The so-called "on-chain American stocks" specifically refers to which investment products, what is their legal nature, whether the returns from investing in on-chain American stocks need to be taxed, and how to conduct tax planning?

Written by: FinTax

1 Introduction: Exchanges Rush to On-chain American Stocks

In 2026, on-chain American stocks transformed almost overnight from small-scale pilots into a new entry that exchanges collectively competed for. On May 26, Bitget officially launched the RWA platform Reality, bringing to market the tokenized American stock product rToken; platforms like Bybit earlier integrated xStocks, allowing platform users to trade some tokenized stocks within their accounts. Robinhood also launched various American stock and ETF token products for EU users and plans to support more RWA scenarios through its own Layer 2 blockchain.

Exchanges have been laying out the tokenization of American stocks track, spurring on the hot narrative of on-chain American stocks. Stocks and ETFs are becoming a more imaginative direction for the next stage of RWA; buying a tokenized asset that tracks the price of NVIDIA, Tesla, or the S&P 500 ETF is far more intuitive than understanding the complex on-chain income structure, giving on-chain American stocks a natural popularity among retail investors and trading demand.

When we shift our perspective on on-chain American stocks from exchanges to a wide range of investors, this emerging investment market represents vast opportunities, but also comes with concerns and risks due to information asymmetry: what specific investment products does "on-chain American stocks" refer to, what is their legal nature, are the returns from investing in on-chain American stocks taxable, and how should tax planning be conducted? The following will systematically break down the definition and structure of American stock tokenization, addressing the major concerns of investors, and briefly analyze possible tax planning issues.

2 What Exactly Are On-chain American Stocks: Concepts and Types

The term "on-chain American stocks" as commonly used in the market is not a strictly legal concept. More accurately, it usually refers to a category of financial instruments that provide investors with tradable economic exposure, income distribution, or rights certificates by referencing U.S. listed stocks, ETFs, or related equity assets through on-chain tokens or smart contract structures.

It is essential to differentiate between the "stocks" themselves and the "economic exposure to stocks." In traditional American stock investments, investors generally hold stocks as registered shareholders or beneficial owners under a brokerage account. However, on-chain American stocks typically only package part of the economic rights into tokens, with investors primarily gaining price appreciation exposure; some products feature dividend mapping or redemption mechanisms, but do not automatically confer full shareholder rights to the holder. In other words, what investors acquire may not necessarily be "stocks," but rather contractual claims against the issuer, rights certificates, or purely synthetic assets that track price.

