Author: Arrakis

Compiled by: Jiahua, ChainCatcher

Testing of cross-platform delays for 29 major crypto perpetual markets, in-depth analysis of the PerpDEX underlying architecture.

This content is for informational and educational purposes only and does not constitute investment advice. Arrakis has made reasonable efforts to verify the accuracy of the data provided but does not guarantee that all information is absolutely accurate, complete, or up-to-date. Thanks to @0xArchiveIO for their contributions to this research.

Introduction

Hyperliquid is the on-chain perpetual contract platform with the largest trading volume and open interest. It has expanded from crypto perpetual contracts to real-world assets, prediction markets, and permissionless DeFi tech stacks.

If you spend enough time on Crypto Twitter, you will hear statements like: Hyperliquid has replaced Binance and has become the center for cryptocurrency price discovery.

We have verified this statement. Inspired by the paper by Hoffmann, Rosenbaum, and Yoshida, we ran an improved version of the Hayashi-Yoshida lead-lag estimation model across three trading platforms (@HyperliquidX, @binance U-based contracts, and @Lighter_xyz).

What We Measured

The core question: How long does it take for a price change of an asset on one platform to be reflected on other platforms?

Each platform publishes trading records, which are detailed transaction records with timestamps.

The most intuitive way to measure cross-platform lead-lag is to extract two sets of trading records, shift one chronologically relative to the other, and select the time shift with the highest alignment of price changes between the two platforms from a range of possible shifts. The shift that produces the clearest alignment is the lead-lag time between the two platforms.

If the timeline of Hyperliquid is shifted back by 700 milliseconds so that its price movements perfectly align with Binance, it means that Binance is leading by 700 milliseconds.

We use the Hayashi-Yoshida estimation model, which is specifically designed for two price series with irregular and asynchronous transaction times. At each candidate time shift point, it calculates:

Where Cov(X, Y) is the covariance between X and Y, in our case, the return series of trades of the two platforms we are comparing. σ_X and σ_Y are the standard deviations of these two distributions.

We run the model separately on buyer trades (taking the sell orders) and seller trades (taking the buy orders) to avoid noise from bid-ask spread fluctuations at sub-second resolution.

For each pair of platforms, we calculate ρ values at 100 millisecond intervals in the range of -2000 to +2000 milliseconds, then read the shift amount when ρ peaks. A positive shift means that the leading platform is ahead.

We analyzed the cryptocurrency assets ranked among the top 29 by market capitalization that have trades on all three platforms:

$BTC · $ETH · $BNB · $XRP · $SOL · $TRX · $DOGE · $HYPE · $ZEC · $ADA · $XMR · $BCH · $LINK · $TON · $XLM · $LTC · $SUI · $AVAX · $HBAR · $NEAR · $TAO · $DOT · $UNI · $ONDO · $WLFI · $ASTER · $ICP · $MORPHO · $AAVE

Our analysis window was 16 days ending on February 26, 2026, with the tested platforms including: Hyperliquid compared to Binance, Hyperliquid compared to Lighter, and Lighter compared to Binance.

The complete analysis methodology can be found in our blog post.

What We Found

Each analysis reached a highly consistent conclusion:

