Author: Chloe, ChainCatcher

In the past decade, the expansion logic of cryptocurrency exchanges was “first users, then compliance.” But this logic was completely reversed in 2026; now, what truly makes a difference is the compliance dividends brought by licenses.

With the end of regulatory arbitrage, how will Binance, OKX, Bitget, Bybit, and Gate compete for the next round of entry tickets with completely different strategies?

The New Battlefield for Exchanges in 2026: Compliance Dividends

According to the annual derivatives market report released by CoinGlass in 2025, the total trading volume of centralized exchanges in derivatives for the whole year reached 85.7 trillion USD, with an average of about 26.45 billion USD per day, and the market share is highly concentrated, with the top five exchanges accounting for over 80% of the open contracts. In such a market scale, any leading exchange cannot continue to grow simply by offering “lower fees” or “more varieties of coins,” as the marginal utility of these advantages is diminishing.

Market Position and Current Ranking of Five Exchanges

Before diving into license assessments, let’s look at the relative positions of these five exchanges in 2026 using data.

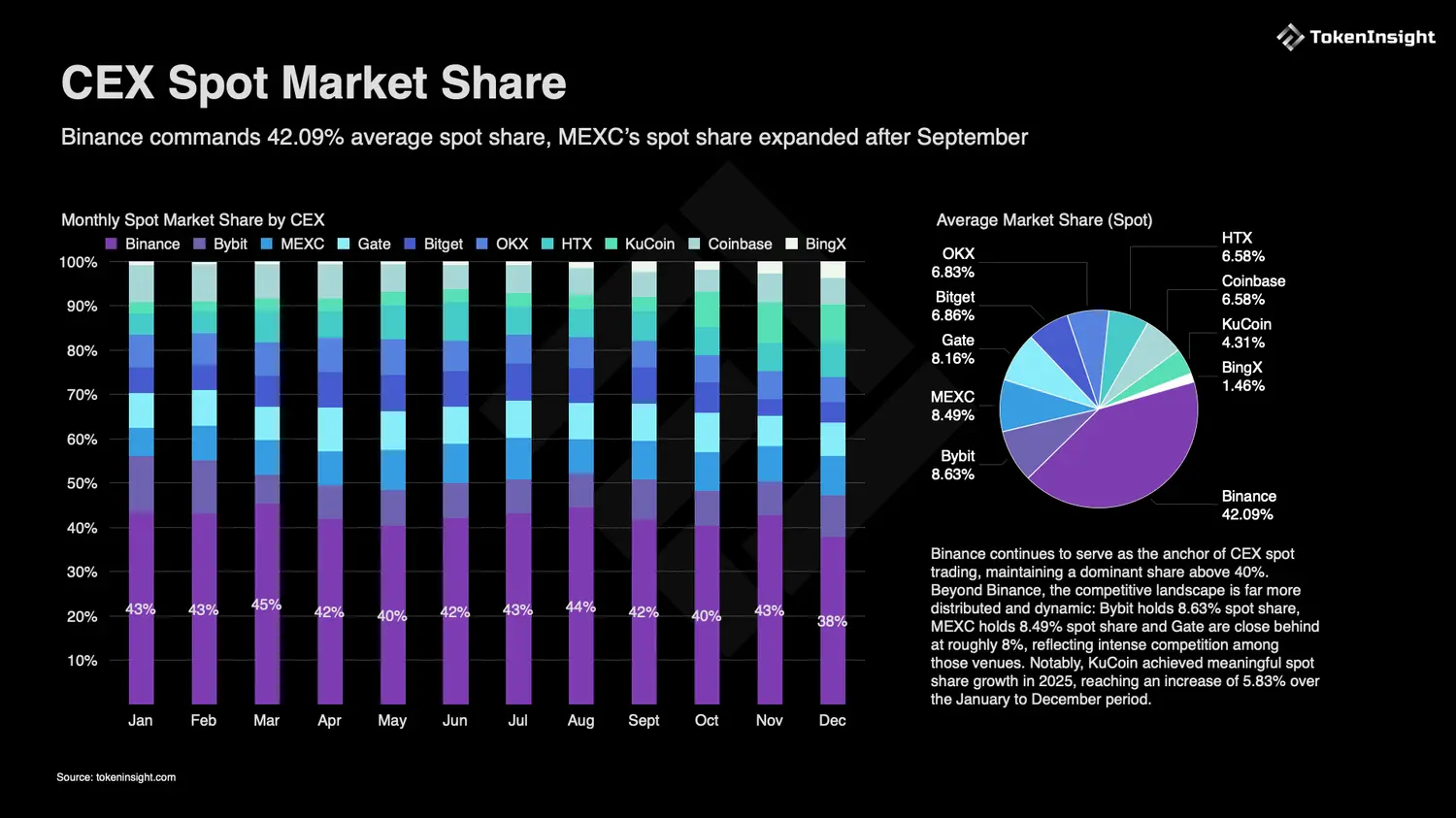

According to the 2025 annual report from TokenInsight, the distribution of spot market share throughout the year is as follows: Binance 42.09%, Bybit 8.63%, MEXC 8.49%, Gate 8.16%, Bitget 6.86%, OKX 6.83%, Coinbase 6.58%, KuCoin 4.31%

