Leverage and Financing in the Crypto World—trillions of dollars in leveraged positions, collateralized lending, yield products—are built on a non-unified benchmark interest rate curve.

Written by: @BlazingKevin_, Blockbooster Researcher

1. Crypto Has No "Benchmark Interest Rate"

Leverage and financing in the crypto world—trillions of dollars in leveraged positions, collateralized lending, yield products—are built on a non-unified benchmark interest rate curve.

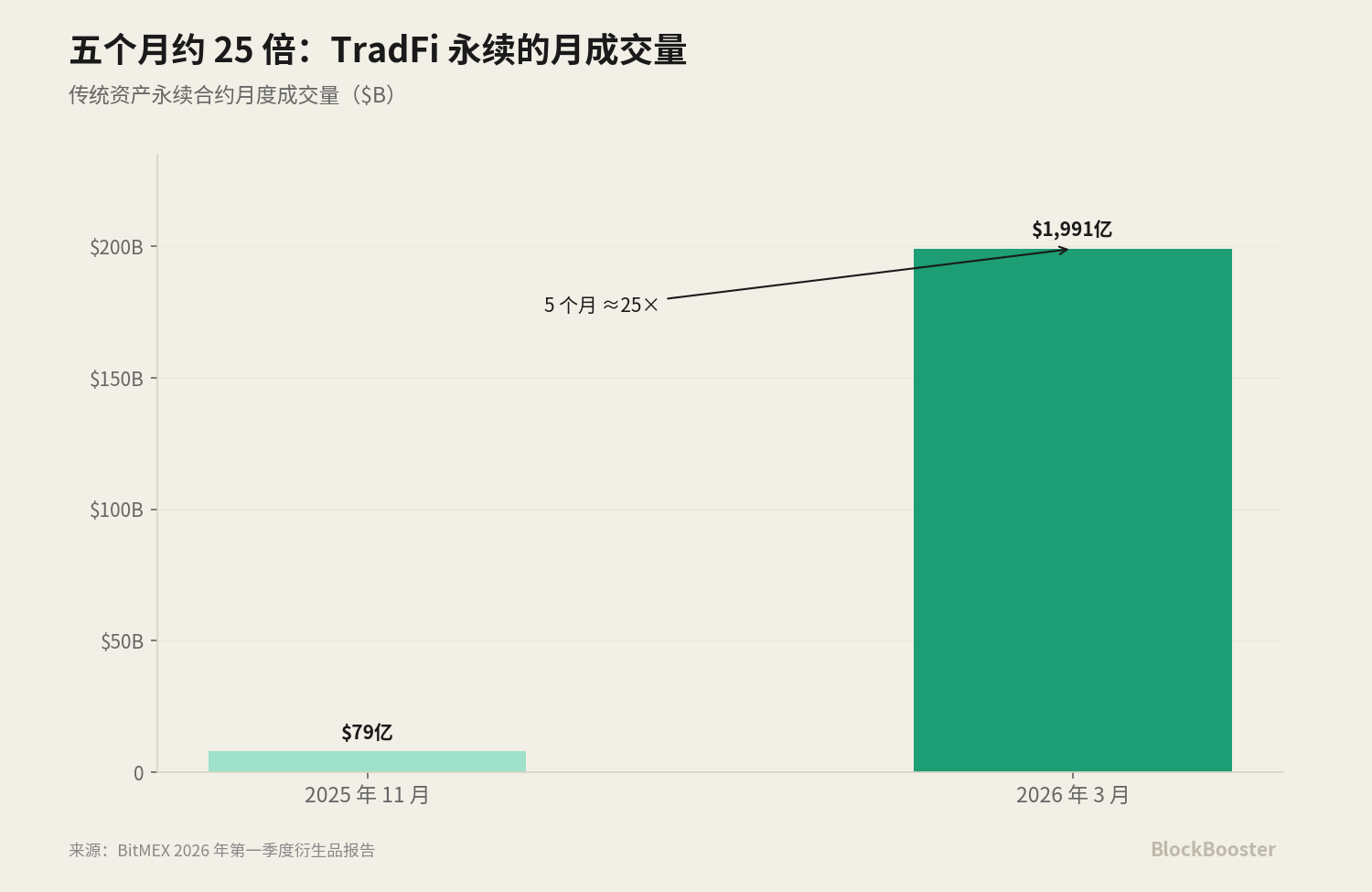

According to BitMEX's Q1 2026 derivatives report, just the new field of "traditional asset perpetual contracts" saw a single season weekly trading volume surge from approximately $525.8 million at the end of 2025 to $30.7 billion in mid-March 2026, a quarterly increase of around 5,756%; its monthly trading volume shot up from $7.9 billion in November 2025 to $199.1 billion in March 2026, growing nearly 25 times in five months.