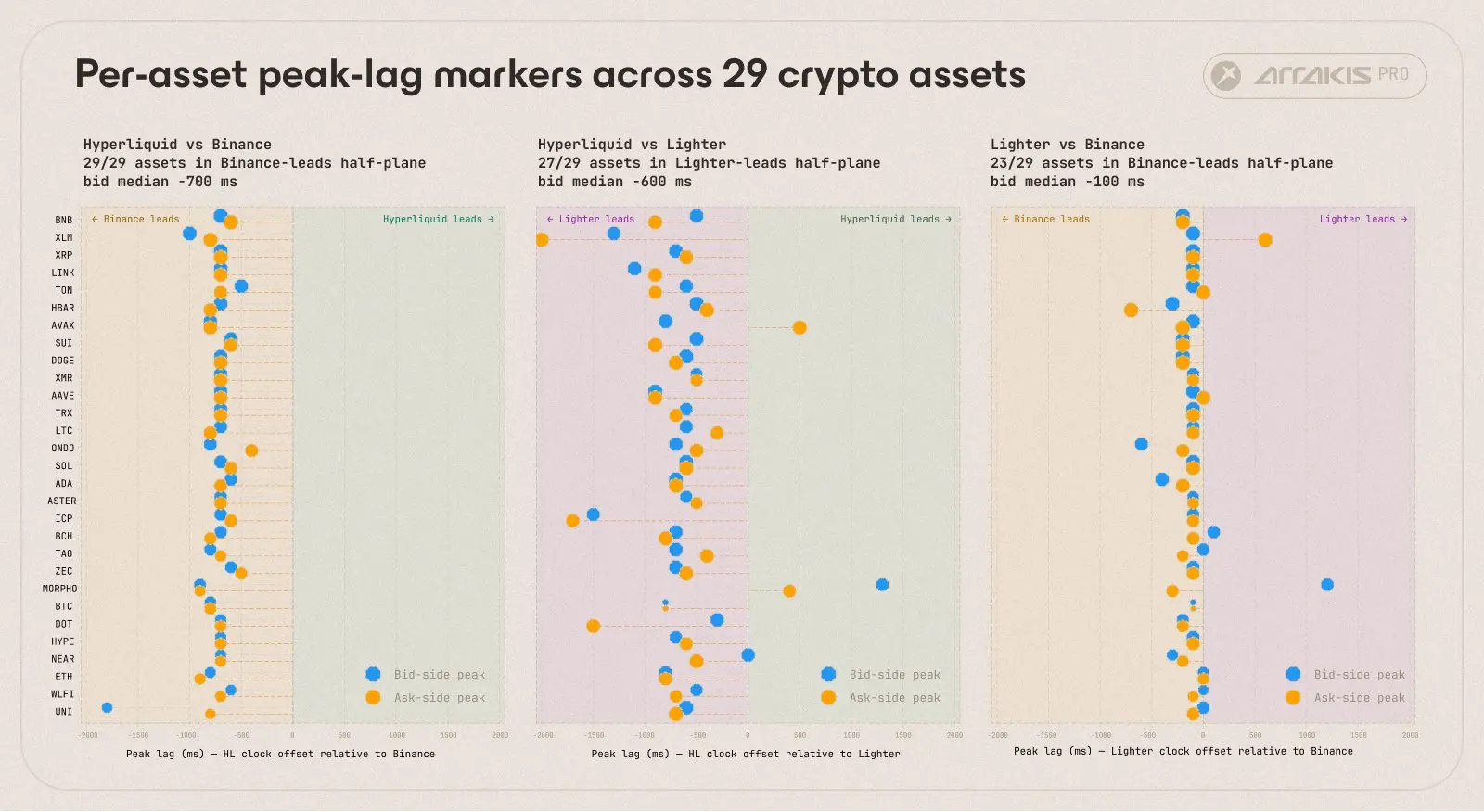

- Among all 29 assets: Binance leads Hyperliquid

- For 27 of the 29 assets: Lighter leads Hyperliquid

- For 23 of the 29 assets: Binance leads Lighter

Peak delays for all assets across the three platforms were marked, with the asset rankings in each panel showing the same order. Regardless of which platform is on the other end, the panels involving Hyperliquid look nearly identical. The Lighter versus Binance panel collapses into a dense cluster at negative delay margins.