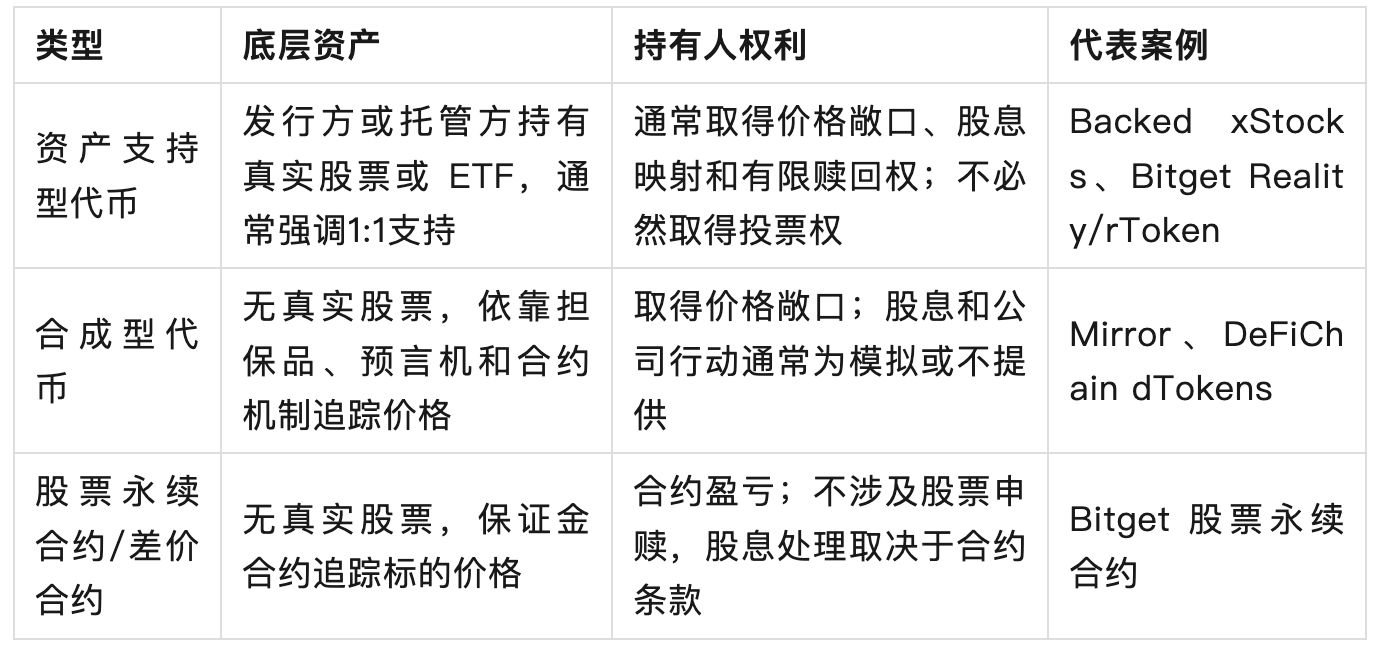

Based on publicly available project materials and market practices, current on-chain American stock products can be divided into at least three categories: asset-backed tokens, synthetic tokens, and perpetual contracts / contracts for difference.

2.1 Asset-backed Tokens

Asset-backed tokens are the model closest to the original connotation of "stock tokenization." Their core structure is that the issuer or its collaborating custodial institution holds real American stocks or ETFs in the traditional securities market and issues tokens corresponding to the underlying assets on-chain. Ideally, each token is backed by a proportional reserve of real stocks or ETFs, and users holding tokens can gain exposure to the price fluctuations of the underlying assets, and, where product rules allow, may gain rights such as dividend mapping.

This model can further be divided into third-party issuance and proprietary issuance by the platform. In the third-party issuance model, tokens are issued by external institutions, and exchanges mainly take on the role of product integration and distribution, allowing users to select tokens in a one-stop shop within the exchange system. For example, in xStocks, the issuer Backed Finance secures stocks and ETFs as reserves, deploying on the Solana chain to issue corresponding tokens, with Bitget, Kraken, and other platforms responsible for distribution and providing trading access.

In the proprietary issuance model, token design, custody arrangements, and other issuance activities are directly handled by the exchange or its affiliated platforms. For instance, Bitget's Reality/rToken products claim that each rToken is backed by real stocks from U.S. brokerages, with the issuer partnering with licensed brokers connected to Nasdaq and the New York Stock Exchange, and using an independent third-party organization for reserve proof, maintaining a reserve ratio of over 100%. Reality converts corporate dividends into stablecoins (USDT) for direct distribution to holders, and stock splits and reverse splits are automatically mapped to rToken balances.

2.2 Synthetic Tokens

Synthetic tokens do not directly link to real stocks but simulate the price performance of a specific stock or ETF through smart contracts, collateral, or oracle price mechanisms. When users buy this type of token, they essentially gain an on-chain synthetic exposure tracking the price of American stocks, without holding rights certificates supported by real stocks. Early products like Mirror Protocol and DeFiChain dTokens exhibit this characteristic.

The advantage of synthetic tokens is their rapid scalability; they do not require real stock custody and brokerage arrangements for each underlying asset. As long as they can provide prices and maintain sufficient collateral ratios, theoretically they can generate multiple stock price exposures. However, this type of architecture also comes with more apparent risks: if the market experiences violent fluctuations or collateral shortages, the token price may become unpegged from the target stock or ETF price. Compared to asset-backed tokens, synthetic tokens are closer to on-chain price derivatives rather than strictly tokenized stocks.

2.3 Perpetual Contracts / Contracts for Difference

Perpetual contracts / contracts for difference are another category easily included in discussions of on-chain American stocks. They typically do not hold real stocks or issue tokens representing underlying securities rights but use stablecoins as collateral to track price changes of a specific stock or ETF through contracts. Users trade positions and profit-loss differentials rather than the stocks themselves. Examples of such products include Bitget's NVDAUSDT, TSLAUSDT, METAUSDT, GOOGLUSDT, which are perpetual contracts for stocks using USDT as collateral.

