Introduction

In the past few years, DAT Company, represented by Strategy, has constructed a typical "coin-stock flywheel" model: continuously financing through capital market tools such as stocks, convertible bonds, and preferred shares, and using the funds to purchase cryptocurrencies like BTC and ETH. As the holdings continue to increase, the market further strengthens its asset exposure and narrative premium, thereby raising stock prices and enhancing financing capabilities, forming a positive reflexive cycle, making it one of the important marginal buyers in the cryptocurrency market.

However, this model is currently undergoing a stress test in the current market environment. As of June 25, the trading price of Strategy's preferred stock STRC has fallen below $80, down more than 20% from the $100 target par value, while significant unrealized losses have emerged in its BTC holdings. Under the dual influence of declining coin prices and contracting capital market premiums, the financing ability of the DAT model begins to be challenged. Not only is Strategy facing balance sheet pressures, but other DAT companies with BTC/ETH as their core assets are also undergoing systemic stress tests brought about by the "flywheel reversal".

1. The Essence of DAT: From Asset Holdings to Financing-Driven Valuation System

The essence of DAT lies not in simple cryptocurrency holdings but in how it is structurally priced by the capital market and transformed into an asset expansion mechanism driven by continuous financing capabilities.

1.1 The Essence of DAT: The "Listing Packaging" of Cryptocurrencies

DAT (Digital Asset Treasury) refers to the structure of listed companies or quasi-listed entities that continuously finance through equity, bonds, and other capital market tools, focusing the raised funds on managing assets in cryptocurrencies like BTC and ETH.

In this structure, the company's valuation anchor shifts from traditional business cash flow to "holdings size + financing ability + market narrative." In other words, DAT essentially provides a way to "trade cryptocurrency beta in the stock market."

Strategy is the starting point of this model. After transforming from a software company to a BTC treasury company, the market gradually abandoned its traditional pricing logic for its business and began to view it as the "listing agent for BTC."

1.2 Why the Market is Willing to Pay a Premium for DAT

The establishment of DAT is essentially because it meets the structural demands of three types of capital.

The first type is traditional funds that cannot directly hold coins, such as pension funds, mutual funds, or securities account users. These funds gain BTC/ETH exposure through the stock market, which has a lower threshold and is more compliant than on-chain or exchange routes.

The second type is funds requiring leverage. DAT stocks essentially provide a combination exposure of "cryptocurrency + financing leverage." When the company continuously buys coins with external capital, the corresponding cryptocurrency exposure per share is amplified.

The third type is demand from indices and institutional allocations. Stocks can enter indices, options, and margin systems to gain passive capital allocation, while direct coin holdings cannot enter this system.

Therefore, the market is willing to pay a premium for DAT, essentially paying for "financeable cryptocurrency packaging structures," rather than simply for the BTC or ETH it currently holds.

1.3 mNAV: The Core Variable for DAT Pricing

The core pricing mechanism of DAT can be abstracted as the mNAV (market net asset value) system, which is the multiple of the company's market value relative to the net value of its held cryptocurrencies. mNAV essentially determines the boundary of DAT's financing capability, namely how much premium the market is willing to pay for "every $1 cryptocurrency exposure."

When mNAV > 1, it indicates that the market is willing to pay a premium for "future financing capabilities + continuous buying capacity";

When mNAV ≈ 1, the market only views it as a passive cryptocurrency holding tool;

When mNAV < 1, it means the market begins to question its capital structure and continuous financing capabilities.

The key to the DAT model lies here. It is not simply "the company buying coins," but "the company using stock market premiums to buy coins." As long as the market gives DAT companies a premium, they can buy more cryptocurrency with relatively cheap capital and attempt to increase the per share coin holding. As long as this process continues, the market will believe that stocks are more resilient than direct coin holdings.

However, this model has an implied prerequisite: the market must continue to believe the company can still finance in the future. Once mNAV shrinks, the financing capability will decline; when financing capability decreases, the speed of new coin purchases will slow down; when new coin purchases slow down, the market will lower expectations for the company's future coin growth. This marks the starting point for the DAT model's transition from a positive flywheel to reverse pressure.

