Author: P Equity Research

Translated by: Deep Tides TechFlow

Deep Tides Introduction: P Equity Research presents a judgement that few people are willing to face: the three giants of memory (Samsung, SK Hynix, Micron) are pushing the AI capital expenditure cycle towards a break with price increases. The contract price of DRAM has approached a year-on-year increase of 700%, and memory is expected to account for 40% of capital expenditures of cloud vendors in 2027. The author predicts that the turning point will arrive in mid-2027, much earlier than the market's general expectation of 2030. A counter-consensus narrative on the memory cycle.

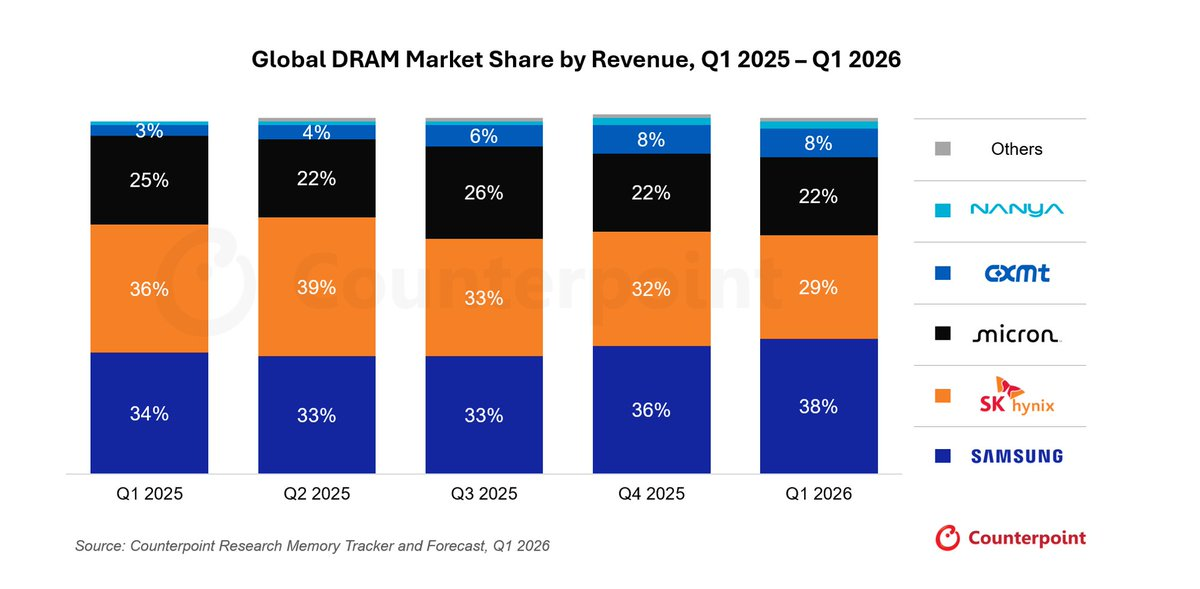

The three giants control 89% of the DRAM market

SK Hynix (000660.KS), Micron (MU), and Samsung ($005930.KS) dominate the DRAM market, holding a total share of 89%, with Samsung alone accounting for 38%. This is an oligopolistic alliance.

Chart Source: Counterpoint Research

This group of DRAM manufacturers has seized the situation of supply outpacing demand, raising prices quarter after quarter to frightening levels.

The logic is simple: to make advanced chips, you need DRAM.

