The shared pool model exposes shortcomings; why are institutions collectively turning to Morpho to isolate the market?

Written by: Vaidik Mandloi

Translated by: Saoirse, Foresight News

All lending protocols in DeFi operate on similar underlying principles: users deposit stablecoins or Ethereum into a shared liquidity pool, and borrowers withdraw funds after collateralizing their assets; decentralized autonomous organizations (DAOs) vote on which assets can be used as collateral and the corresponding collateralization ratios. Aave has developed a deposit volume reaching $50 billion based on this model. Throughout most of DeFi's development, this has been the only prevalent model in the industry, and its rationality has never been truly questioned.

However, on April 18, 2026, a hacker exploited a vulnerability in the LayerZero cross-chain bridge of the Kelp DAO project to forge $292 million worth of rsETH tokens. The hacker deposited these fake tokens into Aave as collateral and borrowed real Ethereum. Within just a few hours, the utilization rate of funds in Aave's major lending markets reached 100%, meaning all available funds in the protocol were borrowed. Over the next three and a half days, the platform lost $15 billion in deposits. Ultimately, Aave had to collaborate with various parties in its ecosystem to raise $160 million to cover the losses.

While the vulnerability originated from the Kelp DAO project, the root cause of such enormous losses lies in Aave's governance mechanism. As early as January of this year, the community voted to increase the collateralization ratio of rsETH to 93%, leaving only a 7% risk cushion for that type of asset. This decision triggered one of the largest bank runs in DeFi lending history.

On the same day, some of the forged rsETH tokens also entered Morpho, the second-largest lending protocol in DeFi. However, the risk exposure was only $1 million and was spread across two independent small isolated markets, preventing a chain crisis.

I conducted a thorough investigation into the matter and found that this event is far from just a simple security attack.