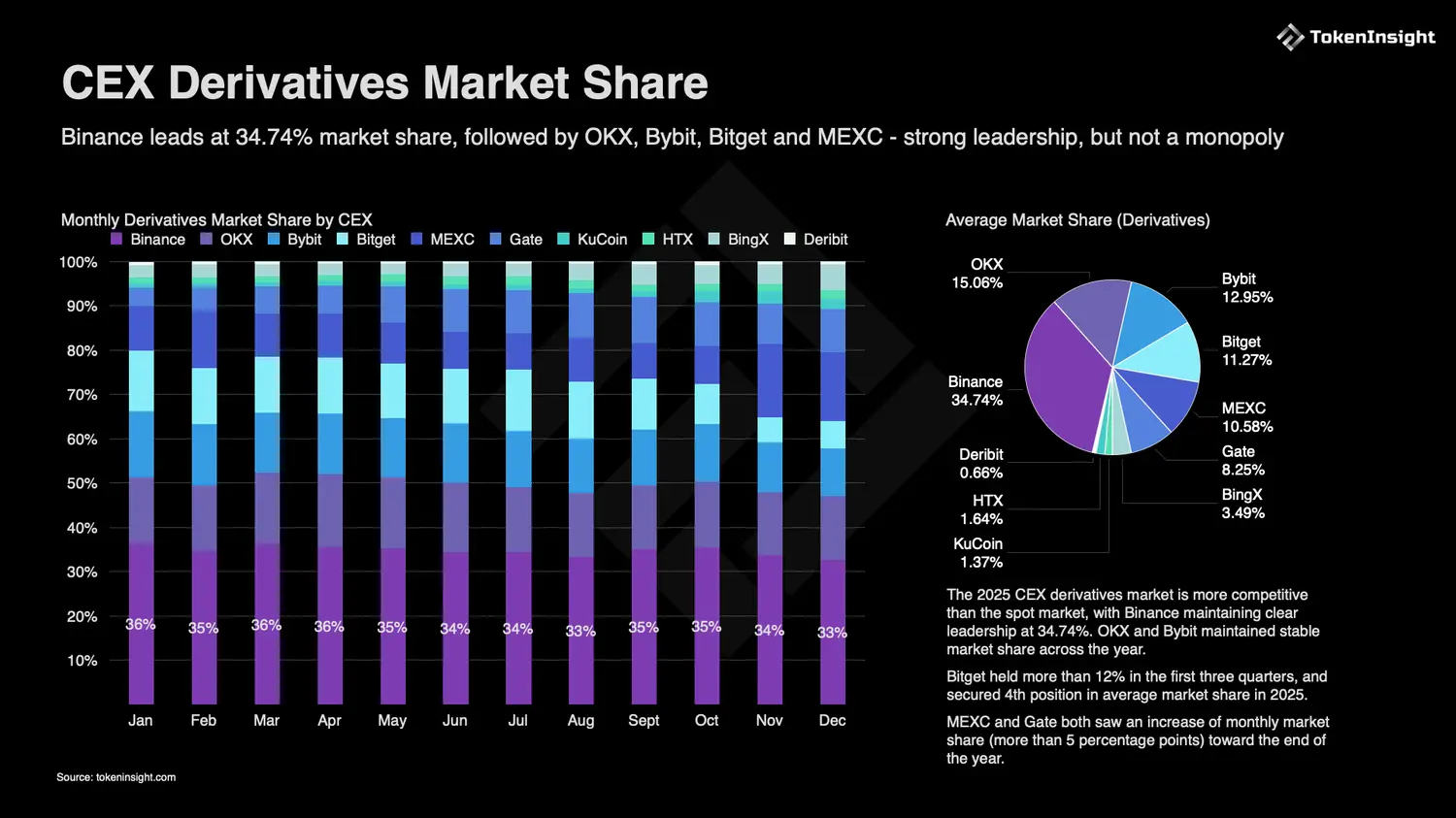

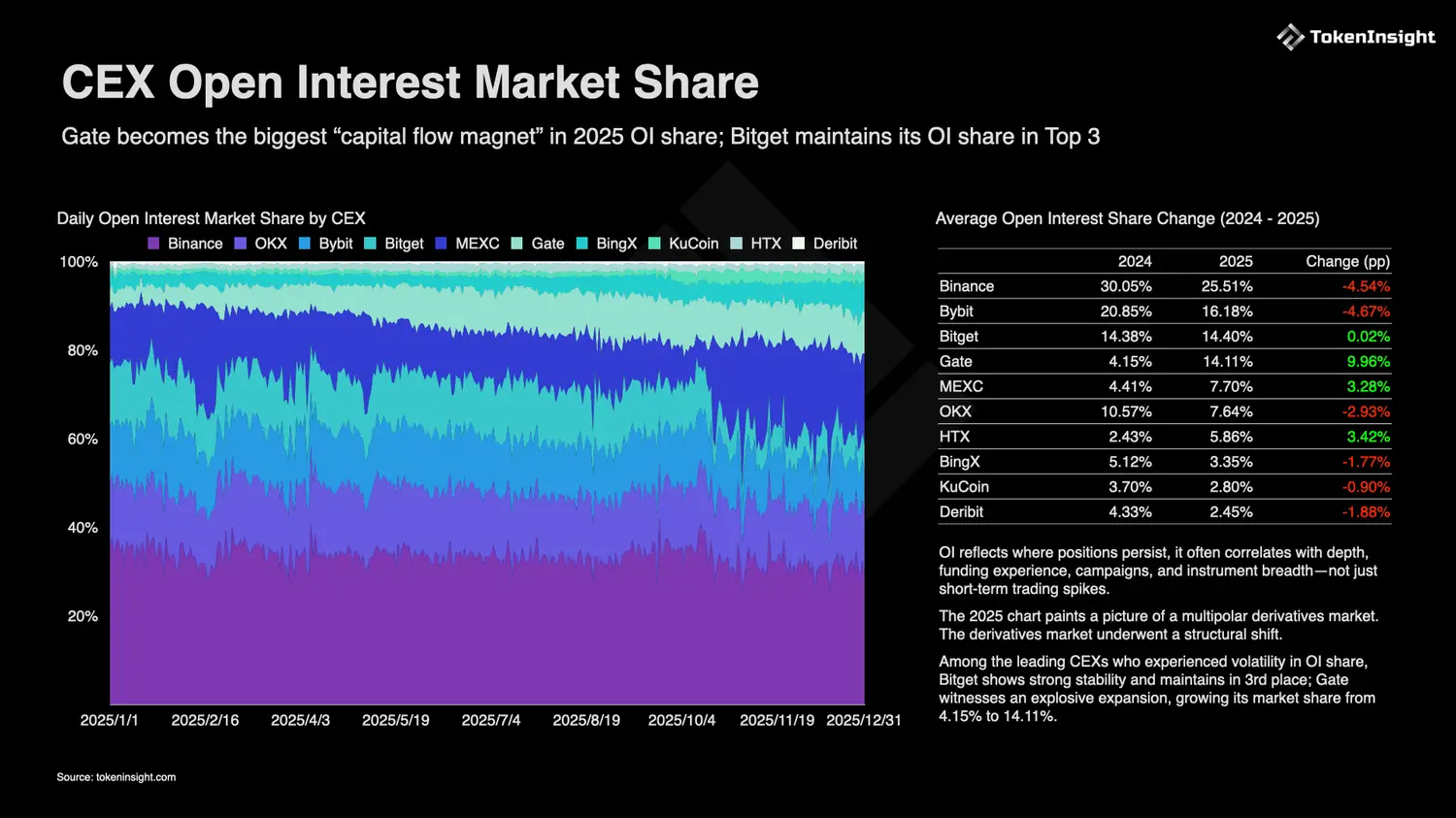

The pattern in the derivatives market shows slight differences. Data reveals that Binance maintained the top position with an average market share of 34.74% for the entire year of 2025, followed by OKX at 15.06%, Bybit at 12.95%, Bitget at 11.27%, and MEXC and Gate at 10.58% and 8.25%, respectively.

