Every Monday, Wednesday, and Friday, we analyze the market based on data and seize opportunities by understanding trends. We cover macroeconomics, US stocks, precious metals, crude oil, and cryptocurrencies, gaining insights into key changes in the global market, produced by PANews.

Macro Market

The global market has entered a clear risk contraction phase under the revaluation impact of the AI and semiconductor industry chain. Previous optimistic expectations regarding the expansion of AI infrastructure have encountered marginal corrections; volatility in the South Korean memory chip industry chain has become the catalyst, combined with tighter expectations for Fed policy and continuous capital outflow from ETFs, collectively suppressing the performance of risk assets.

Following a temporary peace agreement between the US and Iran, the passage of oil tankers through the Strait of Hormuz has fully resumed, and crude oil prices continue to retreat, with WTI crude falling below the $73 mark and Brent crude similarly sliding to about $76, which nearly wipes out all gains since the US-Iran conflict on February 28.

In terms of precious metals, gold and silver have both weakened, with spot gold experiencing a daily drop of nearly 2%, dropping to around $4050, while silver plummeted over 5% in a single day, dropping below $62 to hit a new low this year; copper and tin also fell by 3% and 5%, respectively. Wall Street investment banks have collectively lowered their price expectations for gold, with Goldman Sachs significantly cutting its year-end target price for gold to $4900, stating that gold's correlation with energy has weakened and has re-binded to real interest rates, while rising holding costs are forcing gold ETFs to face extreme capital outflow pressure. Deutsche Bank sees a worst-case scenario price of $3800.

Disagreement intensifies among investment banks on Fed interest rate hike paths:

Bank of America analyst Aditya Bhave: US economy's inflation is worsening, and the Fed is expected to hike rates by 75 basis points in September, October, and December, targeting a range of 4.25%-4.5%.

Deutsche Bank: A 50 basis point hike is expected this year, and an earlier action in July cannot be ruled out, as Waller has shown strong anti-inflation determination.

Goldman Sachs: The probability of a Fed rate hike in July is as high as 50%.

Citi: Has postponed its rate cut expectations by one month, forecasting cuts in October and December 2026 and January 2027.

UBS Group: Believes the market is overestimating rate hike risks, predicting rates to remain unchanged for the whole of 2026 and resuming easing in early 2027.

Next key points of attention:

June 25, 20:30: Release of the final value of US Q1 real GDP annualized quarter-on-quarter (expected 1.6%). If capital expenditures driven by artificial intelligence surpass expectations, this will further reinforce concerns of economic overheating and rate hike expectations.

June 25, 20:30: US May PCE and core PCE price index are released (expected core month-on-month 0.5%, year-on-year rising to 4.1%). As the Fed's most favored inflation indicator, this will directly set the tone for the crucial inflation test regarding an early rate hike in July.

