Author: Fidelity Digital Assets

Translation: Jiahua, ChainCatcher

Mid-year is a good checkpoint for review, allowing investors to assess how market dynamics have changed and whether the judgments made at the beginning of the year still hold true.

In the “2026 Outlook”, the Fidelity Digital Assets research team believes that the key to this year is not in an immediate price surge, but in a more subtle dynamic: a structural “reconstruction” of the entire digital asset ecosystem. Although price performance has been occasionally flat and at times volatile this year, a deeper observation reveals that several underlying trends are steadily advancing.

This article reviews the progress of several key themes from the “2026 Outlook”, pointing out which of our judgments have been confirmed, which have diverged, and what these changes might mean for the future.

1: Acceleration of Integration Between Digital Assets and Capital Markets

We previously anticipated that the integration of digital assets with traditional capital markets would continue to advance by 2026. So far, this trend has indeed been moving forward, with certain areas progressing even faster than expected.

Despite market fluctuations, the demand for exposure to digital assets through mainstream financial channels remains strong, and traditional platforms continue to expand their product lines.

Notably, the open interest of spot Bitcoin ETP options (which are not expected to launch until November 2024) is now comparable to options that are directly settled in Bitcoin, reflecting a continuous increase in adoption by institutions and mainstream investors.

The momentum in the tokenization space is also increasing, with activity seeming to exceed expectations. Traditional financial institutions are increasingly launching blockchain-based investment products, while large exchanges are collaborating with or acquiring stakes in digital asset platforms to broaden distribution channels and connect with on-chain infrastructure.

At the same time, regulatory clarity is also improving. The U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have jointly issued guidelines for establishing classifications of digital assets; combined with the advancement of legislation like the CLARITY Act, this means market participants will welcome a clearer framework.

Overall, these developments indicate that digital assets are continuing to integrate into a broader financial system, driven by both market demand and infrastructure expansion.

2: Rights of Token Holders Gradually Gaining Attention, but Still Unclear

We had expected that by 2026, the interests of token holders would become more closely aligned, with more on-chain enterprises prioritizing mechanisms such as buybacks and clearer ownership.

So far, this direction seems unchanged, and experiments within the entire ecosystem are ongoing: from reserve-based buyback dynamics (like the Hyperliquid/USDC alliance) to governance and structural updates like the Aave DAO/Labs restructuring.

However, although the adoption of these mechanisms is expanding, a distinct “token holder rights premium” has not yet been fully reflected in market pricing. This trend is advancing, but it is still in its early stages, and investors are still assessing which models can truly bring about sustainable value accumulation.

