Ghost shares and securities lending chaos, tokenized stocks are just a repackaging solution.

Written by: Vaidik Mandloi

Translated by: Saoirse, Foresight News

Did you know that a partnership in New York named Cede & Co. is the statutory registered holder of approximately 83% of the circulating stocks in the United States? Even when you buy Apple stock through brokerages like Schwab or Robinhood, the legal holder of those shares remains Cede & Co.

Cede is the nominal holder for the Depository Trust Company (DTC), and its letter of authorization submitted to the U.S. Securities and Exchange Commission (SEC) clearly states: the agency "does not know the identity of the actual beneficial owners of the securities." Simply put, Apple has no idea that you own its stock; only your brokerage knows this because you are its customer. However, in the complete chain of ownership, your identity is completely absent. The word "Cede" comes from Latin, meaning "to relinquish power and transfer rights," which is a fitting name for this institution.

For this reason, I have delved into the origins of this system, what it means for ordinary investors, and whether the stock tokenization model claimed by the crypto industry can indeed break away from this framework.

Ownership Chains and Systemic Risks

When you buy stocks through an American brokerage, strictly speaking, all you hold is a "security benefit right" - to put it bluntly, this is merely a debt claim you have against your brokerage.

The complete process of purchasing stock essentially works like this: the Depository Trust Company (DTC) updates its ledger to record that the corresponding shares belong to your brokerage; the brokerage then updates its internal records to indicate that this share belongs to you. Between you and the actual target stock, there are three layers of debt receipts, and all you have is the intermediary's promise to pay; you have no direct control over the underlying asset.

This multilayered system of rights has given rise to many issues: brokerages have the right, without your permission, to lend your shares to short sellers. In other words, someone can borrow the stock you purchased to bet on a price decline, while you remain unaware of it. Furthermore, voting rights at shareholder meetings cannot directly fall to you; the voting rights will flow through layers of intermediaries. Additionally, throughout the trading day, securities may be repeatedly used as collateral, with multiple institutions simultaneously claiming to hold the same asset.

Estimates indicate that the actual holders of U.S. Treasury bonds are only one-third of the registered creditors; two-thirds of the rest only hold debt certificates that have long been pledged as collateral. This distorted system's origins are even more lamentable.

In the late 1960s, the U.S. stock market operated entirely based on paper certificates. The transfer of stocks meant that physical certificates circulated among various institutions, and a single transfer could require filling out as many as 33 different forms. Every afternoon, hundreds of couriers, mostly retired police officers and firefighters, would drag suitcases and large wooden boxes filled with stock certificates, moving back and forth between brokerages in downtown Manhattan. A firm acquired by Merrill Lynch once employed 600 people dedicated solely to processing paper stock certificates.

Source: Investopedia

In 1968, daily trading volume on the U.S. stock market reached 20 million shares, which was a massive amount at the time, only one percent of today's average trading volume. The overwhelming number of settlement slips completely crushed the brokerages' backend clearing systems, prompting the New York Stock Exchange to close all day on Wednesdays, while also shortening the trading hours on other days, all to catch up in processing the mountain of paper documents.

The enormous clearing pressure directly led to the collapse of longstanding brokerage Goodbody & Co. The chaotic paper settlement system also bred substantial financial crimes. In 1971, the U.S. Attorney General testified to the Senate that the total value of stolen securities exceeded $400 million in just three years; a 22-year-old stock clerk at a brokerage was prosecuted for stealing $900,000 worth of IBM paper stock certificates.

At that time, Congress even suggested that all market clearing and settlement businesses be placed under federal government management. To avoid this scenario, Wall Street completely overhauled the existing paper circulation model: they built centralized depositories to store all physical stock certificates securely, and ownership changes would only update electronic ledgers, eliminating the need to transport physical certificates. This mechanism was known as the "securities immobilization system," and the Depository Trust Company (DTC) was established in 1973 to serve as a unified repository.

