The first interest rate meeting since Warsh took over the Federal Reserve is about to be revealed: The interest rate is almost certain to remain unchanged, but the language leaning towards accommodation is expected to disappear, inflation forecasts are likely to be significantly revised up, and the dot plot shows initial rate hike expectations—the real suspense lies in every word of Warsh's press conference.

Author: Xu Chao

Source: Wall Street Insights

The first interest rate meeting chaired by Kevin Warsh since his appointment as chairman of the Federal Reserve will reveal its results early Thursday morning Beijing time. The interest rate is almost certain to remain unchanged, but there are significant market divergences regarding the language of the policy statement, the economic forecast dot plot, and the signals from Warsh's press conference—this "debut" has real variables that are far more complex than the interest rate number itself.

Regarding the policy statement, Goldman Sachs, Bank of America Securities, and Morgan Stanley all expect the Federal Reserve to remove the "accommodative bias" language that has been in place for months, marking a formal communication from the committee that the probabilities of rate cuts and hikes have become more equal.

At the same time, the updated economic forecast is expected to show a significant upward revision in inflation forecasts—Goldman Sachs predicts that the median core PCE forecast for 2026 will be revised up from 2.7% in March to about 3.3%—and the median in the interest rate dot plot is expected to shift from "one rate cut this year" to "holding steady this year," with a few possible rate hike points appearing. The advancement of the US-Iran agreement has significantly eased external inflationary pressures by causing a sharp decline in oil prices, but core inflation's stickiness continues to limit policy space.

The focus will be on Warsh's press conference. Bank of America Securities pointed out that if he characterizes recent inflation as a one-time supply shock and emphasizes the disinflation potential driven by AI, long-term interest rates may face selling pressure; if he clearly endorses the rate hike path, the 2-year SOFR may rise by about 15 basis points, providing directional support for the dollar. Goldman Sachs classifies this press conference as a pivotal node of "different results paths under the same interest rate decisions," with various asset classes gearing up for corresponding event hedging.

Previously, Trump appointed Warsh to take the helm of the Federal Reserve in anticipation of rate cuts, but the committee Warsh has taken over has quietly turned hawkish at a rapid pace. With inflation high and employment strong, several officials have publicly stated that rate hikes should remain an option. His debut will unfold amid contradictory data, divided expectations, and intentional policy ambiguity he wishes to retain.

Interest Rate Decision: Hold Steady, But That Doesn't Mean Nothing Happens

The meeting is expected to maintain the interest rate range of 3.50% to 3.75% unchanged, which is almost a consensus in the market.