3: Potential Shifts in AI and Mining

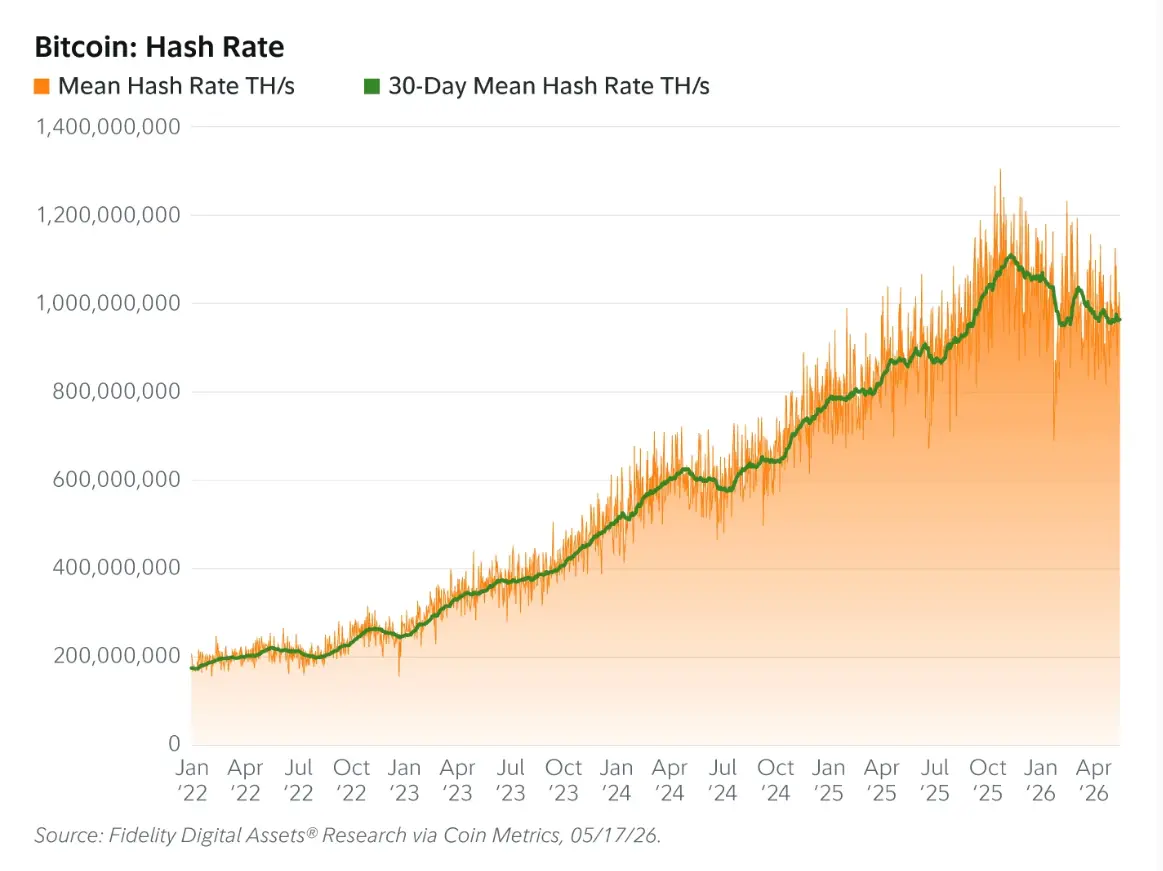

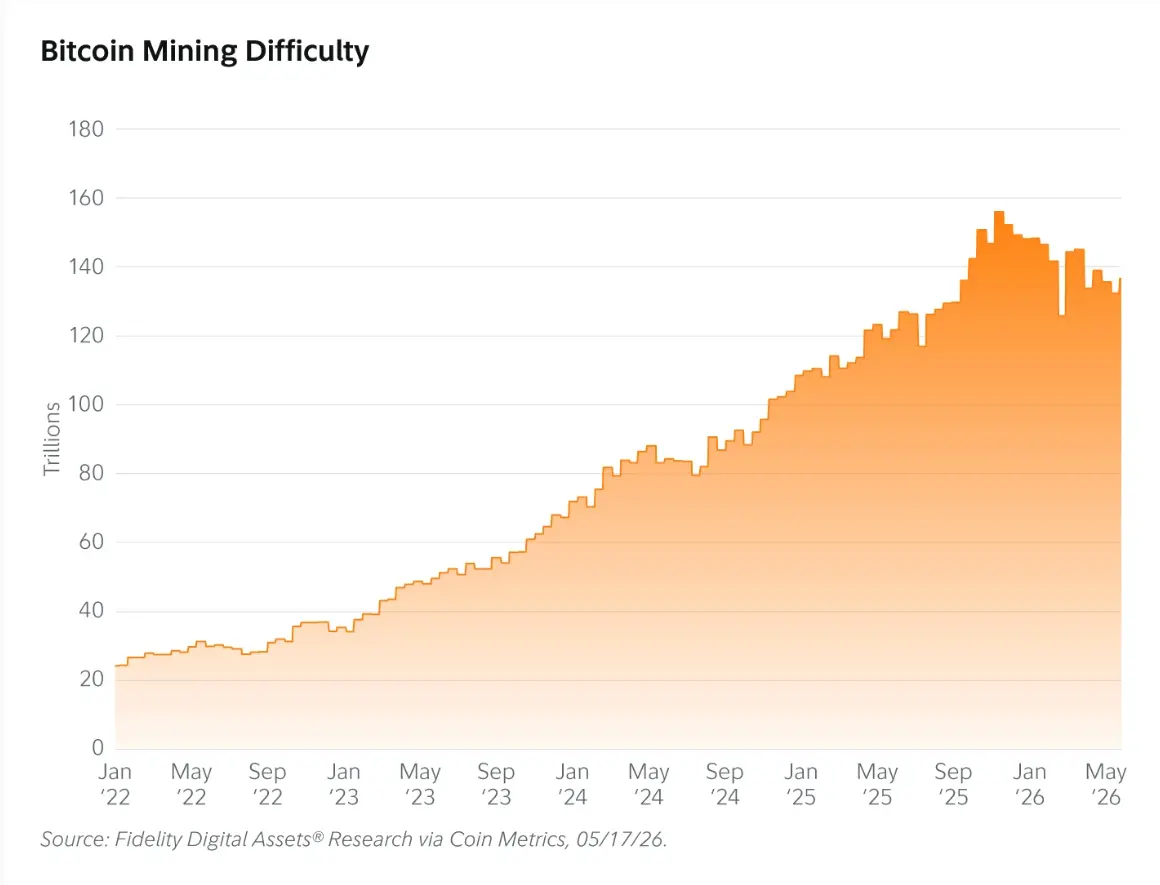

We had suggested that the intensified competition for AI computing power demand could lead to a stabilization in Bitcoin hash rate growth, as miners might redirect energy and infrastructure towards potentially more profitable avenues. This dynamic may currently be manifesting: the 30-day average hash rate and mining difficulty have decreased by approximately 8.8% and 7.8%, respectively, this year.

Although some of this can be attributed to seasonal factors, especially winter-related power restrictions, the recent recovery (with hash rate rebounding by about 1.3% from lower points and difficulty rebounding by about 8.8%) indicates that weather alone cannot fully explain this shift.

Although some of this can be attributed to seasonal factors, especially winter-related power restrictions, the recent recovery (with hash rate rebounding by about 1.3% from lower points and difficulty rebounding by about 8.8%) indicates that weather alone cannot fully explain this shift.

From a longer trajectory, the growth rate of hash power compared to previous years has slowed down, which may be an early signal of structural changes. The business of AI data centers has become increasingly profitable, particularly for large operators that can secure power infrastructure; this seems to be a growing driving force behind these changes.

Although it is still early, the observed slowdown in growth aligns with initial assessments and may reflect that miners are gradually shifting towards alternative revenue sources.