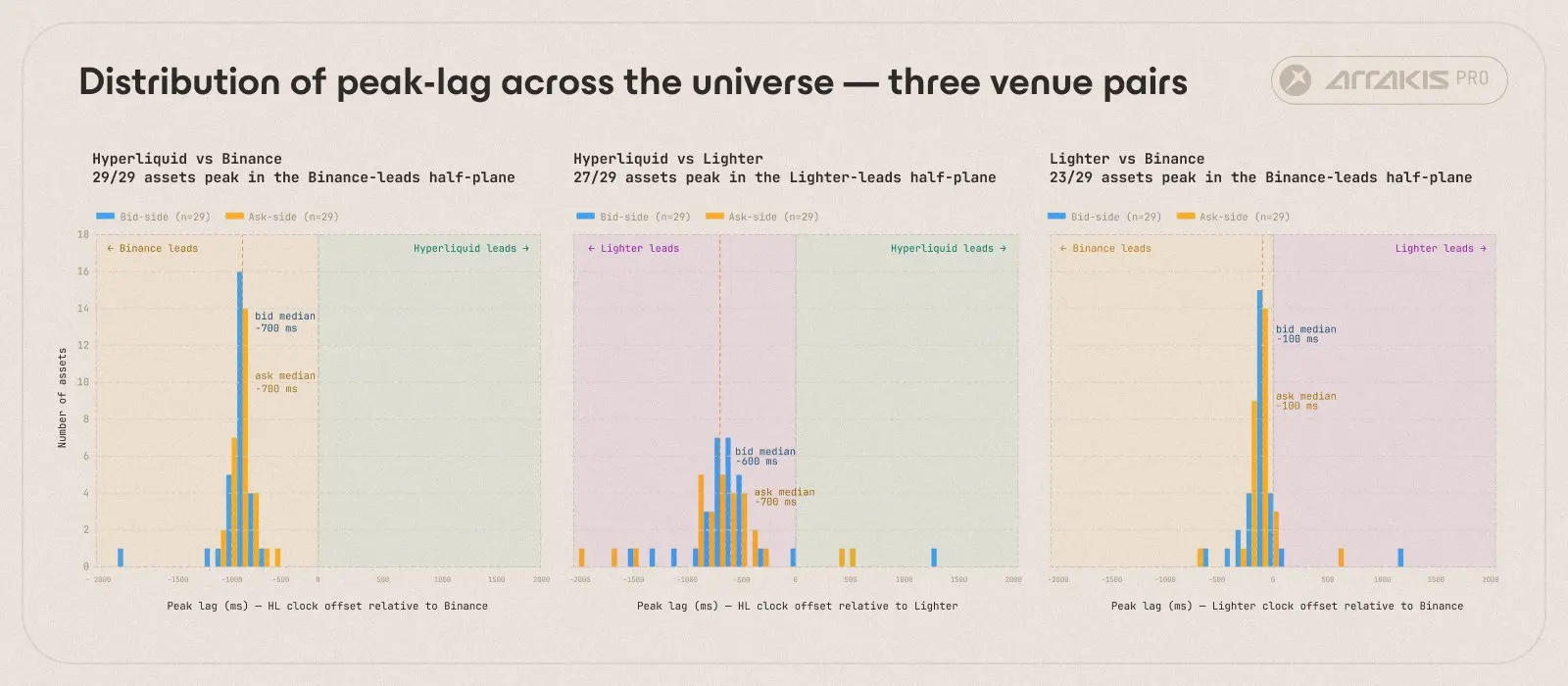

Distribution of peak delay intervals for the 29 underlying assets, ranging from -2000 to +2000 milliseconds in 100 millisecond intervals. Both panels involving Hyperliquid reach their peaks between -600 and -700 milliseconds. The Lighter versus Binance panel peaks at -100 milliseconds.

The two panels involving Hyperliquid look extremely similar: regardless of which platform is on the other end, they are closely clustered around -700 milliseconds.

From Hyperliquid's perspective, the delays of Binance and Lighter are very close, and the degree of their lead over it is roughly similar. The Lighter versus Binance panel is tightly packed by an order of magnitude, around -100 milliseconds, which is also the smallest incremental unit of time series lead-lag tested in our model.

