Author: Tyler Durden (ZeroHedge pseudonym)

Translated: Source: ZeroHedge

Deep Tide Guide: SpaceX fell for three consecutive days, plunging 16.4% in a single day on Monday, erasing $600 billion in market value and dropping back to the opening price of $150. This article straightforwardly concludes that those who wanted to buy have already bought, and more critically, the selling pressure has not really arrived yet. This round of price increases only used 5% of the circulating market, and insiders can sell up to 44% of their shares by early September.

The opening was explosive. SpaceX went public on June 12 with an opening price of $150, far exceeding the issue price of $135. Within two days, aggressive traders began to crazily buy $380 call options expiring in two days, attempting to push the stock price to the sky and create a gamma squeeze (forcing option market makers to buy stocks to push prices higher).

@zerohedge tweeted: They are really going for it.

Canaccord described the "new round of optimism" accompanying SpaceX's IPO in a report earlier this morning:

"The SPCX market shows that the market has entered a new level of frenzy. Before this historic IPO, we thought AI optimism was already full, and sometimes even overblown, but the buying mainly came from rational (if euphoric) institutions—large, well-funded public companies and private equity investors. In our view, SPCX has opened a new chapter, significantly increasing retail participation and pushing the stock into the global top six by market value, increasing its market value by the equivalent of half META in just the first week. Its market value has already far surpassed its sister company TSLA, while its revenue is only about 20% of the latter. Don't be fooled by the company's name SpaceX; its income actually leans towards connectivity services—Starlink contributed $11.39 billion, while launch services brought in only $4.1 billion, and AI computing power is projected to be $3.2 billion by 2025."

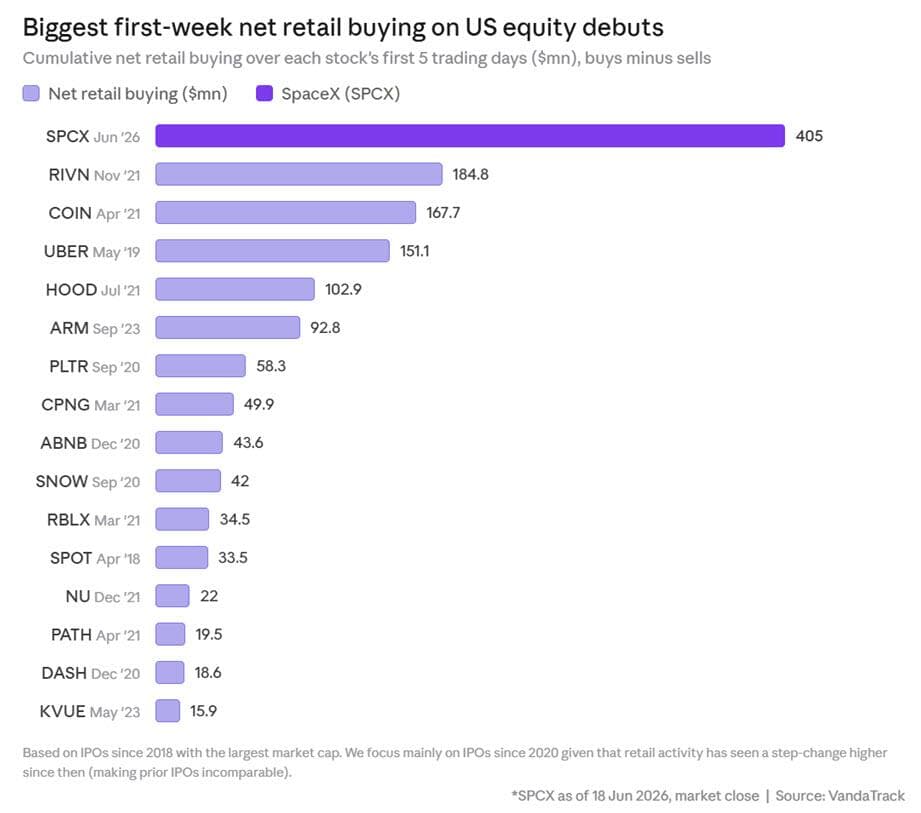

Vanda Track was even more exaggerated. In a review earlier on Monday, it wrote: "SpaceX's first week of trading set a record. Retail investors net bought $405 million of SPCX in the first five trading days, the strongest retail participation in an IPO in recent years. The buying in the first few trading days was extremely fierce, cooling down only later in the week. The funding characteristics increasingly resemble building long-term positions, rather than chasing a short-term meme stock."

