Author: momo, ChainCatcher

In recent years, an interesting phenomenon has been occurring. On one side, traditional financial institutions are starting to embrace crypto assets, from Bitcoin ETFs to stablecoins to tokenized securities, more and more financial institutions are entering the Crypto world.

On the other side, crypto exchanges are continuously extending into traditional financial markets. Stocks, ETFs, prediction markets, RWAs, and other products are successively launched, and the once clearly defined two tracks are starting to move closer to each other.

Especially among crypto exchanges, the once crypto assets have become the away game, while stocks have become the competitive home game. Since last year, around the traditional financial business of "buying and selling stocks," leading crypto exchanges like Binance and Gate have made multiple attempts.

But stock services have always been the domain of traditional brokerages; why do crypto CEXs still have an opportunity to redo "buying and selling stocks"? As more platforms enter this track, what are the paths of differentiation?

1. Why can crypto CEXs redo "buying and selling stocks"?

In the past, the crypto industry attracted users from outside the circle, typically occurring during bull markets. The wealth effect brought by Bitcoin's rise and altcoin seasons has been the most important driving force for new users to enter the market.

However, this bear market has seen two noteworthy new phenomena: first, the crypto industry is still attracting users from outside the circle; second, after entering Crypto, these new users often do not trade crypto assets themselves.

During the severe fluctuations in oil prices in March this year, @smartestxyz recorded a metric - "Non-Crypto-First Users," referring to users whose first on-chain transaction was not cryptocurrency but rather RWA Perp products such as stock indices, gold, and oil, amounting to nearly 50,000 people. In other words, many users from outside the crypto world entered the crypto space not for Bitcoin but for traditional financial assets.

Why is this phenomenon occurring? One important reason is that there are indeed areas in traditional financial services that are not covered.

Especially in parts of Southeast Asia, Latin America, and Africa where financial infrastructure is relatively weak, these issues are often amplified.

Another reason is the generational turnover of trading users. Many new young users now experience crypto asset trading from the start, getting used to the efficiency of funds brought by 24/7 availability, stablecoin systems, and on-chain gameplay.