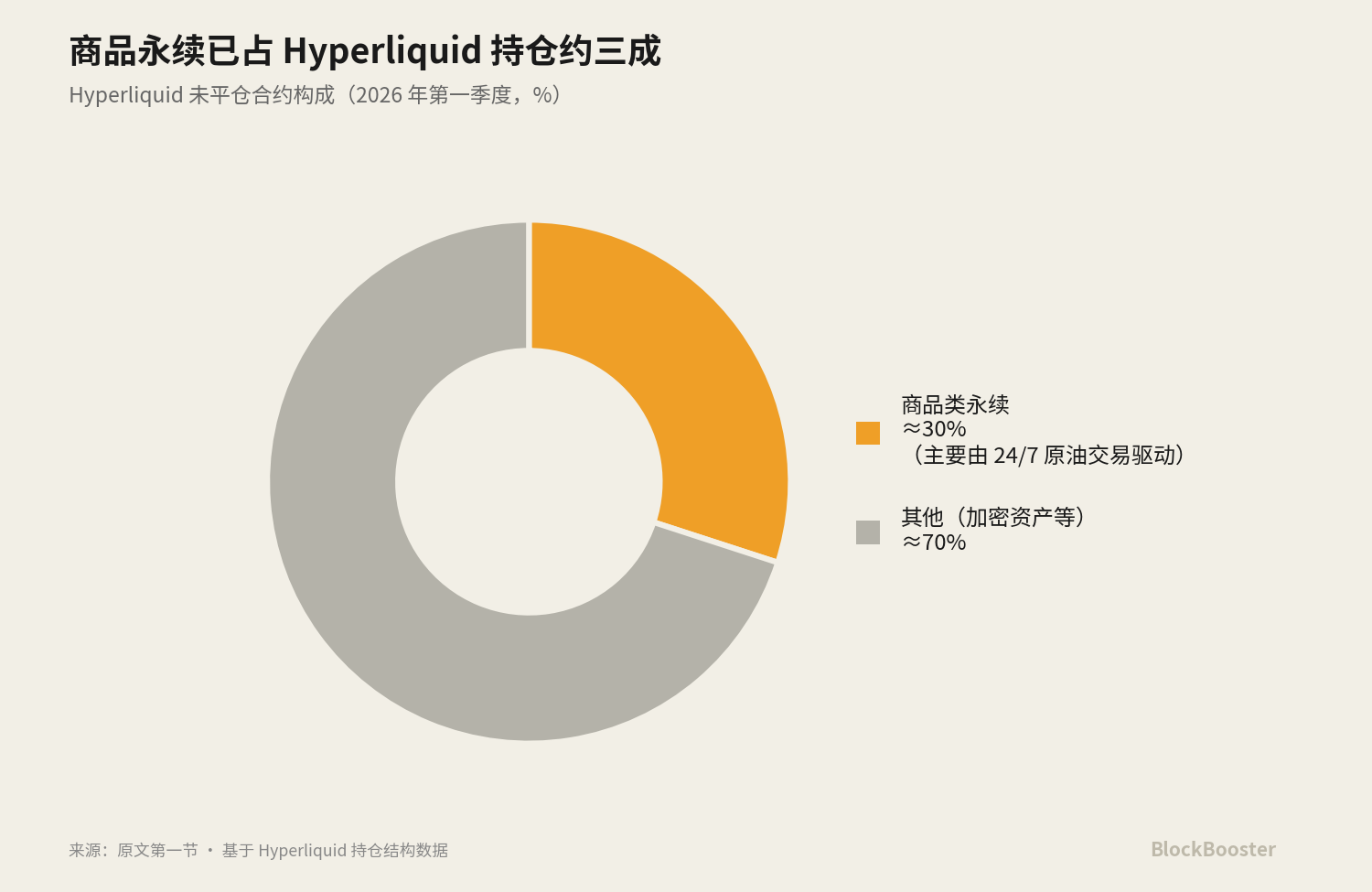

Hyperliquid, according to DefiLlama's 30-day snapshot, processed approximately $172.63 billion in perpetual trades with an open interest of about $9.13 billion. In Q1 2026, commodity perpetuals accounted for about 30% of Hyperliquid's open interest, mainly driven by the demand for 24/7 crude oil trading.