Figure Caption: Retail Fund Flow for SPCX in the First Five Trading Days

Source: Vanda Track

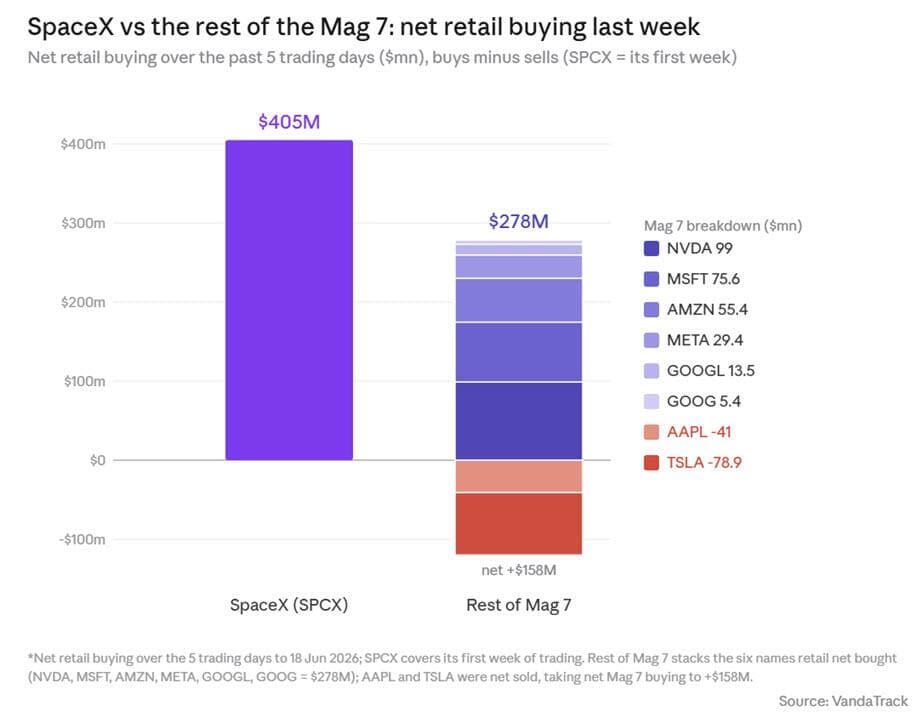

Looking in comparison, the scale of retail buying of SPCX is even more astonishing. Last week, the amount of SPCX bought by retail investors exceeded their total purchases of the other seven MAG stocks—NVDA, MSFT, AMZN, META, GOOGL, and GOOG combined only amounted to $278 million over those five days. The retail buying of SPCX also surpassed the cumulative retail buying of the SPY and QQQ ETFs during the same period ($352 million). A stock that just started trading last week is already competing for retail money with the largest stocks and ETFs in the market.

Figure Caption: SPCX Retail Buying vs. Retail Buying of MAG 7 Stocks

Source: Vanda Track

The old routine is once again enacted. While individual stocks soared, retail investors quickly flocked to various SpaceX leveraged products, showing similarly strong demand. In the first few trading days after the IPO, retail bought $65.8 million of Leverage Shares 2x Long SPCX Daily ETF—it's a substantial number, but still far below the typical levels during retail speculative frenzies. Even so, it has outpaced recent thematic new products: Roundhill's storage ETF (ticker DRAM) only attracted $5.6 million in the first four trading days, and DRAM retail buying accumulated more than what the SpaceX leveraged ETF had attracted, taking 22 trading days.

