to settle in Renminbi. It’s not us initiating it; it’s the customers who brought it up." The number of customers opting for Renminbi, he said, has approximately doubled.

Demand is rising, but the pool can't keep up. In October 2025, the Hong Kong Monetary Authority launched a liquidity injection tool of 100 billion, which was quickly snatched up by 40 banks. Three months later, the quota was urgently doubled to 200 billion—funds flowed through Hong Kong as a hub to ASEAN, the Middle East, and Europe. But these are ultimately just emergency measures.

The fundamental reason for the stagnation of the pool's growth lies in a structural characteristic of the Chinese economy:China is a surplus country, and Renminbi returns to China through trade rather than flowing out. Why is the dollar everywhere? Because the United States is a deficit country—each year buying hundreds of billions of dollars worth of goods, the dollar is distributed globally with the deficit. You can exchange dollars on the streets of Lagos and spend dollars at the night markets of Bangkok. The Renminbi is precisely opposite, with the surplus staying within.

Bloomberg quoted a commodity trader in March. His company had been settling Middle Eastern crude oil in dollars for the past decade, but for the first time this year, a customer requested payment in Renminbi. He spent three weeks researching how to do it, concluding that opening an account would take six to eight weeks, and his ship couldn't wait.

"It's not a technical issue," he said. "It's because you have no channels."

A trillion-dollar pool struggles to catch global demand.

2. Gold Bars from New York to Shanghai

Returning to that shipowner. He asked how to obtain Renminbi, and the intermediary responded with one word: gold.

This is not just a metaphor.

Arthur Hayes—one of the most famous macro analysts in the cryptocurrency world—described a chain in an article in April 2026:

Countries sell US Treasuries → Buy gold with dollars → Ship gold to Switzerland for re-refining → Deliver to the gold market in China → Exchange for Renminbi → Transfer via China's cross-border payment system to Iran.

(Gold-Backed Stablecoins Explained: How They Work and the Top 5 to Watch)

I took some time to break down this chain. The conclusion is: each link exists individually, but the causality between links is inferred, not evidenced. However, each individual link is supported by data. Ultimately pieced together, they form a relatively complete picture:

In the spring of 2026, the non-monetary gold exports from the US became the largest export category in America for several months in a row. It's not chips, not airplanes, not soybeans—it's gold bars. Financial analyst Luke Gromen reviewed twenty years of US trade records, noting that this pattern had never appeared before.

Most of this gold flows to Switzerland. Switzerland has four of the world's largest gold refineries—Valcambi, Argor-Heraeus, PAMP, Metalor—where they perform a very simple task: melting the gold bars from around the world and re-refining them into the one-kilogram standard preferred by China. In 2023, the largest buyer of Swiss gold exports was China, amounting to 25.1 billion Swiss francs. In March 2026, Swiss gold exports to China increased by 18% month-on-month.

In the same month, the People's Bank of China announced it had increased its gold holdings for the 15th consecutive month. The official holdings reached 2,308 tons.

The main reason for the gold flowing out of America is actually the unwinding of 2025 COMEX arbitrage trades—during the tariff panic, 43.3 million ounces of gold surged into New York storage, and now it is starting to flow out. This is primarily a commercial action.

However, these data point in one direction:

Gold is flowing from the West to the East, and it is taking on the role of a translator between two incompatible financial systems by the most primitive value transmission method.

The assets you hold in the dollar world are first converted into a universally recognized "intermediate format"—gold—before being imported into the Renminbi world.

Eighty years ago, when the Bretton Woods system was established, international settlements were done this way. Eighty years later, under the pressure of sanctions and blockades, humanity has returned to the era of transporting metal.

3. An Emerging Channel—CIPS

Gold is a transitional solution. The real long-term solution is a payment channel that most Chinese people are not very familiar with.

First, let's talk about what everyone knows. SWIFT—the "text message system" between banks globally. When you transfer money from China to Japan, SWIFT tells the Japanese bank: "A sum of money is coming from China, how much it is, and who the payer is." SWIFT itself does not move money; it transfers information. But precisely because it delivers information, whoever controls SWIFT can see the details of every cross-border transaction globally.

