Author: Nancy, PANews

A convenient trading window for U.S. stocks is being opened by CEX (Centralized Exchange).

As crypto platforms rush into the U.S. stock market to mine for gold, market liquidity and asset allocation logic will be reshaped, and the flow of funds, trading rhythm, and innovative culture in the crypto circle are also transforming TradFi assets in reverse.

Wall Street fringe stocks are being hotly speculated as Meme coins

When U.S. stocks were brought into the crypto world, players accustomed to high volatility and short-term speculation in the crypto circle directly copied this familiar gameplay.

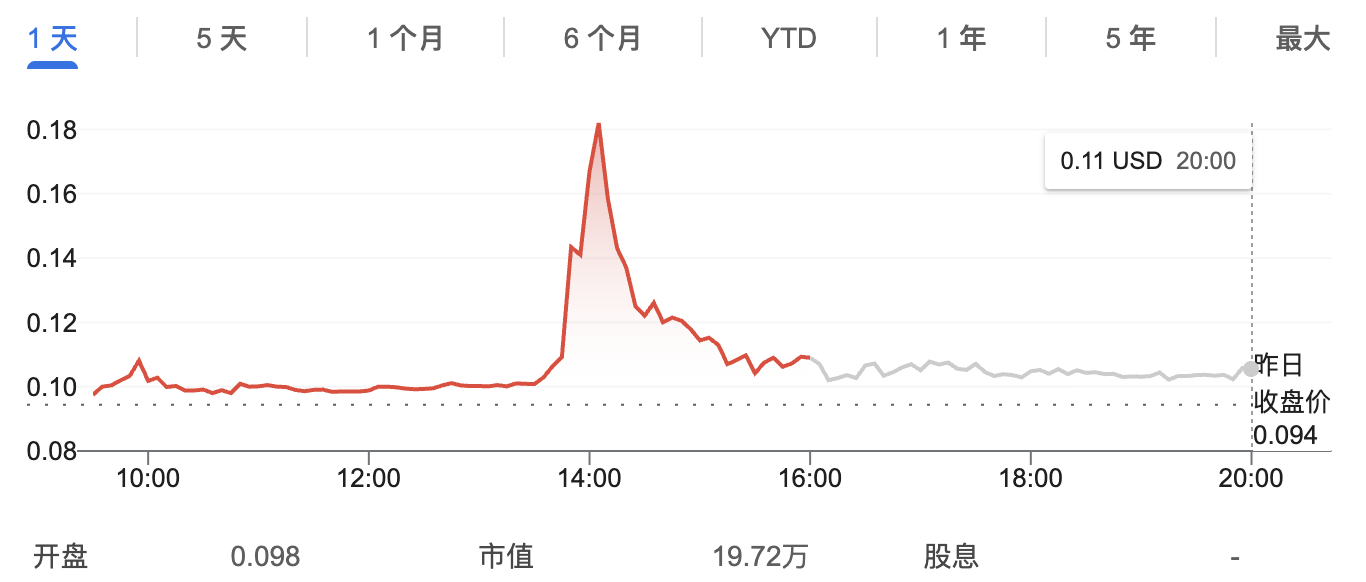

On June 1, the world's largest crypto exchange Binance officially launched U.S. stock trading. On the first day of the launch, a rather unusual phenomenon quickly attracted market attention: the most actively traded stocks were not all blue-chip stocks, but a large number of obscure small-cap, micro-cap, and even nano-cap stocks. For example, stocks like WOK, ZCMD, ANY, ABTS, etc., had daily trading volumes exceeding $100 million, becoming hot targets in Binance's U.S. stock sector.

These long-margin assets that have drifted outside the vision of mainstream investors suddenly became objects of pursuit for crypto funds. In the eyes of many crypto players, these low market cap stocks are essentially no different from Meme coins: small circulation, high price elasticity, easily attract market attention, and as long as there is enough attention and funding to drive it, it's easy to open a “lottery.” However, this logic does not fit well within the U.S. stock market.

Taking the Chinese concept stock Wok (WOK) as an example, this typical nano stock with a market cap of less than $200,000 had previously received a Nasdaq delisting warning because its stock price had long been below $1. Although the company has maintained its listing qualifications through several reverse stock splits, fundamental pressures have always existed. After Binance launched the U.S. stock market on June 1, WOK unexpectedly became the stock with the highest trading volume on the platform, with daily trading volume approaching $400 million.

A large influx of crypto funds, with some players even joking about “quickly buying themselves into becoming a major shareholder.” However, players soon discovered that after a brief surge in its stock price, it quickly fell back. The reason is that WOK holds a massive amount of “ammunition,” having already expanded through shareholder meetings and is ready to issue more shares at market price by SEC shelf registration at any time, thus diluting existing shares.