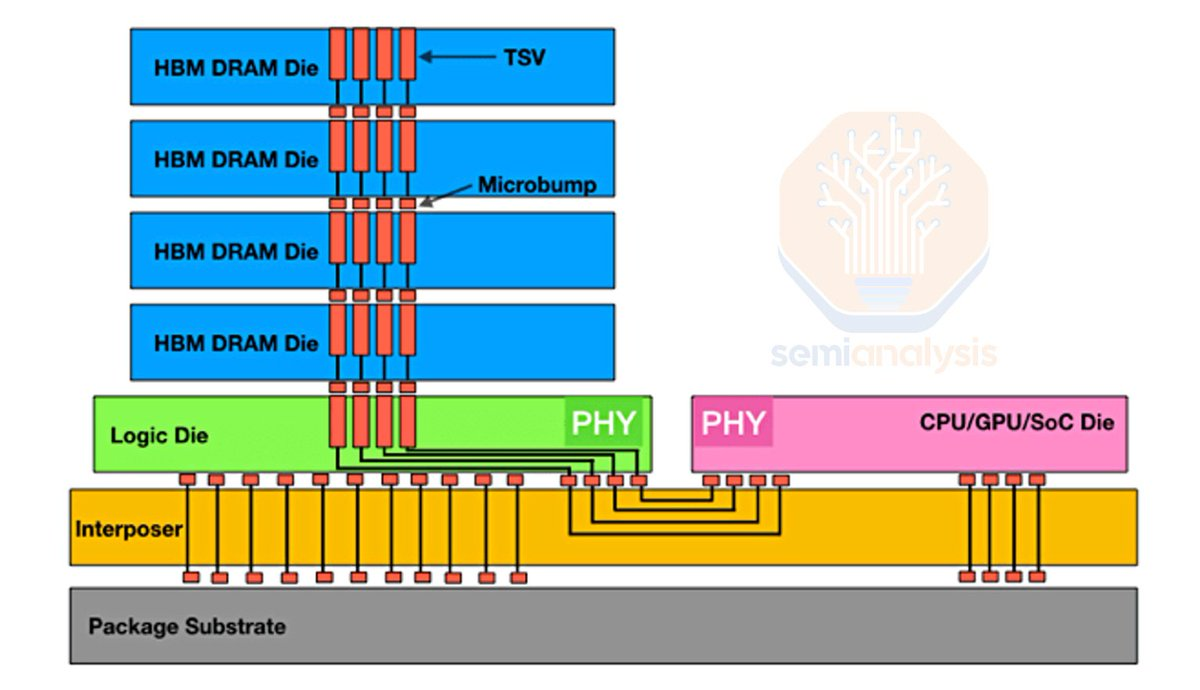

How DRAM turns into HBM

Let’s sidetrack for a moment to discuss how DRAM turns into HBM.

Layer the DRAM die, connecting them in the middle with TSV (Through-Silicon Via), to create HBM.

Chart Source: SemiAnalysis

In ordinary DRAM chips, data has to run to the edge of the silicon wafer to find wires. HBM is different; manufacturers create thousands of micron-sized holes in the middle of the silicon wafer using lasers and chemical etching, filling them with copper, which is TSV. They act like vertical shafts, passing through the entire chip.

Between each layer of DRAM, thousands of microbump solder balls are placed. After heating the entire stack, the solder balls melt, connecting the TSV of the upper and lower layers, forming a continuous, ultra-fast vertical data highway.

This is the entire process of turning DRAM into HBM.

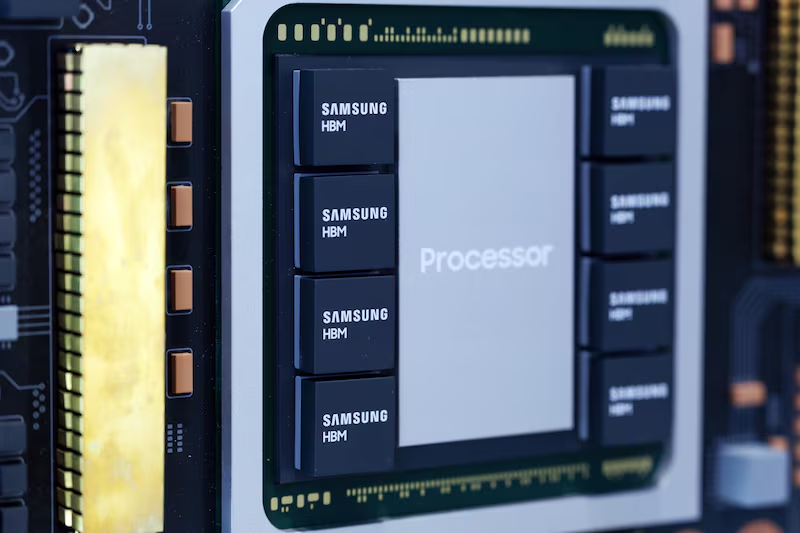

Chart Source: Bloomberg

Computing power requires more advanced chips, and the number of HBM layers is also increasing. HBM3 has 12 layers, while HBM4 aims for 16 layers. The more layers, the higher the bandwidth and the larger the capacity, which is the direction.

Returning to the matter of DRAM demand: the stronger the chip, the more memory is needed, and the memory market is becoming tighter.

My dissatisfaction with these manufacturers: 60% gross margin still not enough

These manufacturers could easily live like kings with a 60% gross margin, yet they are still pushing prices higher; I feel they are actively sacrificing the AI capital expenditure cycle for higher profits.

No one can clearly say when the gross margin will peak until now. This is also one of the reasons I write this piece.