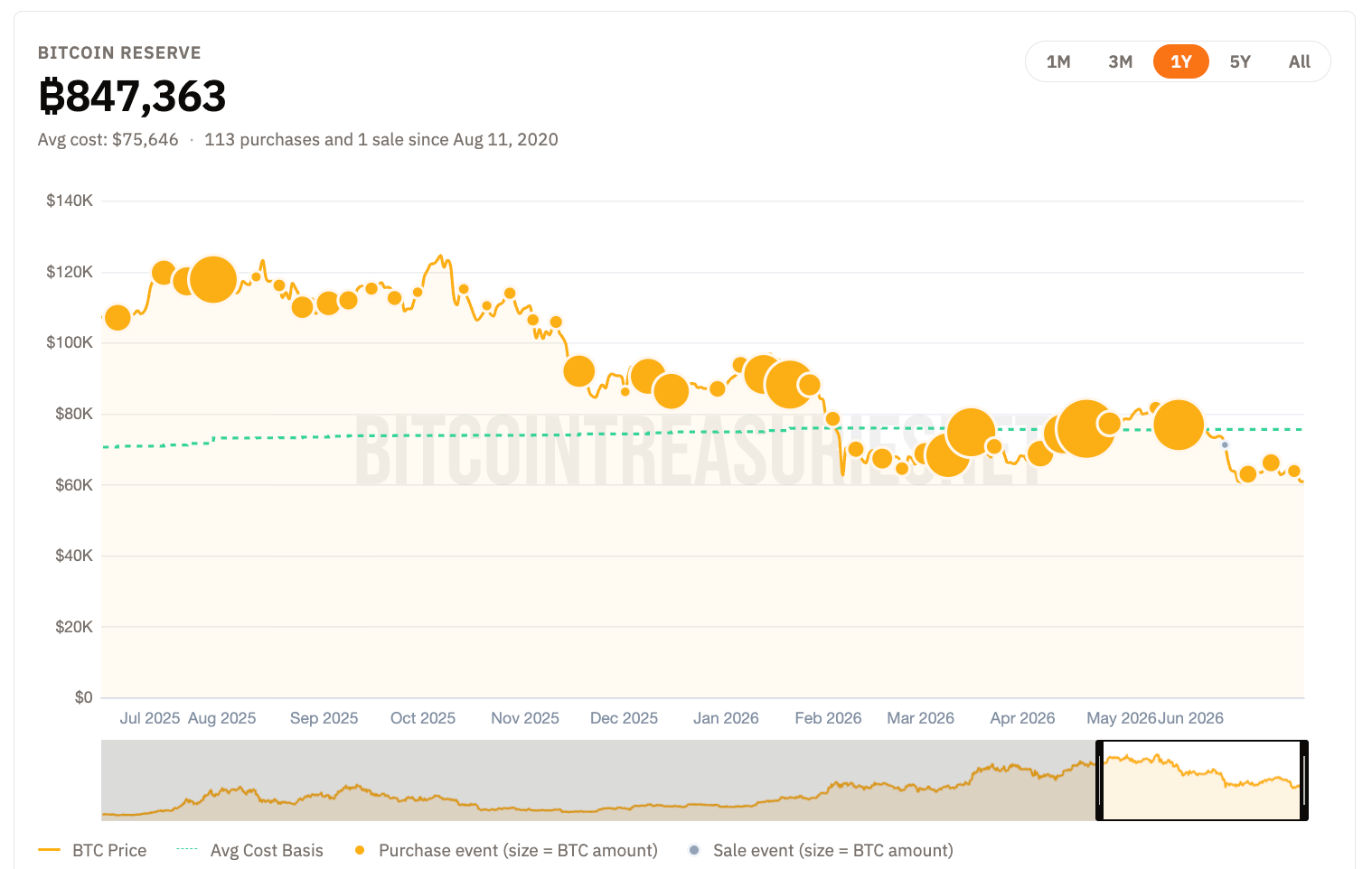

As shown in the figure below, Strategy’s mNAV multiplier has declined from approximately 2x over the past year to 0.7x, falling below the theoretical par level of 1x. This change indicates that the market's pricing logic for its "cryptocurrency holding premium" is undergoing a systemic reassessment, shifting from premium-driven financing to discounted trading.