US Stock Dynamics

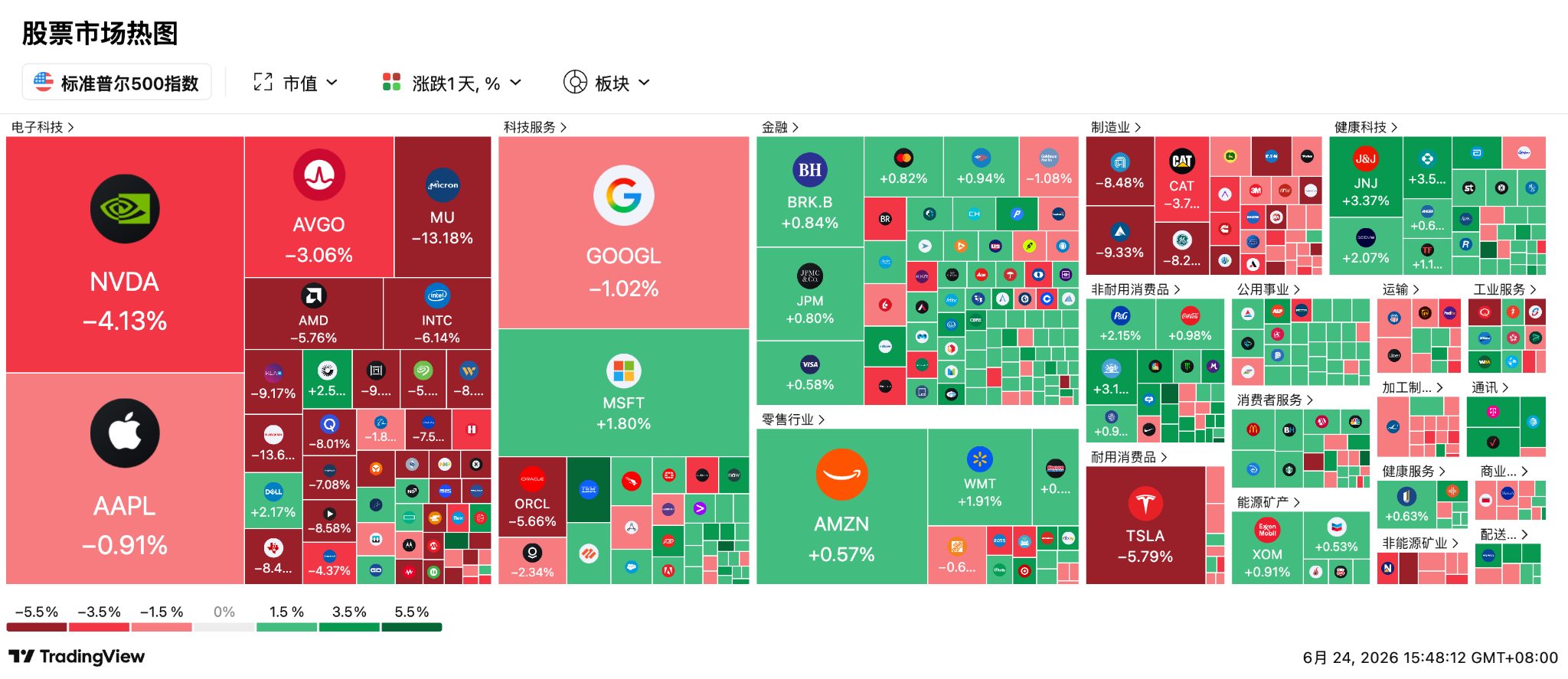

Wall Street faced a terrifying sell-off on Black Tuesday, with the Nasdaq Composite Index plummeting 2.21%, the S&P 500 down 1.44%, while the Dow Jones Industrial Average only slightly dipped 0.09% under defensive funds in consumer and healthcare sectors.

The Philadelphia Semiconductor Index suffered a heavy decline of 7.87%, with all 30 constituents closing down. Micron Technologies, which has surged over 300% this year, saw a drop of 13%, Tesla declined by 5.8%, with SanDisk, ON Semiconductor, Arm, and Applied Materials recording declines of 8% to 14%.

SpaceX ended a three-day decline, eventually rising by 0.98%, with its market cap having briefly fallen below $2 trillion during the day. The current stock price is around $156, down over 27% from its high of $211.39, erasing $600 billion in market value. The company just completed a $25 billion priority unsecured bond issuance (oversubscribed by over $85 billion) for AI expansion of several billion dollars.

Recently listed AI chip manufacturer Cerebras released its first financial report; despite a staggering 92% year-on-year surge in Q1 revenue to $193.4 million, guidance indicating that the core gross margin will drop to 36%-38% next quarter led to its stock price declining by 11% after hours, continuing from $201.

Qualcomm plunged 8%, revealed to be acquiring AI software company Modular at a valuation of $4 billion, yet Bernstein analyst Stacy Rasgon dampened hopes by giving it a "market perform" rating and a target price of $221.90, warning that its data center ambitions face a 37% downside risk.

Nvidia fell 4.15%, with its market cap dropping below $500 billion. The market is waiting for its shareholder meeting to validate executive compensation and the health of AI hardware.

Goldman Sachs strategist Chris Hussey characterized the sell-off as a "deflation of the bubble" rather than a fundamental reassessment; after all, 12 tech stocks that fell over 8% still retain double-digit and even doubled increases this year, showing no signs of capital abandoning the AI narrative.

BTIG analysts referred to this as a "chip disaster" and warned of another 10-15% decline space, with medium-term downside risks not eliminated.

Meanwhile, Evercore ISI and Citi firmly believe that tech giants will regain favor, urging decisive capital deployment during the pullback, claiming that tech giants will recover favor after the sharp drop, and earnings reports will be a moment of proving strength.

Next key points of attention:

Eastern Time on June 24, Qualcomm holds its New York Investors Day Conference: Whether management can quantify the rise in AI mobile unit value and the TAM of over $10 billion in FY2027 will determine if they can escape the recent valuation discount.

June 25, Micron Technology discloses its Q3 financial report for fiscal year 2026: FactSet's John Butters suggests that without Micron, Nvidia's S&P earnings growth will plummet, J.Gold's Jack Gold expects high prices for memory to persist, and Wedbush, Stifel's Brian Chin, and Deutsche Bank have raised target prices to $1300-$1500; FactSet consensus EPS is expected to surge nearly 1000% to $20.57, marking the ultimate battle for the sustainability of AI hardware investment mentioned by Pepperstone analyst Dilin Wu.

June 25, Nvidia holds its annual shareholder meeting: Executives' statements on Blackwell chip progress, executive compensation proposals, and macro capital expenditure will directly influence whether the long-term sentiment in the global semiconductor sector stabilizes.

