Two one-sided specialists gamble on a native full-stack that has never lost on an original battlefield.

Written by: Will A-Wang

The most valuable ability in the payment industry has never been processing transactions, but rather ensuring that money stops where it should and flows where it should—especially in places that others cannot access or reach.

This is precisely what Nuvei intends to acquire with its $2.75 billion purchase of Payoneer.

This article aims to clarify three points:

- This transaction is not about buying a company, but rather acquiring a license network—an entry map that foreign payment companies could almost never build themselves globally;

- This is a self-rescue for two one-sided specialists, not a marriage of two winners;

- Essentially, it is a PE valuation arbitrage, betting on a proposition that no one has navigated: whether a stitched-together full-stack can outperform a native full-stack.

And these three points share a common thread—they are not grown organically; they are bought. Let us first look at the transaction itself, and then dissect its two halves: the acquiring side of Nuvei and the payment side of Payoneer, before returning to its positioning in the global market.

1. $2.75 Billion Cross-Border Acquisition

To read a merger, start by looking at its press release and see who gets the heaviest adjectives: this one goes to the license.

On June 15, Nuvei, a Canadian payment company that has been privatized by Advent for less than two years, announced an all-cash acquisition of the U.S.-listed cross-border payment platform Payoneer for $7.40 per share, totaling about $2.75 billion. The merged entity is expected to generate annual revenue of approximately $3 billion and process over $500 billion annually, serving more than 2.4 million customers across over 190 countries. The transaction is expected to be completed by mid-2027.

Phil Fayer, Chairman and CEO of Nuvei, provided a definition for this transaction that deserves a word-for-word reading:

“The merged platform will allow businesses to collect payments, make payments, issue cards, manage funds and foreign exchange, and access embedded financial services—all at scale.”

This is the standard definition of a global payment full-stack: packaging every link of a transaction from receiving payments to funds and foreign exchange into one platform, serving customers active on leading digital platforms like Amazon, eBay, ByteDance, Shopify, Upwork, and others.

However, the actual "Key Component" singled out in the press release is not technology or customers but rather the license—specifically, Payoneer's regulatory map in major jurisdictions worldwide, which explicitly names online payment licenses in mainland China and cross-border payment aggregator authorization in India.

In contrast, media headlines are almost all focused on "stablecoins" and "AI," but these two words are tucked into a paragraph that begins with "ALSO," and carries the title "Emerging."

The official priority is clear: the full-stack is the narrative, the license is key, and stablecoins and AI are visions for the future.

2. The Acquiring Side: Nuvei is Selling Transactions That Others Are Reluctant to Take

Acquiring is a scale business, and Nuvei is almost the one that relies least on scale within this business.

Ranking global acquirers by processing volume, you will find that Nuvei does not make it into the top tier. According to TSG's 2026 U.S. acquirer directory, after swallowing Worldpay, Global Payments tops the list with about $2.8 trillion in processing volume, followed closely by JPMorgan and Fiserv, with Stripe processing $902.5 billion alone in the U.S., and even Adyen having $316 billion in just the U.S. market. In contrast, Nuvei's total global processing volume is about $240 billion per year—less than 30% of Stripe's U.S. volume.

A company that does not have a scale advantage, why is it privatized by Advent for $6.3 billion, then turns around to spend $2.75 billion to buy Payoneer?

The answer lies not in how much it processes, but rather whose money it processes.

2.1 A Niche It Dominates, Though Small

Nuvei's flagship business is iGaming. In the regulated online gambling and sports betting payment sector, it holds about 12% market share and is among the top five non-bank acquirers by the number of local payment methods supported. Its client list includes sports betting and online casino operators like DraftKings, Betsson, and Carousel Group—not consumer brands, but casinos.

A phrase from a U.S. equity analyst captures it well:

Nuvei has built a robust moat within the limits of what a payment company can achieve, with top-tier technology and connectivity, even dominating a niche—though that niche is neither large nor glamorous (however small and ignoble).

The term "ignoble" is key to understanding Nuvei. It operates in high-risk sectors like gambling, crypto, adult services, and foreign exchange, which mainstream acquirers avoid like the plague.