Source: https://bitcointreasuries.net/public-companies/strategy

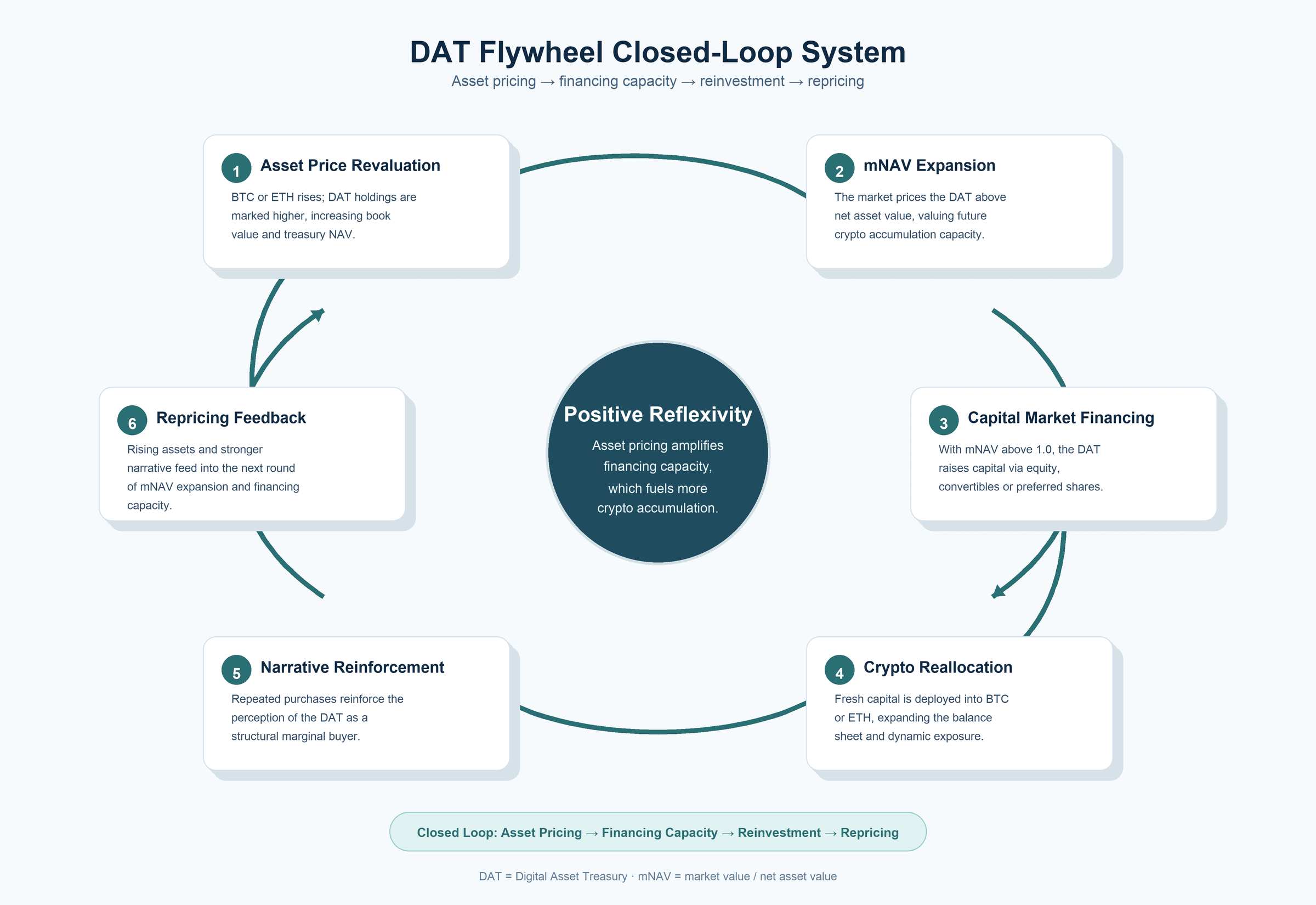

2. The Coin-Stock Flywheel Mechanism: A Structural Positive Feedback Model of DAT

The DAT flywheel is not a single price logic, but a structural positive feedback system jointly driven by asset revaluation, financing capabilities, and market expectations.

2.1 Core Links of the DAT Flywheel: A Closed System from Assets to Financing

The DAT flywheel is not a single pricing logic, but a six-part cyclical system driven by both the capital market and cryptocurrency, sustained by the continuous reinforcement of "asset pricing → financing ability → re-buying → re-pricing."

The first link is asset price revaluation. When BTC or ETH rises, the book value of DAT's holdings rises simultaneously, directly pushing up the company's net asset level. This stage is essentially passive revaluation, but it determines the subsequent opening of financing space.

The second link is mNAV expansion. As the market begins to give DAT companies a valuation multiple above their net assets, the stock price displays a premium relative to underlying assets. This premium essentially reflects the market's pricing for its "continuous buying ability," rather than just stock assets.