The Core Differences Between Two Models

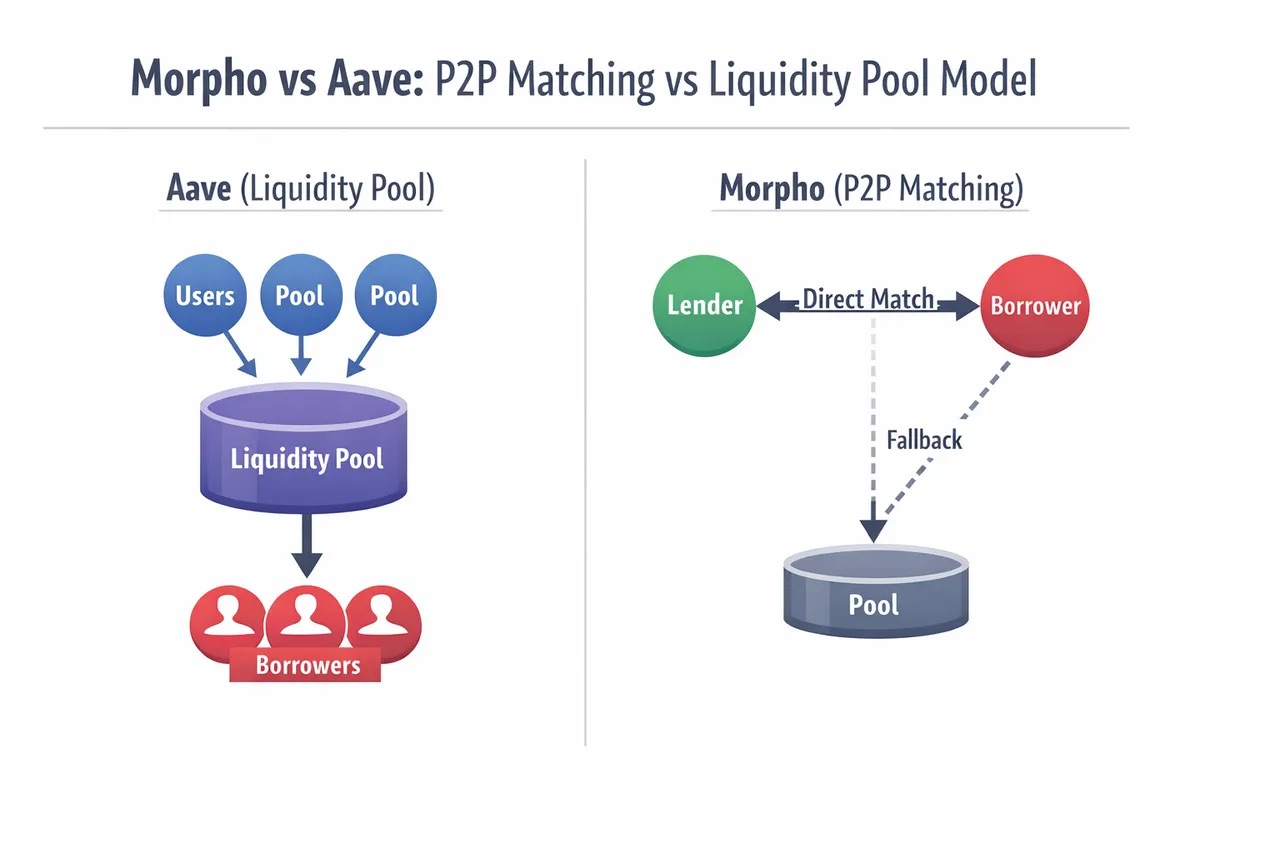

To understand why Aave lost tens of billions of dollars while Morpho remained almost unharmed, one must first clarify the operational logic of the two types of protocols regarding fund storage and operation.

When you deposit USDC into Aave, the funds flow into a single main liquidity pool used to support borrowing operations for all community-approved assets like Ethereum and staked tokens. Deposit users cannot independently choose the type of collateralized assets for their funds; all related rules are determined by DAO voting. Therefore, when the rsETH collapses, even ordinary users who only deposited USDC or have never interacted with rsETH find their assets frozen — everyone's funds are in the same risk pool, experiencing mutual damage.

Source: BingX

More critically, during the market suspension, when users could not withdraw funds, Aave's governance tier even lowered the interest rates for the frozen Ethereum lending market with the aim of protecting borrowers leveraging rsETH. Since deposit rates are directly linked to borrowing rates, low-risk depositors ultimately saw their returns shrink further.

In traditional credit systems, the lowest-risk lenders enjoy priority for repayment. But Aave has completely inverted this rule. The reason for this is that borrowers participating in rsETH leveraged trading are also the most active voting group in community governance. Once a risk erupts, the high-risk participants holding governance authority naturally prioritize their own interests.

Aave introduced an insurance mechanism called Umbrella at the end of 2025, attempting to address such bad debt risks. Users could stake Ethereum, and when a bad debt event occurred, the staked assets would be used for compensation. However, after the Kelp DAO crisis broke out, out of 23,507 staked aWETH, 18,922 entered the un-staking waiting period, with nearly 80% of the insurance pool funds concentrated in withdrawal.

This mechanism ultimately failed completely. On-chain insurance relies on voluntary user participation, and when real risk arrives, fund providers will inevitably choose to exit — after all, their assets only face substantial losses when crises occur. This leads to insurance often existing when nothing is wrong, but becomes ineffective when truly needed.