These two groups of data indicate that apart from Binance, which has an absolute advantage in both the spot and derivatives markets, the shares of the other four are actually closely contested. As the market scale expands and the distribution stabilizes, whoever can obtain licenses for key markets has the opportunity to move up a level in the next round of reshuffling.

It is worth noting that these five leading exchanges maintain a leading position in terms of compliance transparency as well. According to data from the crypto asset data platform RootData, Binance, OKX, Bybit, Gate, and Bitget continue to rank in the top five in the eighth issue of the “Cryptocurrency Exchange Transparency List (Stock Type)” released by the Web3 asset data platform RootData, which highly aligns with the patterns of spot and derivatives market shares. This list continuously focuses on the growth trends of stock assets in cryptocurrency exchanges.

Binance: The Absolute Leader's Compliance Shift

Binance is the only player on this list that does not need to worry about market share, but it has also borne the brunt of regulatory pressure.

Between 2023 and 2024, Binance faced large regulatory fines and settlements with multiple countries in the United States, fundamentally changing the company's strategy. According to a report by Nikkei Asia, Binance's Asia-Pacific head SB Seker stated in March 2026 that Binance plans to obtain five new licenses in Asia within 2026, raising the total number of licensed jurisdictions globally to over 20.

By early 2026, Binance had already obtained regulatory approvals in Asia from Australia, India, Indonesia, Japan, New Zealand, and Thailand, and through the acquisition of a controlling stake in South Korea's Gopax, the South Korean license is also set to enter its territory.

Binance's global scale itself is creating a compliance narrative. According to Binance's 2025 annual report, the number of registered users globally exceeds 300 million, with spot trading volume exceeding 7.1 trillion USD in 2025. At this scale, a ban on Binance in any single country would affect not just local users but also the entire OTC market and stablecoin liquidity. Notably, Binance's licensing strategy differs from other exchanges in that it acquires local licensed entities (such as Gopax) to obtain licenses, instead of applying from scratch. This approach shortens timelines but also means that Binance must bear the historical baggage of the acquired entity.