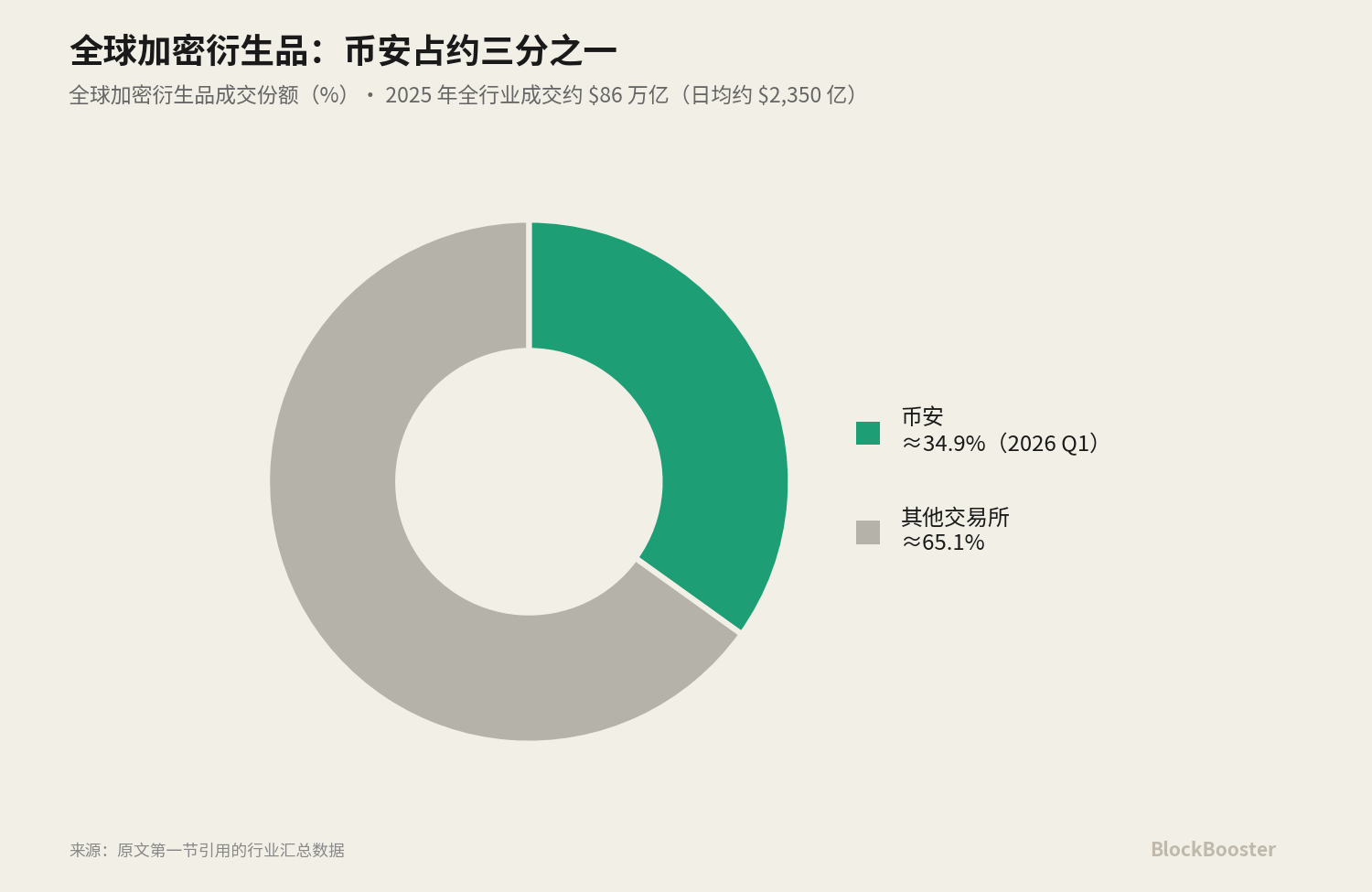

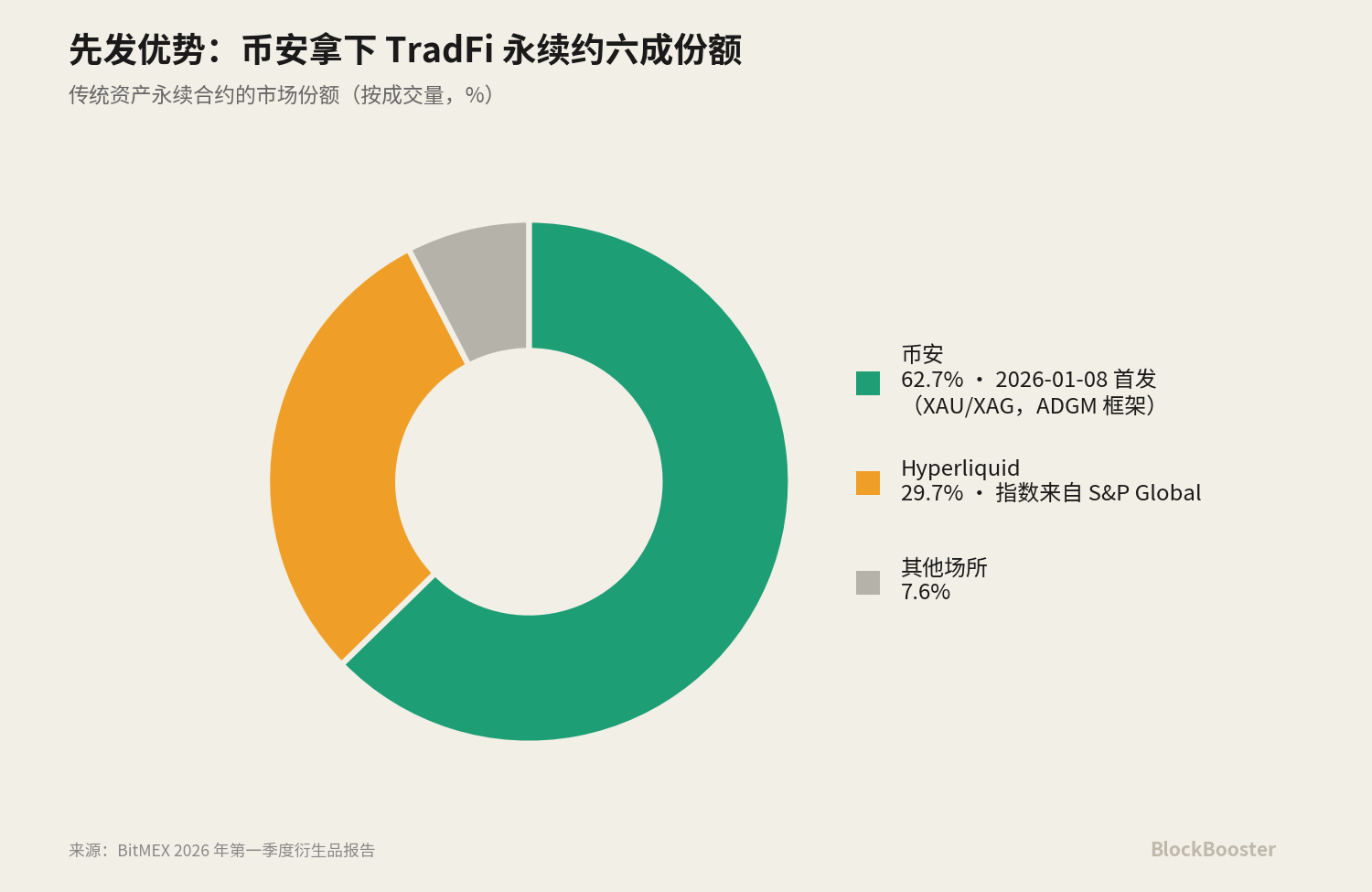

The "traditional asset perpetual" line. Binance launched TradFi perpetual contracts on January 8, 2026, starting with gold (XAUUSDT) and silver (XAGUSDT). Binance has captured about 62.7% of the TradFi perpetual market share with this first mover advantage, with Hyperliquid closely following at 29.7%.

Hyperliquid uses index data for these traditional asset perpetuals from its collaboration with S&P Global, which is currently drawing regulatory scrutiny from the CFTC in the U.S.

