Author: Zach Pandl (Head of Grayscale Research)

Translation: Shenchao TechFlow

Shenchao's Guide: Grayscale Research released its latest report, listing the top 15 on-chain protocols by revenue and comparing their valuation multiples. The core finding is: a large number of protocols generating hundreds of millions in annual revenue are trading at single-digit revenue multiples or even at 1x revenue, with Pump.fun, PancakeSwap, and Meteora having market capitalizations nearly equal to one year’s revenue. Grayscale believes the CLARITY Act may pass next month, opening the door for institutional funds to enter these DeFi financial protocols. However, it should be noted that Grayscale itself is a crypto asset management company; the conclusion of "undervaluation" aligns with its business interests, and investors should make independent judgments.

After a long bear market, many revenue-generating on-chain applications appear quite cheap from a fundamental perspective.

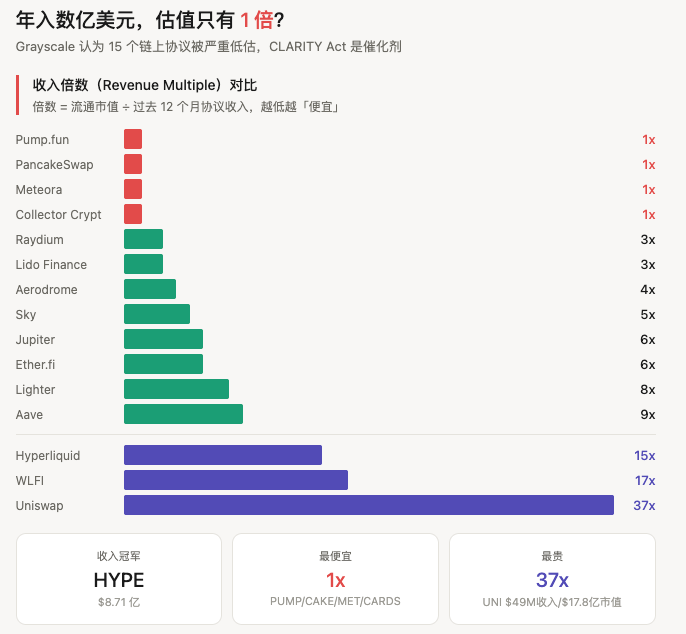

The top 15 on-chain protocols by revenue (including Hyperliquid) have seen most of their revenue multiples over the past 12 months drop to single digits, with many even at just 1x. Since most protocols have low operational costs, when measured by profit or cash flow, they also appear equally cheap.

Grayscale believes that the potential passage of the CLARITY Act (which could happen as early as next month) will help unlock this value. The reason is: if this law is implemented, it will bring the regulatory framework of traditional finance into cryptocurrency assets, which is a significant benefit for these applications.

Specifically, the CLARITY Act will promote the growth of tokenized assets and on-chain finance. Almost all of the top 15 protocols by revenue are tied to financial use cases or closely related infrastructure (such as oracle and staking). Grayscale believes these protocols will significantly benefit from the expected increase in on-chain trading activities following the passage of the CLARITY Act.