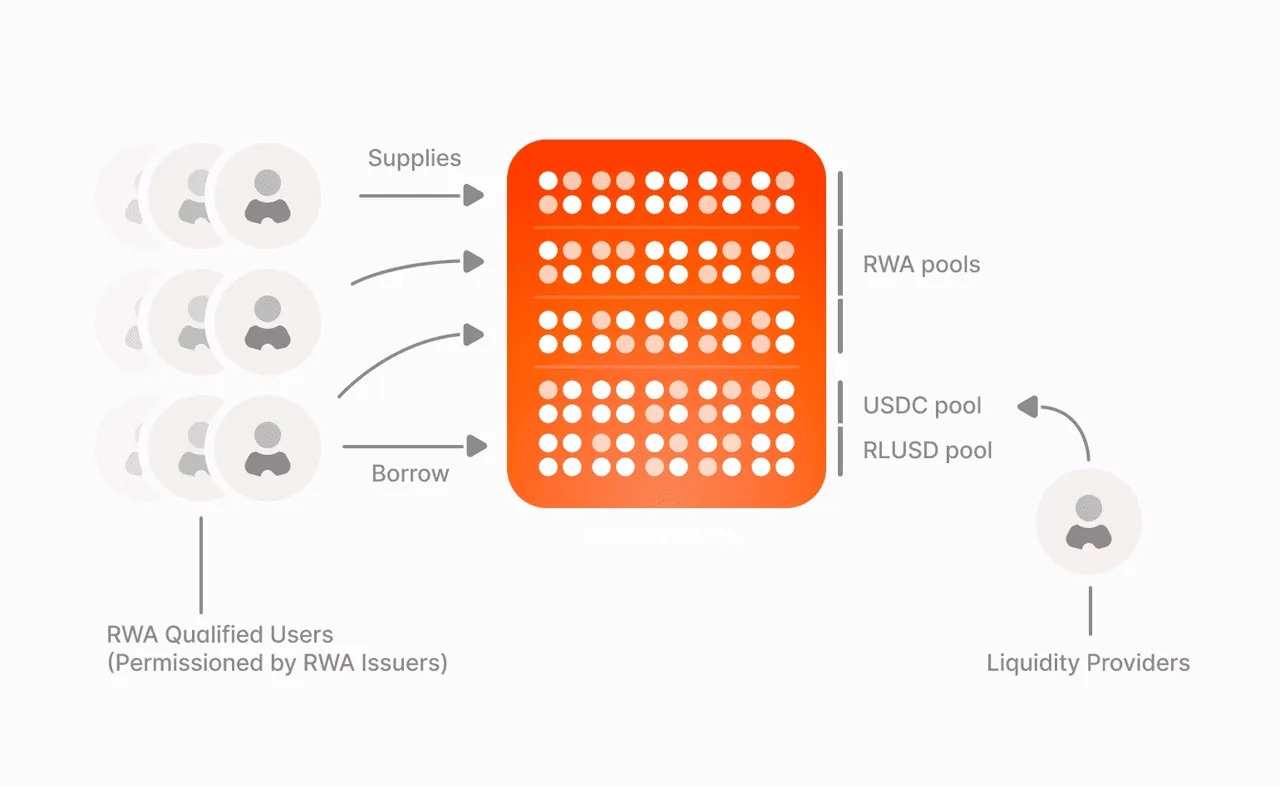

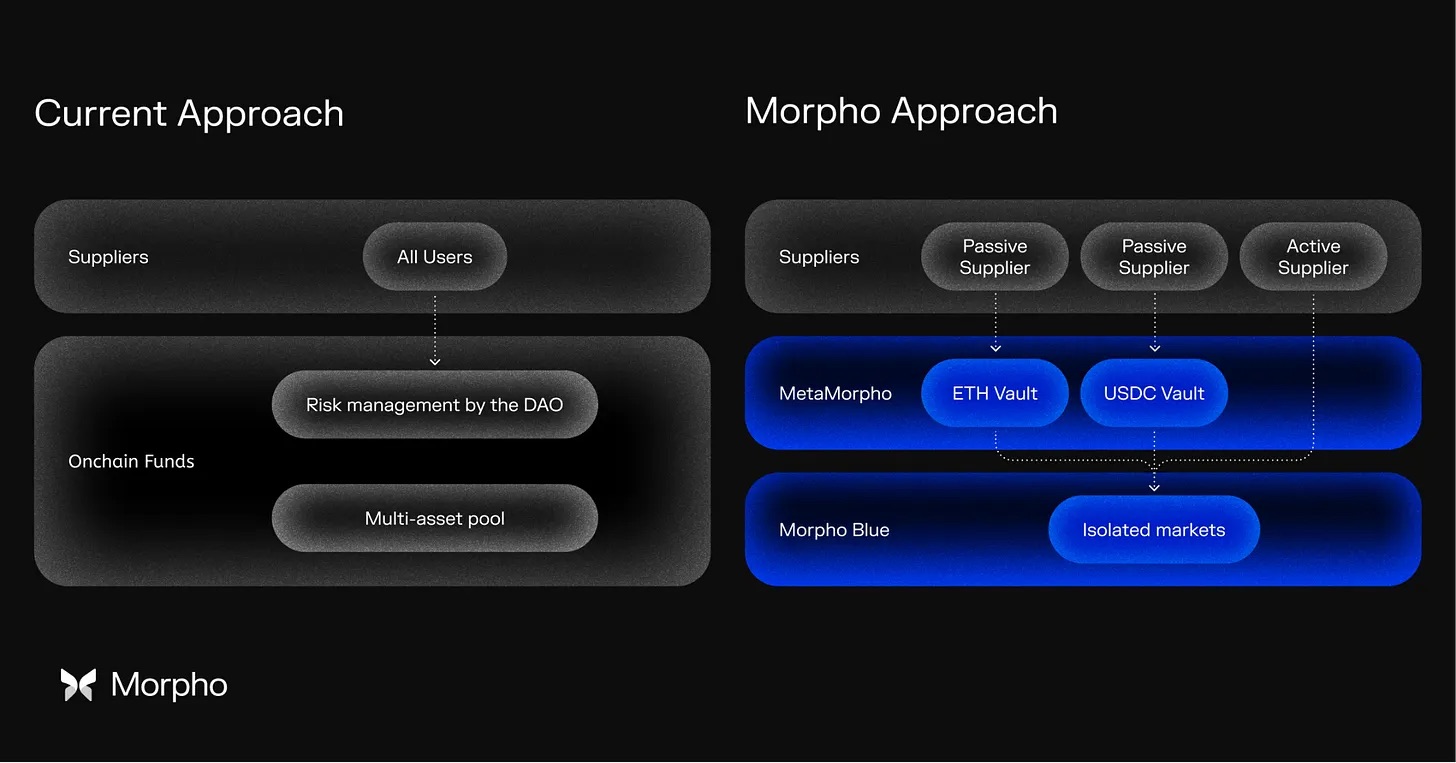

Morpho's operating model is entirely different. It discards a unified shared liquidity pool; anyone can create independent isolated lending markets and preset their borrowing assets, collateral assets, price oracles, and interest rate models. Once parameters are deployed, they cannot be modified. If one wishes to adjust the risk level, a new market must be created.

