Author: Chloe, ChainCatcher

On June 12, SpaceX listed at $135 per share, raising approximately $75 billion, with a valuation approaching $1.75 trillion. However, for many retail investors, the memory of this day is not the excitement of the opening jump to $150, but a refund notice. Through the tokenized subscription packaged by xStocks, over $1 billion in orders were siphoned off on Bybit, Binance, and Bitget, ultimately resulting in full refunds as the underlying shares could not be obtained.

However, the market is also shaping a Plan B, which involves two paths for indirectly holding private assets like OpenAI, SpaceX, and Anthropic through regular brokerage accounts: treasury-type individual stocks and registered private equity funds. This article will examine the trade-offs and risks of each.

Plan A Failed Because: An Extra Layer of Intermediary Preventing Share Acquisition

The IPO of SpaceX faced enormous retail demand. Reports indicated that retail subscription intentions exceeded $100 billion, while SpaceX compressed its originally planned allocation of about 30% for retail investors to just over 20% due to strong demand. Ultimately, the stock was priced at $135 and opened at approximately $150, nearly 12% higher than the issue price. The gap between those who could secure shares at $135 and those forced to buy at $150 is glaring.

Cryptocurrency exchanges initially aimed to open this door via tokenized subscriptions. Bybit, Binance Wallet, and Bitget Wallet launched pre-IPO subscription events for SpaceX, marketing them as a way for overseas retail investors to subscribe at the issue price, receiving a 1:1 backed token upon listing. The activity alone on Binance Wallet attracted about $557 million from 27,689 wallet addresses. However, when the underwriters finalized the allocations, most of these orders were left unfulfilled. Bybit directly informed users that, due to xStocks' inability to deliver the underlying assets, no allocations were received, leading to full refunds. Binance and Bitget Wallet also synchronized cancellations and refunds, offering consolation rewards.

This failure was not due to a blockchain crash or issues with token redemption. CoinDesk quoted insiders indicating that xStocks and its partners accumulated over $1 billion in orders, but there was no direct relationship between these platforms and SpaceX's underwriting team; they could only vie for the underlying shares through this intermediary. With an extra layer of intermediaries, the chances of not securing shares increased. Even retail investors with traditional brokerages only received partial allocations, indicating a supply-demand imbalance rather than a failure of crypto technology. Tokenization can encapsulate a stock into a globally tradable token, but it cannot create a stock that simply wasn’t acquired.

The timing of this event was also crucial. SpaceX is merely the first in a series of mega IPOs, with expectations that OpenAI and Anthropic will also IPO soon, and all three are seen as the most noteworthy group of large listings in recent years. This means that the scenario where retail investors cannot secure SpaceX allocations is likely to repeat with OpenAI and Anthropic. For this reason, there is urgent demand for a channel that does not rely on instantaneous allocations at listing to get access to these companies.

Two Forms of Plan B

Dissecting the refund wave reveals a proof of demand behind it. The over $100 billion in retail orders, along with the series of tokenized and perpetual contract purchases before listing, indicate that retail investors are not seeking a specific product, but rather a path to access cutting-edge private assets. The problem with Plan A is very specific: it places all hopes on the moment of listing, whether it can successfully secure the allocation released by the underwriters. Once the allocations are insufficient, the entire structure becomes ineffective.

The common logic of Plan B is to move this timeframe forward. Rather than fighting with the world for the same batch of new shares at the moment of listing, it’s better to buy the vehicles that already hold these private equity shares. When the target you are buying has already secured the shares before the IPO, the smoothness of the allocation on listing day becomes irrelevant to you. The tools available in the market to achieve this are roughly divided into two paths:

The first path is putting private equity exposure into the balance sheet and trading it as a regular stock through a treasury-type company

The second path is packaging private equity into a registered fund and allowing retail investors to hold fund shares.

Both paths do not require accredited investor qualifications, do not require oneself to engage in SPVs, nor do they require participation in KYC private rounds.