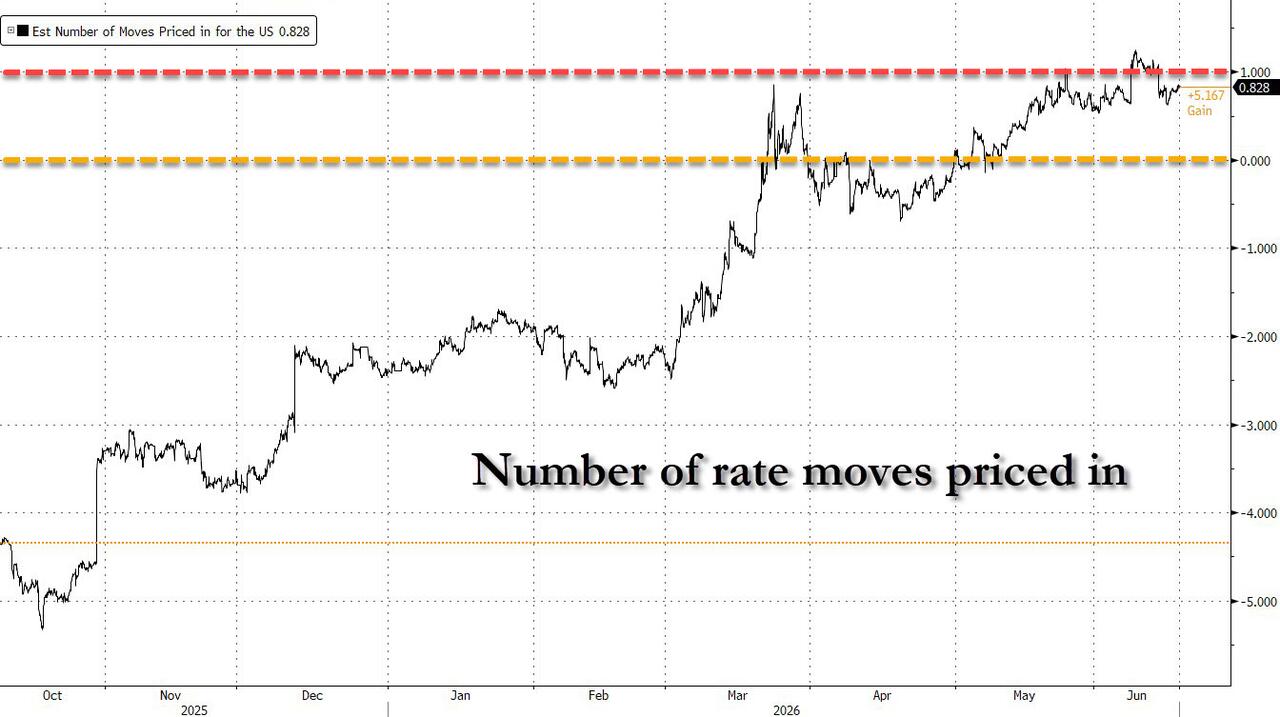

According to a Reuters survey of 102 economists, 72 respondents expect the interest rate to remain until the end of 2026. In the money market, due to the US-Iran conflict driving up oil prices, the market initially priced in a rate hike this year; as negotiations on the US-Iran agreement progress and oil prices fall sharply from their highs, rate hike expectations have narrowed, with current pricing estimating about 18 basis points of cumulative tightening before the end of the year, implying a roughly 72% probability of one 25 basis point rate hike.

The voting results are expected to pass unanimously. Bank of America Securities believes that hawkish committee members should be satisfied with the removal of the accommodative bias, and the only dissenting vote supporting a rate cut, from former board member Stephen Miran, has left, with Warsh taking over. Although Warsh is overall dovish, Bank of America Securities clearly states that he will not advocate for a rate cut at the first meeting.

Statement Language: Accommodative Bias Retires, Policy Balance Returns to Neutral

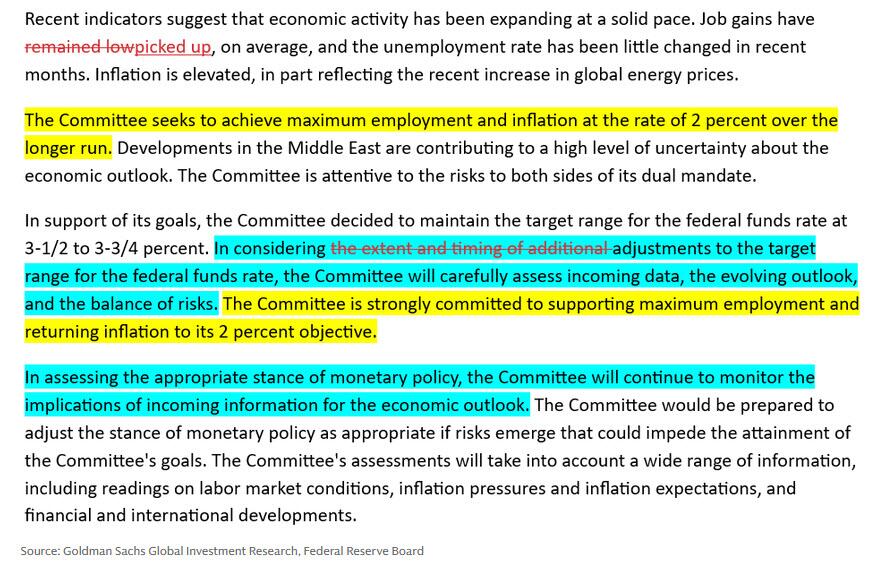

The adjustment of the statement language is the most certain change in this meeting and the most direct signal of the committee's attitude shift. The current wording, "when considering the magnitude and timing of potential further adjustments to the federal funds rate target range…," has long been interpreted as implying that the next step is more likely to be a rate cut.