The financial structure of this business corroborates this point. The management model disclosed in the privatization documents divides Nuvei into three segments: Global Commerce (global e-commerce, including iGaming) is expected to generate around $689 million in revenue by 2024, with an anticipated compound growth rate of 18%; Paya, dealing with B2B, government, and ISVs, is expected to generate about $245 million at the same growth rate; while the original SMB business from Pivotal Payments is expected to see revenue around $310 million, with a yearly negative growth of 3%. The real engine is high-risk online cross-border payments, while the old offline SMB business is shrinking. The focus of this company has shifted over twenty years from corner shops to offshore casinos.

Its identity is also a subtle thread in this transaction. Nuvei was publicly listed on both the Toronto and Nasdaq exchanges under the ticker NVEI, and was privatized by Advent in November 2024, leading to its delisting. Private companies do not have to explain to the public market—this is why the financial details of the Payoneer transaction are disclosed much less than when it was publicly listed.

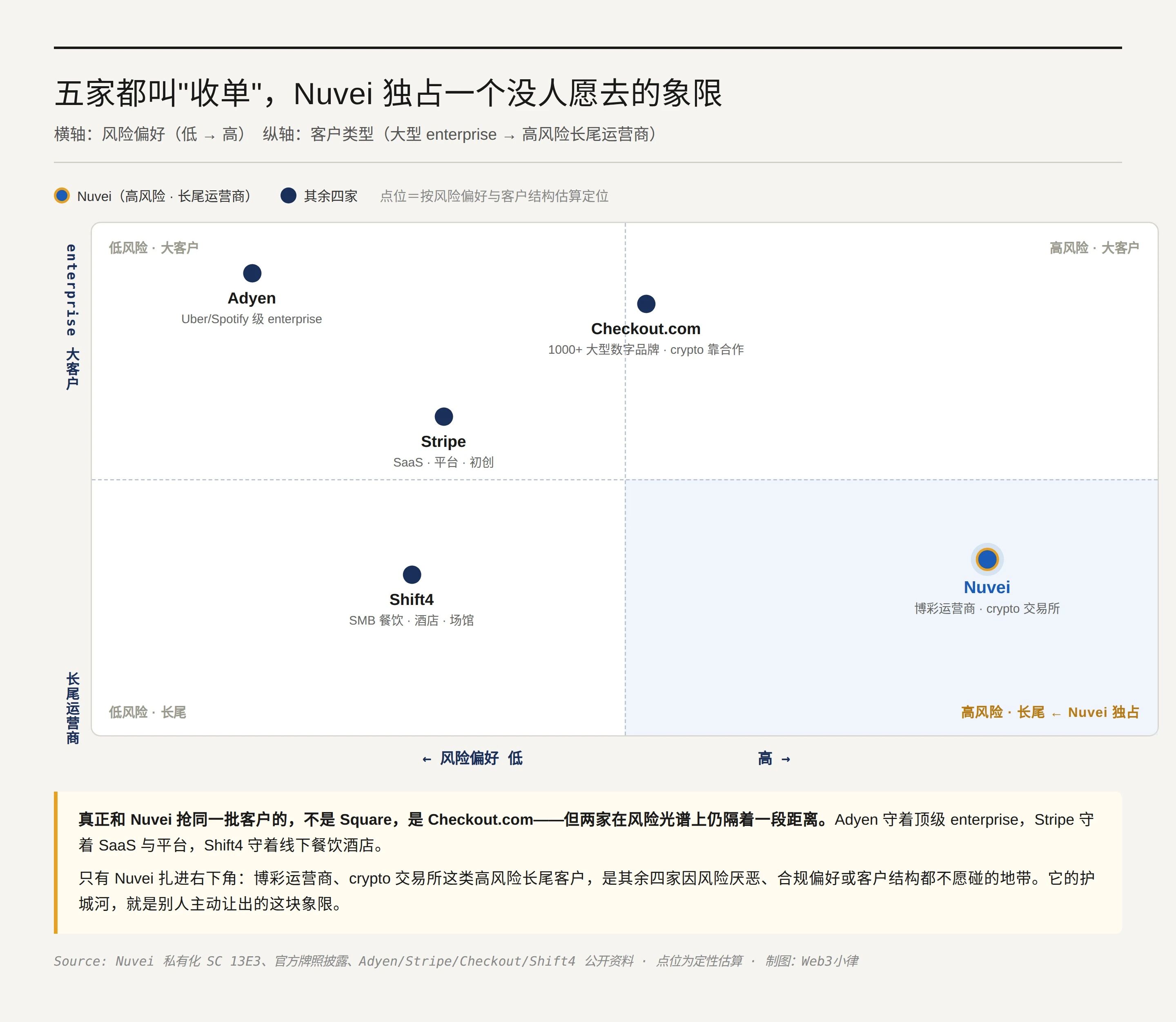

2.2 Differentiation Emerges When Five Are Grouped Together

"Acquiring" is a label that packs five completely different businesses into one term. Placing Nuvei alongside several companies it is often compared to instantly reveals differences.