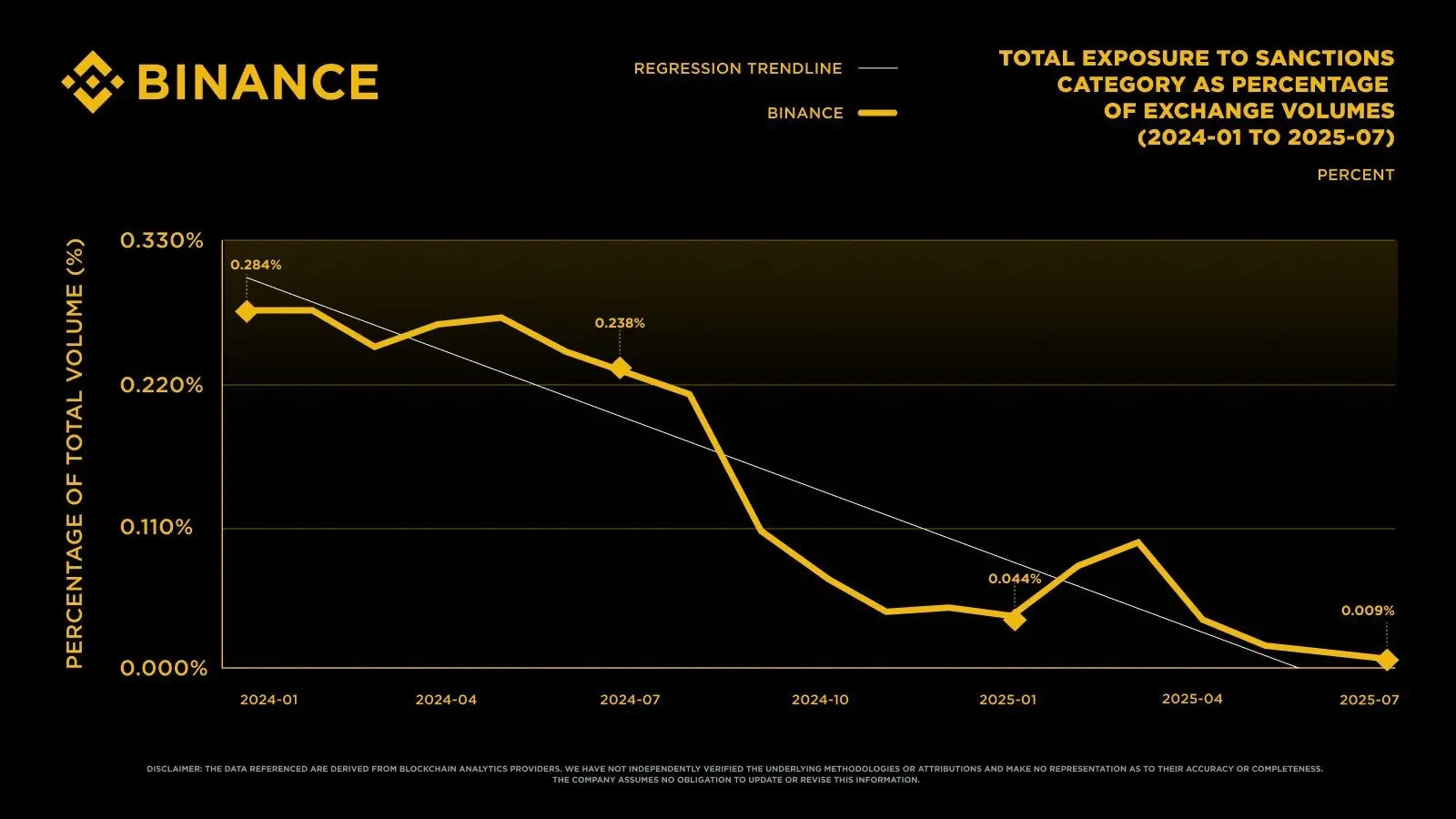

The compliance narrative data for Binance in 2025 will be directly updated in its compliance update reports, showing that the proportion of direct and indirect capital flows related to sanctions fell from 0.284% in January 2024 to 0.009% in July 2025, a drop of 96.8%.

Bitget: A Latecomer Building Licenses from Scratch

Bitget is the last to begin laying out licenses among these five exchanges, but the speed and breadth of acquiring licenses have been quite aggressive. According to a public letter Bitget released in April 2025, signed by Chief Legal Officer Hon Ng, Bitget had then obtained “more than 8 licenses”. By early 2026, Bitget had regulatory registrations in Europe, Asia, the Middle East, Latin America, and Oceania, including Australia, Italy, Poland, El Salvador, the UK, Bulgaria, Lithuania, the Czech Republic, Georgia, and Argentina.

In Asia, Bitget completed registration with VARA (Dubai Virtual Assets Regulatory Authority) at the end of 2025, authorizing it to provide regulated virtual asset services from its Dubai headquarters, and it also obtained a digital asset license in Georgia, establishing Tbilisi Free Zone as a base for Eastern Europe expansion.

In terms of licensing strategy, Bitget is taking the route of “seeking breadth first, depth later,” primarily securing VASP registrations in Europe rather than the complete CASP license under MiCA; it has not yet obtained full licenses for Japan, Hong Kong, and Singapore, which are the most prestigious markets. Perhaps the challenge for Bitget is that once the number of licenses reaches a certain scale, the market will begin to question “quality”.

Bybit: Swinging Between Setbacks and Breakthroughs

Bybit has the most tortuous licensing path among these five. In May 2024, Bybit exited the Hong Kong market due to regulatory pressure from the Hong Kong Securities and Futures Commission, and its associated entity Spark Fintech Limited officially withdrew its license application. By the end of 2025, Bybit announced it would gradually cease services to Japanese residents in 2026 and required affected users to complete identity verification by January 22, 2026, or they would be treated as Japanese residents and restricted from use. In Singapore, the Monetary Authority of Singapore (MAS) required unlicensed digital token service providers to stop overseas operations by June 2025, and Bybit also halted operations in Singapore.