At the April meeting, voting members Kashkari, Hammack, and Logan had already expressed objections to removing the accommodative bias. Following that, the statement from board member Christopher Waller became a key turning point. This official, who had previously been seen as a leading dovish figure in the committee, publicly stated in May: "Based on recent data, I support removing the accommodative bias to clarify that a rate cut is not more likely than a rate hike." Goldman Sachs believes Waller's statement represents a collective shift of the dovish camp.

Regarding the specific way of modifying the language, different institutions have varying expectations.

Bank of America Merrill Lynch expects the committee to possibly remove the word "additional" or further eliminate "extent and timing," replacing it with a more neutral "any adjustments"; Warsh may even push for the entire forward guidance section to be removed, which aligns with his long-standing criticism of forward guidance. Goldman Sachs also anticipates the removal of relevant expressions and points out that there is room for further shortening and simplifying the statement, as some paragraphs contain overlapping content.

The description of the labor market is expected to be upgraded in sync. Bank of America Merrill Lynch predicts that the current wording "job growth remains sluggish" will be modified to reflect several months of strong non-farm payroll reports, possibly revised to "job growth has rebounded, and the unemployment rate has remained stable in recent months."

Dot Plot: Significant Upward Revision in Inflation, Initial Rate Hike Expectations Emerge

This updated SEP is expected to show the clearest hawkish turn in this monetary policy cycle.

In terms of macro forecasts, Goldman Sachs expects the median PCE inflation for 2026 to be significantly revised up from 2.7% in March to about 3.9%, with core PCE revised from 2.7% to about 3.3%, mainly reflecting the combined impact of energy shocks caused by the Iran conflict and rising AI-related memory prices. GDP growth forecasts are expected to be downgraded from 2.4% to about 2.2%, and unemployment rate projections are slightly trimmed to 4.3%.

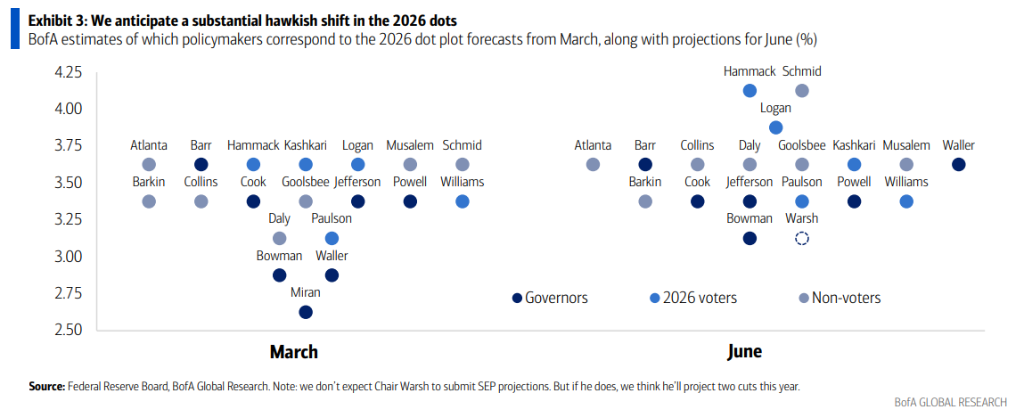

Regarding the interest rate dot plot, Goldman Sachs predicts the median interest rate for 2026 will remain at 3.625%, but about 4 to 5 points will cluster around 3.875%, implying that a few officials have included rate hikes in this year’s baseline forecasts. Bank of America Securities notes that its baseline scenario involves predictions of a rate hike from Hammack, Logan, and Schmid, with potential follow-up possibilities from Kashkari, Musalem, and others. Goldman Sachs strategist Rich Chambers states, "The year-end core PCE forecast is around 3.4%, and market pricing will remain near 3.875%, even if a peace agreement is reached, the rate hike premium will continue."