Within the table are two judgments:

- Shift4 is almost a mirror image of Nuvei: similarly listed, similarly acquisition-driven, and similarly deeply vertical, but it focuses on offline—restaurants, hotels, sports venues—cementing high-touch industries with the SkyTab cash register system. One targets offline, while the other targets online; their hunting grounds do not overlap.

- Adyen stands at the other end of the risk spectrum: it holds a complete banking license and maintains strict underwriting practices while avoiding unlicensed foreign exchange, crypto, and small to medium gambling businesses as per industry norms—what Adyen shuns is precisely what Nuvei thrives on.

However, finding a truly similar competitor to Nuvei is not easy. Checkout.com, often compared, serves thousands of large digital brands, using Coinbase’s collaborative infrastructure for crypto connections rather than handling high-risk acquiring themselves—it is much further from Nuvei’s hunting ground than it appears. No one is really competing with Nuvei for gambling operators or crypto exchanges, which are high-risk long-tail clients: Adyen avoids them due to risk aversion, Stripe avoids them due to compliance preferences, and Shift4 and Square avoid them due to a focus on offline. Comparing Nuvei to Square is akin to comparing offshore casinos’ cross-border acquiring to street-side coffee shops’ card machines—both may be termed acquiring, but they are not in the same market.

2.3 Two Licenses, but Underwriting Authority is the True Moat

Nuvei's truly scarce asset is its underwriting authority. A local acquiring transaction requires two licenses to overlap: a regulatory license (EMI, MTL) and card organization membership. The latter only implies that the underwriting authority lies with a self-holding primary member; if it falls short of that, it must hang on a bank sponsor, which could drop your gambling or crypto merchants at any moment due to risk preference, leaving you with no recourse. For a company that relies on high-risk industries, this is a matter of life and death.

Using this measure to gauge Nuvei, its license map reveals two patterns.

- Self-holding in Europe—holding EMI licenses in the UK, Netherlands, Cyprus, and Lithuania, combined with primary membership in Visa and Mastercard Europe, both licenses are intact; much of its high-risk iGaming and crypto business lies in Europe, which is not by chance.

- Borrowed licenses in the U.S.—holding various state MTL, while card access is under the ISO identity connected to banks like Citizens and JPMorgan Chase. In other words, in the U.S., the world’s largest acquiring bank JPMorgan is both a rival and an upstream sponsor for Nuvei. The underwriting authority is rented, not owned. Sponsor agreements usually reserve the unilateral right to tighten or terminate specific high-risk merchants, a power that JPMorgan has not exercised over Nuvei yet, but this power is written in the contract, inherently a sword of Damocles.

This is also why it is acquisition-driven. Building a complete set of "regulatory licenses plus primary membership" is slow, expensive, and a grind for approvals; acquiring a locally licensed entity often buys both licenses at once—cases like licensed payment institutions in Brazil and Paywiser in Japan are ready examples. It is incrementally working to transition itself from borrowed to self-held licenses in over 50 local acquiring markets; the news of it going live in Mexico with a direct connection described it as "the latest step," not "the final step."

The difference between Nuvei and Adyen lies not in "self-holding or borrowed licenses" but in the weight of those licenses.

Adyen holds a complete Dutch banking license—the heaviest payment license, meaning they are at the end of the settlement chain, relying on it for direct connections in almost all markets (including the U.S.); Nuvei holds an EMI license in Europe, is stable, while still relying on JPMorgan’s license in the U.S. Stripe relies even more on borrowed licenses—it mainly uses BIN leasing to connect to card pathways and has only just applied for a bank license that would allow direct connections by 2025; Shift4 acquired Finaro to gain access to a European bank license all at once. The four entities do not differ in "should we hold a license," but rather in "how many licenses to hold and to what extent to self-hold."

2.4 The Twilight of One-Sided Specialists

But the moat's water level is falling.