Another hotly speculated stock, Zhongchao Medical (ZCMD), is also a high-risk micro-cap shell stock. The company has authorized substantial capital expansion approved by shareholder meetings, effective F-3 shelf registration, and multiple reverse stock split mechanisms authorized by the board of directors, which gives it almost unlimited issuance capability.

For crypto investors unfamiliar with U.S. stock capital operating rules, it is easy to become fuel for the market's liquidity.

The crypto army enters the U.S. stock market, escalating risks and cultural clashes

CEX's layout in the U.S. stock market opens up an unprecedented asset pool for crypto users. But the larger the pool, the deeper the water.

From a risk perspective, the U.S. stock market is actually constructed from different levels. The top layer comprises the Nasdaq and NYSE main board markets. Here gather the vast majority of mature listed companies, which must meet strict requirements for market cap, revenue, profit, or cash flow, and are subject to dual regulation by the SEC and exchanges. Information disclosure is relatively complete, institutional investor participation is high, and issuing shares beyond a certain percentage typically requires shareholder approval, leading to higher market transparency and governance levels.

The middle layer includes nano and micro-cap stocks with a market cap below several tens of millions of dollars. While still listed on the main board market, many companies face long-term delisting risks. After their stock prices persistently fall below standards, they often enter a rectification period, commonly exhibiting dead cat bounces or pre-delisting spikes to offload stocks.

The highest risk lies in the OTC pink sheets market. Here, the listing threshold is extremely low, information disclosure requirements are limited, liquidity is scarce, market makers have considerable influence, and stock price manipulation and shell resource speculation are common.

At the bottom level is the OTC pink sheets over-the-counter market, where there are virtually zero listing hurdles, no issuance restrictions, and no strict delisting mechanisms, leading to rampant shell stocks, significant market maker control, poor information disclosure, low liquidity, and frequent manipulation.

Although the trading threshold for U.S. stocks has been significantly lowered, not understanding the regulatory framework, financing mechanisms, and share dilution rules behind different market levels can easily lead to pitfalls.

However, from another perspective, the crypto army is bringing its trading logic into the U.S. stock market. In the eyes of traditional investors, a company's value largely depends on revenue, profit, cash flow, and growth expectations; yet traders who have grown up in the crypto market pay more attention to circulation scale, market heat, community consensus, and price elasticity.

This differentiation is altering the pricing logic of traditional assets. Particularly, some originally overlooked fringe stocks are beginning to receive inflows of funds and market heat that exceed their fundamentals. To some extent, this is not only a fusion of the crypto and TradFi markets but also a collision of two financial market cultures.

Starting with buying U.S. stocks, CEX opens a new growth curve

While the neighboring stock market is in a frenzy, crypto liquidity is waning. As more exchanges list traditional financial assets like U.S. stocks, there will be a certain siphoning effect on the crypto market in the short term.

Especially given the current weak performance of Bitcoin, Ethereum, and most altcoins, capital is naturally flowing from high-risk assets to more certain assets, which is simply a natural choice in the capital market.

From the perspective of CEX, the significance of entering the U.S. stock market goes far beyond just adding a new trading product. As one of the largest asset pools globally, the U.S. stock market gathers the largest funding scale, most mature liquidity, and greatest attention. For exchanges, listing U.S. stocks essentially means competing for users, capital retention rate, and the gateway to global capital flow amidst a backdrop of industry growth slowdown and intensifying competition.

In the short term, this isn't necessarily a sufficiently attractive business. Over the past few years, CEX's revenue has heavily relied on high volatility, high turnover, and high-leverage trading, while traditional financial investors tend toward long-term holding, low-frequency trading, and asset allocation. Even if a large number of users start to buy and sell U.S. stocks through exchanges, it is difficult to replicate the growth curve seen during the crypto bull market.

What is truly worth noting is CEX's conversion of TradFi users and the potential for ecological expansion. When traditional financial users first open accounts on crypto platforms and buy U.S. stocks with stablecoins, their migration costs have been greatly reduced. From purchasing stocks to holding stablecoins, to exploring crypto assets, participating in crypto products, or engaging in on-chain applications, exchanges can gradually convert this group into crypto users.

To retain this newly added capital, exchanges will also innovate around U.S. stock assets more. For instance, Binance's planned bStocks essentially transforms traditional stocks into programmable assets on the blockchain. Users can use them as collateral for loans, invest in liquidity pools for returns, create structured products, or even develop new derivative strategies around them. This not only significantly enhances user stickiness on the exchange but also opens new revenue streams for the platform.

Overall, the collective entry of CEX into the U.S. stock market marks an important turning point in the history of crypto development.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。