The third link is the release of capital market financing capabilities. Under the condition of mNAV > 1, DAT can engage in low-friction financing through equity, convertible bonds, or preferred shares, converting market premiums into real capital inflow. This stage marks the onset of self-driven flywheel capabilities.

The fourth link is the reallocation of cryptocurrency assets. DAT continues to invest the proceeds from financing into BTC or ETH, thus expanding the balance sheet size, making its holdings not merely static exposures but dynamic exposures that continue to grow.

The fifth link is the strengthening of market narratives. Ongoing coin-buying actions will reinforce the market's recognition of its "perpetual buying power," further positioning DAT as a structural marginal buyer, thus supporting its valuation premium.

The sixth link is re-pricing feedback. Asset price increases and narrative strengthening jointly prompt the next round of mNAV expansion, forming a positive closed loop. At this point, DAT completes its transformation from "asset holder" to "capital market cryptocurrency amplifier."

2.2 Interpreting the STRC Flywheel: Strategy's Multi-Layer Capital Structure

The uniqueness of Strategy lies in its multi-layer capital structure. Ordinary shares MSTR target investors who are more risk-tolerant and willing to accept stock price volatility; convertible bonds target those seeking debt protection and potential equity upside; and preferred shares like STRC, STRD, STRF, STRK, etc., target investors seeking high-yield cash flows.

STRC is a perpetual preferred stock, aiming to trade around a par value of $100 and attracting investors through an adjustable dividend rate. Theoretically, when the market price of STRC falls below the target par value, Strategy can increase the dividend rate to enhance its attractiveness; when the price returns to near or above par value, the company can continue issuing STRC through an ATM mechanism to raise funds to buy BTC. This makes STRC one of the financing engines in Strategy's flywheel. Compared to ordinary shares, preferred shares typically do not directly dilute ordinary shareholders' voting rights and do not require repayment like bonds. For Strategy, if STRC can stabilize around $100, it can continuously obtain funds through the issuance of preferred shares for purchasing BTC.

However, the cost of STRC does not disappear but continues to exist in the form of dividends. Currently, Strategy has approximately $15 billion in preferred shares, with STRC accounting for about $9 billion; the annual dividend payment obligation for preferred shares is about $1.7 billion. In other words, the asset side of Strategy mainly comprises non-interest-bearing BTC, while the liabilities/liability-like side entails continuous cash payment obligations.

This is precisely the source of the flywheel's fragility. The further STRC is from the $100 target par value, the higher the risk compensation required by the market. The more the dividend rate is adjusted upwards, the more Strategy must use higher financing costs to maintain cash inflow. If STRC remains below par value for a long time, Strategy's ability to issue STRC to buy coins will decline because issuing at a discount will harm financing efficiency and further strengthen market concerns about its capital structure. This also demonstrates that the core fuel for the DAT flywheel is not BTC itself, but the willingness of the capital market to believe that BTC will rise in the future and the willingness to finance that belief with current funds.

3. Flywheel Reversal Case: From Financing Tool to Risk Trigger

When financing capability and asset prices are simultaneously under pressure, the positive feedback structure of DAT will begin to fail and gradually shift to a path of reflexive contraction.

3.1 STRC: The Breakage of the Financing Flywheel and Credit Repricing

As a core preferred stock financing tool in Strategy's multi-layer capital structure, STRC supports continued issuance and low-cost financing capabilities. During the smooth phase of the flywheel, this mechanism makes STRC a critical channel connecting the capital market and BTC buying demand.

However, recently the price of STRC has persistently fallen below the target par value range, dipping below $80 at one point, which represents a discount of over 20% from the $100 target par value. This change essentially indicates that the market has begun to reprice its risk compensation structure, no longer viewing it as a "stable financing tool." Currently, Strategy's total holdings have reached 847,363 BTC, with an average cost of approximately $75,651. Based on the spot price of BTC at $61,956 on June 25, its BTC holdings show an unrealized loss of about $11.6 billion.

Source: https://bitcointreasuries.net/public-companies/strategy

The decline in prices of preferred shares like STRC compresses new financing space primarily by raising actual financing costs, and it also reduces the market's expectations for "continuous expansion capability," directly compressing the mNAV premium. When mNAV expectations shrink, the financing ability and asset buying power of DAT decline simultaneously, forming a negative feedback chain of "financing contraction → reduced buying → asset price decline."