From 2025 to 2026, the entire acquiring industry is undergoing intense consolidation. Global Payments swallowed Worldpay for $24.5 billion, and even Adyen, traditionally advertizing itself as "a single platform, never acquiring," has begun making exceptions to buy companies—an experienced observer remarked that the company, which long avoided mergers, changing its course is a clear signal. Once with a stock price exceeding €80, Adyen's market value today is lower than many Series C fintechs. Scale players are using mergers to flatten each other’s boundaries.

For one-sided specialists like Nuvei, the pressure is coming from both ends. One end is scale—it can never catch up to Stripe and Global Payments in size on the acquiring side. The other end is full-stack—Stripe is moving towards cross-border and multi-currency, while players like Airwallex are doing both acquiring and payouts, embedding "receiving" and "paying" into the same account.

When competitors can complete both receiving and sending in one interface, a specialist that only knows how to receive begins to lose bargaining power.

This is the underlying logic behind Nuvei's acquisition of Payoneer. It is not just filling a business gap; it is filling a directional gap. Nuvei is a high-risk specialist on the acquiring side, while Payoneer is a marketplace specialist on the payment side—two one-sided players forced into a corner by full-stack competitors, needing to merge for survival.

The merger is prettily described as “money in meeting money out,” but described coolly, it is two one-sided specialists rescuing themselves in the era of full-stack.

3. The Payment Side: Payoneer is Selling Access to Hard-to-Reach Countries

Payoneer transfers money to corners like Vietnam, Pakistan, and the Philippines that Stripe and Adyen are too lazy to touch—this business has supported it for twenty years but is now conversely trapping it.