There was, in fact, another alternative plan at the time - "paperless total dematerialization," which would completely abolish physical certificates and allow every investor to hold shares electronically. However, the regulators ultimately chose the immobilization system because it could be implemented more quickly under crisis circumstances, originally intended only as a temporary measure. By 1994, the Uniform Commercial Code (UCC amendment) was implemented across all 50 states, effectively legalizing this temporary mechanism permanently, which still continues to this day.

Phantom Shares: The Common Malady of Old and New Systems

This new model of rights assertion relying on ledger changes rather than physical certificates has given rise to entirely new vulnerabilities: multiple parties can simultaneously claim ownership of the same share. For example, when short sellers borrow stocks to sell, the buyer will see a complete stockholding record in the brokerage account, but the lending party’s account, from which the stock was borrowed, has not canceled the original stockholding record.

Both systems will show that they hold the share, and these shares can be lent out again and cycled for short selling. Repeating this operation can result in the total registered debt in the market exceeding the actual total number of shares in circulation of the target company, giving rise to "phantom shares."

In the 2017 Dole Food privatization incident, investors filed claims to hold 49.1 million shares, while the company’s actual circulating share capital was only 36.8 million shares, meaning that the registered debt exceeded the real share capital by 33%. These phantom shares did not arise from man-made fraud or market manipulation but stem from the design flaws of the clearing system dominated by Cede & Co. It was only when the company initiated the privatization process that DTC's ledger exposed the nested, repetitive rights assertion trading vulnerabilities.

The GameStop incident showcased this issue even more severely. In early 2021, the short interest in this stock reached over 140% of the circulating share capital, meaning that the number of shares sold short surpassed the actual market circulation total. This epic short squeeze event hit the headlines across major media, and during the price surge phase, brokerages like Robinhood restricted users from buying but did not prevent selling. Investors from the Reddit WallStreetBets community immediately questioned why brokerages had such control powers, and it was then that everyone discovered that the stocks under their names were not registered in their personal names, but were all held by Cede & Co., and were continuously being lent out for short sellers to bet against themselves.

Source: reddit

Subsequently, a large number of investors chose to transfer all their shares out of brokerages to the official transfer registration institution of WallStreet, directly registering their names on the shareholder list of the listed company. As of 2023, approximately 76 million shares completed direct registration, accounting for about a quarter of the company's total equity.