The First Path: Incorporating Private AI into a Regular Stock

ORBS: Indirectly holding OpenAI, Worldcoin, ETH, and MrBeast's media company

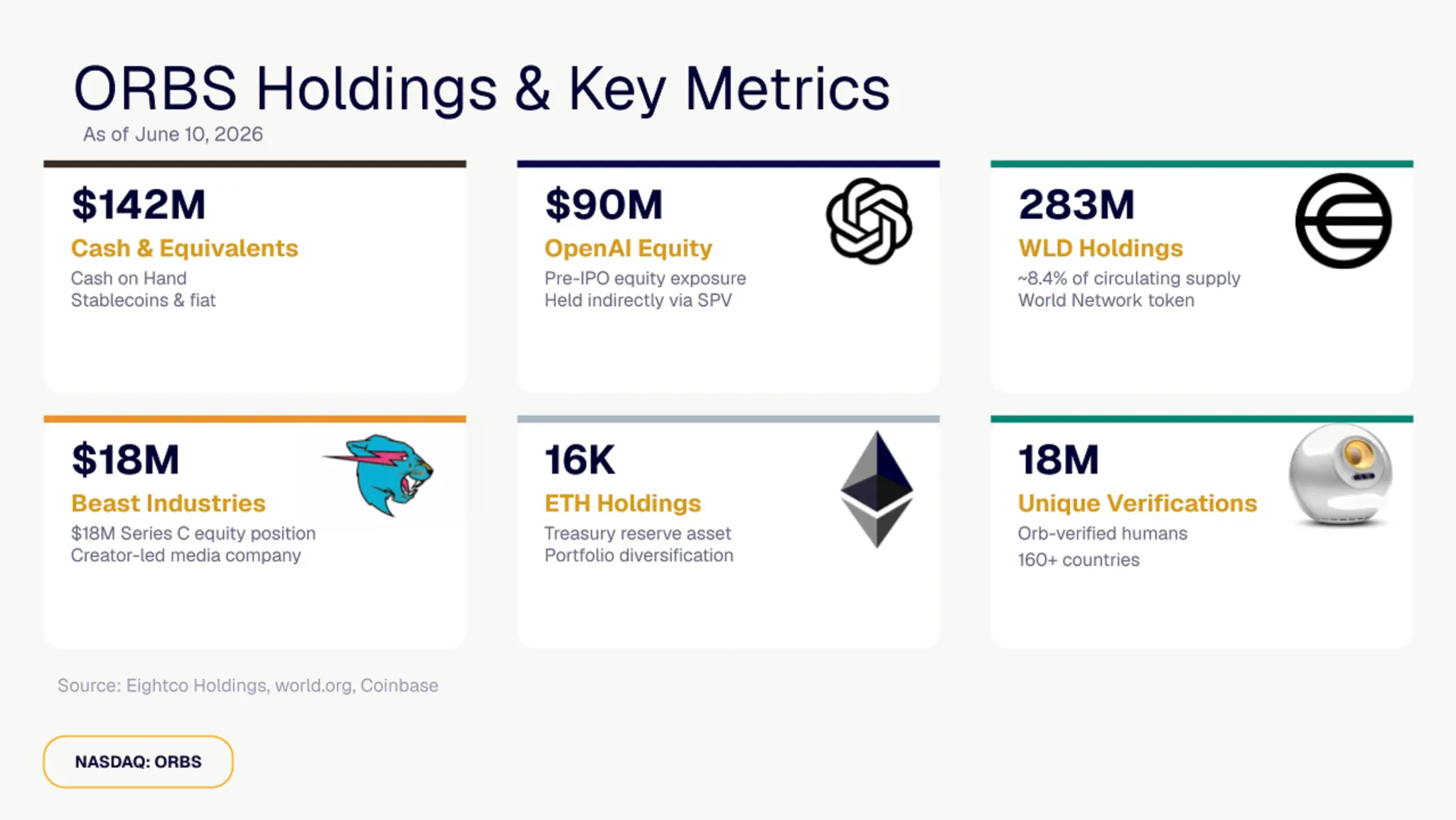

A direct example is Eightco Holding (NASDAQ: ORBS) listed on the NASDAQ. It operates its balance sheet as a bundle of emerging tech assets. According to the company’s announcement on June 11, as of June 10, its latest disclosed total holdings are approximately $406 million, including about $90 million in OpenAI shares held indirectly through SPVs, $18 million in Beast Industries (MrBeast's media company) shares, $1 million in Mythical Games, and 283,452,700 Worldcoin (WLD), 16,278 Ethereum, and about $142 million in cash and stablecoins.