Compared to other products, perpetual contract products are easier to implement because their logic is similar to crypto perpetual contracts: the platform provides price indices, sets collateral rules, funding rates, and liquidation mechanisms, while users trade price fluctuations of American stock underlyings using USDT or USDC. The advantages of perpetual contracts include high trading efficiency, the ability to go long or short, leverage support, and do not require complex stock redemption and dividend distribution arrangements. They do not provide underlying stock ownership and do not promise corresponding real stock reserves.

Table 1: Common Types of "On-chain American Stocks" Products

3 Tax and Regulatory Analysis of On-chain American Stock Products

As mentioned earlier, on-chain American stocks actually include multiple types of products with different legal natures, ranging from asset-backed tokens to perpetual contracts on American stocks to synthetic assets, each with distinct tax characterizations and compliance requirements.

3.1 Issuance and Operation

Taking asset-backed American stock tokens as an example, project operations involve several steps, including underlying shareholding, token issuance and custody, token holding and transfer, among others. Under U.S. tax law, the underlying shareholding entity (such as a U.S. brokerage as a registered shareholder) is obligated to withhold taxes on dividends produced under IRC §1441/§1442, generally withholding at 30% or the agreed tax rate for dividends paid to non-U.S. beneficiaries. For the token issuance entity, if the holders of the products legally enjoy "contractual rights to claim against the issuing entity," and their tokens or related contracts are characterized under U.S. tax law as specified NPCs, specified ELIs, or other materially similar arrangements connected with U.S. stocks, and if they pay or embed dividend equivalents to non-U.S. holders, the issuing entity may become a new withholding tax debtor due to the payment of what is termed "dividend equivalent payment" under §871(m). Meanwhile, the profits and losses from stock perpetual contracts are viewed as derivative trading profits and losses in most jurisdictions, not involving dividends, and do not trigger the typical dividends withholding under §871(m), unless the contract economically embeds or adjusts U.S. stock dividends, being recognized as §871(m) instruments with dividend equivalent characteristics, subject to technical analysis standards like delta. In short, the tax characterizations and treatments of different product types vary, and separately listing perpetual contracts and asset-backed tokens in terms of tax documentation is important for reducing declaration classification errors.

The tax optimization space for issuing and operating tokenized American stock products lies within compliance structures, which include reducing duplicate reporting, clarifying withholding entities, and utilizing tax treaties:

Clear Isolation of Product Lines

Considering the different tax characterizations of perpetual contracts versus asset-backed tokens (derivative profits and losses vs. dividends plus capital gains), separately listing the two product types in user billing and tax documentation can reduce the risk of classification errors for users in their resident countries' declarations.

Avoidance of CARF/CRS Double Reporting through Entity Segmentation

Clearly isolating "crypto asset services" (subject to CARF) from "financial accounts holding cash/fiat" (subject to CRS) at both the entity and account levels can reduce the risk of double reporting of the same balance, making the user's reporting paths more predictable. Additionally, operators should establish CARF and CRS reporting mappings at the entity level, identifying which information should be reported under CARF and which cash or traditional financial accounts may be reported under CRS, thereby reducing the risks of duplicate reporting, underreporting, and account classification errors.

Conduction of Treaty Benefits for Withholding Tax

In certain structures, the 30% dividend withholding rules could impose tax friction on non-U.S. holders. If the issuing entity or the underlying broker operates as a Qualified Intermediary (QI) and establishes a mechanism for collecting the residential identities of the holders, theoretically eligible parties could enjoy treaty-benefit withholding tax rates (usually 15% in most countries). The challenge lies in the anonymity of on-chain holders, who self-custody and can freely transfer, making the identification and collection of identities for treaty benefits technically nearly impossible—this is precisely a structural disadvantage of tokenized stocks compared to traditional brokerage accounts and remains an unresolved issue worth noting.

3.2 Individual Investors

For individual investors, a major misconception regarding on-chain American stocks is interpreting "on-chain holding" as "tax invisibility." With the gradual implementation of CARF and the revised CRS framework, the tax transparency of crypto asset trades and related financial accounts is steadily increasing. In the EU, DAC8 (local legislation for CARF) requires member states to apply related rules starting from January 1, 2026, and to complete information exchanges for the first reporting year by September 30, 2027; jurisdictions including the UK, the US, and Hong Kong have also committed to implementing CARF with corresponding legislative preparations.