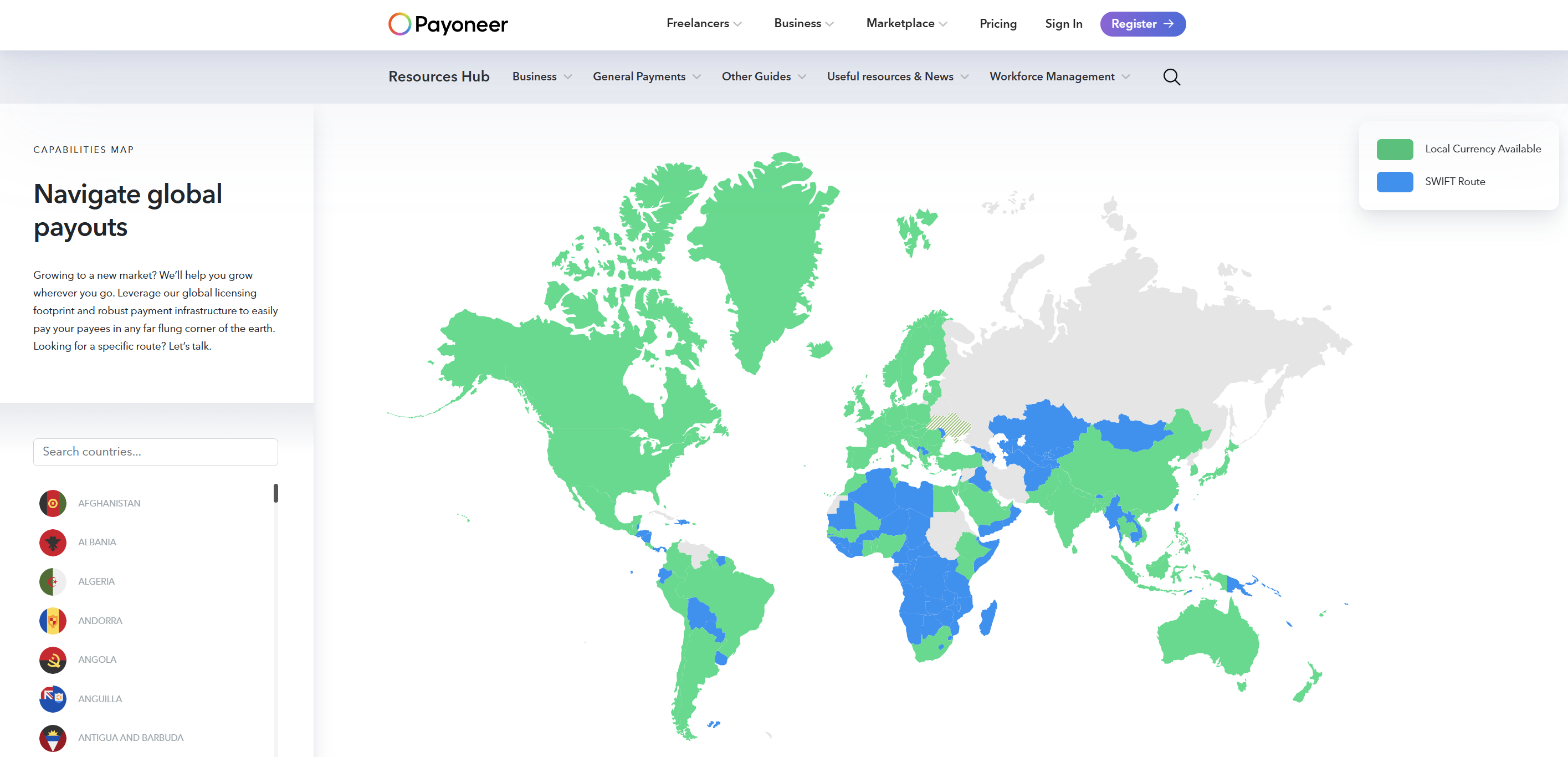

Founded in 2005, Payoneer started simply: issuing prepaid cards to freelancers scattered around the globe so they could receive dollars from a U.S. platform. Twenty years later, it serves over 5 million active customers, with total processing volume estimated around $82 billion in 2025, connecting over 210 countries and more than 160 currencies, thanks to a network woven from nearly 100 banks and payment partners. It transformed a small initiative into infrastructure: enabling Amazon sellers working independently in Vietnam and digital agents in South America to receive funds from platforms into their local accounts.

(Global payment capabilities, Payoneer)

Conversely to Nuvei, Payoneer is a public company—Nasdaq ticker PAYO—listed through a SPAC in 2021. Therefore, the shape of this transaction is a contrast: a private PE platform, Nuvei, acquires a publicly traded company that is struggling with market valuation.

In 2025, Payoneer crossed the $1 billion annual revenue threshold for the first time, buying back 8% of its shares—both demonstrating its value and failing to convince the market to assign a corresponding valuation. The acquisition price of $7.40 is where the divergence between the market and the buyer lies.

3.1 A Time Bomb Hidden in the Revenue Structure

What Payoneer should be scrutinized for is not how much revenue it generates, but rather where that revenue comes from. Its revenue composition in 2024 is: approximately 45% from marketplace sellers, about 19% from B2B SMBs, while interest income accounts for 26%.

That 26% is a time bomb. Payoneer manages around $7.9 billion in client funds, with over 80% earning interest—this translates to around $230 million in interest revenue for 2024, nearly all of which is pure profit without any cost. The high interest rates of recent years have allowed this money, which belongs to customers, to generate significant profits for Payoneer while simply lying idle. In a sense, it has, at one point, become a "money market fund disguised as a payment company."

But the management is more aware of this bomb than anyone—they are actively defusing it.

First, by hedging: locking in a substantial portion of interest income for 2026-2028 regardless of interest rate movements; second, by redirecting growth focus to stickier B2B SMB and "high-value" clients transacting over $10,000 per month, which had already accounted for over half of total transaction volume by early 2026.

The effect is tangible: in 2025, it withstood the headwind of a $25 million decline in interest income, relying on core business growth to boost overall profits, publicly only presenting numbers excluding interest. A company going to such lengths to prove that it can "survive without luck" inherently indicates how much luck has previously played a part.

3.2 License Map: Same Strategy as Nuvei

Payoneer’s moat is similarly described in its official press release as a "key component"—not technology, but licenses. This point is identical to Nuvei, even in strategy: relying on acquisitions to buy licenses and conquer markets others cannot.

It holds EMI licenses in the UK and Ireland, along with licenses in the U.S., EU, Japan, Singapore, Australia, and Hong Kong. But the truly valuable assets are two tough nuts to crack:

- China: In 2025, it acquired a licensed payment institution, Easylink, becoming the third foreign platform licensed to operate online payments in China—something Visa and Mastercard have spent over a decade trying to accomplish without success. Payoneer had tried to establish a 46% joint venture in China in 2019 to apply for a local license, which eventually led to its direct acquisition of Easylink in 2025.

- India: In early 2026, it received the Reserve Bank of India's principle authorization for cross-border payment aggregation, allowing it to conduct two-way cross-border transactions for Indian importers and exporters. Both licenses are not acquired through applications, but rather obtained through purchases and endurance.