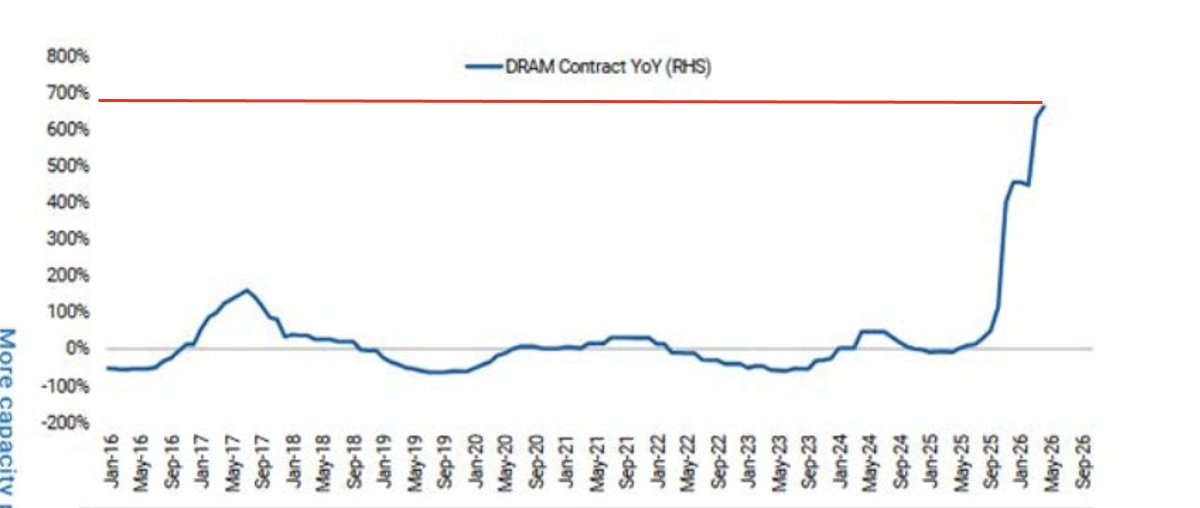

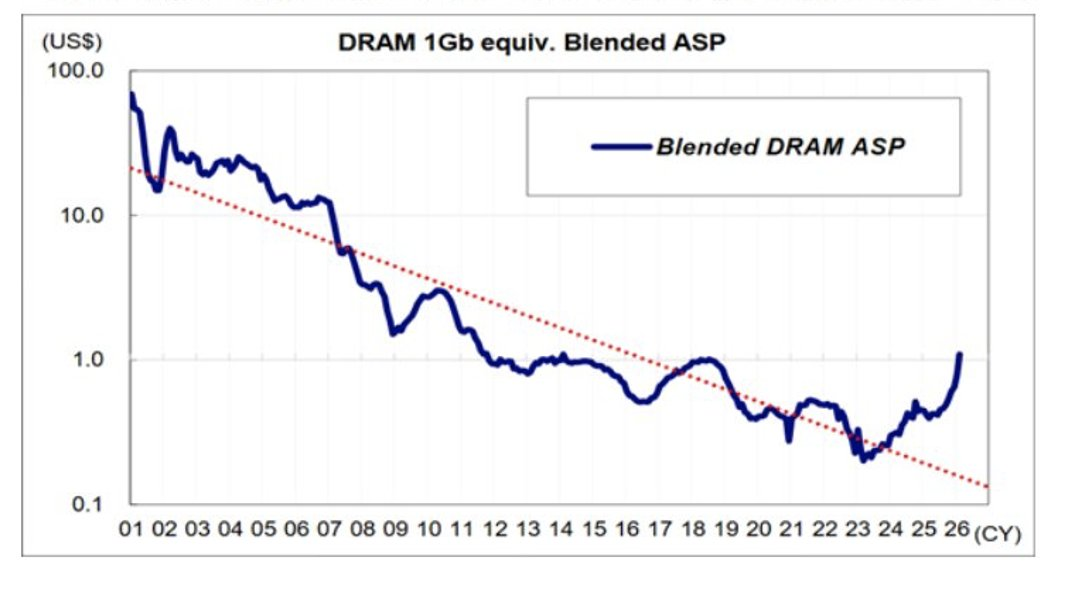

What can be confirmed is that in the remaining time of the calendar year 2026 (CY26), prices will continue to rise. The year-on-year DRAM contract price has approached 700%.

Chart Source: Morgan Stanley

Micron, Samsung, and SK Hynix have waited until 2024 to 2025 before starting plans for large-scale capacity expansion. These companies have experienced cycles of prosperity and collapse—after price increases, when demand retreats and supply exceeds, prices collapse.

Chart Source: Morgan Stanley

I do not blame them for delaying so long; there are two reasons:

Past expansions have brought down memory margins; enduring a bit longer in the expenditure cycle allows for greater visibility of demand.

The problem is, they currently hold the world’s pricing power, enough to choke the entire capital expenditure cycle's neck, and there aren't enough people paying attention to this.

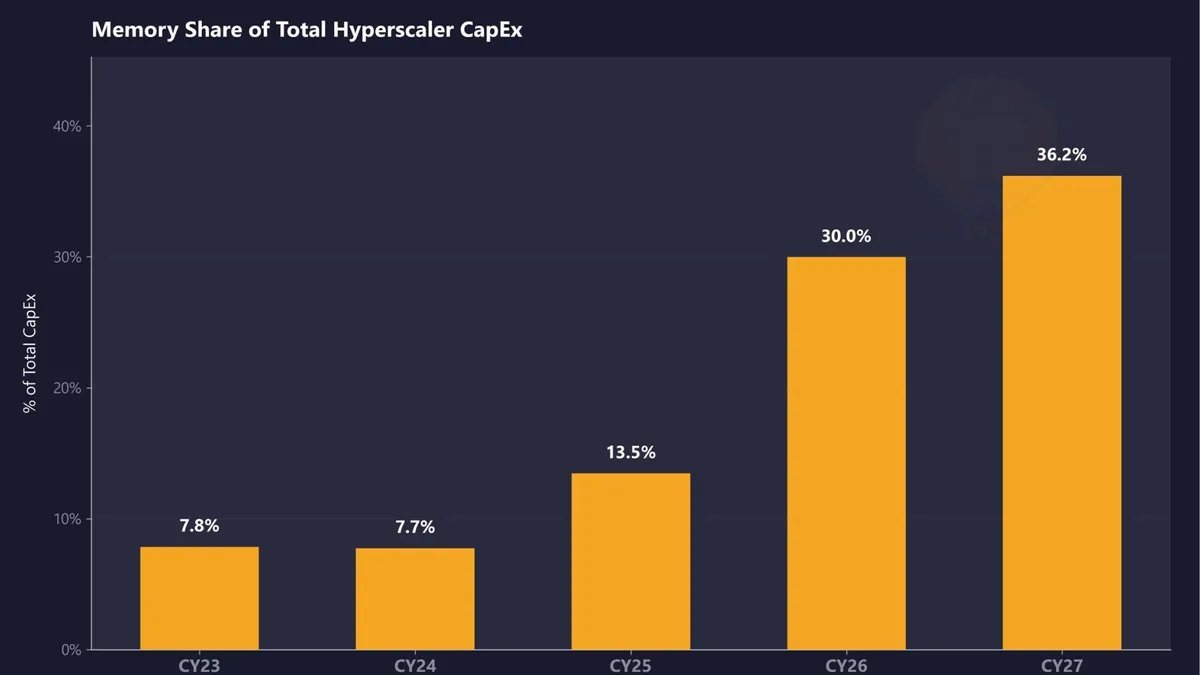

Memory will account for 30% of cloud vendors' capital expenditure in 2026; I bet 40% by 2027