Among these, the Worldcoin holdings account for approximately 8.4% of the total circulating supply, making it the largest disclosed institutional position currently available. Comparing this list with Plan A highlights the differences. A retail investor hoping to access OpenAI normally would need to be an accredited investor, find a way into a certain SPV, or invest in the private round through layers of KYC, which blocks the vast majority of people.

ORBS consolidates all these steps internally, allowing retail investors to simply purchase a stock symbol through a regular brokerage account and indirectly gain exposure to OpenAI, Worldcoin, ETH, and even MrBeast's portfolio. This is precisely what Plan A seeks to achieve but fails at: compliance, tradability, and genuinely having the underlying assets.

Cost and Risks of Individual Stocks?

Incorporating private equity exposure into a regular stock does not mean the risk disappears; it merely changes form. A significant portion of ORBS's holdings are in crypto assets, with the company's total holdings fluctuating within a month from about $337 million, $437 million to $406 million, primarily due to price changes in WLD and ETH.

The stock price itself has also been volatile, experiencing a drop of about 57% over the past six months and often oscillating between discounts and premiums to its net asset value. In other words, what you acquire is a leveraged combination of crypto and private equity valuations, which will be significantly more volatile than merely holding a mature tech stock.

ORBS is not an isolated case; it is part of a whole category of “treasury-type” targets. The market also has cross-border funds like XOVR, which packages SpaceX through zero-cost SPVs into an ETF shell, as well as numerous individual stocks and ETFs focusing on space and private equity exposure. However, the purity of the underlying assets, fee structures, and premium/discount conditions vary for each, and one cannot overlook risks just because they all carry the same star name.

The Second Path: Incorporating Private AI into Registered Funds

If treasury-type individual stocks are a way to stuff private equity exposure into a single company, then the second path is turning it into a regulated fund, allowing retail investors to hold fund shares. There are several funds aimed specifically at packaging “pre-IPO AI” investment options.

Destiny Tech100 (DXYZ): Closed-end fund, SpaceX is the largest holding

The closed-end fund Destiny Tech100 (NYSE: DXYZ), listed on the New York Stock Exchange, has consistently had SpaceX as its largest holding, accounting for about 16.2% of the portfolio, along with holdings in xAI, OpenAI, Anthropic, Databricks, Shield AI, and other private companies. Currently, it holds about 27 companies, with a goal of expanding to 100. As it continues adding to positions like Anthropic, more recent disclosures show the weights have shifted, with Anthropic's economic exposure rising to 18.1%, SpaceX around 14.5%, and OpenAI about 5.8%.