Grayscale's "Bargain List": A Look at 15 Protocols One by One

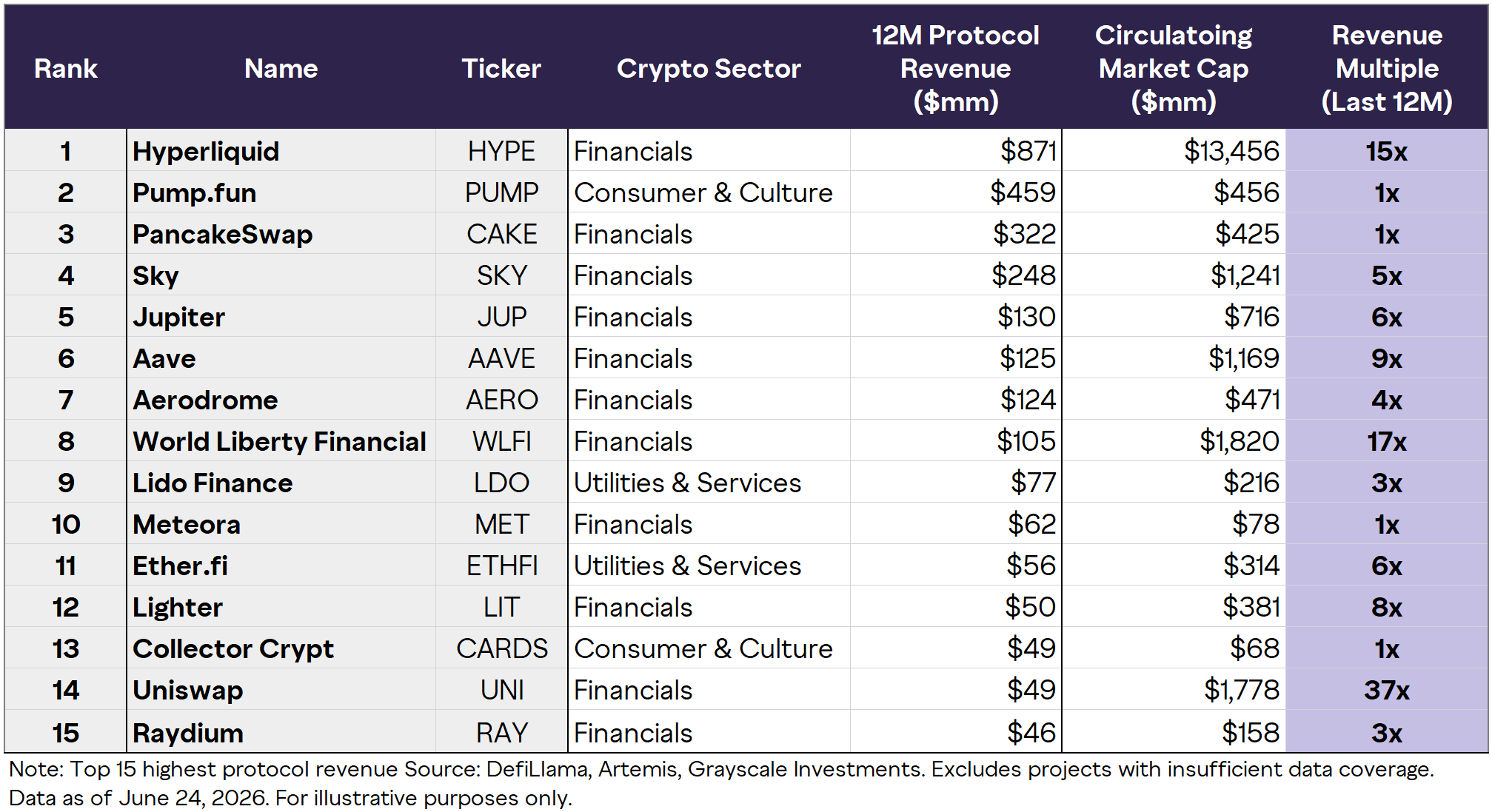

Caption: Ranking of the top 15 on-chain protocols by revenue. Data is as of June 24, 2026. Source: DefiLlama, Artemis, Grayscale Investments. Excludes projects with insufficient data coverage. Chainlink is not included due to having both on-chain and off-chain revenues.

This table is densely packed with information, and the following breakdown presents it layer by layer.

"1x Club": Market Cap ≈ One Year Revenue

The most notable item in the table is the four protocols with a Revenue Multiple of only 1x:

Pump.fun (PUMP) — Revenue of $459 million in the past 12 months, circulating market cap of $456 million. A software business with nearly $500 million in annual revenue and almost no operating costs has a market cap equal to one year’s revenue, which would immediately attract the attention of value investors in traditional markets. However, Pump.fun's revenue is highly dependent on meme coin speculation, and when sentiment shifts, this volume may evaporate in an instant. The 1x valuation may indicate that the market has overlooked genuine cash flow, or it may reflect the market correctly discounting unsustainable revenue.

PancakeSwap (CAKE) — $322 million in revenue, $425 million market cap, 1x. The largest DEX on the BNB Chain, with business spread across AMM trading, liquidity mining, prediction markets, etc., and a more diversified revenue source than Pump.fun, with a solid user base in the Asia-Pacific region.