Memory is expected to account for 30% of the capital expenditure of hyperscale cloud vendors in the calendar year 2026, rising to 36.2% in 2027.

Chart Source: SemiAnalysis

I believe even these estimates are conservative because memory prices have consistently defied predictions. I predict that memory's share will reach 40% in CY27.

For example, let’s take ALETHEIA CAPITAL:

“We now expect the average selling price (ASP) of server DRAM to jump by 30% in the third financial quarter of 2026 (previously expected to be 10% to 15%); it may increase another 10% to 15% in the fourth quarter (consistent with previous expectations). We expect the ASP of HBM to double year-on-year by 2027.”

Chart Source: ALETHEIA CAPITAL

They even expect that the content value of memory in AI hardware will rise from just over 40% in 2025 to above 70% in 2027, with some memory-intensive cabinets exceeding 90%.

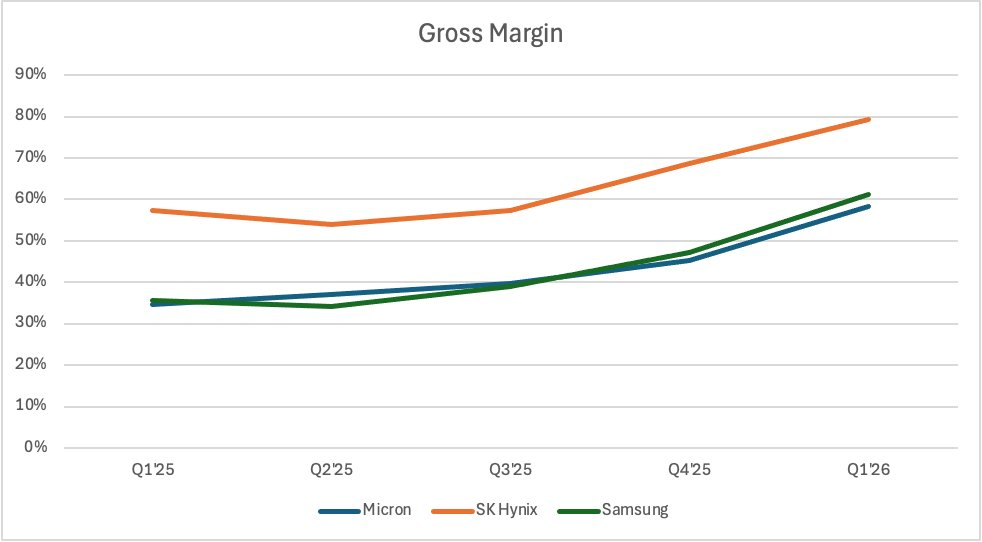

Chart Source: Company Reports, P Equity Research

Samsung and Micron's gross margins may reach over 70%, while SK Hynix could reach the mid-80s. This situation may last until 2027 and extend into 2028.

Micron CEO Sanjay Mehrotra has mentioned in an interview with Bloomberg that meaningful new capacity will not come online until 2028.

Video: https://x.com/MilkRoadAI/status/2066231053749006634/video/1

Have to wait until 2028?

Memory costs may not peak until 2028, while cloud vendors, already facing tight free cash flow (FCF), can only adjust spending to hedge against the rising memory costs.