A key variable is whether Warsh himself participates in the SEP. Bank of America Securities and Deutsche Bank both expect him not to submit forecasts, partly due to his short tenure and fundamentally because of his systemic doubts about the nature of forward guidance tools. If Warsh is absent from the dot plot, it will implicitly shift the median towards hawkish, as his potential low rate forecast points will disappear from the calculations.

Goldman Sachs's baseline forecast indicates the Federal Reserve's last two rate cuts will occur in June and December 2027. However, Goldman Sachs also notes that "the flat path of keeping rates unchanged" has become an alternative option close to the baseline scenario, and the overall probability-weighted interest rate forecast remains more dovish than market pricing, mainly reflecting Goldman Sachs's low probability judgment for a rate hike scenario.

Press Conference: Warsh’s Policy Style to Debut

Warsh's first post-meeting press conference is the core market risk point of this meeting. How he balances the hawkish committee with his personal dovish tendencies will provide the market with firsthand material to assess his policy framework.

From a public stance, Warsh has repeatedly emphasized his opposition to excessive forward guidance during his Senate confirmation hearings, advocating for a reduction in the balance sheet and a return to interest rate-centric policy tools. He tends to view the Dallas Fed mean (currently about 2.35%) as a reference indicator for inflation, believing it better reflects underlying inflation pressures than core PCE, and has questioned the accuracy of the current inflation measurement system. He has also appointed conservative policy analysts Paul Winfree and Daniel Hall as advisors.

Bank of America Securities' baseline expectation is that Warsh will send gentle dovish signals at the press conference: characterizing the Iran conflict as a one-time energy shock that will not materially change the inflation fundamentals; emphasizing the disinflation potential of AI-driven productivity gains; reaffirming that monetary policy should remain forward-looking and not be swayed by monthly fluctuations in energy prices. However, Bank of America Securities also clearly states that recent data is insufficient to support advocating for a rate cut soon, and Warsh will emphasize patience, reserving room for easing later this year.

Goldman Sachs's trading desk overall expectation is that Warsh will acknowledge inflation is above target and the labor market is stabilizing, but will not provide a clear direction for future tightening paths, instead expressing a "neutral stance, ready to respond bi-directionally"—this statement will help him unify differing opinions within the committee, avoiding unnecessary market volatility at the first meeting.

Bank of America Securities also points out that Warsh may announce that post-meeting press conferences will change from after each meeting to quarterly; this change itself will constitute an important signal for communication mechanism reform. Goldman Sachs indicates it does not expect Warsh to touch on topics such as reducing the FOMC size, balance sheet reduction, or officially canceling forward guidance at this meeting.

Economic Background: The Coexistence of Inflation Stickiness and Employment Resilience

Before this meeting, economic data presents a pattern of "strong employment, sticky inflation," setting the tone for the committee's policy discussions.

In terms of employment, the May non-farm payroll report recorded a third consecutive month of strong growth, with a three-month average of about 188,000. Goldman Sachs expects that even with economic growth below potential levels and oil prices forming a certain drag on consumption, the unemployment rate will only rise slightly to 4.4%, and the overall labor market remains on a solid track.

Regarding inflation, energy shocks have driven up overall inflation, and Goldman Sachs expects PCE inflation for the entire year to exceed 4%, with core PCE over 3%. As the US-Iran agreement progresses and oil prices retreat, some economists believe May could be the peak for overall inflation, provided that navigation through the Strait of Hormuz is smoothly restored. Goldman Sachs believes that the combined effects of tariffs, energy prices, and rising AI-related memory prices on core PCE have passed their most extreme phase, and month-on-month increases are expected to gradually decrease; however, inflation is likely to remain above the Federal Reserve's 2% target for the foreseeable future.

Goldman Sachs points out that good labor market data allows the committee to focus on whether the inflation situation has worsened to the extent that rate hikes are necessary. The anchoring situation of core inflation expectation indexes and the breadth of high inflation data will be key dimensions for the committee's future policy judgments.