However, Payoneer's cross-border model diverges fundamentally from Nuvei's. Nuvei desires "to hold licenses and underwriting in core markets," because its business is acquirers, and the underwriting authority must be in hand; Payoneer seeks "to transfer money into local accounts in every country," following a mixed network of self-held licenses and nearly 100 banking partners.

It does not need to hold a license in all 190 countries; it needs 7,000 trade corridors to be accessible. One seeks "self-held underwriting," while the other chases "compliance network coverage"—two businesses, two licensing philosophies.

3.3 Vulnerability: Its Most Profitable Segment is Being Undercut at Lower Prices

Payoneer's moat lies in its native integration with marketplaces—when you sell on Amazon, freelance via Upwork, or receive funds from Fiverr, money can directly enter your Payoneer account before cashing out to local currency. This direct connection was built over twenty years and is difficult for new players to replicate instantly. However, it has a fatal experiential weakness: FX is expensive.

Airwallex has mainstream currency exchange fees around 0.5%, Wise approximately 0.57%, while Payoneer fluctuates between 0.5% to 3.5%—0.5% is the lower limit for transfers between Payoneer accounts using mainstream currencies, and 3.5% is the upper limit for withdrawing smaller currency types, creating a difference of seven times. They also charge annual fees. Once opponents no longer utilize Payoneer, costs immediately gravitate toward the upper limit.

The high costs are not due to the pricing team's lack of effort, but rather a necessity of their business model.

Payoneer’s moat is about locking customers into its closed network—charging no fees for entry but monetizing the exit (withdrawing, exchanging, or transferring to non-Payoneer counterparties). FX is not a service it intends to compete on; it is a monetization gate after locking in users, offering no incentive to lower it to 0.5%.

On a deeper level, much of its profit over the past few years has come from interest on customer balances, passively collected, making it naturally insensitive to exchange rate discounts. In contrast, players like Airwallex, which do not hold deposits and must earn through transactions, have been forced to make FX as cheap as possible from day one. One survives on transaction volume, while the other survives on interest—hence Airwallex can use FX as a weapon, while Payoneer can only regard it as a gate. The expense of FX and reliance on interest are ultimately two sides of the same root problem: comfort derived from the era of cash flow.

Thus, this erstwhile moat, today is becoming a reason for loss, as Airwallex aggressively attacks with a 0.5% transparent fee rate and Shopify plugins. Airwallex offers broader options (multi-currency accounts, business cards, expense management, APIs), while Wise is cheaper and more transparent, both simultaneously pinching Payoneer's market share among marketplace sellers. Its two most lucrative segments—interest on deposits and the closed network FX—are at risk, one due to the luck of interest rates, and the other being eroded by cheaper competitors.

Consequently, Payoneer's situation is strikingly similar to Nuvei's: one is on the acquiring side and the other on the payment side, both being one-sided specialists cornered by full-stack competitors. What they need is not to optimize one more product, but rather a breakthrough in a direction. This is precisely why they are willing to be absorbed.

4. How to Position This Transaction: An Edge Full-Stack, an Arbitrage Bet

This transaction must be viewed in two layers: it stitches together an edge-based full-stack, while inherently being an arbitrage bet on valuation discrepancies.

4.1 Edge Full-Stack

This network is real. Nuvei has taken Brazil, Mexico, and Japan on the acquiring side, while Payoneer has taken on China and India on the payment side—together, they form a complete set of access criteria for North America, the EU, China, India, Southeast Asia, and Latin America.

In the payments business, licenses cannot be replicated by technology, cannot be rapidly bought by capital, and cannot be transferred between different markets. The merger of two one-sided specialists saves each the five or ten years needed to acquire licenses in each market individually. This is a network that foreign payment companies could almost never build themselves.

However, it is a network built on the edges, not the mainstream. Stripe and Adyen occupy the center—low-risk, large enterprise, developed markets; the Nuvei+Payoneer full-stack addresses the edges—high-risk industries, long-tail sellers, and difficult-to-enter markets. It is not competing with Stripe for SaaS customers in Silicon Valley; it is building a full-stack where others are unwilling to go.

This is both a moat and a ceiling: margins are high in edge areas, but it’s hard to spin a sexy growth story like Adyen.

Additionally, this edge network has a crack; the license that is most valued by officials could arguably be the most vulnerable. Payoneer holds licenses in China, while Nuvei primarily operates in gambling and crypto—two industries explicitly forbidden in China. Coupled with the beneficial ownership transparency filings beginning in November 2024, the PBOC can see who the offshore parent company of the license is. The license touted as a crown jewel could also be among the first to be scrutinized.