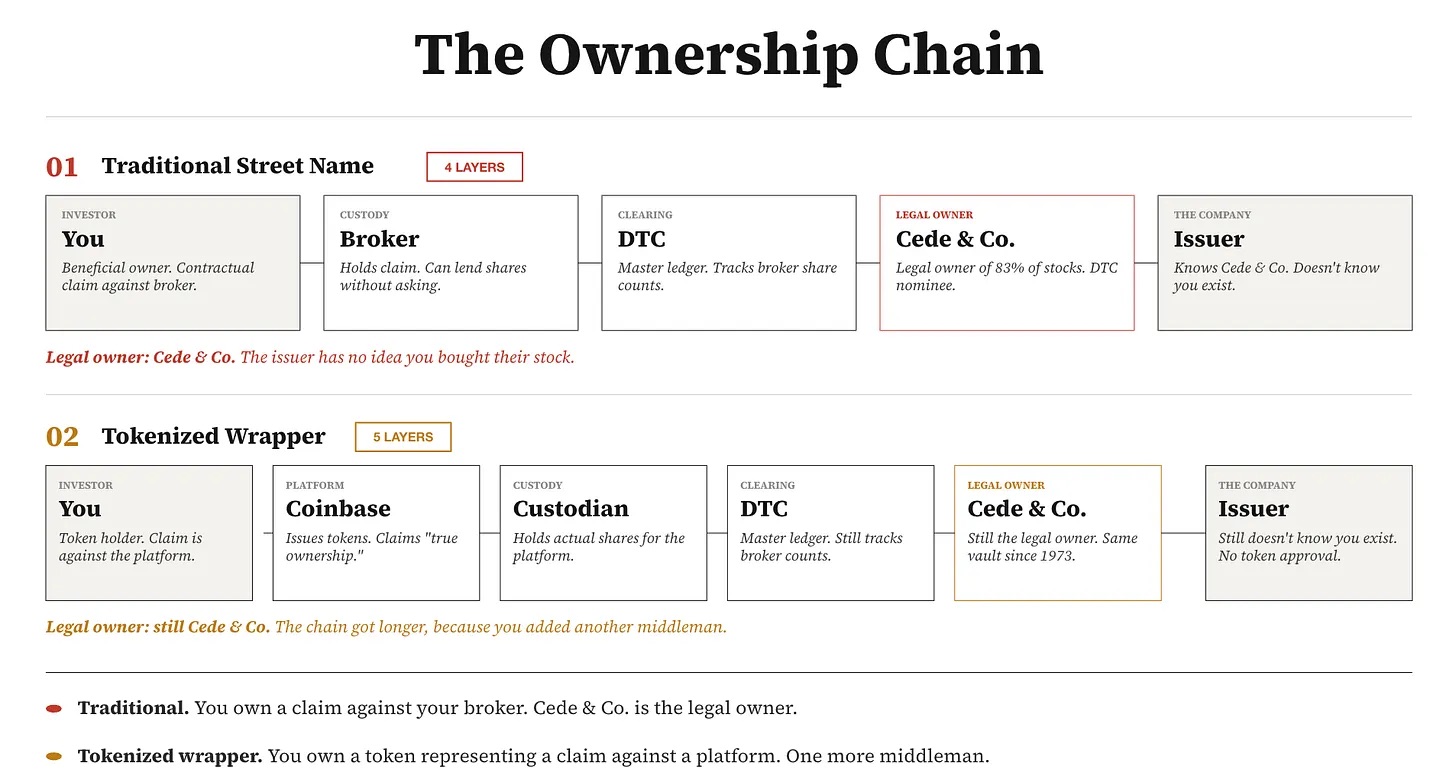

Recently, Coinbase launched a tokenized stock product, claiming to achieve "true equity ownership," ensuring full shareholder voting rights and dividend entitlements. However, dissecting the underlying operational logic reveals that tokens backed by third-party custodians one-for-one corresponding to stock are essentially still a debt claim of the investor against the custodian. The only change is that the accounting database has switched from the DTC's internal ledger to a blockchain ledger; the intermediary layers between you and the real stocks remain unchanged, and even there is an additional layer of the token issuance platform.

Traditional system's layers of ownership:

- Registered holders in the shareholders' registry of listed companies: Cede & Co.

- Cede as the custodian holding shares for the Depository Trust Company (DTC)

- DTC's ledger records the total amount of shares held by each brokerage

- Brokerage internal ledger splits record the corresponding shares for each retail investor

You and the listed company are separated by four layers of intermediaries, and the listed company is entirely unaware of your existence.

Moreover, the tokenized stock models launched by Coinbase and Robinhood do not represent any breakthrough: custodial institutions still hold shares through the DTC, and the statutory registered holder remains Cede & Co.; the token issuance platform further issues debt certificates based on the custodial assets; the tokens in your hand are merely a debt claim against the token platform.

Last year, Robinhood launched the OpenAI tokenized investment product in Europe, employing this model. These tokens do not represent direct ownership of OpenAI equity but rather allow ownership of shares in a special purpose vehicle (SPV) that holds the corresponding stocks. What you own is merely the interest in this shell company, and OpenAI itself will have no knowledge of your identity. Within hours of the product's launch, OpenAI officially announced that it had never authorized any stock equity splitting or transfer, and had no connection with the token product.

Anthropic took an even stronger stance in May 2026, directly announcing that any stock transactions not approved by the board were invalid. Previously, the PreStocks platform had a thriving token trading market for Anthropic, and after the announcement, the price of these tokens plummeted by 27% in a single day.