Market Impact: Differentiated Responses from Rates, Forex, and Stocks

Each asset class has formed its own response framework to this FOMC meeting.

In terms of the interest rate market, Bank of America Securities believes that Warsh's neutral to dovish statements should be interpreted as hawkish for data-sensitive positions, suggesting investors go long on 2-year US Treasury yields (currently around 4.07%, target 4.25%) and maintain flattening trades from 2 to 10 years. Goldman Sachs strategist Josh Schiffrin states that the space for significantly lower front-end rates is limited and that the market's expectations can only shift from rate hikes to cuts upon clear weakening in the labor market.

In the forex market, Bank of America Securities notes that the hawkish adjustments in the statement and SEP have been largely digested by the market, with the greatest upside risk for the dollar arising from a more hawkish than expected press conference from Warsh; if he downplays recent inflation citing the US-Iran agreement, the dollar may face short-term downward pressure. Goldman Sachs forex options strategist Harriet Bull points out that the current conference gap for G10 currency options pricing is about 45 to 55 basis points, which is in a higher range compared to the past year, yet as risk sentiment improves, the underlying volatility has somewhat decreased, making it attractive to hold long options volatility in the pre- and post-conference period from a risk-reward perspective.

In the stock market, Goldman Sachs derivatives strategist Cindy Lu points out that there are two-way risks associated with this event: if Warsh's stance is dovish or neutral, it may continue the recent stock market rebound; if he clearly adopts a hawkish position, it would pose a major threat to risk asset positions. Given that the VIX expiration overlaps with the front-end implied volatility being at recent lows, holding gamma longs around the event has relatively prominent cost-effectiveness.

In the gold market, Goldman Sachs data shows that CTA, ETF, and futures markets have all turned net short on gold, with GLD call skew falling to a ten-year low and put skew rising to a historical high. Goldman Sachs believes that if the Federal Reserve releases neutral or dovish signals and the Iran agreement proceeds smoothly, there may be a phase of rebound opportunity for gold after the shorts are cleared, suggesting positioning for upside risks through risk reversal strategies.

Iran Agreement: Warsh's "Buffer" and Greatest Tail Risk

The easing of US-Iran tensions is the most critical macro background variable for this meeting.

During the peak of the conflict, soaring energy prices pushed the market to fully price in a rate hike this year; as the framework of negotiations takes shape, Brent crude has significantly fallen from its peak to around $82—its lowest in over three months. Currently, the market's pricing for a rate hike this year has narrowed to about 18 basis points, with the formal signing of the agreement expected to be completed this Friday.

Goldman Sachs points out that historically, the Federal Reserve's monetary policy response to oil price shocks has generally been restrained. The correlation between high oil prices and hawkish rhetoric is low, and current wage inflation remains moderate, with no signs of an overheating labor market, fundamentally undermining the basis for aggressive rate hikes. Goldman Sachs predicts that the extreme inflationary effects of oil prices and AI-related memory prices on monthly inflation have largely passed and will gradually fade over the remainder of the year.

Goldman Sachs's global emerging markets and G10 spot forex trading head Alan Stewart points out that this provides Warsh with ample grounds to characterize the recent inflation shock as a temporary supply-side event, thereby providing both political and logical support for a "wait-and-see" stance. However, he also warns that if the agreement process experiences setbacks or if the Strait of Hormuz's resumption of navigation fails to meet expectations, "the previously cooled rate hike expectations may rebound quickly."

Under Goldman Sachs's baseline forecast, the Federal Reserve will keep rates unchanged throughout 2026, with the final two rate cuts delayed until June and December 2027. Goldman Sachs's probability-weighted Federal Reserve path remains significantly more dovish than current market pricing, primarily due to its skepticism regarding rate hike scenarios. Goldman Sachs's report bluntly states, "Trump appointed Warsh for rate cuts, not hikes, and Warsh himself is aware of this." This does not mean he will act rashly at the first meeting, but it reflects a cautious attitude towards rate hikes as well. The most likely outcome of Warsh's debut is a "no bomb"—but a slip in wording could ignite a fuse at any moment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。