Meanwhile, the market capitalization of Ethena's USDe was around $4.5 billion to $5.9 billion at the beginning of June 2026.

Each of these products reports its own "interest rate" or "yield"—the perpetual has a funding rate, lending protocols have lending APRs, sUSDe has staking yields, and tokenized government bonds have coupon rates—but crypto has yet to have its own SOFR. There is no widely accepted benchmark curve that can serve as a pricing anchor. Each exchange, each protocol is becoming a mini financing market, quoting its own price, yet there is no public, trustworthy reference frame among them.

2. What Constitutes a Crypto "Benchmark Interest Rate"?

Let’s first look at three groups of different interest rates for comparison:

- First Group: Benchmark financing rate vs product yield vs implied derivative rate. The APY of sUSDe is a kind of product yield—it is the return for holders; the perpetual funding rate is an implied derivative rate—it is the fee paid between longs and shorts to maintain the perpetual's price anchored to the spot; the benchmark financing rate should be a public reference that can be quoted by countless other products for pricing. Product yields and implied derivative rates are not benchmarks—they are "downstream" from the benchmark, being results after various premiums and structures have been layered on top.

- Second Group: Overnight rate vs term rate. The perpetual funding rate settles every hour or eight hours, which is essentially an overnight rate—it only reflects the funding cost "from this moment to the next settlement point," lacking a term structure. It cannot tell you the price difference between "borrowing for 30 days" and "borrowing for 90 days." Just as SOFR itself is an overnight rate that relies on the futures market to construct a Term SOFR with term structure. A rate with no term structure cannot support any medium to long-term fixed income market.

- Third Group: Actual borrowing rate vs algorithmic/implied rate. Feasible bilateral borrowing transactions (such as Bitfinex's margin financing market, which matches real lenders and borrowers) and algorithmic utilization pricing (like Aave, where rates are calculated automatically based on the utilization of the liquidity pool) are based on fundamentally different price generation mechanisms. The former is what market participants vote with real money, while the latter is a curve designed by protocol developers in code.

From these three groups, we can distill the standards that a "qualified benchmark" should meet:

It must be based on real transactions, with an underlying market that is broad enough and deep enough (difficult for a single participant to manipulate), governance independence (no conflicts of interest between managers and the priced market), and ideally possess a term structure (able to support medium to long-term pricing).

(The underlying of SOFR is overnight repurchase agreements collateralized by U.S. Treasuries, with daily trading volumes "frequently exceeding $1 trillion." This is the real trading volume of overnight repos. It is completely different from the nominal amounts that support Term SOFR.)

Using the logic of SOFR to examine crypto has structural isomorphism. The Bank for International Settlements, in its research, likened the on-chain collateralized lending market to a "crypto-native money market," its operating mechanism resembling that of traditional triparty repos—over-collateralization, mark-to-market settlement, and overnight rolling. Since on-chain lending structurally resembles collateralized financing, it is appropriate to evaluate crypto benchmarks using the design of SOFR (a benchmark built on the real transactions of repos) as a relevant isomorphism.

3. What Are the Characteristics of SOFR? Why is LIBOR Being Phased Out?

LIBOR (London Interbank Offered Rate) was once the cornerstone of global finance. At its peak, about $300 trillion in financial contracts (including interest rate swaps, mortgages, student loans, corporate bonds, etc.) relied on LIBOR from five currency zones. However, LIBOR has a fatal design flaw: it is not based on real transactions, but is an estimate of borrowing costs reported daily by a small number of quote banks.

This flaw was explosively revealed after the 2008 financial crisis. Regulatory investigations found that traders at several major global banks systematically manipulated LIBOR quotes to benefit their derivative positions.

The manipulation scandal directly led to the phasing out of LIBOR.

In its place came SOFR (Secured Overnight Financing Rate). The design of SOFR is almost a "reverse engineering" for each flaw of LIBOR: it does not use self-reported estimates but is based on real transactions in the overnight repurchase market collateralized by U.S. Treasuries; it takes the volume-weighted median of transactions from three repo markets (triparty repos, GCF repos, and bilateral repos cleared via FICC's DVP service), which have a wide base, great depth, and are difficult for a single participant to manipulate; it is managed by the New York Fed, adhering to IOSCO benchmark principles, ensuring there is no conflict of interest between managers and the priced market.

However, SOFR has an "intrinsic defect": it is an overnight rate without a term structure. The market requires more than just "today's overnight cost," but also "expected funding costs for the next three months" to price medium to long-term loans. Thus, CME introduced CME Term SOFR—a set of forward-looking rates covering 1 month, 3 months, 6 months, and 12 months tenors.

It deduces the market's expectations for future SOFR paths based on the trading data of SOFR futures to "piece together" a forward-looking term curve. (The representative nominal amount for constructing Term SOFR with SOFR futures is about $23 trillion daily in Q4 2023.)

4. Some Discussable Candidate Rates

There are many candidates in the market regarded as "interest rates" or "yields." Here, we will break them down one by one and discuss why some rates are obviously unsuitable as benchmark rates and which ones have the potential for evolution.

A thread running through all this analysis is—"who has the power to decide": is it market-weighted, algorithmic utilization, or governance-set?

4.1 Perpetual Funding Rate (Hyperliquid/Binance)

The perpetual funding rate is the implied price of leverage driven by the basis between the spot and perpetual: it is essentially an overnight rate without a term structure.

When the spot market for TradFi assets is closed (such as stocks or precious metals during weekends), exchanges cannot get real spot prices to calculate the funding rate. Binance's solution is to freeze the index price at the last spot price and instead use an EWMA marked price with a ±3% cap; Hyperliquid also switches to EWMA on weekends, setting volatility limits by category. During closed periods, the "anchor" for perpetual prices is actually a predicted value rather than a real transaction price. When the market reopens and the real price gaps exceed this cap, a limit-up/limit-down situation occurs. Thus, the price during closed market periods is a prediction, not an arbitrageable real anchor.