Figure Caption: Comparison of Retail Fund Flows for SPCX Leveraged ETF vs. Thematic ETFs

Source: Vanda Track

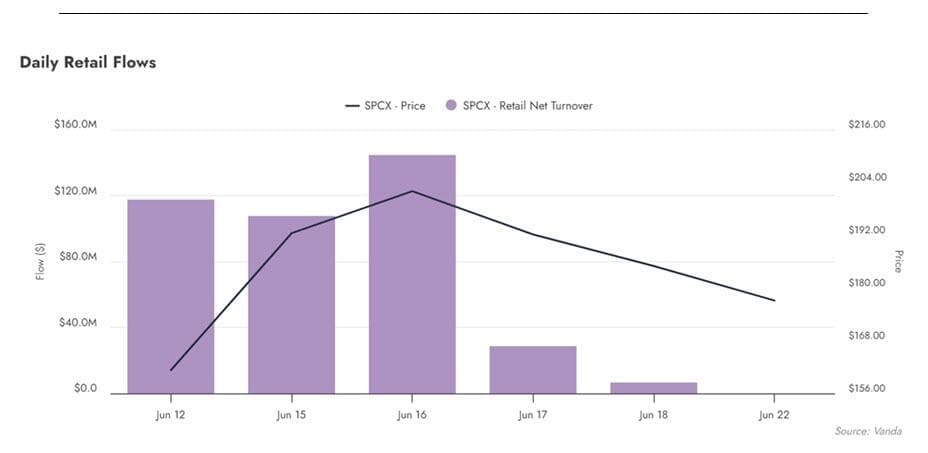

After bursting through the gate, the momentum quickly faded, and the fantasy of "sitting on a recyclable rocket all the way to a gamma squeeze into orbit" dissipated. June 16 was the peak, with SPCX touching a record high of $225 that day, briefly exceeding Microsoft's market value. After that, retail daily fund flows collapsed, and the retail turnover almost went to zero.

Figure Caption: SPCX Daily Retail Fund Flow—Dramatic Decline After the Peak on June 16

Source: Vanda Track

This brings us back to Canaccord’s statement. Based on SpaceX's early performance, the investment bank judged that "tech stocks can likely maintain momentum in the short term," but it also warned: "There is now an additional layer of dangerous vacuum under these stocks."

Sure enough, as the momentum faded and the market realized that trillions of shares would soon be unlocked, the stock price fell for three consecutive days and crashed directly on Monday. That day, while the bond market was still exuberant, SpaceX aimed to issue more than $20 billion in investment-grade bonds for the first time before the debt market window closed, to replace a much higher-interest bridge loan. SPCX plunged 16.4%, erasing a record $600 billion in market value in a single day. Including the 5% drop on Wednesday and the 3.5% drop on Thursday, this stock is now barely above the $150 opening price it had two weeks ago.

Figure Caption: SPCX Price Trend Since IPO—Falling from the $225 Peak to Around $150

Source: ZeroHedge

Worse still, after-hours SPCX briefly touched the opening price of $150. If it opens tomorrow below this price, then everyone who bought and held in the secondary market will be stuck.

