Author: David Christopher, Bankless Analyst

Compiled by: Yuliya, PANews

Editor's Note: This article provides an in-depth analysis of the severe financial challenges currently facing Strategy, a company under Michael Saylor. The company’s operating system relies heavily on three pillars: Bitcoin, MSTR common stock, and STRC preferred stock, all of which are currently weakening simultaneously. As the pressure to pay preferred stock dividends increases and cash reserves continue to dwindle, Strategy finds itself in a dilemma: should it continue to bear the cost of diluting its stock or break from tradition and sell its prized Bitcoin reserves? Here is the detailed translation:

Today, Strategy, led by Michael Saylor, is experiencing its most severe crisis:

Its STRC preferred shares have fallen to around $80, marking the largest historical discount relative to its $100 par value;

The price of MSTR shares has also continued to decline, falling below the $100 mark for the first time since March 2024;

At the same time, the price of Bitcoin has also dropped below $60,000.

This crisis did not arise suddenly, but has been brewing since late May. At that time, Strategy repurchased debt and sold a nominal amount of Bitcoin to pay preferred stock dividends, and despite cracks appearing in market confidence in STRC, it still chose to continue buying Bitcoin.

It can be said that today is the moment when all warning signals have converged.

The Three Pillars that Keep This Machine Running

Strategy's structure is composed of three interdependent parts:

Bitcoin as Reserve Asset: It is the third-largest asset globally, marketed on the premise of “only going up.” However, Bitcoin itself does not generate any output, dividends, interest, or revenue. While Strategy can hold it indefinitely, dividends on preferred stocks must be paid in cash, necessitating some mechanism to bridge this funding gap. Today, the mismatch between assets and income is undergoing severe scrutiny.

MSTR Common Stock as Core Engine: When MSTR’s stock price becomes worth more than its underlying Bitcoin, Strategy can issue more stock to purchase additional Bitcoin, and this premium allows the buying behavior to add value to the company. However, once MSTR's stock price declines, the costs of this strategy increase. Raising $500 million at a stock price of $500 requires issuing 1 million shares; if the stock price drops to $50, 10 million shares must be issued. The same capital, but with ten times the dilution of equity, undoubtedly greatly weakens investors' reasons to hold MSTR.

STRC Preferred Stock as Credit Pillar: This is a preferred share with a face value of $100 that pays an 11.5% cash dividend. When the price drops, Strategy can attract buyers by raising the dividend rate. However, for this mechanism to work, investors must believe that dividends will be paid continuously, and currently, the “shelf life” of that trust is shortening. The current price of STRC hovers around $80, which signals the market saying: “If you want us to consider it as a $100 asset, you have to offer much higher returns.”

These three parts support each other—if one suffers, all suffer. When they all weaken simultaneously, the focus of attention shifts from “How much Bitcoin does Strategy actually have?” to “Does it have enough cash to meet its dividend commitments?”

The Current Predicament

Now, Strategy is simultaneously losing “trust” and “liquidity,” and these two are madly harming each other.

As Bitcoin declines, MSTR often suffers even greater losses because the market views it as leveraged Bitcoin. The drop in MSTR's stock price has made it more difficult to raise cash through stock sales, pushing all funding pressure onto the reserve assets.

Reports indicate that STRC's annual dividend bill has skyrocketed from around $300 million in January to approximately $1.2 billion now, while the company's cash reserves have drastically shrunk due to debt buybacks and Bitcoin purchases. The funding turnover period necessary to maintain these dividend payments has plummeted from over seven years to about 14 months.

This is the predicament the company currently finds itself in. While there is no lack of options, each option comes at a heavy cost:

Continue buying Bitcoin: This will further deplete cash reserves, thereby weakening market trust in STRC.

Issue more MSTR common stock: This means more severe equity dilution, which will diminish investors' motivation to hold MSTR.

Issue more preferred stock: This will increase dividend payment obligations, and raising the STRC dividend rate will only lead to deeper cash outflows.

Stop paying dividends: Absolutely not feasible, as this would completely destroy trust and lead to the collapse of the entire system. Since the entire structure relies on this, in the end, there seems to be only one path left: sell Bitcoin.

Why Selling Bitcoin Is a Double-Edged Sword?

Selling Bitcoin can quickly replenish cash reserves. Strategy can use this money to pay dividends, or even buy back STRC below par, redeeming $100 bonds at about $82. From a financial statement perspective, this is very reasonable. The analysis company CryptoQuant points out that to restore a 24-month funding turnover period, Strategy needs approximately $2.8 billion, which is about $1.4 billion more than its current reserves.

However, this implies that a massive amount of Bitcoin will need to be sold.

In fact, Strategy has already tested this dangerous edge. On June 1, the company announced it sold only 32 Bitcoin (worth about $2.5 million), which is just a rounding error for its total holding of over 840,000 Bitcoin. But since then, MSTR's stock price has plummeted by about 38%.