On May 29, 2026, the U.S. CFTC approved KalshiEX's Bitcoin perpetual contract (BTCPERP), which marks the first truly perpetual, regulated Bitcoin contract without an expiration in the U.S., along with a policy statement on perpetual contracts, staff guidelines for 24/7 trading and clearing, and a no-action stance for Coinbase’s perpetuity provided through Deribit. The significance of this move lies in the fact that a regulated, centrally cleared perpetual means its funding rate and basis are generated in a compliant, clearing-supported environment—this is precisely one potential candidate for the future "Crypto SOFR." Together with the aforementioned Hyperliquid–S&P Global collaboration under CFTC scrutiny, it signals that "regulation is approaching a crypto benchmark."

4.2 Bitfinex Margin Financing + FRR

This is the native U.S. dollar term financing market of crypto.

The mechanism works like this: Bitfinex operates a peer-to-peer margin financing market, where lenders lend funds to margin traders to earn interest. The key design is that the financing term is from 2 to 120 days (common terms are 2 days, 7 days, 30 days), and both the interest rate and term must match when matched. This means that Bitfinex's financing market naturally constitutes a genuine borrowing curve from the short to the long end: the rates for 30-day funds and 120-day funds differ, matched by real supply and demand. This is one of the few genuine lending markets in the crypto world with a natural term structure.

The FRR (Flash Return Rate) serves as the reference rate for this market: FRR is the average rate weighted by the size of all active fixed-rate financings, updated every hour. Essentially, it is "a Bitfinex version of a benchmark reference rate"—an index reflecting the current average borrowing cost in the market. Lenders can directly choose to lend based on FRR, thus allowing their rates to automatically follow the market.

