Written by: Ada, Deep Tide TechFlow

Recently, Nvidia's venture capital firm NVentures invested in a French quantum computing company, Alice & Bob, focusing on fault-tolerant quantum computing.

It is a common misconception to categorize all of Nvidia’s external investments under NVentures. In fact, this venture capital department, established in 2021, collectively made 30 investments in a year that do not match the size of a casual check from the corporate development team. For example, a single equity investment in Synopsys by the latter is set to reach $2 billion by the end of 2025, already several times more than NVentures' total investment over the last three years.

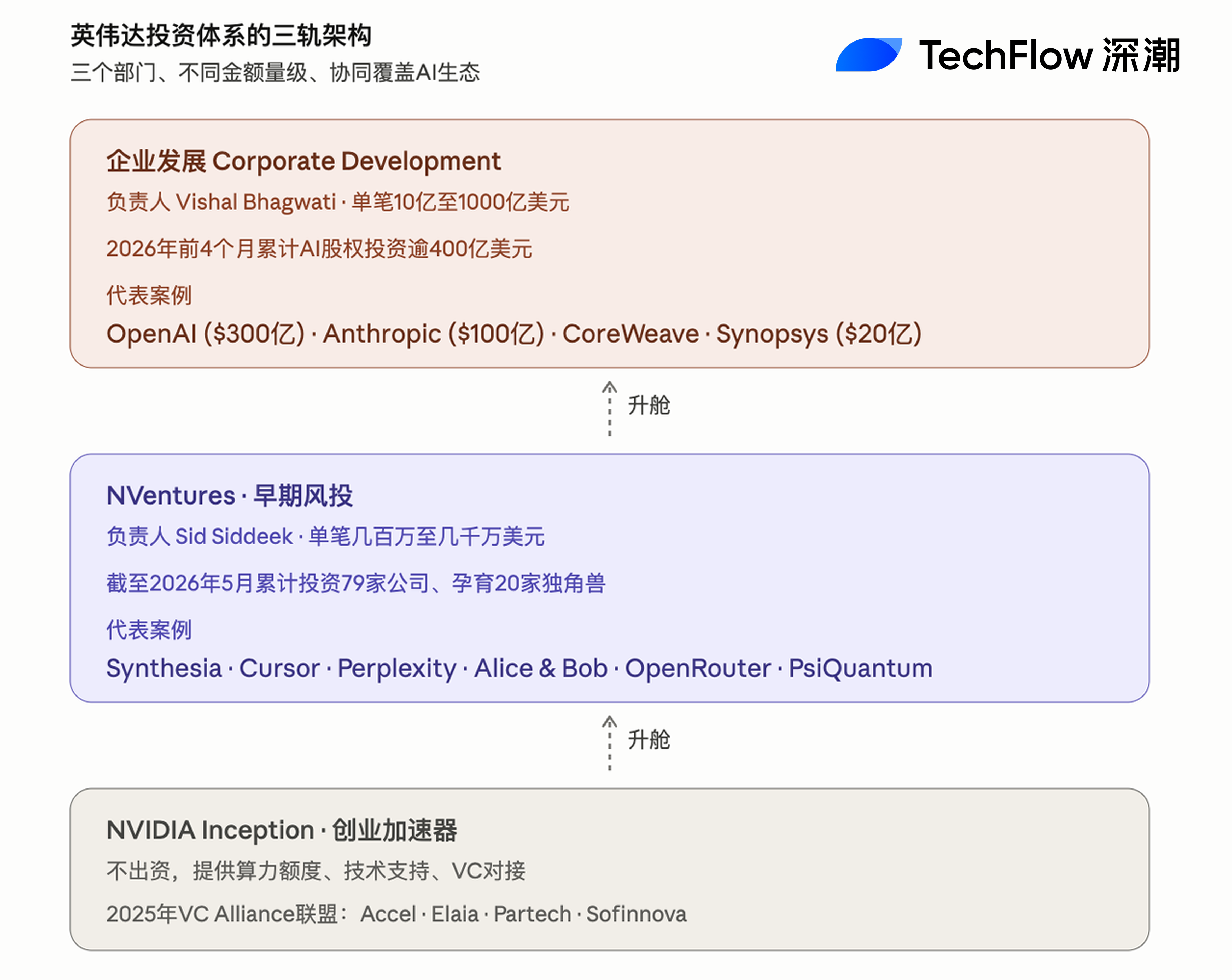

To understand how Nvidia weaves the AI ecosystem with capital, one must start with its investment system's "three-track structure." The corporate development team is responsible for strategic large-scale investments and mergers worth billions to hundreds of billions, while NVentures handles early-stage, broadly industry-related financial investments, and NVIDIA Inception is an accelerator that does not invest but provides resource connections. Together, these three create the largest and fastest capital deployment machine in Silicon Valley's history, which has also become the focal point of short sellers’ skepticism over "circular financing."

The True Face of NVentures: A 2-Person Team, 79 Companies, 20 Unicorns

Although NVentures operates under Nvidia's banner, its internal scale is surprisingly small. According to private equity data firm Tracxn, as of May 2026, the entire team consists of only 2 people, with cumulative investments in 79 companies, nurturing 20 unicorns, including AI video generation platform Synthesia, clinical AI company Abridge, and quantum computing company PsiQuantum. In the past 12 months, the team completed 43 new investments, making 20 moves in just the first 5 months of 2026, showing a clear acceleration in pace.

Leading NVentures is Mohamed "Sid" Siddeek, the company's vice president and head of NVentures. Siddeek's resume reflects Nvidia's positioning of this department. He worked at Morgan Stanley in the late 1990s and accompanied Jensen Huang on Nvidia's IPO roadshow; then he transitioned to head TMT and telecom investments at the UAE's sovereign fund Mubadala for nearly a decade; later, he moved to the SoftBank Vision Fund to oversee corporate software and healthcare investments; he returned to Nvidia in 2021 to establish NVentures.