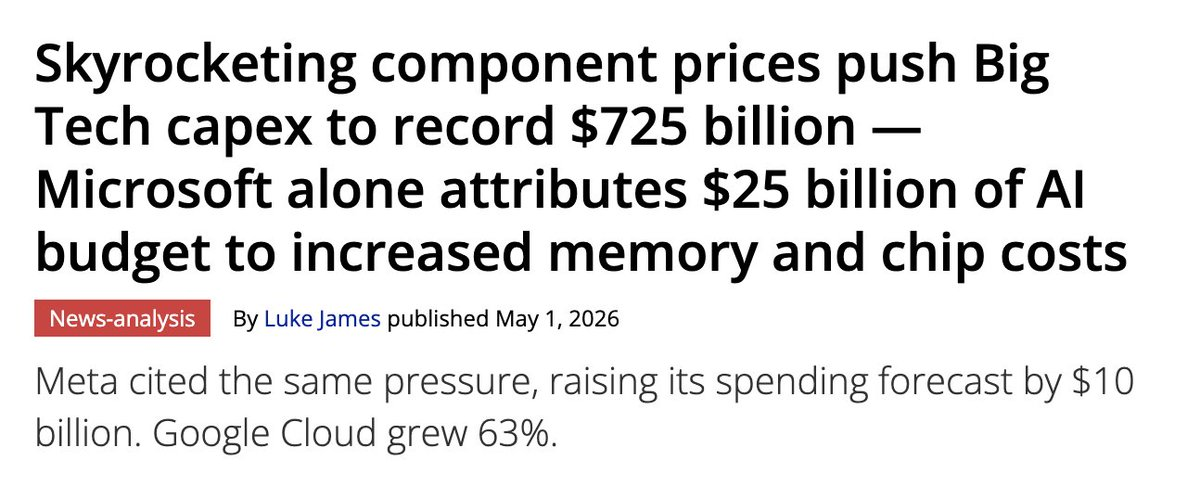

Microsoft spent an additional $25 billion on memory and chips

Chart Source: Tom's Hardware

Microsoft has raised its capital expenditure by $25 billion to cope with rising memory and chip prices. $25 billion.

Other cloud vendors have not provided specific figures directly linked to memory costs, but their wording is similar, or they indirectly acknowledge it:

Meta said, “This year, component prices are higher, especially memory”; Microsoft said, “Component prices are higher”; Amazon said, “Memory prices have surged due to limited supply and strong demand across the industry.”

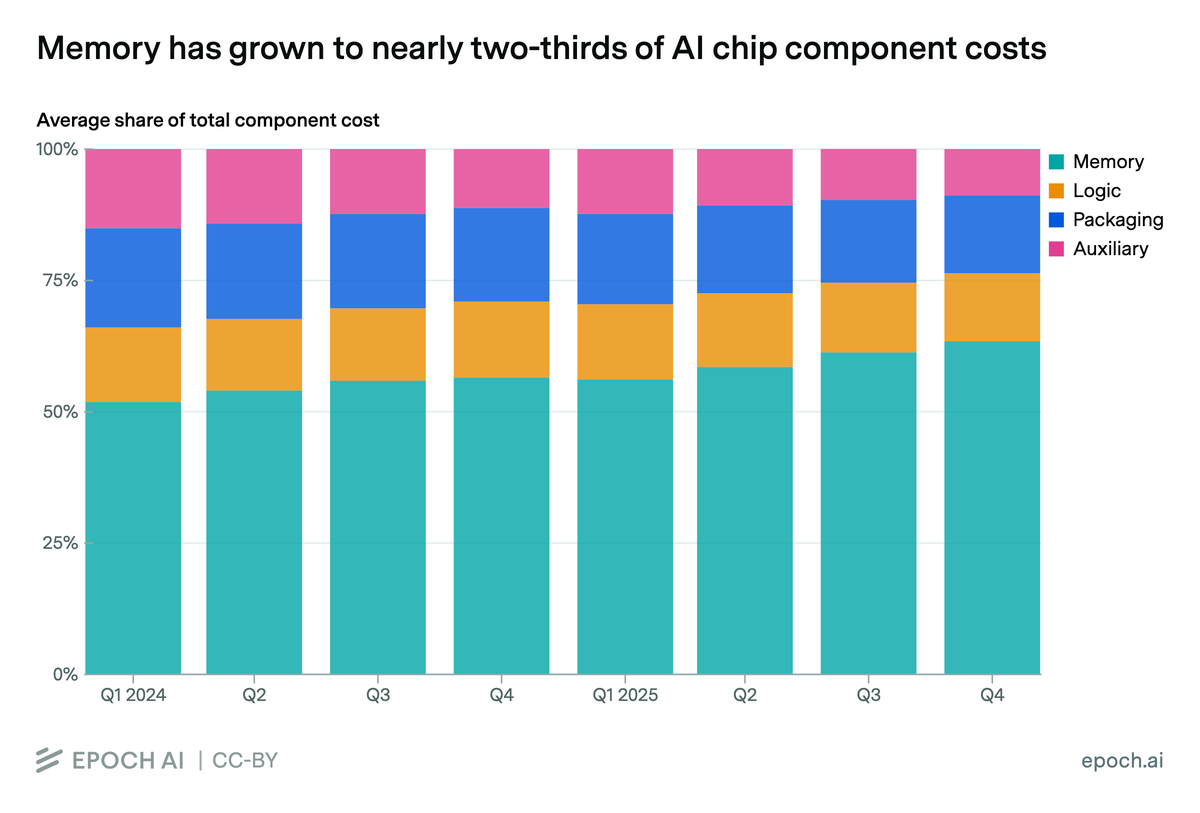

Chart Source: EPOCH AI

No matter who you ask, memory has become a cost threat for everyone. It accounted for 64% of the total component cost in the fourth quarter, and is likely to exceed 70% by the end of 2026.