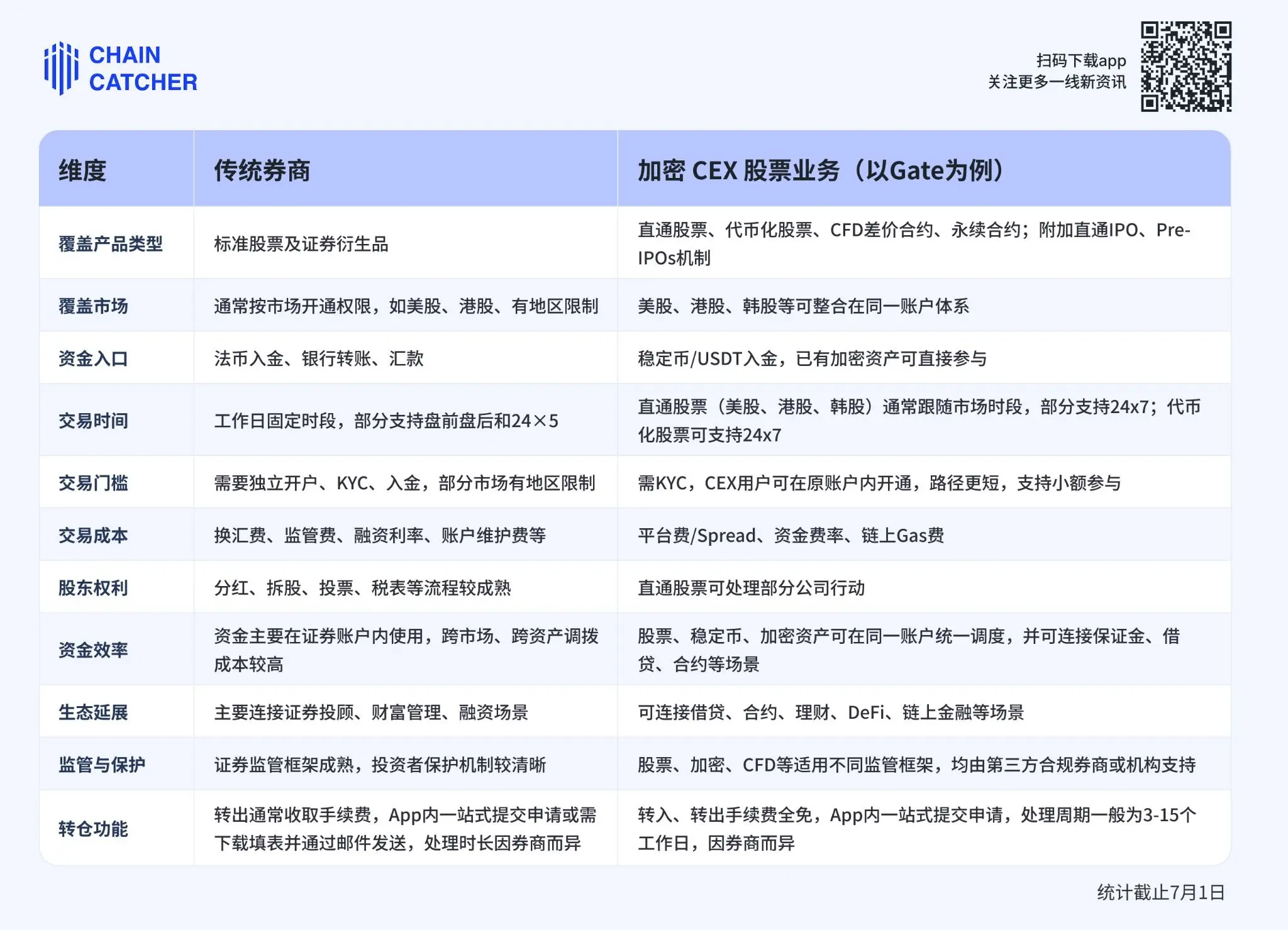

Specifically, we can compare the differences between traditional brokerages and crypto CEXs in the stock business. Currently, Gate, in terms of business model and product categories, is one of the more complete platforms, so this article uses Gate as a reference for the comparison.

First, let's look at a question most users care about: whether the underlying assets they purchase are indeed stocks.

In the past, the stock business of crypto CEXs mainly involved tokenized stocks and CFDs, where users primarily gained exposure to stock prices rather than the stocks themselves.

However, in the last year, this situation has begun to change. Platforms represented by Gate and Binance have successively launched direct stock trading models. For instance, Gate collaborates with licensed brokerage Alpaca Securities to provide execution, clearing, and custody services for stocks, allowing users to hold stocks and enjoy dividend payouts. In addition, Gate's functions like stock splits, consolidations, and stock transfers are now live.

This means that, from the perspective of asset supply, the gap between crypto CEXs and traditional brokerages is rapidly narrowing.

Under this premise, the real differences between the two are increasingly reflected in user experience and account systems.

First are the accessibility thresholds and trading times. Compared to traditional brokerages, which are restricted by trading hours, account opening processes, and regional limitations, crypto CEXs, relying on global accounts and stablecoin systems, offer more flexibility in accessibility. For example, in Gate's direct stock business, some stocks have already opened pre-market and after-hours trading, even 24x7 trading, while tokenized stocks provide longer trading hours, aligning more with crypto users' trading habits. At the same time, Gate's newly launched stock transfer function can also enhance users’ flexibility and convenience in managing stock assets.

It is worth mentioning that Gate's stock transfer function directly addresses users' pain points in asset transfers across brokerages and exchanges. As CEXs launch stock businesses, many users still hold positions with external brokerages, and if they want to switch platforms, they often have to sell first and then buy, which is both time-consuming and exposes them to price fluctuation risks.

Gate's transfer function supports transferring U.S. and Hong Kong stock holdings freely between Gate and external brokerages. In contrast to brokerages generally requiring transfer fees, Gate's transfer in and out is completely fee-free, truly achieving flexible cross-platform configuration of stock assets.

Of course, this type of model also needs to comply with relevant regulatory requirements and relies on licensed brokerages for asset custody, and its market acceptance still needs further observation.

Secondly, the unified account system brings about capital efficiency. Traditional brokerages are closer to having "one market corresponding to one account." When users participate in different markets such as U.S. and Hong Kong stocks, they usually need to separately enable access permissions, and capital flow relies on bank accounts, currency exchange, and cross-border remittance systems.

In contrast, crypto CEXs function more like "one account managing global assets." From launching U.S. stocks on June 1, 2026, to introducing Hong Kong stocks on June 11, and then launching Korean stocks on June 22, Gate integrated the three major global stock markets in less than a month, sharing a unified stock account system. Funds are settled uniformly through USDT. For users who already own crypto assets, they can complete asset allocation between different markets within their existing accounts without experiencing currency exchanges or cross-border remittances.

More importantly, under a single account system, stocks, stablecoins, and crypto assets can form the same liquidity pool, further connecting lending, wealth management, derivatives, Polymarket prediction markets, and other trading scenarios, covering mainstream derivatives such as spot, contracts, options, wealth management, lending, as well as traditional trading methods like CFDs and direct stock access, achieving comprehensive coverage of assets and trading tools within one account system, enhancing the efficiency of asset flow and reuse.

In addition, the product forms are also more diverse. Traditional brokerages mainly provide real stocks and some security derivatives, while crypto CEXs often offer multiple trading methods around the same underlying asset.

Besides direct stock trading, Gate has also diversified into tokenized stocks, CFDs, and perpetual stock contracts. For users who also have confidence in a company, those with different risk preferences and trading cycles can choose different products according to their needs, rather than being limited to a single stock trading method.

2. How does the stock business path of crypto CEXs differentiate?

After understanding some of the differentiators between traditional brokerages and crypto CEXs in stock, let's take a look at some of the internal path differentiations among crypto CEXs.