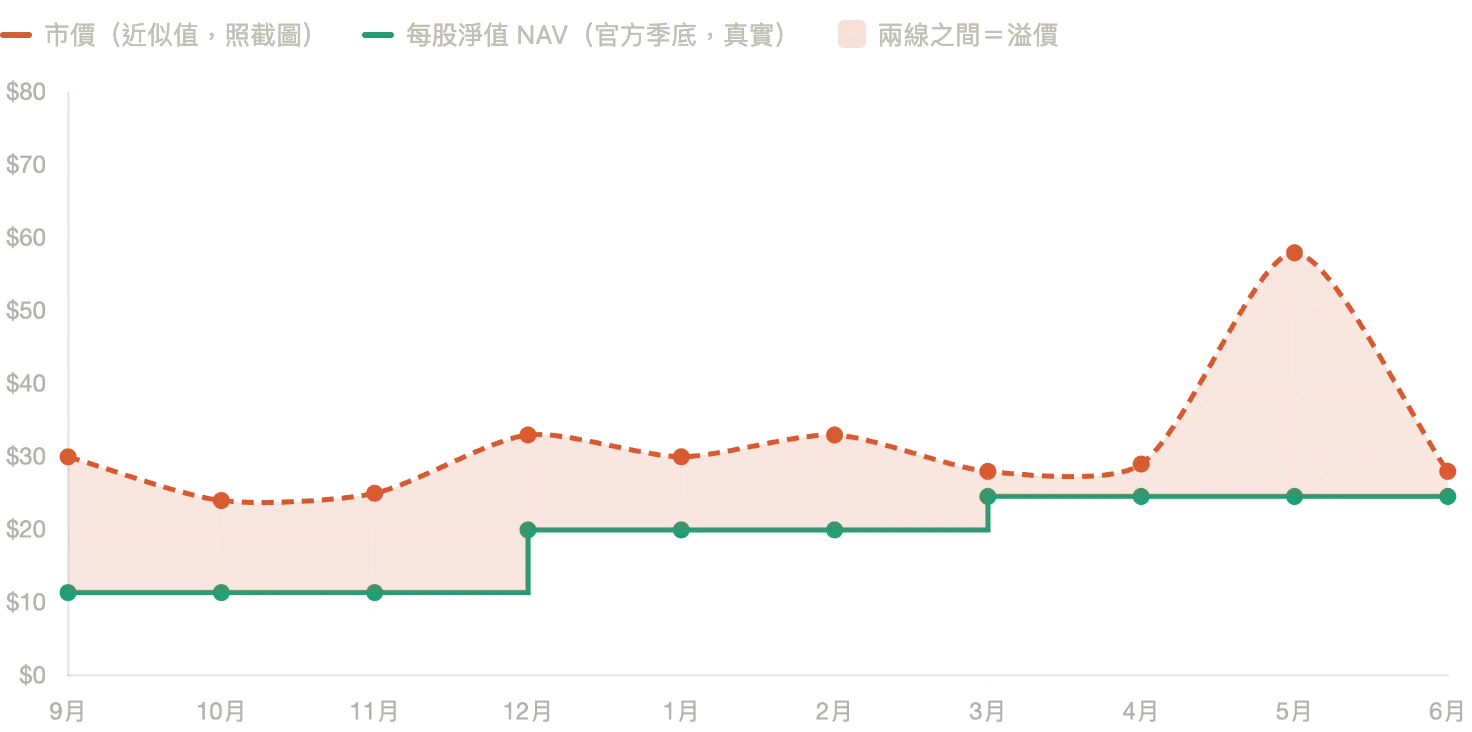

The key risk that DXYZ needs to watch is the premium/discount situation. The market price of closed-end funds can deviate from their net asset value over the long term, and DXYZ often skews towards a premium. The net value is updated only once a quarter, with the latest net value around $24.56 as of March 31, while the market price peaked at about $60 in late May, essentially buying at a price far above the underlying assets. The fund is also planning a market offering up to $1 billion, and such actions of continuously issuing new shares at high premiums can lead to dilution for existing shareholders. For retail investors, this means that even if you correctly identify the underlying company, you might incur losses due to purchasing at excessively high premiums.

This discrepancy is clearer when visualized rather than through numbers. The following two graphs show together: one depicts DXYZ’s actual market price movements on the NYSE, peaking at about $72 in May 2026, before subsequently dropping to about $28; the other overlays the official announced net value per share during the same period, which is a step-like line rising from approximately $19.97 at the end of 2025 to $24.56 on March 24, 2026. The gap between these lines represents the premium.

ARK Venture Fund and Fundrise Innovation Fund VCX: Interval Funds

ARK Venture Fund (ARKVX) and Fundrise Innovation Fund VCX are both SEC-registered closed-end interval funds, but with different structures compared to DXYZ.

ARKVX is actively managed by Cathie Wood's Ark Invest. It is an SEC-registered closed-end interval fund with a minimum investment threshold of $500, not requiring accredited investor qualifications. Retail investors can purchase it through platforms like SoFi, Titan, and Public or via channels like Schwab. SpaceX is the largest position, now accounting for about 14% of the overall portfolio, and the top five holdings also include OpenAI, Replit, Figure AI, and Anthropic, totaling over 40% and spanning more than 60 public and private companies.