Source: Kucoin

This sufficiently demonstrates that merely being able to track stock price fluctuations is entirely different from actually owning stock rights. The former only allows you to earn gains from rising stock prices, while the latter grants you the statutory rights of shareholders, voting rights, and a complete ownership certificate recognized by the court.

The most typical extreme case is SpaceX. Multiple crypto exchanges launched tokenized share products related to the anticipated IPO of SpaceX and sold them to the public, accumulating total orders exceeding $1 billion. The market hype at the time was unprecedented, as ordinary retail investors had no channels to invest in SpaceX; these token products made investors feel that the crypto industry had finally fulfilled its initial promise of inclusive investment. However, later the leading service provider XStocks was completely unable to deliver the underlying stock, forcing all exchanges to cancel orders and issue full refunds.

This product fundamentally had no underlying tokenizable assets; the entire business was built upon a debt claim, but within the entire business chain, no party could access real stocks.

Of course, there are exceptional solutions that can achieve true stock ownership, which is also a third viable model. Superstate is a registered transfer registration institution with the U.S. Securities and Exchange Commission (SEC), directly registering statutory equity on the Solana blockchain. The tokens held by users are equivalent to direct stock ownership, with no custodial intermediaries existing between investors and the listed company. This is precisely the effect that was intended to be achieved fifty years ago with the promotion of a completely paperless registration scheme and is the only model that rightfully deserves the term "ownership."

Kraken also operates tokenized stock business relying on its licensed brokerage firm, and it continues to thrive while peers have collapsed. In addition, Singapore's central depository has already established related mechanisms, allowing all retail investors to directly and legally hold their shares with direct voting rights, without any nominal holder intermediaries throughout the process.

The pathways for relevant regulation have long been clear. In May 2025, the U.S. Securities and Exchange Commission (SEC) officially confirmed that licensed transfer registration institutions could directly use blockchain as an official shareholder registry, without needing to build an off-chain paper ledger. Superstate has already implemented this mechanism on the Solana public blockchain: while users hold tokens, their personal names will be recorded as registered shareholders in the core files of the transfer institution. Securitize adopted the same structure, providing technical support to BlackRock's BUIDL fund, which manages over $4 billion in tokenized assets; the New York Stock Exchange (NYSE) also selected Securitize in March 2026 to build its own tokenized securities trading platform.

Countries like Switzerland, Germany, and Liechtenstein have also introduced laws recognizing on-chain records with legal ownership certificate validity. However, the reality is that, solely in the U.S. market, this multilayered intermediary industry chain is worth $200 billion annually. Just for the processing of proxy voting materials and investor information handling, Broadridge earns about $3.4 billion annually. When the DTC launched its own tokenization pilot project at the end of 2025, it still used the original structure, retaining Cede & Co. as the statutory registered holder, without a single reduction in any of the intermediary links of the entire industry chain.

Objectively speaking, token products do have certain value. For investors in places like Lagos and Jakarta, who previously had no access to buy Apple or NVIDIA stocks, even holding tokens representing debt claims through a special purpose vehicle (SPV) constitutes a new investment channel. However, the fact that OpenAI could deny the validity of related tokens mere hours after the product launch, and that Anthropic could declare all such equity tokens void with a single board announcement, is enough to prove that the stability of this investment channel entirely depends on the weakest link in the chain. Just as the SpaceX incident demonstrated, if the entire chain cannot match real underlying stocks, the so-called investment channel becomes meaningless. The core demand should be to balance global investment channels with complete statutory ownership, allowing investors not to have to choose one over the other.

This is the complete picture of the matter. Today, the vast majority of so-called "tokenized stocks" in the industry merely replace the debt claims issued in 1973 with a blockchain database to house them. The truly applicable technologies that can achieve direct rights assertion already exist, and some teams have put them into practice, but the remaining participants in the industry have chosen to transition to being a new generation of intermediaries - after all, the substantial profits lie within the intermediary business.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。