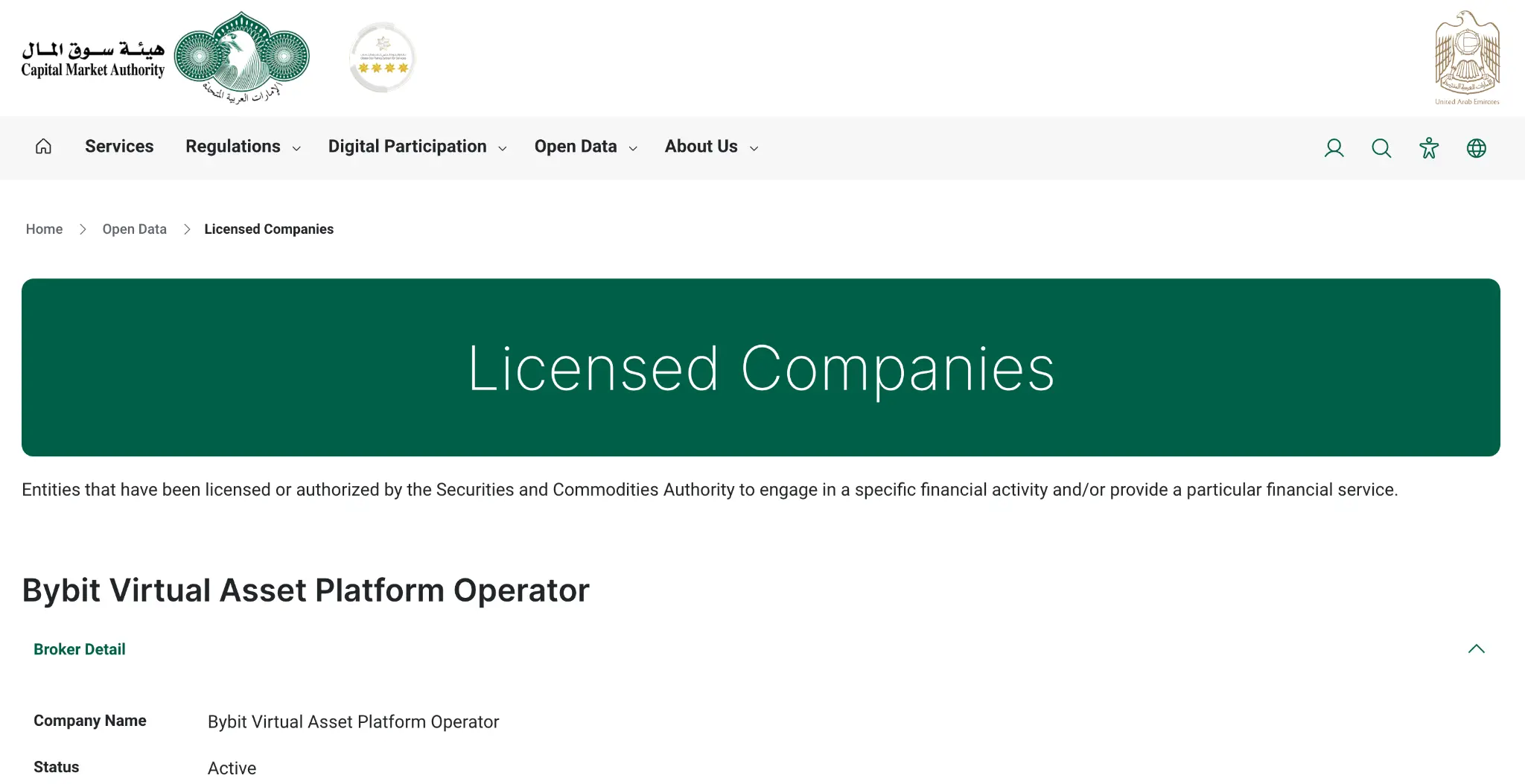

However, on another front, Bybit secured two relatively high-value licenses in the industry. In October 2025, the UAE Securities and Commodities Authority (SCA) granted Bybit its first complete “virtual asset platform operator license,” covering trading, brokerage, custody, and fiat services across all seven emirates of the UAE. In Europe, Bybit EU GmbH obtained a MiCAR license from the Austrian Financial Market Authority (FMA) in May 2025, allowing operations in 29 countries within the European Economic Area.

Additionally, in February 2025, Bybit experienced the largest hacking incident in crypto history, resulting in losses of approximately 1.46 billion USD. This event put immense pressure on Bybit’s compliance and security narrative in 2025 and became one of the triggers for the Japanese Financial Services Agency's consideration of requiring exchanges to establish capital reserves. Bybit's case illustrates one thing: “holding a license” and “being able to continuously hold a license” are two different matters.