4.2 Arbitrage Bet

Whether the licenses can be retained is one question; how much this network is worth is another, and a more critical one—because the true motive behind this transaction lies in the valuations.

Industry media almost uniformly interpret this as a "countering Stripe" move. This is not incorrect—what the merged entity is stepping into is a market where scale is becoming vital, with Stripe recently achieving a $91.5 billion valuation, placing it on a collision course. However, a more critical judgment comes from a repeatedly validated industry observation: this year’s string of acquisitions by Stripe, Mastercard, Flutterwave, and Airwallex all point toward "control points" in the transaction lifecycle—billing, settlement, data, and licenses.

Everyone is not just probing; they are seizing the same set of capabilities while they can still buy them. Building organically takes time, whereas acquisitions are a shortcut— the entire market is reorganizing around “platform control.” Nuvei's acquisition of Payoneer is merely the largest move in this territorial expansion.

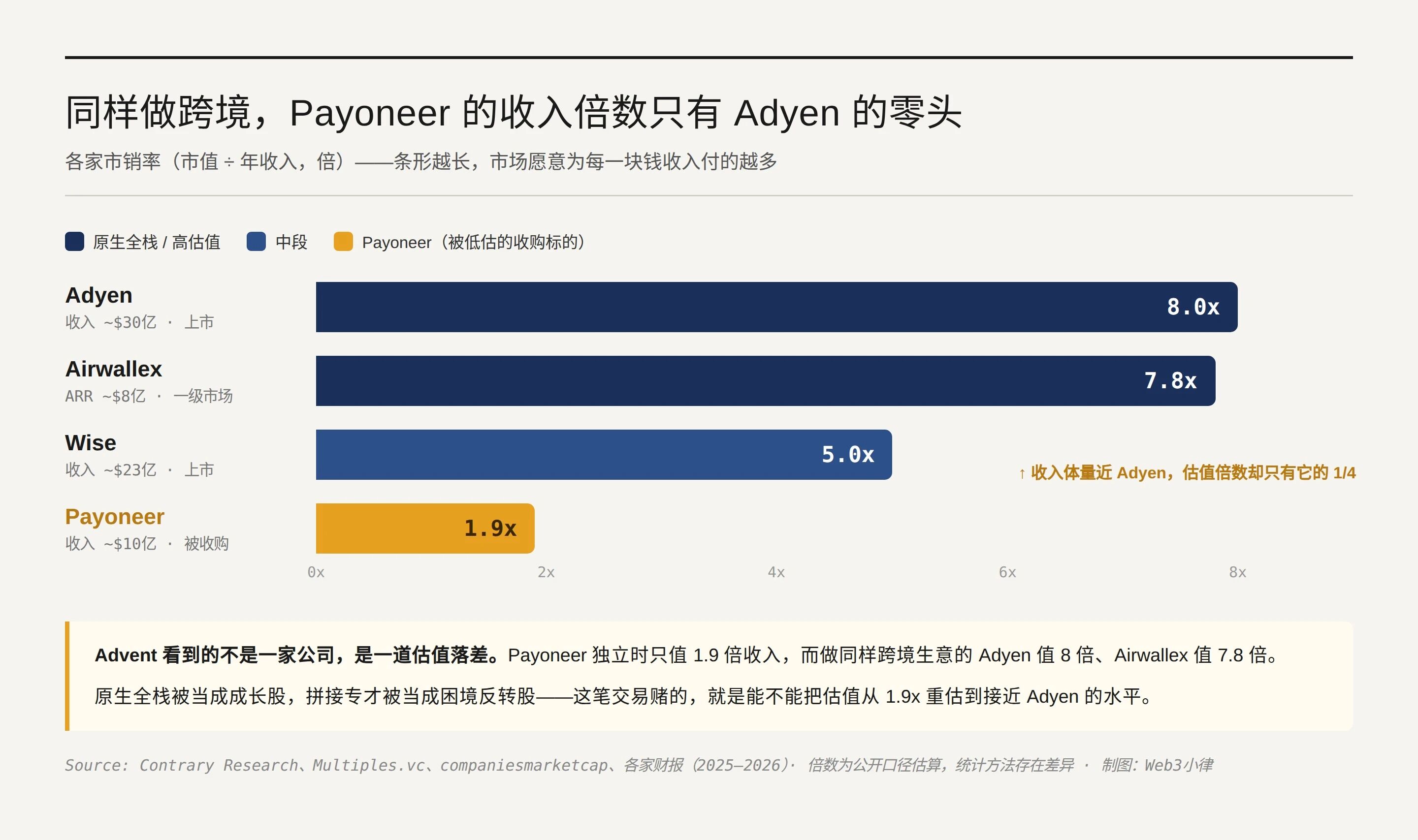

Operating in cross-border trade within the same revenue scale, the market can assign drastically different prices. When players in this lane are lined up in one table, the disparities are immediately evident.