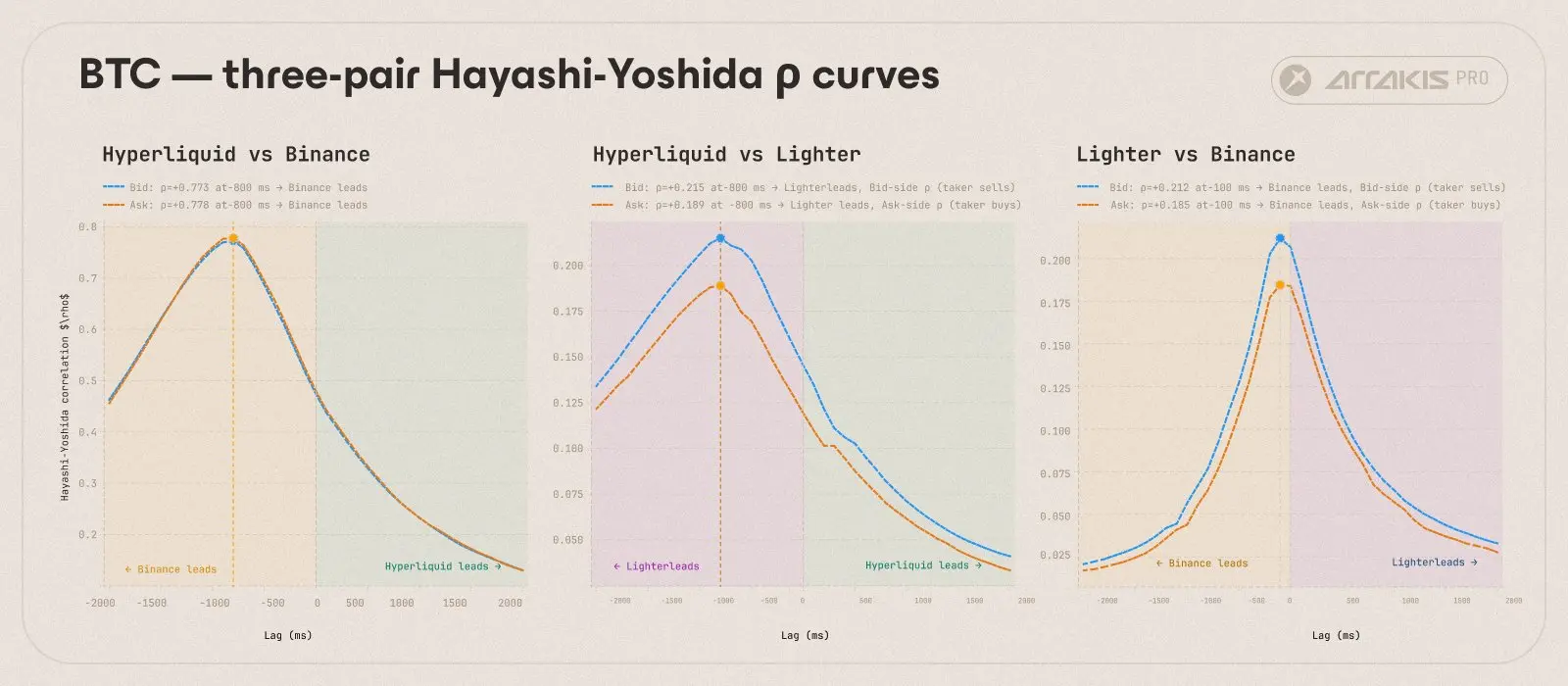

When observing BTC transaction data, this phenomenon is clearly visible at the level of individual assets. The correlations of Hyperliquid compared to Lighter and Hyperliquid compared to Binance consistently peak at -800 milliseconds, indicating that Hyperliquid is always lagging behind these two platforms at both levels.

Comparison of BTC correlation delay curves across all three platforms. The direction of the delay is consistent: both panels involving Hyperliquid show -800 milliseconds, while the Lighter versus Binance panel shows -100 milliseconds.