4: Bitcoin at a New Turning Point

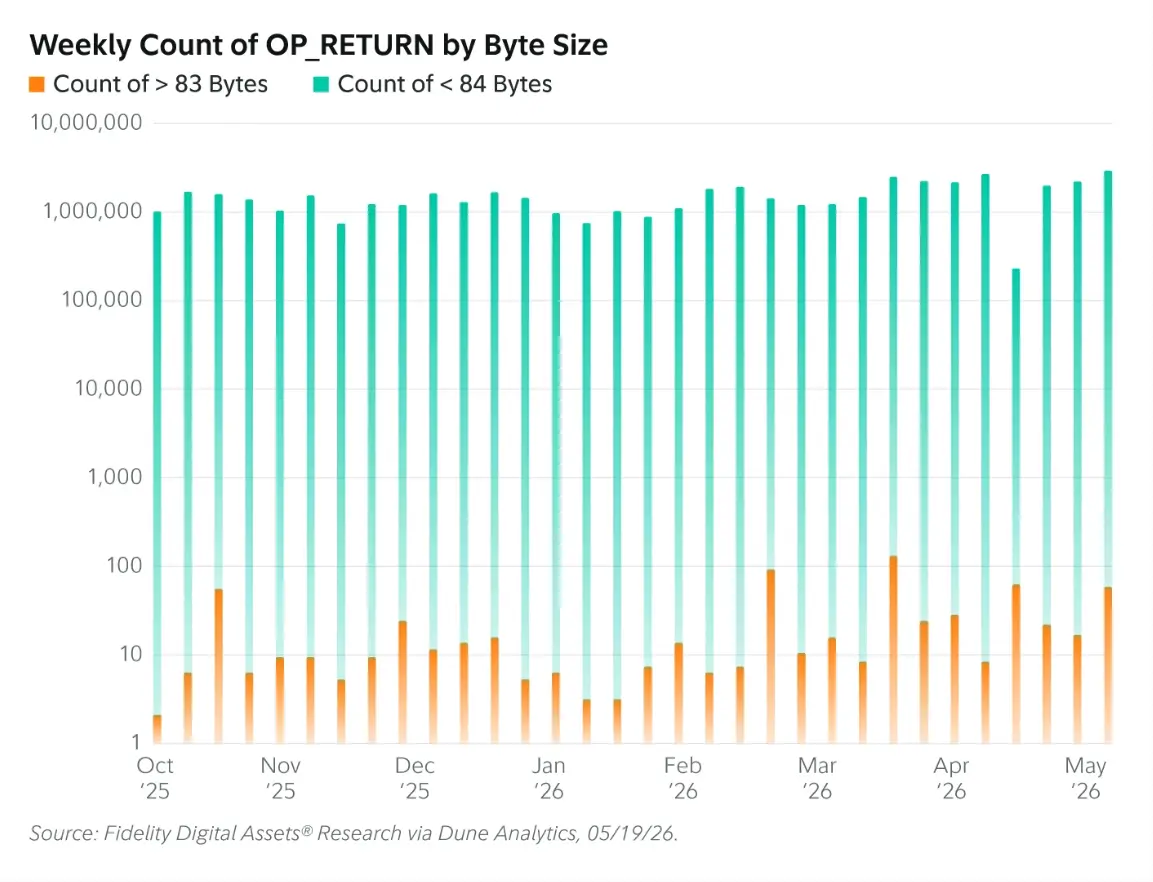

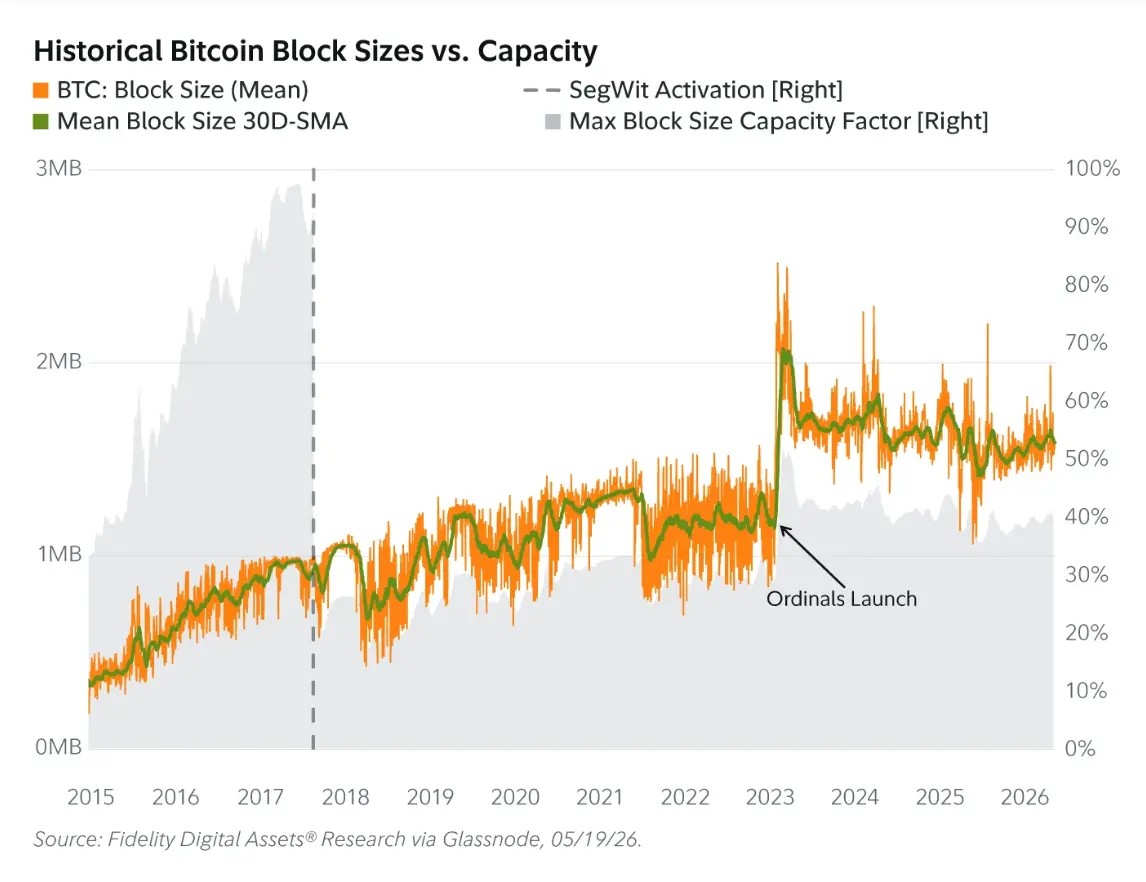

We had anticipated that increasing the writable data volume of the OP_RETURN opcode would not lead to a significant bloating of the blockchain (OP_RETURN is used for writing data on-chain, and paying transaction fees for increasing its data limit has not resulted in abuse or network bloat). So far, the data seems to support this judgment.