Siddeek describes the scope of investment as: "There are only two real selection criteria, the first being any area Nvidia can touch, and the second which fields are investable." In an interview with Global Corporate Venturing, he revealed that this implies horizontal coverage across nearly all industries that AI can transform, including medical, manufacturing, robotics, autonomous driving, quantum, and a vertical range from foundational tools to application layers within NVentures' investment scope.

Three-Track Structure: Corp Dev for Strategy, NVentures for Early-Stage, Inception for Ecosystem

Nvidia's external investment system consists of three distinct parts, with clear divisions of labor.

The first tier is the Corporate Development team, led by Vishal Bhagwati, responsible for all strategic-level large investments, joint ventures, and mergers. The amount range in this line is not comparable to NVentures at all. Representative actions from the second half of 2025 to the first half of 2026 include a $30 billion lead investment in OpenAI in February 2026 (part of an approximately $110 billion funding round), with a future commitment of an additional $100 billion; a $10 billion commitment to Anthropic in November 2025; a $2 billion injection into Synopsys by the end of 2025; an additional $2 billion investment in CoreWeave at the beginning of 2026, alongside a $6.3 billion cloud capacity procurement agreement; a $2 billion investment in Nebius in March 2026; and an equity commitment of up to $2 billion for xAI.

According to CNBC, just in the first four months of 2026, the corporate development team's lead in AI equity investments exceeded $40 billion. Nvidia's total investment in private companies and infrastructure funds for the fiscal year 2025 amounted to $17.5 billion.

The second tier is NVentures, led by Sid Siddeek, positioned as a traditional venture capital firm seeking financial returns. Individual investment sizes range from several million to tens of millions of dollars, primarily making moves in the Seed to Series B stages. Siddeek has clarified to Global Venturing that NVentures "mainly focuses on early-stage investments, while the corporate development team is responsible for larger, more direct strategic investments." Behaviorally, NVentures primarily follows funding others, with only about one-eighth of its investments leading the rounds, participating more in rounds led by top VCs like Accel, a16z, and Sequoia through Nvidia's endorsement.