Underlying structural differences between traditional DeFi lending models (represented by Aave) and Morpho's "morphological method."

Furthermore, Morpho introduces independent risk control institutions (managers), such as Gauntlet and Steakhouse Financial. These institutions set up funds and allocate them to different markets based on their evaluations while receiving performance-related fees; if losses occur, the losses are limited to their own funds. Gauntlet has also provided risk control suggestions for Aave, but within the Aave system, their professional opinions are often voted down by token holders seeking high yields, while Morpho fundamentally eliminates this issue.

The Overlooked Hidden Costs

Aave and Morpho are currently the two most widely used lending models in the crypto space: Aave employs a shared liquidity pool model where all deposits are pooled together, and risk rules are determined by community voting; Morpho focuses on the isolated market model, where each group of lending transactions is independently controlled by specialized institutions.

The Kelp DAO vulnerability exposed the flaws and defects of the shared pool model. However, even during stable periods without security incidents, this model has a long-overlooked hidden cost. The three core markets on the Ethereum chain (Ethereum, USDT, USDC) contribute to 89% of Aave's lending volume. In these three markets, deposit rates are consistently 25% to 35% lower than borrowing rates. The difference essentially reflects idle funds sleeping in the liquidity pool, where depositors cannot profit from it, while borrowers still bear the full borrowing cost.

With the interest rate mechanism relying on fund utilization rates, it can raise rates during heightened risk but cannot mobilize idle funds during periods of low demand; a large volume of assets remains stuck in the pool without generating returns. Just among these three markets, the value loss due to idle funds annually reaches $52 million, close to a quarter of Aave's annualized earnings in a single quarter. Even eliminating reserve requirements and waiving platform fees does not resolve the idle funds issue — this is an inherent shortcoming of the shared pool structure.

Morpho's interest rate model aims to maintain fund utilization at 90%, significantly higher than Aave's range of 60% to 80%. The reason this model can withstand high utilization is that deposits within the platform are not used as collateral for other loans, thereby avoiding the risk of cascading liquidations from the source, and does not require reserving large amounts of funds as a risk buffer. When borrowing demand is high and funds are borrowed extensively, rates automatically rise to attract more depositors; when borrowing demand is low, rates fall, stimulating borrowing. The entire system achieves dynamic balance without needing community voting.

Source: Gate.com

Actual data also confirms its advantages: even after deducting management fees, the returns to depositors from Morpho's leading USDC pools exceed those from Aave and Compound. Currently, Morpho's loan-to-deposit ratio is 41%, while Aave's is 39%, and the former's volume reaches several billion dollars, with profit advantages accruing daily to all depositors on the platform.

Institutional Choice: Who is More Trustworthy?

Surprisingly, all crypto asset lending operations under Coinbase are built on Morpho. The related loan scale has surpassed $2 billion, and over 100 million users on the platform are indirectly enjoying the financial returns brought by Morpho.

The vast majority of users are even unaware that they are using DeFi services. Coinbase has neither developed its own lending system nor chosen other platforms; the core reason lies in Morpho's underlying architecture, allowing platforms to independently set risk control parameters and select cooperating risk control institutions, fully controlling the overall product experience.

Apollo Global Management, a firm with over $1 trillion in assets under management and 30 years of experience in private credit, recently signed a four-year cooperation agreement, planning to acquire up to 90 million MORPHO tokens, representing 9% of the total token supply. The organization plans to use its tokenized fund assets as collateral to access the Morpho platform, with Highlight responsible for managing the fund and conducting market stress tests.

Moreover, Anchorage Digital, the first native crypto bank in the U.S. to obtain a federal charter, has also accessed the Morpho fund for its multi-billion dollar institutional clients; SG-FORGE, the compliance arm of Société Générale, is the first licensed bank to implement DeFi lending through Morpho.

These strictly regulated traditional financial institutions collectively chose Morpho with a common demand: the isolated market model enables them to meet their compliance and risk control requirements without relying on DAO decision-making. In contrast, Aave's market rules are all subject to community voting and are completely incompatible with institutions' need for independent control.

Changes in the regulatory environment further amplify this trend. The U.S. "GENIUS Act" stipulates that stablecoin issuers must not directly distribute financial returns, meaning that stablecoin organizations need neutral underlying infrastructure to activate massive existing assets. Relevant forecasts indicate that by 2028, stablecoin reserves directed toward U.S. Treasury securities will surge from the current $120 billion to over $1 trillion. This enormous capital urgently needs a lending foundation that allows asset holders to independently manage risks, and Morpho is currently the most fitting choice.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。