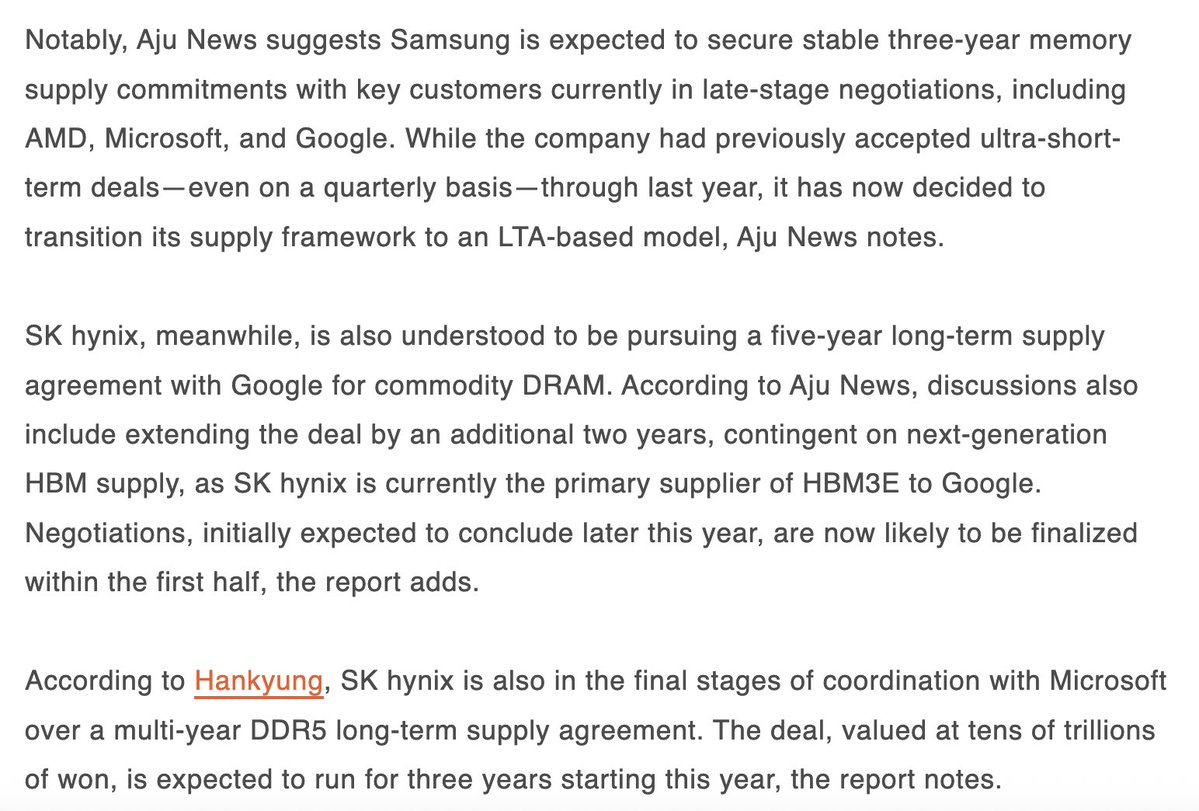

So, what can cloud vendors do? They can do nothing. Even long-term agreements (LTA) won't save them.

In plain terms, cloud vendors are facing skyrocketing memory costs because they have to buy both HBM and memory modules. The capacity consumption of HBM is three times that of ordinary server memory. Factories are frantically shifting equipment to make HBM, leading to a collapse in the supply of ordinary server memory, and prices are soaring as a result.

LTA also has hard limits on the quantity that can be purchased at a discounted price. The AI boom came too quickly, and cloud vendors almost instantly used up their contract quotas. Additional demand can only be purchased at current market prices.

Chart Source: TrendForce

Cloud vendors have no choice but to sign new LTAs with memory manufacturers. These contracts are not signed for a year but for 3 to 5 years, as chip manufacturers want to quickly lock in prices to hedge against the rapid rise of DRAM. To make matters worse, these LTAs lock in old memory that will not be massively adopted in the future. Transitioning from HBM3 to HBM4 will see prices rise again.

Cloud vendors remain in a passive position, with pricing power firmly held by this alliance.