Figure Caption: SPCX After-Hours Drop to Around the $150 Opening Price

Source: ZeroHedge

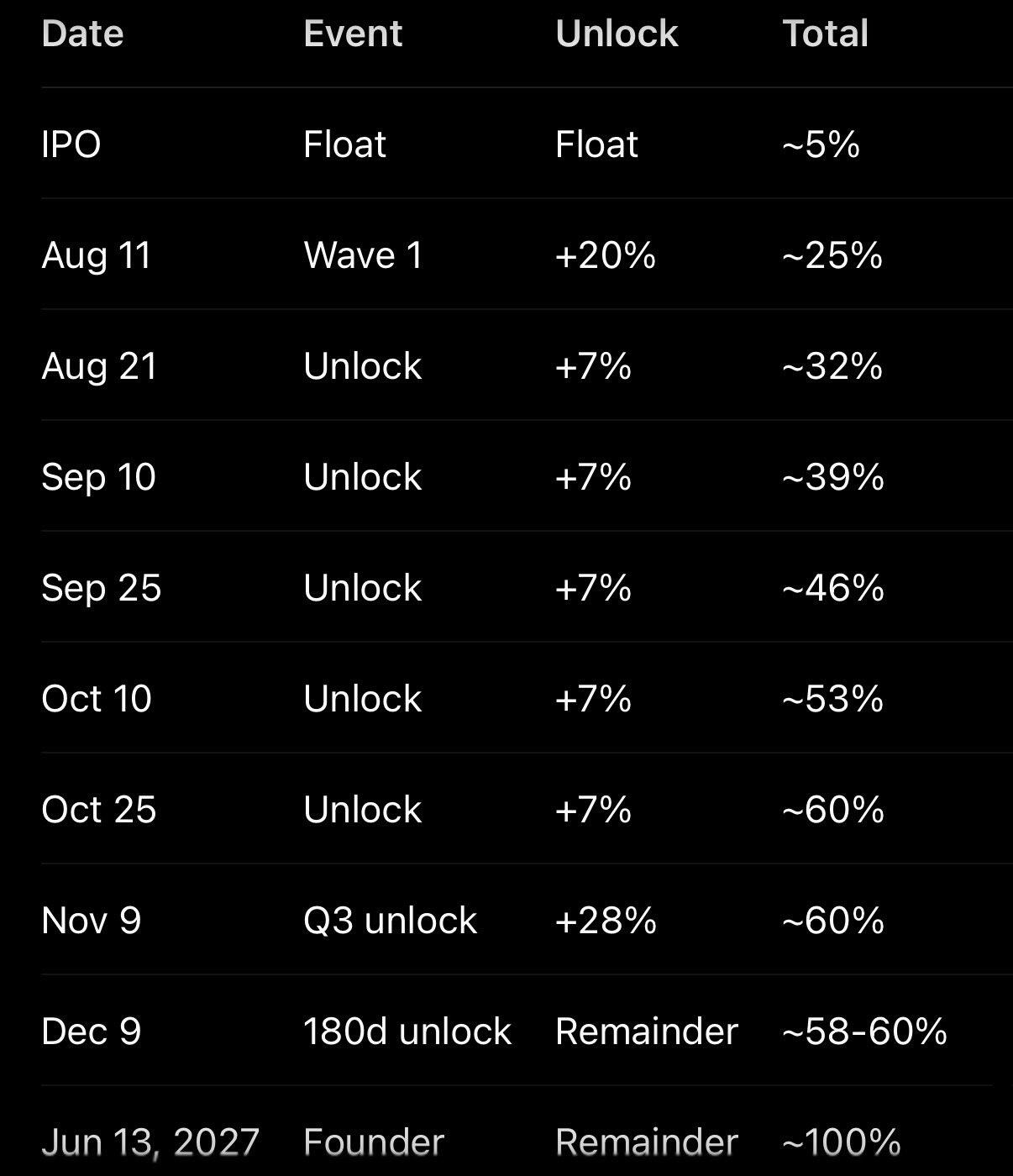

It is especially worth mentioning that this price increase and sell-off occurred with only 5% of the circulating stock available for trading—95% of the shares have not yet been unlocked. But that will change soon.

Figure Caption: SPCX Unlocking Structure—Currently Only 5% Circulating, 95% Locked

Source: ZeroHedge

22V Research strategist Jeff Jacobson said that after SpaceX reports its financials in early to mid-August, 20% of insider shares will be unlocked. Additionally, if the stock price exceeds the issue price by 30%, another 10% will be unlocked; there will be two instances of 7% unlocking around August 21 and September 10.

Figure Caption: SPCX Lock-Up Release Timeline

Source: 22V Research

Jacobson stated that insiders could sell up to 44% of SpaceX shares by early September, expanding the current circulating market by about 900%.

In other words, it will only become more difficult to lift the stock price going forward. Meanwhile, JonesTrading chief market strategist Michael O'Rourke said: "The sellers have regained control," adding, "The people who want to buy in this world have already bought it all."

Bloomberg noted in its analysis of today's decline that SpaceX's drop "has dragged down a large part of the market."

Whether this is true remains to be seen. But in this market—having been supported almost entirely by retail fervor and momentum chasing since the March low—once retail truly gets frightened, first SpaceX, then the storage bubble, and finally the semiconductor stocks that have reaped the AI trading dividends...