Three figures placed together illuminate self-judgment.

The merged entity has an approximate revenue scale of $3 billion, comparable to Adyen—but the market’s valuation multiples for the two are completely dissimilar. In publicly comparable terms, Adyen stands at about 8 times revenue, Wise at 5 times, while Payoneer had only 1.9 times when independent. Operating in cross-border environments, Adyen commands top-tier valuations, while Payoneer receives bottom-level valuations.

This is the fundamental reason Advent is willing to make a move: enough revenue scale, a market price that is low, and the gap in between is the PE arbitrage space.

The comparison with Airwallex is most striking. Airwallex has an $800 million ARR and an $8 billion valuation—its revenue is only a fraction of that of the merged entity, yet its valuation is on par with the overall purchase price of Payoneer.

Why does the market assign it such a high premium? Because it is a native full-stack, organically grown, tech-led—viewed by capital as the future; whereas Nuvei+Payoneer comprises two one-sided specialists forced into a merger, seen as the past. Although both claim to be full-stack, one is treated as a growth stock while the other is seen as a distressed turnaround stock.

Thus, the most honest interpretation of this transaction is not that “two specialists see the future of full-stack,” but rather that “Advent sees an asset generating $3 billion yet only worth 1.9 times, paired with its similarly undervalued Nuvei, betting on a valuation revaluation.”

Full-stack is the narrative; arbitrage is the motivation.

All-cash, 5.5 times leverage, privatization operations—these are the fingerprints of PE financial tricks, not the fingerprints of a product vision.

And what it is betting on is a proposition that no one has navigated successfully: whether a stitched-together full-stack can outperform a native full-stack.

Airwallex has proven that a native full-stack can command high valuations, but its revenue is only a fraction; Adyen has shown that a single platform can attain high valuations, but it does not touch high-risk or long-tail segments. Nuvei+Payoneer must prove a third path—using acquisitions to stitch together two specialists into a full-stack, expanding in edge markets, and then convincing capital that this stitched entity is worth Adyen's valuation.

4.3 The Largest Question Mark Above

This path has never been successfully traversed. Fiserv amassed a slew of assets, yet long suffered valuation pressure; FIS acquired Worldpay only to sell it at a discount years later. The specific failures of the two cases differ—one was overly diverse in assets, while the other’s strategic direction was flawed—but they share a commonality: the capital market has a structural discount on "stitched entities."

A bunch of licenses and businesses accumulated through acquisitions, even if each piece looks fine when viewed in isolation, the market finds it hard to believe they can be integrated into a coherent growth-synergizing whole, and thus value them as "value stocks" rather than "growth stocks." The internal frictions of integration are superficial; the true curse of such transactions is the valuation discount.

Nuvei bets on being different: its twenty years of acquisition muscle (having seamlessly integrated SafeCharge and Paya), the patience from Advent's privatization that doesn’t require explanations to quarterly reports, and a demand side more certain than ever before—when stablecoins and AI genuinely begin reshaping cross-border payments, a global network of licenses covering China, India, and high-risk industries will be worth much more than it is today. That future, stuffed into an "also" paragraph by the officials, may indeed be the true long-term bet of this transaction, yet no one dares to write it into today's purchase rationale.

Therefore, this transaction has only two possible outcomes. Either the full-stack stitched together by the two specialists actually works, valuations reappraise from 1.9 times to approach Adyen’s 8 times, resulting in Advent earning a textbook-level arbitrage; or the stitched entity repeats Fiserv's mistakes, the license network is developed, but the valuation remains stuck at a "value stock" discount.

5. In Conclusion

Enticingly articulated, it is money in meeting money out. Coolly stated, it is two specialists cornered by the full-stack era, stitching together their respective licenses accumulated over twenty years, betting on a future no one has navigated successfully.

What is bought has never been a company; it is a bet.

And in the cross-border B2B payment arena, this bet has yet to be won.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。