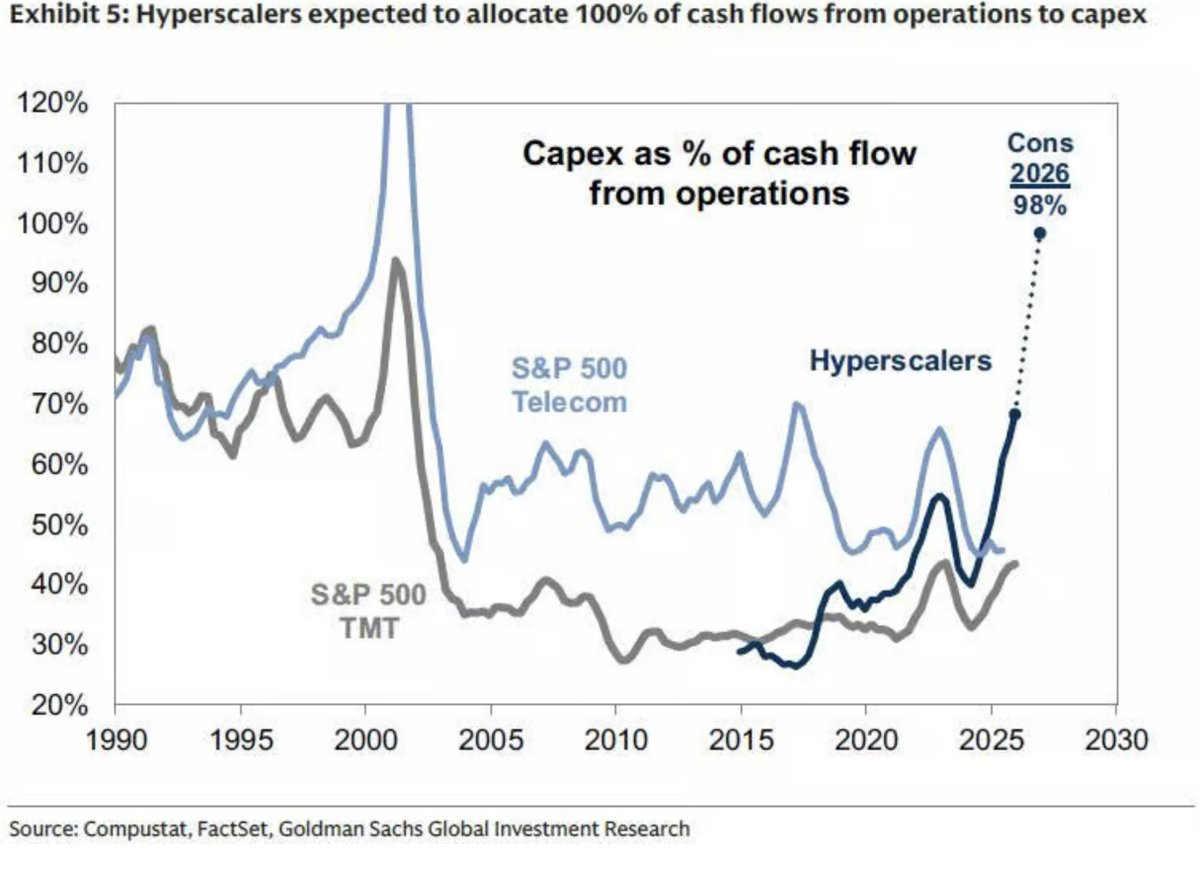

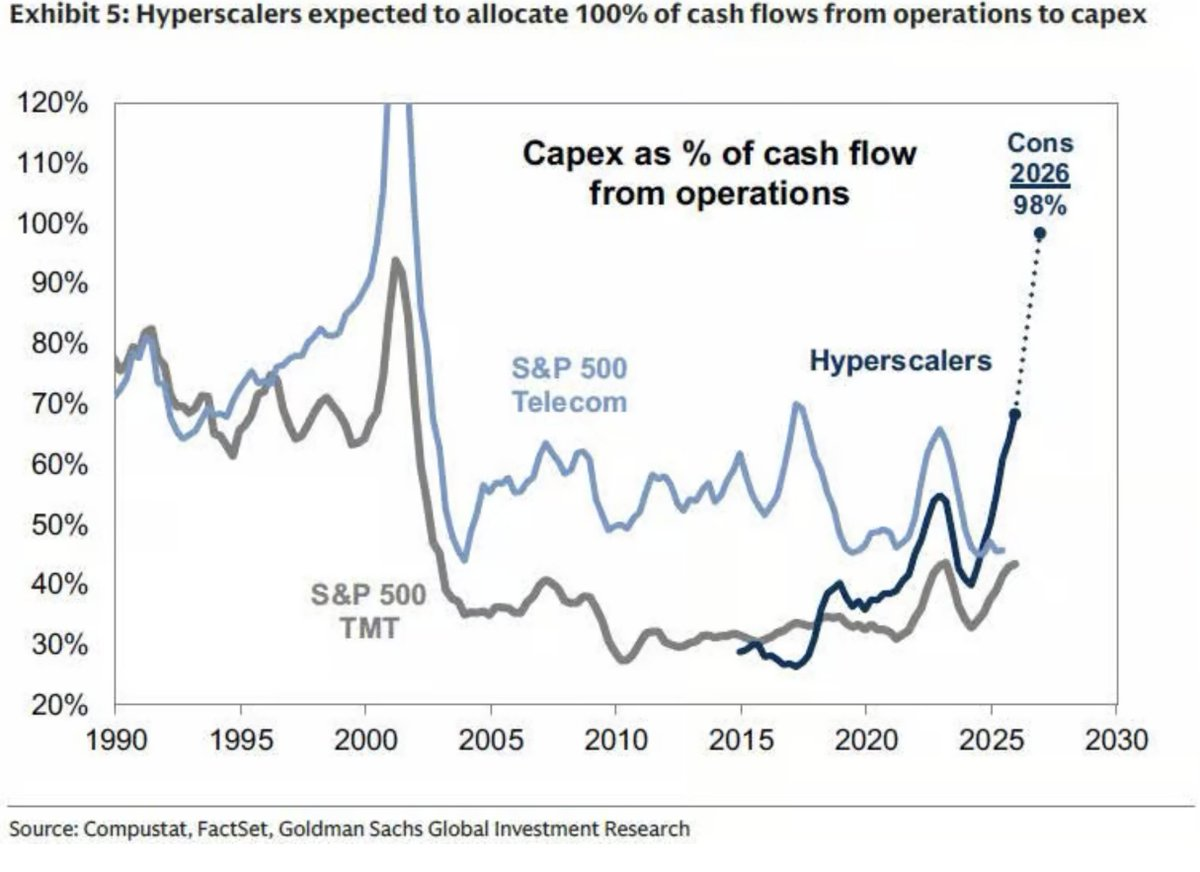

Free cash flow at a bottom: 98% of operating cash flow consumed by capital expenditure

Cloud vendors have no choice but to continuously issue equity and bonds. Google, Meta (hinting at possible issuance?) are doing so, and perhaps Amazon will soon follow suit.

Free cash flow is rapidly depleting, with cloud vendors pouring 98% of their operating cash flow into capital expenditure. This is the highest level since the internet bubble.