Currently, real stocks are no longer confined to a few platforms. Whether it's Binance or Gate, both have successively launched direct stock trading services and provided underlying securities execution and custody through licensed brokerage systems.

Simultaneously, all platforms also retain cryptonative products such as tokenized stocks and perpetual contracts, hoping to balance the investment attributes of real stocks with the all-time, low-threshold trading experience of the crypto market.

In terms of fees, platforms have also started to align with the low-fee model of traditional internet brokerages. Taking direct stock trading as an example, Gate has integrated a VIP level system where the lowest stock trading fee can be reduced to 0.023%, and there are no holding fees.

This means that the gap for crypto CEXs in "availability of stocks" and whether they can provide competitive advantages in crypto experience is narrowing. What truly begins to create differentiation is no longer whether stocks are available, but which markets are covered, which products are offered, and whether these products can be integrated into the same trading system.

From the leading platforms, each development path is also different. Binance tends to rely on its large global user base, gradually improving its real stock capabilities while integrating tokenized stocks to enrich trading scenarios; in contrast, Gate's layout emphasizes "multi-market coverage + multiple product paths + account unification," building a relatively complete global stock trading closed loop.

Currently, Gate has formed four product lines: real stocks, tokenized stocks, CFDs, and perpetual stocks, and covers three major securities markets: U.S. stocks, Hong Kong stocks, and Korean stocks, with additional functionalities like direct IPO (IPO Access) support, allowing new shares to be purchased directly, while Pre-IPO mechanisms allow for premature anchoring of valuation changes in unlisted companies, creating a complete investment chain from Pre-IPO to secondary markets.

Specifically, concerning U.S. stocks, Gate supports over 10,000 U.S. stocks and ETFs, covering mainstream U.S. trading markets such as the NYSE and Nasdaq, allowing users to hold real stocks and synchronize basic shareholder rights such as dividends.

In terms of Hong Kong stocks, Gate has become the first crypto trading platform in the industry to launch real Hong Kong stock spot trading, currently covering over 1,500 high liquidity stocks from the main board and growth enterprise market of the Hong Kong Stock Exchange, supporting fractional trading and sharing the same stock account system with U.S. stocks without needing to open an additional Hong Kong stock account.

Recently, with the Korean stock market's rising popularity, Gate has also exclusively launched the Korean stock market, now covering the top 1,000 listed companies in terms of market capitalization on the Korea Exchange (KRX), including key targets such as Samsung Electronics, SK Hynix, NAVER, and Hyundai Motors, also supporting fractional trading and included in unified stock account management.

Overall, Gate's approach is not to focus around a single market or product but aims to integrate the major global stock markets with various trading forms into the same account system.

3. From competing on products to competing on distribution, the logic of competition among exchanges has changed

Previously, we discussed why crypto CEXs began to engage in the stock business and how each is executing this business.

Looking at the longer perspective, this competition is no longer just among CEXs but is a competition across the entire trading platform industry.

A clear trend is that traditional brokerages and crypto exchanges are moving in the same direction. In the past year, in addition to stocks, Robinhood has launched crypto, prediction markets, and tokenized stocks; Nasdaq and NYSE are also advancing the tokenization of securities. On the other side, crypto exchanges continuously expand into assets like stocks, ETFs, precious metals, and prediction markets.

Both parties are entering each other’s home field, which reflects the changing logic of competition in trading platforms. In the past, crypto exchanges competed on product supply, where being the first to launch hot assets yielded more traffic. But as the altcoin season wanes, the number of quality assets that platforms can continuously create is decreasing, shifting the competition from "competing on products" to "competing on distribution." Whoever can integrate high-quality global assets faster and reach users with lower thresholds and higher efficiency will have more opportunities to retain users' wallets.

Currently, the development directions of each platform have begun to differentiate. Some platforms focus more on U.S. stock access, while others continue to strengthen the crypto-native experience; meanwhile, Gate seems clear in its intention to excel in global high-quality asset distribution.

On one hand, it continues to expand its asset coverage. It now supports over 12,500 stock assets, covering U.S. stocks, Hong Kong stocks, and Korean stocks while becoming the first crypto platform in the industry to launch real Hong Kong stock spot trading. On the other hand, it does not only provide one type of stock product but simultaneously lays out multiple product forms including real stocks, tokenized stocks, CFDs, and perpetual stocks, allowing users with different risk preferences and trading scenarios to find corresponding trading methods.

In other words, compared to simply increasing several stock access points, Gate focuses more on integrating as many quality assets and their corresponding trading paths into the same account system. If more real-world assets enter the blockchain in the future, this framework can continue to expand without needing to build a new set of product systems.

Perhaps in a few years, people will no longer deliberately differentiate between a platform as a "crypto exchange" or a "traditional brokerage." What truly determines competitiveness will be who can continuously connect global quality assets and distribute these assets to global users more efficiently.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。