Transitivity Test

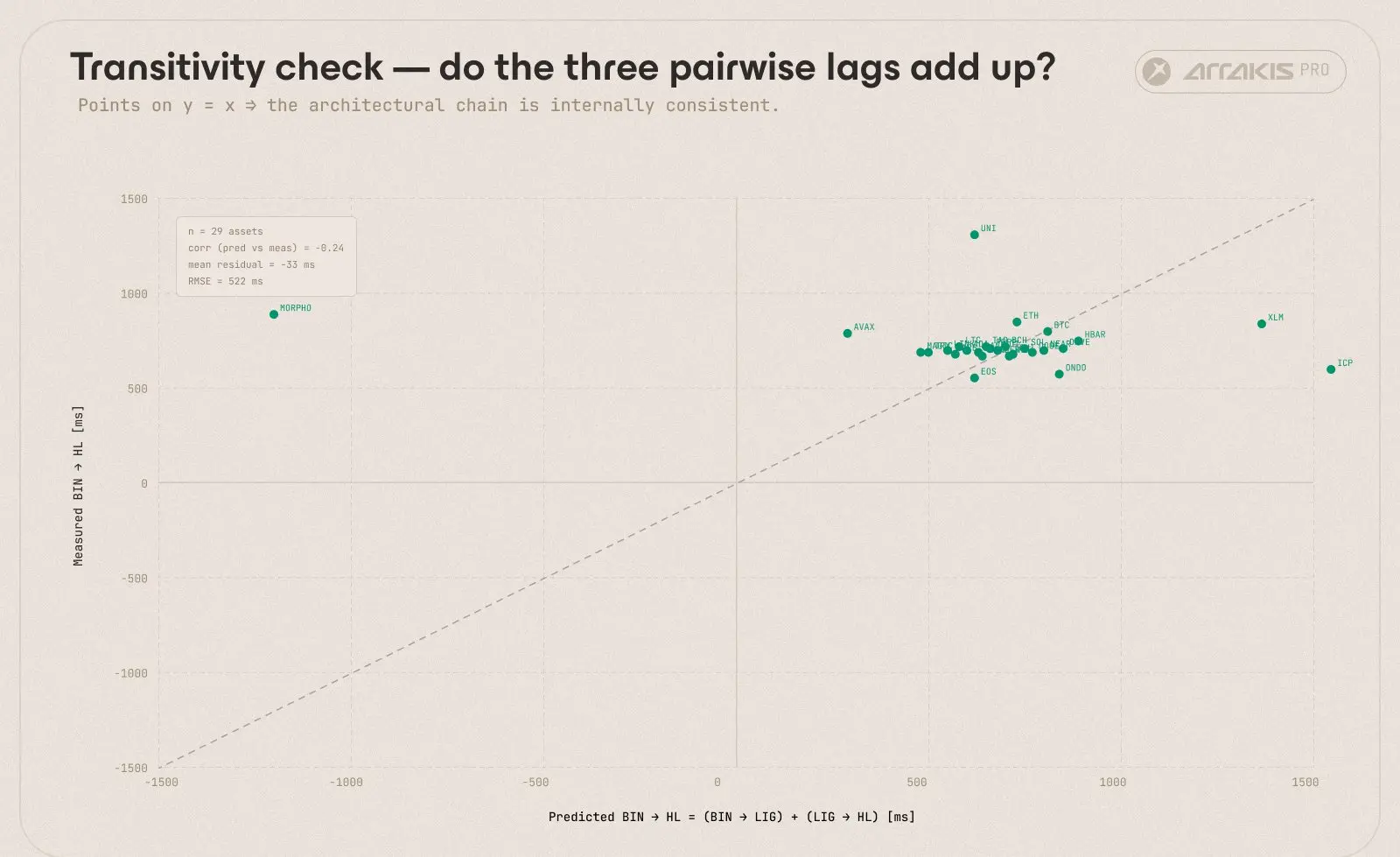

If these three paired delays reflect the same underlying microstructure, they should be additive: the delay from Binance to Hyperliquid should equal (Binance to Lighter) plus (Lighter to Hyperliquid). We tested this across the 29 markets we analyzed.

The X-axis is the predicted delay from Binance to Hyperliquid (i.e., the sum of Binance to Lighter and Lighter to Hyperliquid), while the Y-axis is the actual measured delay from Binance to Hyperliquid. Each data point represents a single asset. The overall median residual of the data is -33 milliseconds.

The median residual is only -33 milliseconds, indicating that these assets satisfy transitivity. Outliers (MORPHO, ICP, XLM, UNI) have more noise, as their delay correlation curves never truly peaked within our ±2000 milliseconds window. Our estimation model could not derive a precise lead-lag value for them.

All other markets conform to transitive relationships. This consistency indicates that the lead-lag phenomenon is determined by structural factors such as the matching and settlement mechanisms of these platforms, rather than being an artifact arising from comparisons between specific sets of platforms.