Meteora (MET) — $62 million in revenue, $78 million market cap, 1x. A liquidity infrastructure on Solana, and a project co-founded by Jupiter's creator Meow. Attention is needed due to the team risks arising from the resignation of Meteora's co-founder Ben Chow due to financial misconduct allegations.

Collector Crypt (CARDS) — $49 million in revenue, $68 million market cap, 1x. Represents the "consumption and culture" sector, with the least recognition among the 15 protocols.

Middle Tier: Single-Digit Multiples, Solid DeFi Protocols

Raydium (RAY) — $46 million in revenue, $158 million market cap, 3x. A core AMM on Solana, benefitting from trading activity and new token issuance within the Solana ecosystem.

Lido Finance (LDO) — $77 million in revenue, $216 million market cap, 3x. The largest liquid staking protocol on Ethereum, representing on-chain staking infrastructure in the "tools and services" category.

Aerodrome (AERO) — $124 million in revenue, $471 million market cap, 4x. The largest DEX by TVL and trading volume on the Base chain, utilizing a ve(3,3) token economics model with concentrated liquidity, serving as a liquidity hub for the Coinbase L2 ecosystem.

Sky (SKY) — $248 million in revenue, $1.241 billion market cap, 5x. Formerly known as MakerDAO, an on-chain lending and stablecoin protocol.

Jupiter (JUP) — $130 million in revenue, $716 million market cap, 6x. The largest DEX aggregator on Solana, recently surpassing Uniswap and PancakeSwap in daily transaction fees multiple times.

Ether.fi (ETHFI) — $56 million in revenue, $314 million market cap, 6x. A representative protocol in the re-staking sector.

Lighter (LIT) — $50 million in revenue, $381 million market cap, 8x.

Aave (AAVE) — $125 million in revenue, $1.169 billion market cap, 9x. The largest lending protocol on-chain, Grayscale conducted a detailed DCF (Discounted Cash Flow) analysis of AAVE in another report, representing a methodological breakthrough in the crypto industry, as detailed later.

High Multiples Area: Paying for Narrative and Option Value

Hyperliquid (HYPE) — $871 million in revenue, leading the list, with a circulating market cap of $13.456 billion, 15x. Revenue scale far exceeds the second place, but the valuation multiple is also not low. The story of Hyperliquid is not just about perpetual contract exchanges: The HIP-3 proposal launched in October 2025 allows third parties to deploy perpetual contract markets on Hyperliquid without permission, expanding the underlying instruments to stocks, commodities, indices, and Pre-IPO stocks. In March of this year, S&P Dow Jones Indices authorized a HIP-3 deployer for the S&P 500 Index, creating the first S&P 500 perpetual contract product. The peak open interest in the HIP-3 market reached $3.2 billion, with a cumulative transaction volume of about $200 billion. 99% of protocol fees flow back to the protocol through buybacks. Grayscale has launched a Nasdaq-listed staking ETF (HYPG) for HYPE.

World Liberty Financial (WLFI) — $105 million in revenue, $1.82 billion market cap, 17x. Valuation is clearly high, reflecting more of its political connections with the Trump family and market visibility rather than fundamental output.

Uniswap (UNI) — $49 million in revenue, $1.778 billion market cap, 37x. Despite being second to last in revenue ranking, its valuation multiple is the highest in the table. This reflects a long-standing structural issue: the premium paid by UNI holders is primarily for governance rights and optionality on the "fee switch" (distributing protocol revenue to token holders), rather than current cash flows. The market is pricing UNI based on "what it could become" rather than "what it is now."

CLARITY Act: The Catalyst for These Protocols

Grayscale's argument is not just that "these protocols are cheap," but rather that "they are cheap before a regulatory catalyst arrives."

Out of the 15 protocols in the table, 12 are financial protocols: decentralized exchanges, lending platforms, liquid staking, yield infrastructure. The CLARITY Act (formally known as the Digital Asset Market Clarity Act) specifically targets these financial use cases with its regulatory framework.

The core of this law is to clarify the jurisdictional boundaries between the SEC and CFTC, establishing a framework that differentiates "investment contracts" from "digital goods." It has passed the Senate Banking Committee by a vote of 15:9 (with 2 votes from Democrats), and Polymarket gives a 67% probability of it passing this year.