CIPS is another system built by China—the Cross-Border Interbank Payment System. Unlike SWIFT, it can both send messages and move money, integrating messaging with clearing and settlement. Most of the time, CIPS still uses SWIFT to send messages—about 80% of transactions do so. But the key is that it can operate independently. When it needs to operate independently, CIPS can send messages and move money by itself.

(CIPS to Launch Yuan-Denominated Letter of Credit Service during Lujiazui Forum)

In 2012, the People's Bank of China initiated the construction of CIPS. Three years later, on October 8, 2015, the system officially went live. On that day, 19 banks were connected, and not many globally paid attention. The first transaction completed on the launch day was the Industrial and Commercial Bank of Singapore clearing 35 million Renminbi for a company to Shanghai Baosteel. On the same day, Standard Chartered Bank completed a Renminbi transfer from China to Luxembourg for IKEA via CIPS.

A Singaporean trader and a Swedish furniture company were the first users of CIPS.

By the end of 2025, CIPS had grown to 193 direct participants and 1,573 indirect participants, covering 124 countries and regions, processing $26.4 trillion throughout the year. From 19 to 193, it silently grew tenfold. The list of shareholders of CIPS itself is quite telling—16% is owned by the central bank, while the remaining shareholders include UnionPay, major state-owned banks, as well as HSBC, Standard Chartered, Citibank, DBS, Societe Generale, and ANZ. This is not a closed system but a hybrid led by China, with Western banks participating.

Moreover, expansion is accelerating. In early 2026, the First Abu Dhabi Bank in the UAE joined CIPS, becoming the first Renminbi clearing bank in the Gulf region—formerly, using Renminbi for settlements in the Middle East required routing back to banks within China; now it can be completed directly in Dubai.

The head of DBS Bank in China once told the media: "Companies have clear business reasons to use Renminbi—optimizing cash management, reducing foreign exchange costs, and diminishing uncertainty."

This is not a geopolitical slogan. This is a businessman doing the math.

The Greek shipowner might not be able to purchase Renminbi today, but it doesn't mean he won't be able to do so in three years. Channels are being carved out, one by one.

4. What Can't Be Bought and What Can't Be Returned

The shipowner ultimately did not manage to obtain Renminbi. It was too slow. Opening an account would take weeks, compliance checks another few weeks, and his ship couldn't wait. He still paid with USDT.

But he did one thing. After returning to Athens, he asked the company’s financial director to study how to open a Renminbi account in Hong Kong. Not because he needed it today, but because he didn’t want to face an option he could not choose next time.

He is not choosing a side. He simply realized that being on a track with only one path makes one too vulnerable in this world. Opening an additional account and accessing another channel is not due to distrust of the dollar—but because those who have only one path to walk down do not walk with ease.

The batch of gold flowing out of America is currently being re-refined in Swiss refineries. It will be transformed into one-kilogram standard gold bars in Shanghai's delivery warehouses and then turned into a sum of Renminbi, flowing into a certain channel. Perhaps it will be a payment for a Chinese company in the Middle East, or a routine payment for a Shenzhen factory importing Australian iron ore.

What cannot be bought is the reality of Renminbi at this moment, and what cannot be returned are those dollar channels that might be disrupted tomorrow.

And those who have already found an entrance will not look back.

At least, that shipowner will not.

The character of the shipowner in this article is based on real cases from multiple public reports, and does not represent any specific individual or enterprise.

Citations and references: Citrini Research "Strait of Hormuz: A Citrini Field Trip" (April 2026); Arthur Hayes "No Trade Zone" (April 2026); Atlantic Council GeoEconomics Center; TRM Labs; Fortune; Luke Gromen, FFTT; Wells Fargo; Swiss Federal Customs Administration; World Gold Council; CIPS official data; China's Ministry of Commerce blocking order announcement (May 2, 2026); Bloomberg; Financial Times; CNBC.

Related reading: Whose Dollar? USDT in Hormuz and the Disordered Dollar System

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。