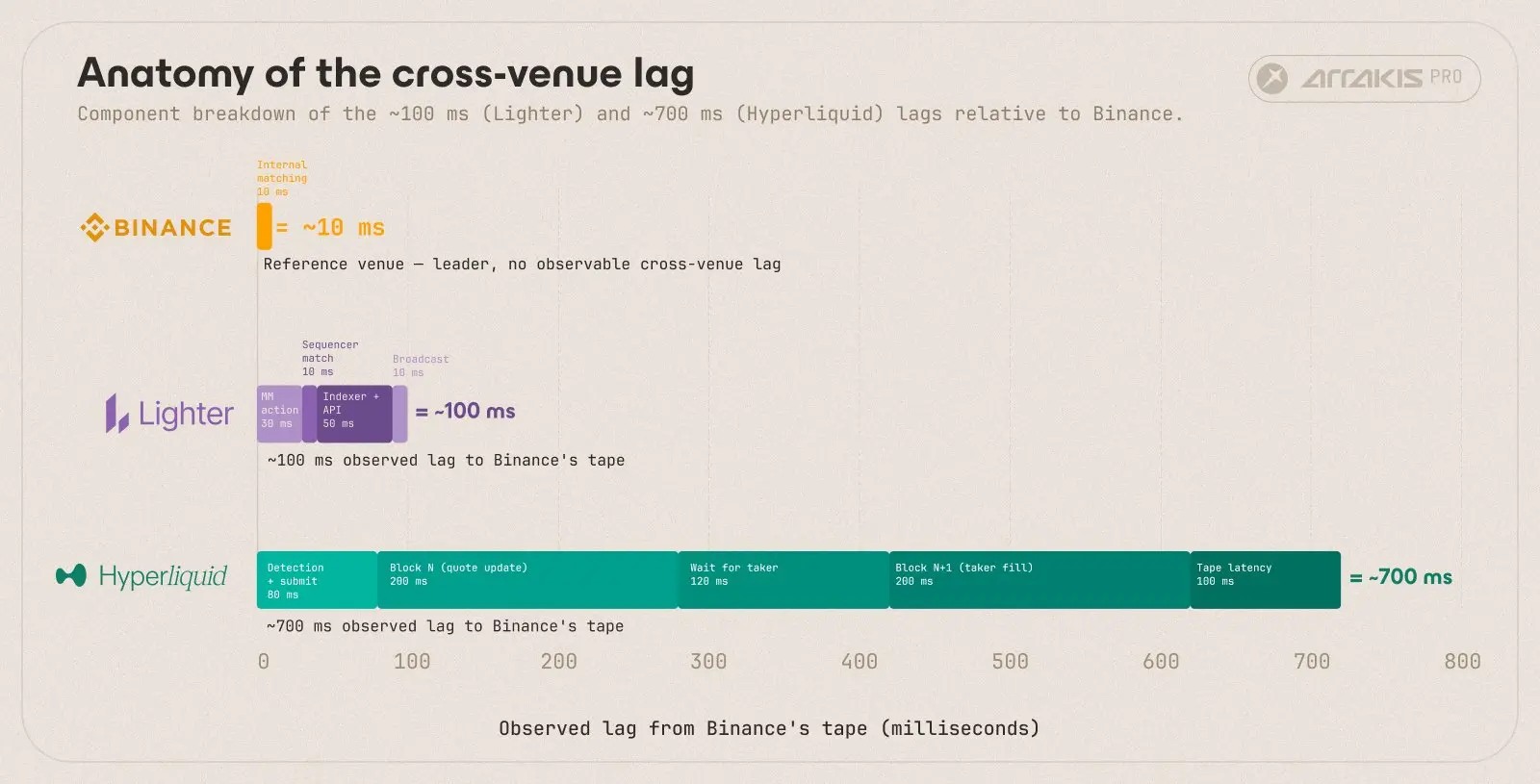

Where Does Hyperliquid's Delay Come From?