Gate: A Quietly Built Compliance Matrix

Gate has less visibility in the Asian Chinese community compared to Binance and OKX, but when looking purely at the details of its licensing coverage, Gate’s layout is surprisingly complete. According to Gate’s published licensing page, by early 2026, Gate had obtained regulatory registrations, licenses, or approvals in more than eight jurisdictions, including Hong Kong, Gibraltar, Malta, Japan, Australia, the Bahamas, Dubai DMCC, and Cyprus.

In terms of regulatory coverage, Gate's strategy is closer to “establishing independent entities in each key jurisdiction and obtaining licenses individually,” rather than “using a headquarter license to operate in multiple countries.” This approach is costlier but also offers stronger resistance to regulatory risks. For example, in Europe, Gate has both VASP registration in Lithuania (earlier EU standard) and a MiCA license from Malta (passport under the new framework), providing dual insurance.

On the other hand, the growth of Gate's share in the Asian derivatives market is particularly noteworthy. Data from TokenInsight shows that Gate's open interest market share grew from 4.15% at the beginning of 2025 to 14.11% by the end of the year; the speed of licensing and the speed of market share growth displayed a high degree of synchronization.

OKX: Compliance Restart Bought with Settlement Funds

OKX's licensing journey experienced a complete restart in 2025. In April 2025, OKX reached a settlement with the U.S. Department of Justice, paying around 505 million USD in fines, and formally resumed operations in the U.S., headquartering in San Jose, California. By early 2026, OKX held currency exchange licenses in over 40 states in the U.S. and registered as a money service business with FinCEN.

In Asia, OKX's licensing distribution is as follows:

Singapore: OKX SG Pte. Ltd. obtained a full major payment institution (MPI) license from the Monetary Authority of Singapore (MAS) in 2024 and appointed former MAS official Gracie Lin as the CEO of Singapore. This license is considered to have high value in Asia due to MAS's strict review standards and slow license issuance pace.

Dubai: OKX holds a VASP license with VARA and is one of the first international exchanges to sign an MOU with VARA and obtain a temporary license.

Europe: OKCoin Europe Ltd. obtained a MiCA license in January 2025, operating out of Malta, allowing operations in 30 countries in the European Economic Area, making it one of the first international exchanges to receive the complete MiCA CASP license.

Australia: OKX Australia Pty Ltd is registered with the Australian Securities and Investments Commission (ASIC).

However, OKX also has significant licensing gaps; in Hong Kong, OKX has withdrawn its VATP license application, and in Japan, as of early 2026, OKX still appears on the restricted services list. In other words, OKX's high-value licenses in Asia are concentrated in Singapore and Dubai, while it has yet to unlock the Japanese and Hong Kong markets.

Its licensing narrative might be “paying the price to re-enter the U.S. and using that price to gain global institutional trust.”

Why Do Some Licenses Have “Low Value”?

Based on verifiable regulatory documents and industry experience, cryptocurrency licenses can generally be classified into three tiers.

First Tier: High-Value Licenses

These licenses are characterized by: the licensing authority belongs to a mainstream financial regulatory system, the application process is lengthy, capital and governance requirements are high, full retail operations are allowed, and they can connect with local banks and fiat channels.

Representatives include:

The complete MPI license from Singapore MAS (held by OKX SG). According to Bloomberg, Singapore issued only 13 crypto licenses in total in 2024.

Hong Kong SFC's Type 1 and Type 7 licenses. By the end of 2024, there were a total of 7 fully licensed virtual asset trading platforms in Hong Kong (4 of which obtained restrictive licenses on December 18), and 7 more with temporary licenses.

Japan FSA’s cryptocurrency trading operator registration. Dubai VARA's complete VASP operational license.

The complete virtual asset platform operator license from UAE SCA (Bybit being the first).

Complete CASP license under EU MiCA.

Second Tier: Medium-Value Licenses

These licenses are characterized by: they can operate legally but have limited business scopes, either the regulatory framework in their jurisdictions is still under construction or the local financial system is relatively small.

Representative cases include VASP registrations from EU member states like Lithuania, Italy, and Poland (many exchanges hold them, but they are typically a stopgap during the MiCA transition period), El Salvador's BSP and DASP licenses, Georgia's digital asset license, and Bulgaria's VASP license.