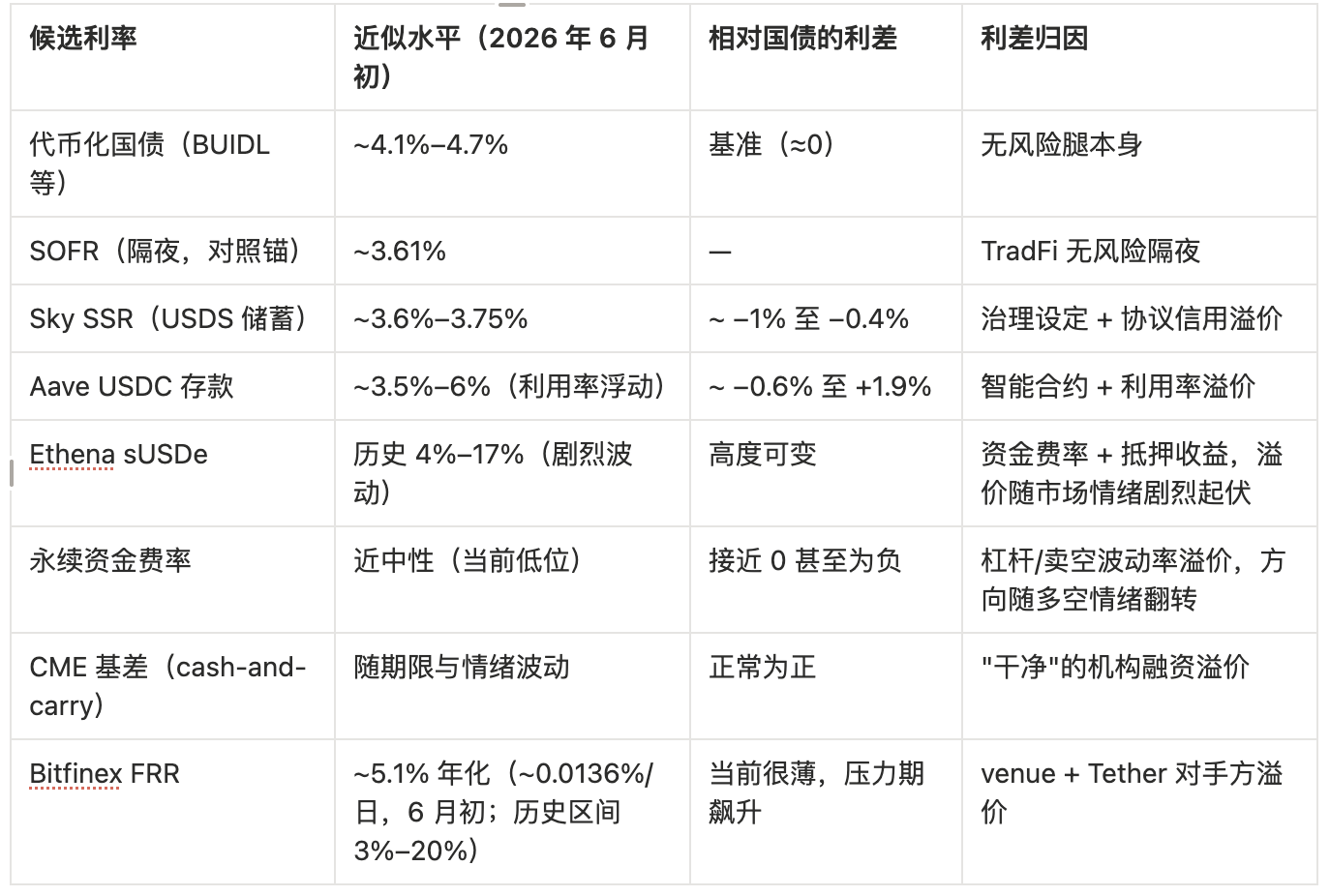

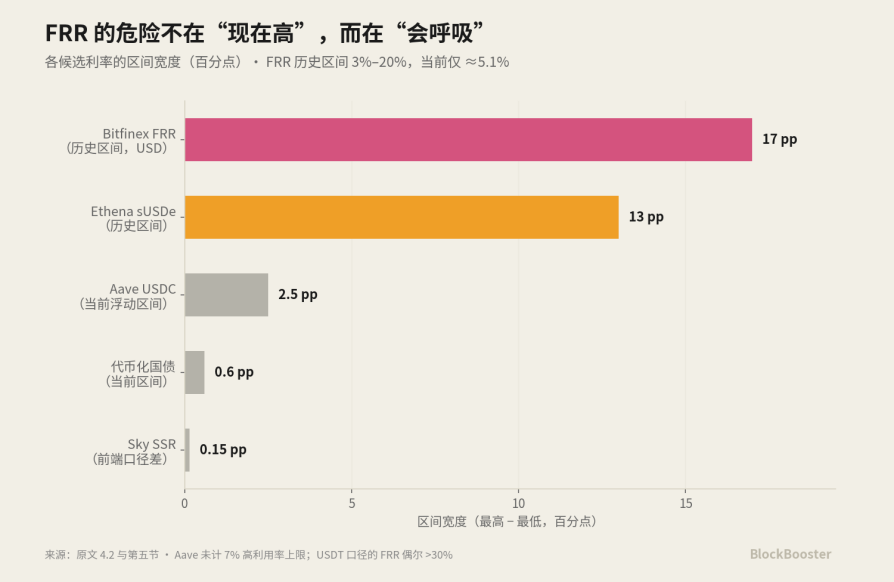

Bitfinex charges about 15% fees on lending yields (with hidden orders at 18%); the minimum order amount is $150. FRR is quoted as a daily rate and annualized based on the daily rate: Bitfinex USD’s FRR is about 0.0136% per day, approximately 5.1% annualized—at par with candidates like tokenized government bonds, Aave, SSR, etc.

The key point is its volatility: the historical range for USD lending rates fluctuates sharply between 3%–20% APR, closely tied to leverage demand.

This daily rate curve expands across terms from 2 to 120 days, forming a native U.S. dollar financing curve in crypto with genuine term structure.

Bitfinex and Tether share the parent company iFinex, and there is overlap in management. This gives Bitfinex the most abundant USDT liquidity in the entire crypto world—one of the reasons for its deep financing market; however, at the same time, it has concentrated counterparty risks along with risks from the stablecoin issuer within the same composite. Borrowing money from Bitfinex, utilizing Bitfinex's matching, priced in Tether, and backed by the same parent company under extreme conditions—this is a highly self-contained structure.

Although the Bitfinex financing market is the oldest and deepest native U.S. dollar term financing market in crypto, its absolute scale (the stock and daily matching volume of the financing pool) remains much smaller compared to the trillions in trading volume seen in the aforementioned perpetual markets.

Comparing FRR to LIBOR and SOFR, on the dimension of "whether based on real transactions," FRR is actually cleaner than LIBOR; FRR is calculated based on real, executed fixed-rate financing weighted by size, reflecting actual market behavior. However, FRR comes from a single exchange's order book (concentration), operated by the same parent company iFinex that simultaneously controls the largest stablecoin Tether (conflict of interest), and this operator is also the last lender of record for this market (further concentration and conflict). Thus, FRR, in terms of concentration and conflicts of interest, hits the areas that SOFR aimed to eradicate.

4.3 DeFi Lending Rates (Aave/Morpho)

This is representative of algorithmic utilization pricing: the interest rates are not determined by bilateral matching but are automatically calculated by the utilization rate of liquidity pools through preset formulas—the higher the utilization, the higher the interest rates. It fluctuates in real-time with borrowing demand.

The USDC deposit rates on Aave's mainnet fluctuate between about 3.5%–6% based on utilization; the USDC treasury managed by curators on Morpho, after deducting curator fees, yields about 5%–7%.

4.4 MakerDAO/Sky Savings Rate (DAI's DSR/USDS's SSR)

This is a "policy-like interest rate" directly set by protocol governance. DAI's DSR (Dai Savings Rate) and USDS's SSR (Sky Savings Rate) are widely referenced, functionally similar to a policy rate set by a central bank—it is not determined by market matching or triggered by algorithmic utilization, but by governance voting within Sky.

The governance setting of DSR/SSR, the market weighting of FRR, and the algorithmic utilization of Aave constitute a contrast of three fundamentally different interest rate generation mechanisms.