In August 2022, the OECD completed revisions to the CRS framework, including specific electronic money products and central bank digital currencies within its reporting scope. The revised CRS mainly targets financial accounts and various indirect cryptocurrency-related transactions, including electronic money, central bank-issued digital currencies, and exposures to cryptocurrencies generated through derivatives or funds; while CARF focuses on on-chain or cryptocurrency-related transactions, requiring relevant institutions to report at the transaction level.

A prudent understanding of the applicable boundaries of both is that investing in on-chain American stocks is not a "one or the other" between CARF and CRS, and different tiers of information may trigger different mechanisms; at the on-chain token level, the platform serves as a Reporting Crypto-Asset Service Provider (RCASP) applicable under CARF. Meanwhile, underlying U.S. brokerage accounts, user stablecoin balances, and fiat currency balances may fall under CRS. These mechanisms may overlap within the same product, specifically requiring attention to the following aspects:

Stablecoin and Fiat Balances Held in Custody

User-held USDT in platform accounts, stablecoins used for redemptions, and fiat deposits may fall under CRS if the relevant entity is identified as a financial institution under CRS (holding financial accounts). While the OECD strives to avoid CARF/CRS double reporting, the practical division of "crypto assets subject to CARF, associated cash balances subject to CRS" still objectively exists.

Underlying Brokerage Accounts

Accounts at U.S. brokerages holding real stocks are indisputably traditional financial accounts, which themselves (with the issuer as the account holder) fall under the traditional reporting frameworks of CRS/FATCA, paralleling CARF reporting at the on-chain level. Thus, the same economic benefits may trigger CARF (on-chain tokens) and CRS/FATCA (off-chain brokerage accounts) regulatory requirements at different structural levels.

Of course, whether these institutional principles ultimately affect specific taxpayers depends on a series of practical conditions, such as whether the jurisdiction where the exchange operates has implemented CARF, whether there is an activated exchange relationship with the user's resident country, and the access progress of the user's resident country.

It is important to point out that whether information can be automatically exchanged and the taxpayer's obligations under their resident country's tax laws are two independent issues; the latter is not exempted by the absence of the former. In other words, even if on-chain American stock holding information is currently difficult to be automatically exchanged back to the resident country via CARF or CRS, the holder still has the obligation to voluntarily report and pay taxes on their related offshore income (such as capital gains or dividend income) according to their country's tax laws.

Finally, the invisibility of on-chain assets is not the end of the story; the financial chain ultimately must return to the traditional financial system—when holders convert earnings into fiat, transact via bank accounts, or use them for actual consumption or purchasing assets, these stages remain within the sight of tax authorities and anti-money laundering regulation; the obscurity of on-chain holdings will ultimately be re-exposed at the contact points with the traditional financial system.

Conclusion

Based on market data, the development of tokenized American stocks is still in its early stages, but the growth rate is increasing enough to attract exchanges and issuers to layout in advance. CoinGecko's 2026 RWA report shows that the market value of tokenized RWA increased from $5.42 billion at the start of 2025 to $19.32 billion by the end of the first quarter of 2026, a growth of 256.7% over 15 months; tokenized stocks account for approximately 2.5% of the RWA market, while tokenized ETFs account for about 1.5%. Although this volume is still limited compared to the global stock market, it is sufficient to illustrate that stocks and ETFs are gradually standing out from the RWA narrative, becoming a new entry for trading platforms to compete for. For exchanges, the appeal of tokenized American stocks lies not only in market trading volume itself. Crypto spot, derivatives, and other businesses are influenced by market cycles, and exchanges need to introduce new tradable assets to expand revenue from trading, market making, custody, redemptions, and structured products. For users, the advantages of tokenized American stocks are reflected in smaller participations, extended trading hours, and near real-time settlements.

"On-chain American stocks" may seem like a mere transfer of American stocks onto the blockchain, but behind it is not a single product form, but rather various structures corresponding to different underlying assets and holder rights. If they are simply understood as American stocks, investors may underestimate product risks. If they are all understood as crypto assets, operators might overlook compliance requirements stemming from the underlying securities and dividend withholding rules. For market participants, the opportunities presented by tokenized American stocks deserve attention, but the complexity of the products regarding tax and regulation cannot be ignored. Only by rooting in a compliance mindset can one navigate steadily and far as the RWA market ventures into deeper waters.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。