The third tier is NVIDIA Inception, essentially an entrepreneurship accelerator project that does not directly invest but provides startups with Nvidia hardware credit, technical support, marketing promotions, and channels for VC connections. The "VC Alliance" launched by Nvidia in 2025, in conjunction with institutions like Accel, Elaia, Partech, and Sofinnova, distributes NVIDIA DGX Cloud Lepton compute coupons to its invested companies, extending Inception's reach in Europe.

There is a clear "funnel" relationship among the three. Inception discovers early projects and integrates them into Nvidia's ecosystem; those with investment value enter NVentures' sight and may receive early checks of several million to tens of millions; when a company grows to a size that can impact Nvidia's strategic layout (becoming an important customer, key supplier, or potential acquisition target), it will "upgrade" to the corporate development team, entering a cooperation framework worth tens of billions to hundreds of billions.

Recent Movements from NVentures: Quantum, Inference Routing, AI Security

In May 2026, NVentures was notably active. In just the last month, four investments were publicly disclosed. On May 22, the French quantum computing company Alice & Bob announced that NVentures participated in its €100 million Series B expansion round. Alice & Bob's core technology is a fault-tolerant quantum computing architecture based on "cat qubits," collaborating deeply with Nvidia’s CUDA-Q, cuQuantum, Dynamiqs, and NVQLink quantum-classical hybrid computing tech stack; on May 26, the AI model routing platform OpenRouter completed a $113 million Series B round, with NVentures participating alongside Google CapitalG and Snowflake. OpenRouter's business is to provide developers with a unified interface to access APIs from dozens of different model suppliers worldwide; on May 28, the AI inference infrastructure startup Tensormesh completed a $20 million seed extension round, with NVentures co-investing alongside CoreWeave and AMD; on May 6, the AI cybersecurity company Xbow completed a $35 million Series C extension, with NVentures participating.

In terms of investment targets, NVentures has recently clearly leaned toward three directions: quantum computing (Alice & Bob, Quantinuum, PsiQuantum), AI biomedicine (Relation Therapeutics, Genesis Therapeutics), and AI agents and inference layers (OpenRouter, Tensormesh, etc.). This aligns with Siddeek's assertion of "any field Nvidia can touch" and coincides perfectly with Nvidia's ongoing investment in next-generation software stacks like CUDA-Q, CUDA-X, and Triton.

Geographically, NVentures' European expansion has noticeably accelerated. In 2025, it completed 14 investments in Europe, double the 7 investments in 2024.

Three Layers of Interconnected Investment Portfolio Overview

If the three-layer investment portfolio is placed on the same map, Nvidia's "capital radiation" towards the AI ecosystem can be summarized into five main quadrants.

The base model layer includes OpenAI, Anthropic, xAI, Mistral, Cohere, Thinking Machines Lab, Reflection AI, Black Forest Labs. This layer is primarily funded by the corporate development team, with NVentures participating in smaller share follow-ons.

The cloud and infrastructure layer includes CoreWeave, Nebius, Lambda, Crusoe, Nscale, Firmus Technologies. This layer is similarly led by the corporate development team, with individual investments often reaching billions of dollars, accompanied by long-term computing power procurement contracts.

The application and development tools layer includes Cursor, Perplexity, Synthesia, Runway, Lovable, Together AI, Weka. NVentures has a higher level of participation in this layer, with amounts relatively smaller.

The robotics and autonomous driving layer includes Figure AI (latest valuation of $39 billion) and Wayve (valuation of $8.6 billion). Both the corporate development team and NVentures jointly invest here.

The quantum computing and biomedicine layer includes PsiQuantum, Quantinuum, Alice & Bob, Relation Therapeutics. This is primarily made up of early investments led by NVentures, forming Nvidia's hedge against the computing paradigm in the "post-GPU era."

According to venture capital research firm F4 Fund, from 2025 to early 2026, among the investment rounds involving Nvidia (corporate development + NVentures), at least 10 companies had valuations exceeding the $1 billion threshold, including OpenAI, Anthropic, xAI, Mistral, Figure AI, Cursor, Perplexity, and Scale AI.