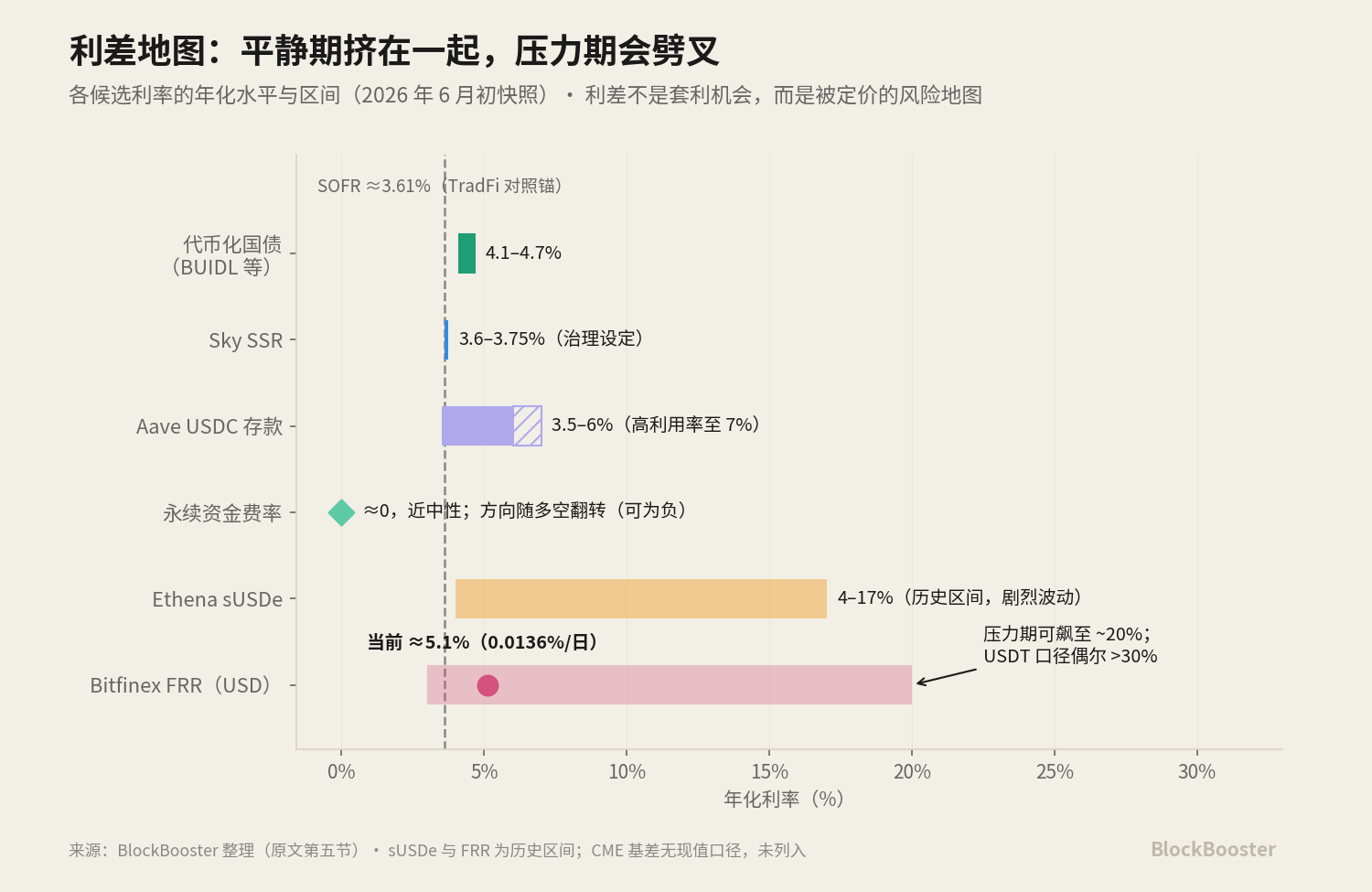

Governance setting vs. market weighting vs. algorithmic utilization—each of these mechanisms has its own trust issues and risks of manipulation, and a mature market benchmark should ideally come from the one that is least susceptible to manipulation (true trades weighted by market, and wide and deep enough). Currently, the SSR was adjusted down from 4.75% by governance to about 3.6%–3.75% by early June 2026 ("governance setting" operates along Fed paths); USDS circulates approximately $11 billion.

4.5 Tokenized Government Bond Yields (BUIDL/BENJI, etc.)

This represents about a 4–5% "risk-free leg," qualifying it as a candidate for "crypto's risk-free benchmark." BlackRock's BUIDL, Franklin Templeton's BENJI, etc., bring the coupon yields of U.S. Treasuries on-chain. Currently, the main tokenized government bonds (BUIDL, USDY, USDM, USYC, etc.) pay around 4.1%–4.7% APY as of April 2026, closely aligning with the yield of 3-month U.S. Treasuries. Its yield almost directly parallels traditional risk-free rates.