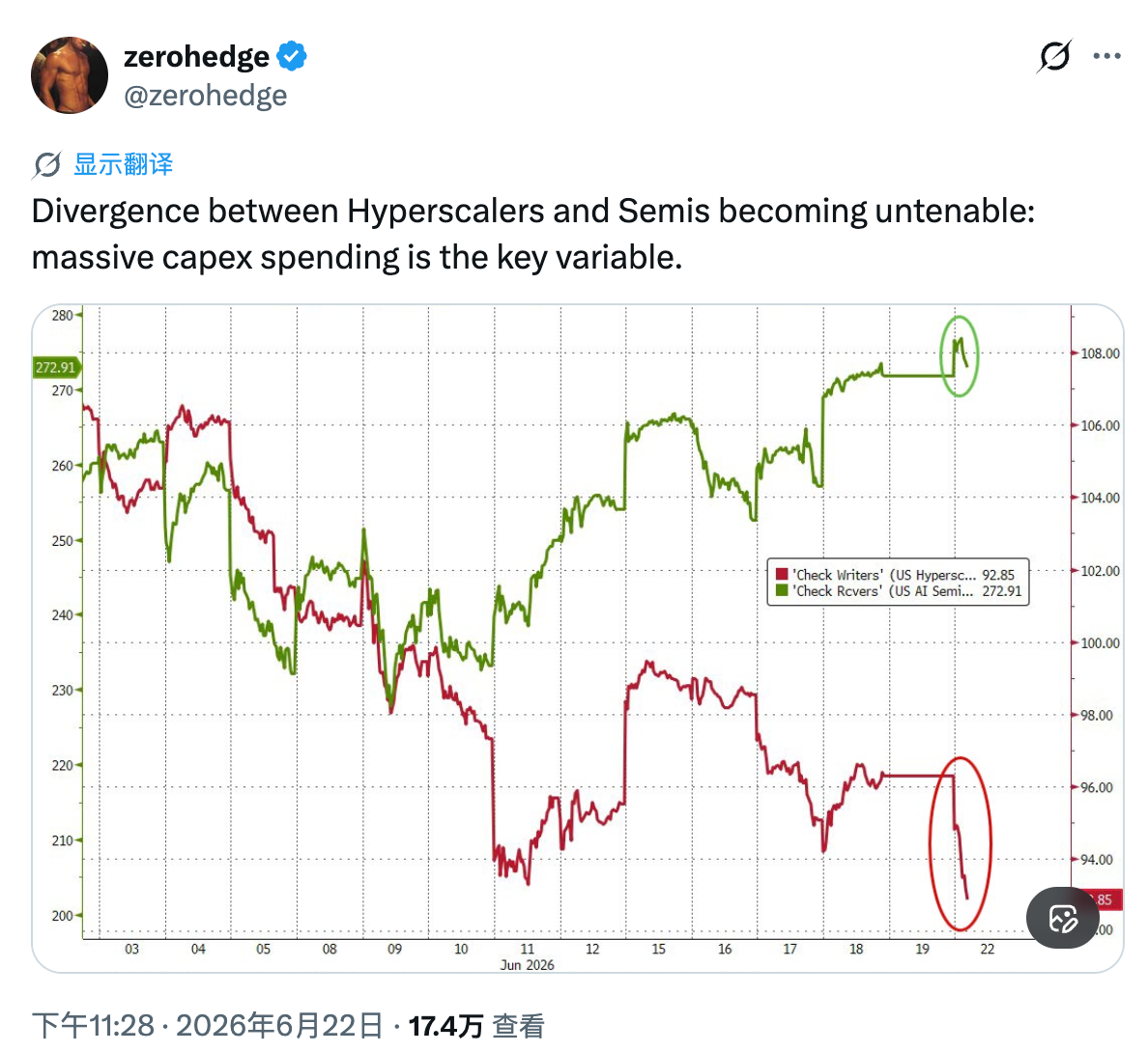

@zerohedge tweeted: The divergence between mega-scale cloud vendors and semiconductors can no longer be sustained: massive capital expenditures are the key variable.

…At that time, we should reverse the words of Eliot: The weeping of the selling will turn into a great sound.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。