Chart Source: Goldman Sachs

Meanwhile, Morgan Stanley predicts that capital expenditure will remain strong in 2027, at approximately $1.1 trillion.

Chart Source: Morgan Stanley

Let’s calculate: about 40% of this money will go to memory, roughly $440 billion. This is nearly equivalent to the total capital expenditure for the entire year of 2025.

There are two points that make me uneasy:

One is that the equity and debt financing in the market is already sending negative signals to participants—cash is hitting a bottom, and the ratio of price-to-sales and free cash flow multiples are off the charts.

The second is that cost pressure may cause the growth rate of capital expenditure to slow down, or even to pause earlier than expected. According to my estimates, around mid-2027, earnings call reports will start to reveal signs of stopping.

I believe the second point will approach memory manufacturers by the end of 2026, much earlier than many expect.

From here on, the number one issue repeatedly emphasized in earnings calls will be component prices—especially memory—and how it squeezes spending budgets. I do not believe cloud vendors will ignore this point and recklessly continue to ramp up capital expenditure.

This is just my opinion.

Chip manufacturers are already looking for ways to save on memory

AMD, Nvidia, and Google are already heading towards memory optimization.

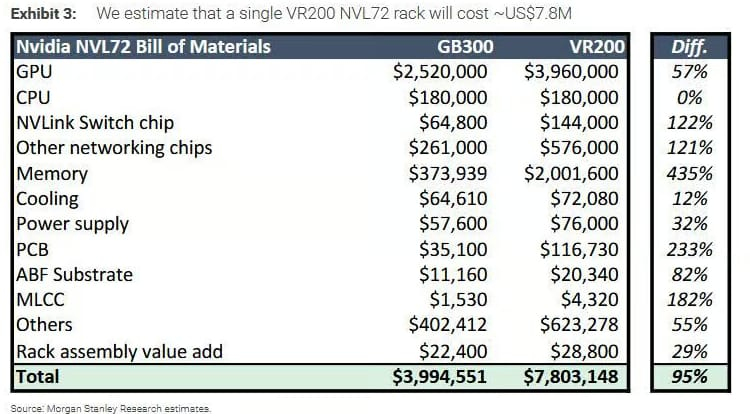

Nvidia’s next-generation Rubin NVL72 cabinet’s CPU-side SOCAMM DRAM may cut from about 55TB per cabinet to about 28TB, nearly halving it. This makes sense, as the bill of materials for the VR200 indicates that memory costs have risen by 435% compared to the GB300.

Chart Source: Morgan Stanley

SOCAMM is not HBM, but the cost pressure driving frugal thinking is the same principle—whether AMD uses MEXT for memory pooling (making flash memory act like DRAM) or directly reducing SOCAMM DRAM.

Chip manufacturers actually have fewer options: they are already paying for HBM, and then adding the cost of SOCAMM? Painful. They are squeezed from both ends.

Memory is still cyclical; the turning point is in mid-2027

Finally, let’s talk about the cyclicality of memory.

I do not agree with the notion that "memory is no longer cyclical."

Even if I am entirely wrong, if capital expenditure can be strong for ten years, you will still naturally encounter the cycle of boom and bust. Those who refute me must assume: memory demand grows year after year, and cloud vendor spending never enters a cycle—which is impossible.

Chart Source: SEMI

These manufacturers who are desperately expanding production are betting on continuous growth in capital expenditure (which seems unlikely judging by this momentum) and continued strong demand for memory (which relies on constant capital expenditure growth to support it).

My projection is that by 2027, DRAM pricing will start to peak:

SK Hynix will have a margin of about 80%; Micron will be around 78% to 80%; Samsung will be around 70% to 75%.

The price curve will flatten under continued tight capacity, roughly in February or March. Then, around mid-2027, you will start to sense a slowdown in capital expenditure growth or even the signal of a pause.

I believe that most memory stocks will begin to retract their gains starting from this position, as investors will price in the upcoming contraction in gross margins.

By 2028, more capacity will come online (supply will still be tight), but demand expectations will no longer be as strong, and margins will continue to decline to just over 60%. From 2028 to 2030, capacity will continue to be added, the supply tightness will ease, and there will be no substantial growth in capital expenditure. I predict that a real collapse will occur during this phase, with a large number of stock price gains starting to retract from late 2027.

Everyone believes memory will be strong until the end of 2030, but my prediction is that gross margins will start to contract from mid-2027, and many memory stocks will reverse their gains.

That said, if in 2027 cloud vendors claim that capital expenditure in 2028 will be significantly stronger, then my article would be in vain and I would look foolish. The truth will be decided by time, but I believe that memory is on this path moving forward.

Why I am not so optimistic

I am not as optimistic about memory as others, and there are a few reasons for this:

Memory manufacturers are too greedy for margins; I believe memory still has cyclicality, and the "no cycle theory" is betting all on capital expenditure never entering a cycle; chip manufacturers are finding ways to save on memory, which itself proves they are fed up with high costs; CFO's cash is nearly 100% depleted by capital expenditure, and memory will still account for 40% of costs in 2027. Continuing to issue bonds and raise shares is no longer sustainable.

The only good outcome would be a sudden influx of crazy supply dumping in the market, collapsing the memory prices of the three manufacturers. In that case, the same capital expenditure could yield more output.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。