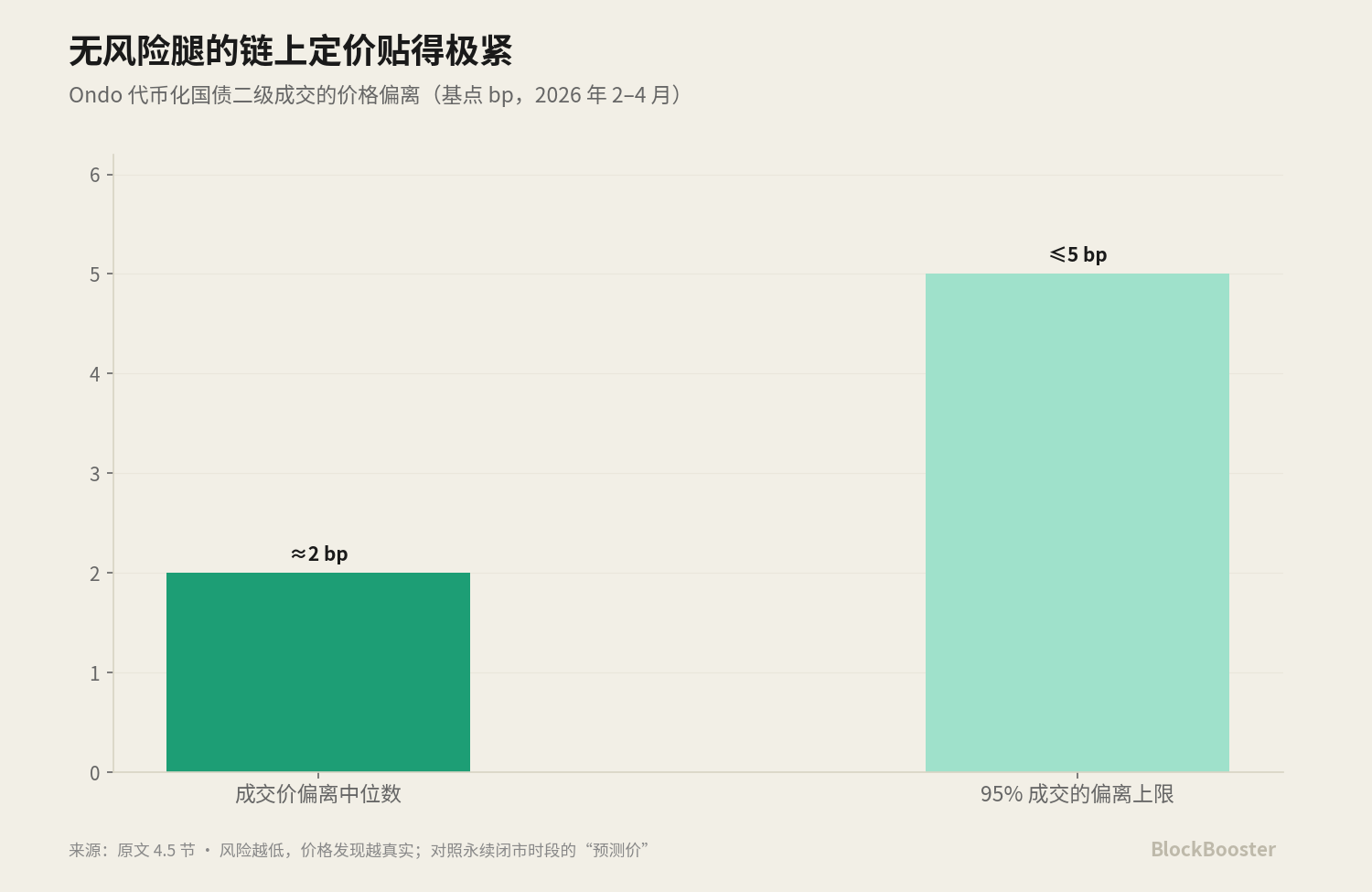

The pricing of this "risk-free leg" in the secondary market is very tight—for instance, Ondo’s tokenized government bonds, from February to April 2026, showed a median trade price deviation of only about 2 basis points, with 95% of trades falling within 5 basis points. This illustrates that when the underlying asset is sufficiently standardized and risk-free, on-chain price discovery can be very accurate; in contrast, the "prices" of high-risk varieties like perpetuals during closed market periods are filled with predictive elements—lower the risk, the more real the price; higher the risk, the more pricing resembles guessing.

4.6 Ethena sUSDe

This is a securitized product combining perpetual funding rate and collateral yield. Its APY heavily depends on the funding rate level in the perpetual market, thus, it is essentially a repackaging of the implied rates, not a benchmark in itself.

Putting seven candidates together: each measures different things (leverage sentiment, actual borrowing, algorithmic utilization, governance policy, risk-free coupons, institutional arbitrage), carries different risks (liquidation, counterparty, smart contracts, governance, credit), and is priced by different entities.

No single one meets all three conditions of "wide base + term structure + governance independence" simultaneously.

This is the current state of the crypto benchmark rate: there is not one piece that can independently serve as an anchor.

5. Discussion on Building a Spread Map:

We place the above candidate rates side by side on the same or comparable tenors and first provide a numerical snapshot with a cut-off date:

Writing the logic of this table in attribution form:

- Perpetual funding rate − Government bond yield ≈ Leverage / short-selling volatility premium

- Bitfinex FRR − Government bond yield ≈ venue risk premium + Tether counterparty premium

- Aave lending rate − Government bond yield ≈ smart contract risk premium

- DSR/SSR − Government bond yield ≈ governance setting and protocol credit premium

- CME basis − Government bond yield ≈ "clean" institutional financing premium

Looking at Bitfinex's FRR. Currently, it is about 5% annualized, closely aligned with tokenized government bonds (~4.5%), Aave (~4–5.5%), SSR (~3.6%)—the spread is very thin. FRR appears unremarkable, similar to other candidates. However, the danger of FRR does not lie in its "extreme volatility." The historical range of USD lending rates has fluctuated sharply between 3%–20% APR: during calm periods like now, it converges near risk-free rates; yet once it enters high leverage, high demand, or market pressure periods, it can surge rapidly.

Treating such a rate as the pricing anchor for the entire market means that the anchor itself will fluctuate wildly at the times most in need of stability.

In traditional finance, if two instruments reflect the same risk yet provide different rates, arbitrageurs would quickly step in to compress the spread. But in crypto, the spread is rather the structural risk priced by the market.

The Bank for International Settlements (BIS) Working Paper points out: the scale of carry in crypto can become extremely large—sometimes exceeding 40% per annum and fluctuating wildly over time; and at moments of stress, it can turn violently in the opposite direction—during the FTX collapse, CME's carry briefly dropped below −50%. Crypto presents negative convenience yields (investors prefer holding futures over spot), which is exactly the opposite of commodities markets—yet similar to dynamics seen in certain government bond markets (balance sheet constraints make derivatives more attractive than holding spot). In other words, the largeness of crypto carry and its resistance to arbitrage being leveled out stems from the difficulty of regulated capital holding spot, only participating through futures, alongside the scarcity of arbitrage capital due to margin and clearing risks.

Conclusion

Judging by regulatory trends and capital flows. The possible combinations in the future might be: tokenized government bonds as the foundation of a risk-free leg + term curves constructed from CME basis / Bitfinex term structure / on-chain interest rate swaps—or, a governance-neutral aggregated index.

The logic behind the former is that the risk-free leg should naturally be anchored by the assets closest to being risk-free, while the term curve needs to be pieced together from existing sources with term structures; the logic behind the latter is that rather than relying on any single source, it is better to create a neutral index aggregated from multiple sources, designed to avoid concentration.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。