Investors are willing to hold MSTR precisely because the company almost never sells its assets. This was meant to be a levered, long-term bet that continuously hoards Bitcoin in the treasury. However, the moment Strategy began selling Bitcoin to pay for its preferred stock dividends, its treasury ceased to be sacrosanct and transformed into a source of funding to maintain the upper structure's operations. This fundamentally altered expectations about future capital shortages: if selling $2.5 million is acceptable, then larger-scale sales are naturally no longer far-fetched.

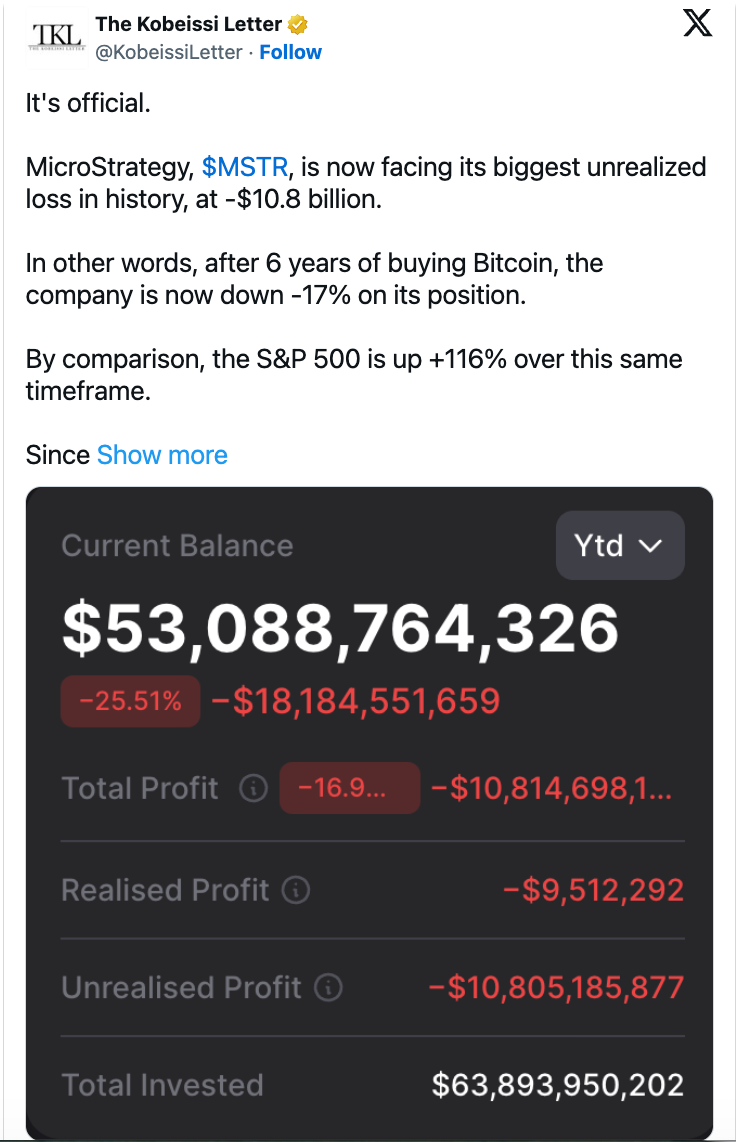

Additionally, selling Bitcoin now will turn paper losses into actual losses. CryptoQuant estimates that on Bitcoin purchased between 2024 and 2026, Strategy is currently facing an unrealized loss of about $10.6 billion. If held, these losses would remain theoretical; but if sold at current price levels, the losses would be completely locked in. However, this cleanest and most straightforward solution would also be the action that most affirms market panic.

It should be clarified that this does not mean Saylor will empty all his chips tomorrow.

Strategy still has cash on hand, can still issue more stock or increase STRC dividends, and Bitcoin still has the potential to rebound. Thus, this machine is not yet completely out of order today.

However, the road ahead is clearly becoming darker. Looking back at a series of operations since late May: debt buybacks, symbolic sales, issuing more stock, continuing to buy Bitcoin, while STRC remains in decline. All signs indicate that this structure has exhausted its means of coping with the crisis easily.

Looking on the bright side: If Bitcoin skyrockets, MSTR's stock price will rebound, STRC's yield will attract buyers again, and the entire flywheel will start spinning quickly once more. However, if a structure must rely on diluting equity, increasing dividends, or selling Bitcoin to maintain investor trust, then it has effectively lost its former brilliance.

Looking on the dark side: Although Strategy bought time through issuance and buying more Bitcoin, the dividend bill is accumulating at compound interest. The most obvious self-rescue method is really “stop buying immediately and save some cash,” but this would undoubtedly stifle the only engine supporting the entire company’s narrative.

This is the dilemma Saylor finds himself in:

If he sells Bitcoin, he will personally destroy the grand narrative of "permanent accumulation" that has allowed MSTR to achieve its current success;

If he refuses to sell, all pressure will concentrate on equity dilution, dividend payments, and cash reserves.

Both paths are challenging and can severely impact market confidence in Strategy, and even affect treasury companies built on the same principles.

However, sometimes the most painful path forward is the one that must be taken. Hopefully, a better situation will eventually come.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。