Controversy: Burry's Short Selling and the "Circular Financing" Question

However, Nvidia's vast external investment landscape is provoking increasing skepticism. The most representative criticism comes from Michael Burry, the hedge fund manager who gained fame from the film "The Big Short."

According to Scion Asset Management's Q3 2025 13F filing, Burry built a short position against Nvidia and Palantir before September 30, 2025, including put options for approximately 1 million shares of Nvidia, with a notional exposure of about $187 million at the time of the stock price; and 50,000 put option contracts for Palantir (each corresponding to 100 shares), with an actual premium expenditure of about $9.2 million. Burry posted on his X account "Cassandra Unchained" with a scene from "The Big Short," captioned "Sometimes we can see the bubble," and subsequently retweeted Bloomberg's chart about Nvidia's circular financing, directly pointing the finger at Nvidia's capital deployment model.

Burry's specific accusation is technical. He estimated in his Substack that between 2026 and 2028, cloud vendors including Microsoft, Google, Oracle, and Meta will cumulatively underestimate depreciation by about $176 billion by extending the accounting depreciation period of Nvidia GPUs, thereby artificially inflating profits during the same period. This accounting adjustment resonates with Nvidia's equity investments in its clients, allowing buyers to have higher "paper profits" to absorb larger capital expenditures, while the latter directly provides funds for buyers to purchase Nvidia hardware.

On the institutional side, similar doubts have also been accumulating. In March 2026, the EU competition regulator explicitly included the "circular expenditure risk" in the review scope of Nvidia's investment system. Seaport Research estimates that for every $1 of equity investment by Nvidia, there corresponds about $3.5 of downstream chip procurement revenue. Bloomberg's March 2026 publication, "AI Circular Trading," illustrated the flow of funds among Nvidia, CoreWeave, OpenAI, Oracle, and Anthropic in a dense network chart. Nvidia holds about 7% of CoreWeave's equity; CoreWeave uses Nvidia GPUs as collateral for financing, which in turn uses cash to procure more GPUs from Nvidia, while Nvidia signs a $6.3 billion cloud capacity procurement agreement, promising to absorb CoreWeave's excess capacity until 2032; Nvidia commits to invest up to $100 billion in OpenAI, which promises to purchase Nvidia hardware and build a $300 billion data center through Oracle, which then procures GPUs from Nvidia; Nvidia invests $10 billion in Anthropic, and Anthropic commits to deploy Claude on Microsoft Azure, which then procures Nvidia's Grace Blackwell and Vera Rubin systems.

Responses from supporters also exist. Asset management firm Janus Henderson characterizes this model as a "virtuous cycle," arguing that binding both parties’ supply and demand through "equity + long-term procurement agreements" is a reasonable commercial arrangement in an era of extreme computing scarcity. Morningstar's analysis pointed out that Nvidia's arrangement to guarantee the purchase of CoreWeave's "excess capacity" actually exposes Nvidia itself to CoreWeave's inventory risk, instead constituting a constraint on the impulse to promote hardware in the short term.

In this controversy, NVentures' position is quite subtle. Its early, small-scale, follow-on-focused, and industry-diverse investment style stands in stark contrast to the corporate development team's "circular trading" model. The companies NVentures invests in, such as Alice & Bob, Tensormesh, and OpenRouter, lack the scale to constitute a cycle of being "both Nvidia customers and Nvidia investment targets"; their investment behavior is closer to the financial investment logic of traditional CVCs. However, from the perspective of Nvidia's overall investment system, whether NVentures, to some extent, acts as a "VC compliance facade" in external disclosures, allowing outsiders to more easily understand Nvidia's investment activities as normal venture capital behavior rather than systematic sell-side financing, is an implied question that Burry and EU regulators do not explicitly state but are raising.

Nvidia's consistent official statement is that all investments are based on independent business judgment and are not tied to hardware sales. However, market observers are increasingly frequently quoting a saying; in an era of computing scarcity, is it really wise to believe that "the intertwining of equity and procurement agreements is coincidence"? This itself is a matter of trust.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。