3.2 BitMine: The Shrinkage of Revenue-Generating Assets Brings Pressure on the Asset Side

If STRC represents "pressure on the financing side," then BitMine represents "pressure on the asset side." BitMine has a structure similar to Strategy, but its underlying assets shift from BTC to ETH, complicating its risk structure. ETH has staking yields, DeFi participation capabilities, and ecological expansion attributes, theoretically providing an "internal source of revenue." However, it also adds risks such as smart contract risks, liquidity risks, staking lock-in risks, and protocol-level uncertainties. Therefore, the ETH treasury is not merely an "upgraded version of the BTC treasury," but a more complex asset structure with multidimensional risks. In upward cycles, this structure is priced as a "revenue enhancer," but during volatile cycles, it is re-priced as a "risk amplifier."

Currently, BitMine holds 5,672,956 ETH, accounting for about 4.7% of the total ETH supply, making it the largest corporate treasury of ETH globally. Its average cost is about $3,513, and based on the price of ETH at approximately $1,653 on June 25, the current unrealized loss of BitMine's ETH holdings is about $10.5 billion.

The core issue for BitMine is not merely whether it holds ETH, but whether it can continuously generate "additional value beyond holding coins." If the market believes its earning capacity is limited, then BitMine will face structural compression in its valuation: reverting from an "actively managed asset vehicle" to a "passive ETH exposure tool," or even converging towards a closed-end fund discount. When the price of ETH declines, this issue will be further amplified: unrealized losses combined with revenue uncertainty prompt the market to reassess the necessity of holding ETH in stock form.

STRC and BitMine reveal the same core issue from the financing and asset sides respectively: the risk of DAT is not a single-point problem, but a structural resonance risk. When this mechanism operates smoothly, it is manifested as a "structural buyer of continuous coin purchases"; when financing ability and asset prices simultaneously contract, DAT will transition from a "positive feedback flywheel" to a "negative feedback cycle": declining financing capability → reduced buying → weakened asset support → further contraction of financing premiums, ultimately forming a typical reflexive contracting path, switching the entire structure from an expansion logic to a defensive logic.

4. DAT Risk Reassessment: From Unrealized Losses to Structural Constraints

The risks of DAT do not stem from price volatility itself, but from the systematic constraints between its financing structure and balance sheet.

4.1 Cognitive Correction: DAT Risks Do Not Arise from Price Volatility

The risks of the DAT model are often misunderstood by outsiders as "the risk of cryptocurrency price volatility," but this understanding is not accurate. Both the rises and falls of BTC and ETH are merely triggering variables, not decisive factors.

The central problem for DAT is not the direction of asset prices, but whether its capital structure can continue to support the "financing—coin-buying—re-pricing" cycle. In other words, price volatility is merely an exogenous shock, while the true determinant of system stability is whether financing capability remains.

4.2 Dual Constraint Model: Structural Coupling of Asset Retreat × Financing Contraction

The risks of DAT arise from the simultaneous changes of two variables, rather than a single factor: on one hand, price retreats of BTC and ETH directly compress net asset value, causing mNAV to start shrinking; on the other hand, discounts on financing tools represented by STRC significantly raise financing costs and weaken continued expansion capabilities.

These two variables do not operate independently but are mutually reinforcing structural coupling relationships: falling asset prices weaken financing expectations, and financing contractions further reduce market buying, thereby further suppressing asset prices. Thus, what DAT faces is not linear risk but a structural problem of "both variables tightening simultaneously."

4.3 Pricing Mechanism Shift: Risk Narrative Transformation Triggered by mNAV Contraction

The market pricing of DAT is not static but highly dependent on changes in mNAV. When mNAV is in an expansion phase, the market is trading on "future financing capabilities," thus willing to give DAT companies a premium; but when mNAV begins to shrink, the market pricing logic undergoes an essential shift from "growth narrative" to "risk narrative."

The core triggering variable for this shift is not the price itself but changes in expectations regarding financing capabilities: when the market begins to question whether companies can still finance at low costs, its valuation anchors shift from "expansion capacity" to "asset safety margins."

4.4 Irreversible Transmission Mechanism: Closed-Loop Feedback from Financing Contraction to Liquidity Retreat

The systemic nature of DAT's risks lies in its self-reinforcing transmission path. A contraction on the financing side (such as STRC discounts) first weakens new coin-buying capabilities, leading to a decline in marginal market buying; decreased buying further suppresses asset price performance, causing mNAV to contract further; and mNAV contraction again exacerbates financing difficulties.