The usage of larger sized (≥84 bytes) OP_RETURN has remained essentially unchanged, and the overall growth of the blockchain remains within predicted parameters (around 1.35-2.5MB). Other blockchain utilization metrics show that capacity still remains below 50%, indicating that the increase in data flexibility has not placed substantial pressure on the network.

Meanwhile, the focus has shifted to more macro network dynamics. Bitcoin Knots nodes have shown significant fluctuations, rapidly rising and then quickly falling, raising speculation about potential Sybil-like activity.

According to current data, Bitcoin Core nodes still account for about 77% of the network, while Knots nodes account for about 17%. Although still a minority, this brings an unexpected risk of fragmentation—though the probability is low, it is not zero: under certain conditions, Knots nodes could diverge into a chain that is stagnant or less secure, which, according to current estimates, could occur in about 80 days.

However, the dominance of Core still anchors network consensus. Meanwhile, the momentum around long-term security upgrades is also growing. BIP-360 has been streamlined with the introduction of quantum-resistant output types (Pay-to-Merkle-Root, referred to as P2MR); the ongoing OP_CHECKSHRINCS research reflects an exploration of hash-based post-quantum signature schemes.

While there is currently no definitive timeline for when quantum threats may emerge, these advances indicate that the industry is increasingly prioritizing early preparations for the future security of the network.

5: Shorts Temporarily Control the Situation

In January of this year, we outlined two scenarios where bulls and bears would be evenly matched as we approached 2026, anticipating that macro conditions would lead to nonlinear movements, despite structural fundamentals improving.

So far this year, the bearish scenario has largely prevailed: Bitcoin has fallen 13%, driven by deleveraging triggered by liquidations, persistently high inflation, and geopolitical uncertainties prompting market expectations of further rate hikes. However, recent market performance reveals a more subtle dynamic.

Following the initial round of sell-off triggered by recent geopolitical conflicts, Bitcoin rebounded and outperformed traditional assets during the same period, which may reflect a demand for highly liquid, neutral assets during times of stress.

Nonetheless, structural benefits remain, including the ongoing formation of institutional capital, gradual clarity in regulations, and an expansion of global liquidity.

While the short-term environment remains constrained, our broader judgment still seems valid, albeit with less smooth progress.

6: Gold Strongly Sustains, What Will Happen Next?

We had pointed out that it was not surprising for gold to have another strong year, with support stemming from central bank gold buying demand and the global trend of gradually moving away from the dollar system.

This year, gold first rebounded nearly 30% amidst geopolitical tensions, then fell back to a more moderate increase of about 3-4%. Despite the pullback, gold may still outperform the broader market by the end of the year.

Evidence supporting the move away from the dollar system continues to grow, including some emerging alternative settlement methods, such as Iran accepting Bitcoin for toll payments and payments related to activities in the Strait of Hormuz.

At the same time, demand from central banks for gold remains strong. Recent data indicates that accumulation is still ongoing, and notably, gold has surpassed dollars and U.S. Treasuries to become a major component of global reserves.

The performance of gold and the sustained demand from central banks aligns closely with our initial judgment; however, the expected excellent performance of Bitcoin has not yet materialized.

Conclusion: Building Strength Beneath the Surface

As we reach mid-year, the landscape of digital assets in 2026 presents a balance between short-term pressures and long-term progress. Several themes in the “Outlook” are developing as expected, particularly regarding institutional participation, regulation, and infrastructure; however, others are still in early stages or have yet to fully materialize.

For investors, this indicates the need to look beyond short-term price fluctuations to see how structural changes are forming. Many foundations supporting the next phase of growth seem to be thickening, even if they have not fully manifested yet.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。