These licenses are legitimate and real but are relatively easy to obtain, making them insufficient alone to form competitive barriers.

Third Tier: Low-Value Licenses

These licenses are characterized by: the licensing authority may be a small country's financial department, commercial registration body, or free trade zone management unit. The standards may only require basic KYC/AML processes, and the license holder may not enjoy any access to fiat banks or local retail operations. From a credibility and signaling value perspective, these licenses are closer to a “company registration” rather than a “financial license.”

After hierarchical classification, reviewing the licensing performance of these five exchanges yields a clearer picture:

Binance has obtained six high-value licenses in Asia (seven including the soon-to-be-acquired Gopax), which serves as its absolute moat.

OKX has high-value licenses in Singapore, Dubai, and the EU MiCA, but Japan and Hong Kong are absent.

Bybit secured the complete UAE license and MiCAR, but simultaneously faces obstacles in Japan, Hong Kong, and Singapore, presenting a polarized situation.

Gate entered Japan through acquisition and obtained a MiCA license in Malta, along with a complete operational license from Dubai VARA, securing three footholds in the high-value category.

Bitget is currently the weakest in the high-value category, primarily narrating its expansion through the breadth of medium to low-value licenses.

The Next Phase of the Compliance License Race

From the trajectories of these five exchanges, several clear patterns can be summarized.

The era of regulatory arbitrage has ended

In the past, exchanges could register in Seychelles or the British Virgin Islands and serve global users through decentralized operational structures; this path has essentially been blocked as of 2025. The EU MiCA, Singapore DTSP system, Hong Kong VATP framework, and Japan FSA system are all requiring exchanges to have a physical presence, licenses, compliance history, and capital reserves in the local market.

“Acquiring licensed entities” is more efficient than “reapplying”

Binance's acquisition of Gopax to enter Korea, Gate's acquisition of Coin Master to enter Japan, Bybit negotiating the acquisition of Korbit, and Binance acquiring Sakura Exchange Bitcoin to enter Japan all follow this logic. For regulators in mature markets (Japan, Korea), issuing new licenses requires lengthy reviews; however, allowing existing licensed entities to change shareholders is a more feasible route.

Regulatory fines instead become proof of compliance

After OKX paid 505 million USD in settlement funds, it officially entered the U.S.; Bybit’s Indian subsidiary obtained FIU-IND registration after paying approximately 1.06 million USD in fines, reflecting an unexpected phenomenon: in the crypto industry, having undergone regulatory penalties and completed settlements is viewed as proof of having “cleansed” itself. The past issues are “priced in” and can be seen as good news once the negative factors have been exhausted.

The number of licenses will become a key indicator of enterprise value

In the past, the criteria for assessing exchanges were trading volume, user count, and number of coins. In the future, an additional criterion will be added: “the number of high-value licenses.” From recent mergers and financing valuations within the industry, this metric has already begun to influence pricing.

Conclusion: Compliance Is Not the End, But the New Starting Line

In the past, the industry often said “compliance is a cost.” But the data from 2025 to 2026 clearly shows that compliance is also a source of revenue.

CoinGecko data shows that the total trading volume of the top ten centralized exchanges in 2025 was approximately 18.7 trillion USD, with a year-on-year increase of 7.6%. Within this growth, the contribution from regulated markets (EU MiCA, Singapore, Dubai, Japan) significantly outpaced that from unregulated markets; in other words, the growth rate of the compliance market has already surpassed that of the gray market.

For the five exchanges, this signifies that whoever secures full licensing in Japan, gets through the third-party review in the Hong Kong VATP list, is viewed as a “qualified counterparty” by European banks under the MiCA framework, and passes institutional business audits by MAS in Singapore will have the opportunity to ascend to a higher tier in the next landscape.

For users and investors, understanding the true value of licenses, rather than merely seeing slogans like “holding licenses from XX countries,” is essential for judging the long-term sustainability of an exchange.

Licenses are not a panacea. In February 2025, Bybit was still subjected to a hacking incident resulting in 1.46 billion USD in losses despite holding multiple licenses; in 2024, the scandals involving Hong Kong's JPEX and HOUNAX caused losses exceeding 172 million USD. Licenses can reduce regulatory risks but cannot eliminate the impacts of individual events.

However, exchanges that hold licenses, have reserves, offer independent custody, and undergo regular audits will see the differences in marginal safety compared to those that lack these attributes magnified in each black swan event.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。