VCX, on the other hand, is an interval fund with a higher concentration of AI, with Anthropic making up about 21% of its holdings, alongside significant investments in OpenAI, SpaceX, Databricks, Anduril, and Ramp.

The key characteristic of interval funds is that they do not trade continuously on the exchange. Their shares cannot be sold like stocks at any time; they can only be redeemed during periodic open buyback windows. This contrasts sharply with ORBS, DXYZ, XOVR, and similar securities that can be traded anytime during market hours: you exchange for a portfolio of diversified holdings closer to a venture capital mix with lower single-asset risk, at the cost of having liquidity locked up.

A Common Cost: You are Buying “Holders,” Not Shares

Examining these funds together reveals that they share a common set of trade-offs. The benefit is diversification: DXYZ and ARKVX are not betting on a single company but rather a basket of cutting-edge private assets, aligning with the idea of “instead of betting on which one is the next winner, why not buy into the entire trend.”

However, there are three layers of costs:

Fees: Active management and fund structures incur ongoing costs

Premium/Discount: Closed-end and interval structures can lead to market prices deviating from net value

Liquidity: Especially tight for interval funds

More fundamentally, these tools generally adopt a market-value assessment, with no such thing as “cheap entry before listing.” You benefit from the “post-listing upward space” rather than being able to secure a position at insider prices. What you acquire is never the shares of SpaceX or OpenAI themselves but rather a “holder of them.”

Fundamental Differences Between Plan A and Plan B: From Securing Allocations to Buying Holders

Comparing both plans reveals that the differences lie not in the interface or fees, but in your relationship with the underlying shares. The tokenized subscription of Plan A essentially involves competing for the same batch of new shares with the world at the moment of listing; your success depends on whether the underwriting team is willing to allocate shares to your intermediary; if you do not receive allocations, all you get is a refund.

In contrast, Plan B completely bypasses the allocation scramble because vehicles like ORBS, DXYZ, and ARKVX have already held shares or SPV exposure before the IPO; you are buying them rather than waiting in line for new shares.

The costs also shift. The cost of Plan A is the uncertainty of geographical barriers and falling short on allocations; the cost of Plan B includes premium, fund fees, liquidity, and the concentrated risk of single vehicles.

The question the former must answer is “Will I be able to secure it?”; the latter must address whether “am I willing to pay this premium and cost for something that is already held?” For retail investors who have long been locked out of private markets, what Plan B truly changes is transforming a binary, potentially falling short bet into a measurable, quantifiable option. Another dimension that changes is the time factor. Plan A is a one-time event; once the subscription window closes and allocations are distributed, it’s over. In contrast, Plan B offers a prolonged exposure that can be built up gradually before the IPO and can be continued or exited after the IPO, flattening a bet positioned at a single point into a stock curve that can be managed long-term.

When “securing an IPO allocation” Is No Longer the Only Entry

Last week's $1 billion refund was superficially a setback for tokenization, but in reality, it has illuminated a clearer dividing line for the entire market. Tokenization addresses “how to wrap a stock for circulation,” but it does not solve the more fundamental issue of “first needing to actually secure that stock.” Plan A bets on whether allocations can be squeezed at the moment of listing, and when demand outstrips supply by multiples, the inability to secure them is almost a certainty.

The value of Plan B lies in shifting the problem one notch forward. It no longer asks whether you can secure it on listing day, but whether you are willing to pay a premium and cost for something that is “already held.” Their forms differ, but they point to the same fact: in the race for cutting-edge assets, what has always been truly scarce is not technology, but the underlying shares themselves. Those who can secure shares before the IPO truly possess the channel that retail investors are desperately vying for.

When “owning a small piece of a private company” can be a stock, a fund, or a balance sheet, the next question worth pursuing might be: as these proxy tools continue to proliferate, will the premiums and discounts between them become a new way for the market to price these private giants?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。