Cryptocurrency

Bitcoin has been fluctuating downward under shrinking macro liquidity and pressure from US stocks, falling again to below $62000 yesterday. Currently, the short-term support level is in the $60000-$61000 area, while the upper resistance level is between $63500 and $65000. Market maker Wintermute reports that the depletion of liquidity in the summer and stagnant ETF fund inflows are pushing prices toward $59000 as a key observation point. Several analysts indicate that if bulls cannot maintain the weekly 200MA, a complete breakdown will occur, with BTC falling to between $53000 and $58000.

Ethereum followed the market down, dropping nearly 4% to around $1650, while the internal disputes within the ecosystem pose an even graver situation than market price. Faced with the warning from former contributor Trenton Van Epps regarding core development costs of $30 million annually, Kleros co-founder Clément Lesaege proposed to extract 0-10% from validator earnings (approximately 50,000-70,000 ETH, worth up to $115 million) to subsidize the ecosystem, only to be severely criticized by Figment and Twinstake as a "monopoly-style harvest" exploiting retail investors. Although the Ethereum Foundation has decisively laid off 20% (54 people) and cut the budget by 40%, and five former researchers established Ethlabs to bring in capital from BitMine, Sharplink, and Joe Lubin for self-rescue, Bitwise analyst Max Shannon still warns that a 2.7% staking yield is likely to trigger a severe liquidity exit crisis.

Key points of the day:

Binance will support the Polygon (POL) network upgrade and hard fork on June 25

Newton Protocol (NEWT) will unlock approximately 139 million tokens on June 24, valued at about $7.6 million

Plasma (XPL) will unlock approximately 88.89 million tokens on June 25, valued at about $10.4 million

Humanity (H) will unlock approximately 266 million tokens on June 25, valued at about $68.56 million

Upbit 24-hour trading volume ranking: APX, XRP, BTC, WLD, ETH

Bitcoin spot ETF: -$114 million, continuing a four-day net outflow

Ethereum spot ETF: -$82.35 million, continuing a four-day net outflow

HYPE spot ETF: +$1.4583 million

Today, the biggest gains among the top 100 cryptocurrencies by market cap are: BEAT up 49.1%, AVAX up 3.8%, LIT up 2.7%, DASH up 2.5%, KITE up 2.3%.

Asia-Pacific Market

The Nikkei 225 index suffered a steep drop of nearly 4% in early trading due to the sell-off in US tech stocks and global panic sentiment. However, with low buy orders stepping in, the index slowly recovered, ultimately retreating slightly by 0.88%. The yen continues to oscillate in the extremely risky range of 161 to 162, approaching the lowest levels since 1986. Despite the Bank of Japan having raised its benchmark interest rate to a 30-year high of 1.0%, the glaring US-Japan interest rate differential raised by the increasingly intense rate hike expectations from Goldman Sachs and Bank of America has left the market highly wary of any potentially catastrophic foreign exchange intervention actions that the Japanese Ministry of Finance might issue at any moment.

The Seoul Composite Index (KOSPI) in South Korea experienced an epic flash crash yesterday (June 23), with a single-day drop reaching 9.99% and triggering multiple circuit breakers. This plummet resulted from a combination of retail high-leverage margin calls, institutional rebalancing, and policy panic.

On Wednesday (June 24), the KOSPI index rose by 3.26% amid high volatility, with Samsung Electronics up 9.84%, having previously plummeted 12.31% yesterday. The company successfully boosted market confidence by raising its HBM4 shipment expectations and announcing a massive stock repurchase plan worth up to 90 trillion won.

SK Hynix slightly rose 0.98%, after a steep decline of 12.47% at its closing yesterday, marking its biggest single-day drop since December 24, 2008. Despite facing pressure due to delays in HBM4 mass production and reduced shipment expectations, the company is stabilizing fundamentals by leaning towards the highly profitable general DRAM market and signing large contracts with Microsoft.

In the A-share market, the Shanghai Composite Index closed down 0.11%, while the Shenzhen Composite Index rose 1.24%, the ChiNext Index increased by 1.41%, and the STAR Market saw more than a 2% surge. The newly listed semiconductor component stock Zhenbao Technology (688797) skyrocketed to a high of 465 yuan on its first day, closing up 1212%, with the highest profit for one share exceeding 210,000 yuan.

Next key points of attention:

June 25: Bank of Japan Governor Kazuo Ueda will attend an IMF-held central bank lecture event. His statements regarding the inflation outlook and the reduction of bond purchases/rate paths will directly determine whether the yen will instantly breach historical exchange rate defense lines, triggering a global capital reallocation.

July 3: SK Hynix is expected to complete the Korean Financial Supervisory Service’s review for listing American Depositary Receipts (ADRs). If successful, it will significantly reshape the global pricing power of Asian memory giants and have a siphoning effect on capital flow in the general DRAM and HBM markets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。