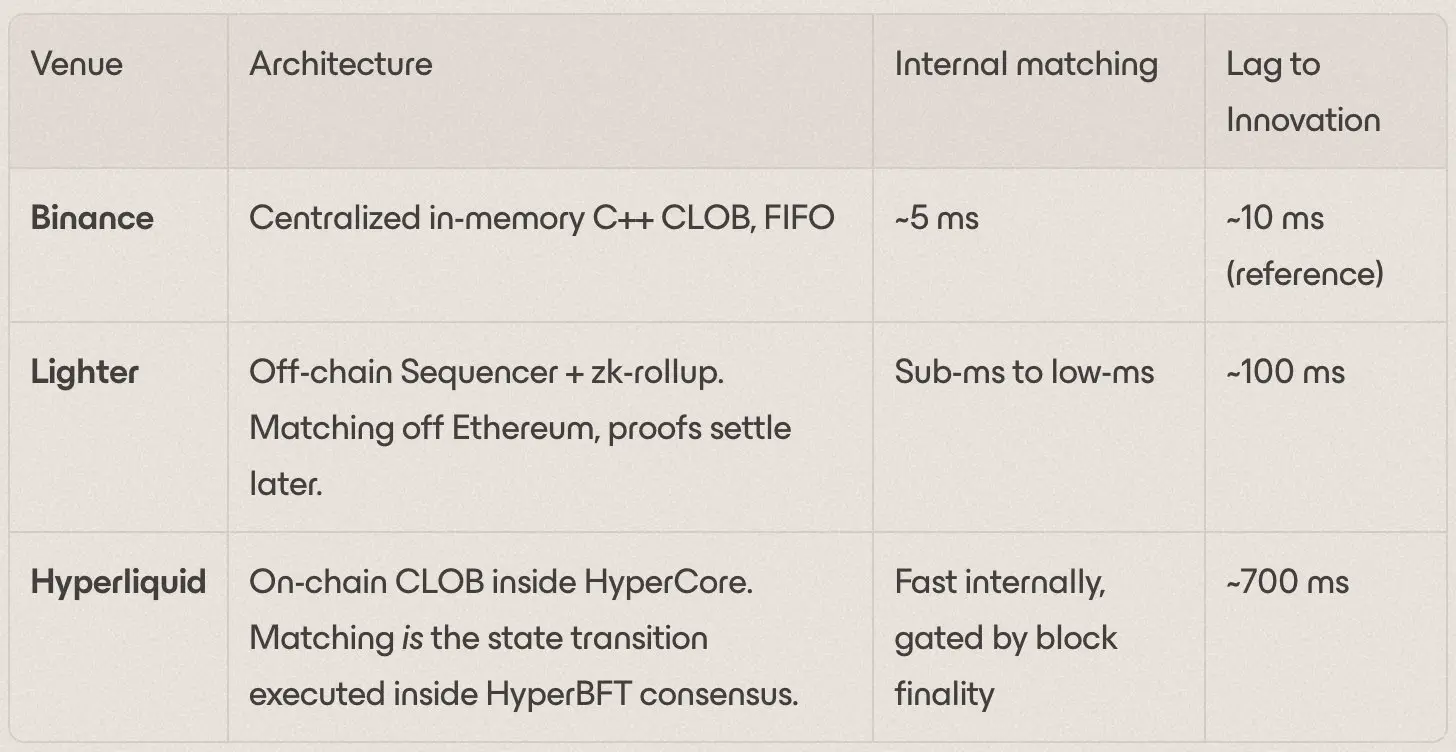

These three platforms utilize three completely different matching architectures.

Cross-platform delay analysis. Using Binance as the reference benchmark. Lighter's delay of approximately 100 milliseconds is primarily due to the time taken for the sequencer to indexer to API pipeline.

Hyperliquid's delay of approximately 700 milliseconds is primarily composed of two complete HyperBFT consensus cycles, one corresponding to the order maker's price update cycle (block N), and the other corresponding to the taker’s execution cycle (block N+1).

Both Binance and Lighter complete matching at millisecond speed in memory, while Hyperliquid's matching process essentially involves state transitions of HyperBFT, meaning each transaction must wait for approximately 200 milliseconds for block finality (according to Hyperliquid's official documentation).

Both Binance and Lighter complete matching at millisecond speed in memory, while Hyperliquid's matching process essentially involves state transitions of HyperBFT, meaning each transaction must wait for approximately 200 milliseconds for block finality (according to Hyperliquid's official documentation).

However, the actual observed delays in transaction records are around 700 milliseconds, not 200 milliseconds. The additional approximately 500 milliseconds is due to the maker-taker round-trip process built on single-block finality.

The most reasonable explanation is that this involves a maker-taker round-trip interaction spanning two consecutive blocks. Here’s the series of processes after a price change on Binance:

1. Stale liquidity remains on Hyperliquid. Existing market maker quotes are off compared to Binance’s new price.

2. Memory pool speed racing. Arbitrageurs speculative send a large number of IOC (Immediate or Cancel) orders targeting expected stale liquidity. Market makers issue cancel-and-replace orders to refresh their quotes, ensuring these operations enter the block's top. Market makers that fail to refresh quotes in this block will be arbitraged.