The logic chain is simple: clear regulatory rules → reduced compliance friction for institutions → growth in on-chain activities and TVL → increase in revenues for these protocols → current low valuation multiples being re-priced.

[Supplementary Translation] Grayscale's DCF Valuation of AAVE: One-Year Target Price of $175

The following content is derived from Grayscale's mid-June report "Guide to Buying the Dip: Valuing Crypto with Cash Flows," and does not belong to the original text of this article, but is supplemented and integrated by the translator.

Grayscale places crypto assets on a valuation spectrum: at one end are pure commodity-type assets like Bitcoin, priced based on supply and demand; at the other end are protocols like Hyperliquid and Aave with substantial revenue, suitable for traditional Discounted Cash Flow (DCF) models.

Framework for analyzing Aave:

Aave Labs essentially functions like a permissionless on-chain bank, earning the spread between depositors and borrowers, plus fees and stablecoin (GHO) income. Grayscale estimates Aave's protocol profit in 2026 to be about $60 million, with an operating profit margin of around 50%.

Using comparable valuation multiples from fintech companies (20-25x price-to-earnings ratio), AAVE's fair value is estimated to be around $80-100, while the trading price at the time of the report's publication was about $75. AAVE's current forward P/E ratio is about 18x, lower than comparable fintech companies.

Under the baseline scenario (accelerated token adoption and regulatory clarity), Grayscale gives a one-year target price of approximately $175, representing an upside of about 130% from current levels.

Several unique challenges in valuing crypto protocols are not covered by traditional tools:

Token value return mechanisms vary — Buybacks (AAVE), token burns (HYPE), fee refunds (CoW), staking rewards (CRV), each mechanism has different efficiencies in conveying values to holders.

Special expenditure items — including supply-side costs (paid to liquidity providers), token emissions (ongoing inflation dilution), and capital expenditures by DAOs.

Legal structure uncertainties — Holding governance tokens typically does not imply legally enforceable rights to protocol assets. Different DAOs use various legal frameworks to align protocol operations with applicable laws.

[Supplementary Translation] Macro Background: Market Differentiation Since the War with Iran

The following content is from Grayscale's concurrent weekly report, providing a macro context.

Since the outbreak of the Iran War at the end of February, the U.S. stock market has risen 9% (boosted by AI spending), while Bitcoin has dropped 1% and gold has fallen 20%. Part of the reason for BTC and gold underperformance is the market's expectation that the Federal Reserve may raise interest rates to combat inflation — the one-year expected federal funds rate has risen by about 60 basis points, with about half of Federal Reserve officials believing that raising rates in 2026 may be appropriate. The European Central Bank has already raised rates.

Grayscale disagrees with this expectation, with the baseline scenario being that the Federal Reserve remains steady. If this assessment is correct, BTC price may catch up to the stock market.

In this risk-off macro environment, the valuations of on-chain protocols have been further compressed, which also serves as a time window for Grayscale's argument of "bear market multiples + regulatory catalyst."

How to View This Report Objectively

The picture painted by Grayscale is indeed worthy of attention: high-margin protocols trading at compressed valuation multiples, a possible regulatory tailwind on the horizon, while the overall market remains in a risk-off state. This is a rare investment thesis based on fundamentals in a market that is typically driven by sentiment.

However, two things must be made clear:

First, the catalyst is conditional. The timeline and final shape of the CLARITY Act are not guaranteed. An investment thesis based on a legislative event naturally carries the risk of that event occurring late or being disappointing. A 67% probability of passage also implies a 33% probability of failure.

Second, Grayscale is a stakeholder. It is a crypto asset management company whose business model is built on increasing investor exposure to these assets. It has already launched a Nasdaq-listed staking ETF for Hyperliquid. Its conclusion that "now is an attractive entry point" should be read in this context of interest rather than as neutral analysis.

Valuation data is verifiable, and anomalies are real. However, whether this signifies a bottom or if the market is correctly pricing perceived risks is a question each investor must answer for themselves.

For those tracking the CLARITY Act, the signal to watch is not just whether the bill itself passes, but whether institutional funds truly flow into these protocols in the weeks following its passage — that will be the true validation of Grayscale's argument.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。