This process is not a simple linear transmission but a typical reflexive closed-loop system. Once into a contraction phase, the structure does not naturally revert to an expansion path but tends to continuously adjust downwards until it finds a new pricing equilibrium.

In summary, the core issue for DAT does not lie in what assets it holds, nor in the scale of short-term unrealized losses, but in whether it still possesses the structural capability to continuously generate liquidity. When financing capability persists, DAT is a "capital market cryptocurrency amplifier"; but when financing capability contracts, its structural attributes reverse and gradually evolve into a "passive liquidity consumer." Therefore, the essence of DAT is not a traditional investment target but a structural liquidity system with capital market financing capability as a core variable.

5. Future Direction: Cycle Differentiation and Structural Repricing for DAT

The future evolution of DAT will not progress in a single direction but will be jointly determined by two core variables:

One is mNAV, which determines whether the market remains willing to price for "expansion capabilities";

The other is the degree of openness of the financing window, which determines whether DAT can still continuously expand its balance sheet at low costs.

When mNAV is in the expansion range and the financing window is open, DAT enters a positive flywheel phase; when mNAV contracts but the financing window still exists, the system enters a fluctuation phase; and when both contract simultaneously, it enters a reverse contraction cycle. Thus, the essence of DAT is not a linear growth or decline model but a cyclical structural system driven by "capital market pricing willingness."

5.1 Scenario One: Flywheel Repair Path (Cycle Rebound Driven Re-expansion)

In the event of a periodic rebound in BTC/ETH, DAT's balance sheet will repair synchronously, and mNAV is expected to expand again, restoring financing capabilities.

In this scenario, preferred shares like STRC may return to the target par value range, financing costs decrease, and the capital market is again willing to pay a premium for "continuous buying ability."

The essence of this stage is not merely a price rebound, but a structural restart of "repairing financing expectations → returning capital premiums → restarting the flywheel."

5.2 Scenario Two: Low-Speed Operation Path (Structural Stabilization After mNAV Convergence)

If BTC/ETH enters a long-term fluctuation range, DAT may not experience severe contraction but will also find it difficult to re-enter a high-premium expansion cycle.

In this state, mNAV will gradually converge towards 1, company financing behavior will tend to be cautious, coin-buying pace will slow, and the asset structure will shift from an "expansion model" to a "stock management model."

DAT will gradually revert from a "capital market cryptocurrency amplifier" to a "cryptocurrency holding listed tool," and its valuation system will shift from growth premium to NAV logic.

5.3 Scenario Three: Reverse Flywheel Path (Financing Contraction and Structural Repricing)

When mNAV remains below 1 and the financing window contracts, DAT will enter a reverse flywheel phase.

In this stage, the decline in financing capabilities first weakens new coin-buying abilities, further reducing marginal demand in the market; under pressure, asset prices compress mNAV further, making financing conditions worsen, thus forming a typical reflexive contraction cycle.

It is important to emphasize that this process does not equate to "liquidation risk," but rather a process of "the capital market exiting the expansion logic": the market no longer rewards expansion behaviors but begins pricing the robustness of capital structures.

Conclusion: The Essence of DAT is "Cyclical Liquidity Structure"

In summary, the core of DAT is not a simple asset holding structure, but a financing—buying cycle system driven by mNAV. Its essence lies in transforming the capital market's valuation premium into the marginal buying source for the cryptocurrency market. In different cycles, this system may manifest as an expanding flywheel, low-speed operation, or reverse contraction, with the key variable always being the market's pricing change concerning "continuous financing capabilities."

Therefore, the so-called "end of the coin-stock myth" is not a black-and-white conclusion. A more accurate statement is: DAT is transitioning from a narrative-driven phase to a balance sheet phase. In the future, the market will reward not merely aggressive expansion but also the resilience of capital structures, financing discipline, cash reserves, transparent disclosures, and the ability to navigate across cycles.

About Us

Hotcoin Research, as the core investment research institution of the Hotcoin Exchange, is committed to transforming professional analysis into your practical tool. We analyze market trends for you through "Weekly Insights" and "In-Depth Research Reports"; leveraging the exclusive column "Hotcoin Select" (AI + expert dual screening), to secure potential assets and reduce trial-and-error costs. Every week, our researchers meet with you through live broadcasts to interpret heat topics and predict trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and grasp the value opportunities of Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investments carry risks. We strongly recommend that investors make investments only after fully understanding these risks and under a strict risk management framework to ensure the security of their funds.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。