3. Block N is submitted at approximately 200 to 300 milliseconds. Cancel orders remove the market maker's stale quotes. New orders publish the refreshed quotes. Surviving IOC orders consume the remaining stale liquidity at the old price, so most trades in this block occur at stale prices relative to Binance.

4. At this point, Hyperliquid's order book has been cleared, but no one has traded at the refreshed quotes yet.

5. The taker starts trading at the updated price.

6. Block N+1 is submitted at approximately 500 to 700 milliseconds. The taker matches with the refreshed maker quotes. This is the first trade carrying new price information, linked to changes in the data our model captures regarding lagging prices relative to Binance.

This means that price changes on Binance take at least two complete HyperBFT cycles to be reflected in Hyperliquid's transaction data.

In contrast, Lighter completely bypasses this process. Its sequencer performs matching in memory; price updates and trades against those prices occur within the same millisecond. An approximate 100 milliseconds of delay reflects delays at the indexer and API levels, which is also the finest granularity of lead-lag time series we have added in the model.

What Lighter Proves

Lighter's pricing closely follows Binance, with only a small delay relative to Hyperliquid. This breaks the assumption that Hyperliquid's delays are because it is a DEX, as Lighter is also a DEX. Orders flow to a centralized off-chain sequencer, but the whole system achieves verifiable decentralization through settlement to Ethereum via zero-knowledge proofs (zk-proofs).

The difference lies in where decentralization is executed. Hyperliquid enforces decentralization at the matching layer: every order, cancel, and trade is confirmed by a collection of validator nodes; while Lighter executes decentralization at the settlement layer: the sequencer performs matching in memory before proving the accuracy of its trades to Ethereum.

Lighter exchanges speed for shifting the trust boundary from the matching layer to the settlement layer. Hyperliquid retains the trust boundary at the matching layer and thus incurs the cost of delays.

What Hyperliquid Can Do

To improve its pricing delay issues relative to price discovery platforms like Binance, Hyperliquid could make the following adjustments to its current design:

- More compact HyperBFT pipeline. By optimizing leader rotation, parallel voting, or networking, compressing the median block time to below 200 milliseconds. Each millisecond saved can significantly reduce the round-trip time of two blocks.

While this cannot eliminate the structural reasons for delays, any substantial improvement in block time could exponentially reduce pricing delays. - Pre-confirmation or soft finality layer. Establish an independent rapid channel for pre-confirmation of block packaging, then asynchronously realize HyperBFT finality. Market makers can publish quotes against the pre-confirmed state, leading to an effective decrease in the latency of price updates.

The trade-off is that pre-confirmation requires a trusted infrastructure or a margin backed by a penalty mechanism to ensure reliable commitment. Both methodologies would reintroduce trust assumptions currently evaded by Hyperliquid. - Decoupling matching from consensus. This is the most ambitious and costly option. Running an off-chain rapid matching layer to generate initial trading results, then batch-submitting them to consensus mechanisms, structurally aligns more closely with the design of Lighter.

While this would significantly lower the delay threshold, the trust assumptions would undergo substantial change, deviating entirely from the current model based entirely on free validation.

Each pathway requires profound modifications to the architecture at different layers and introduces trust assumptions that are currently absent from the system. Whether the delay improvements these methods bring are worth the price of additional trust assumptions must be decided collectively by the team and community.

What This Means

Hyperliquid has established its leading PerpDEX position in terms of liquidity, open interest, and retail participation. It is pioneering entirely new frontiers in DeFi, launching innovative markets that do not exist in traditional finance: weekend trading of stocks and commodities, perpetual contract markets for private equity before IPOs, inflation outcome markets, etc.

However, as the market matures and more participants join, the next round of competition in on-chain perpetual contracts will unfold on the delay track. Hyperliquid has built the most liquid platform on the basis of decentralized on-chain matching engines.

The suspense now lies in whether Hyperliquid can remain dominant in the price discovery of these innovative markets it has created while adhering to this design.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。