Written by: Rita

Guide to Trends

Bloomberg recently quoted sources saying that Meta is planning a cloud computing business, covering model hosting APIs and bare metal computing capacity rental. Morgan Stanley's judgment on July 1 was direct; the part of the plan that involves renting idle computing power is far more reliable than a complete cloud service that competes with AWS, as the former does not require large-scale hiring and enterprise sales teams, while the execution risks for the latter are significantly higher.

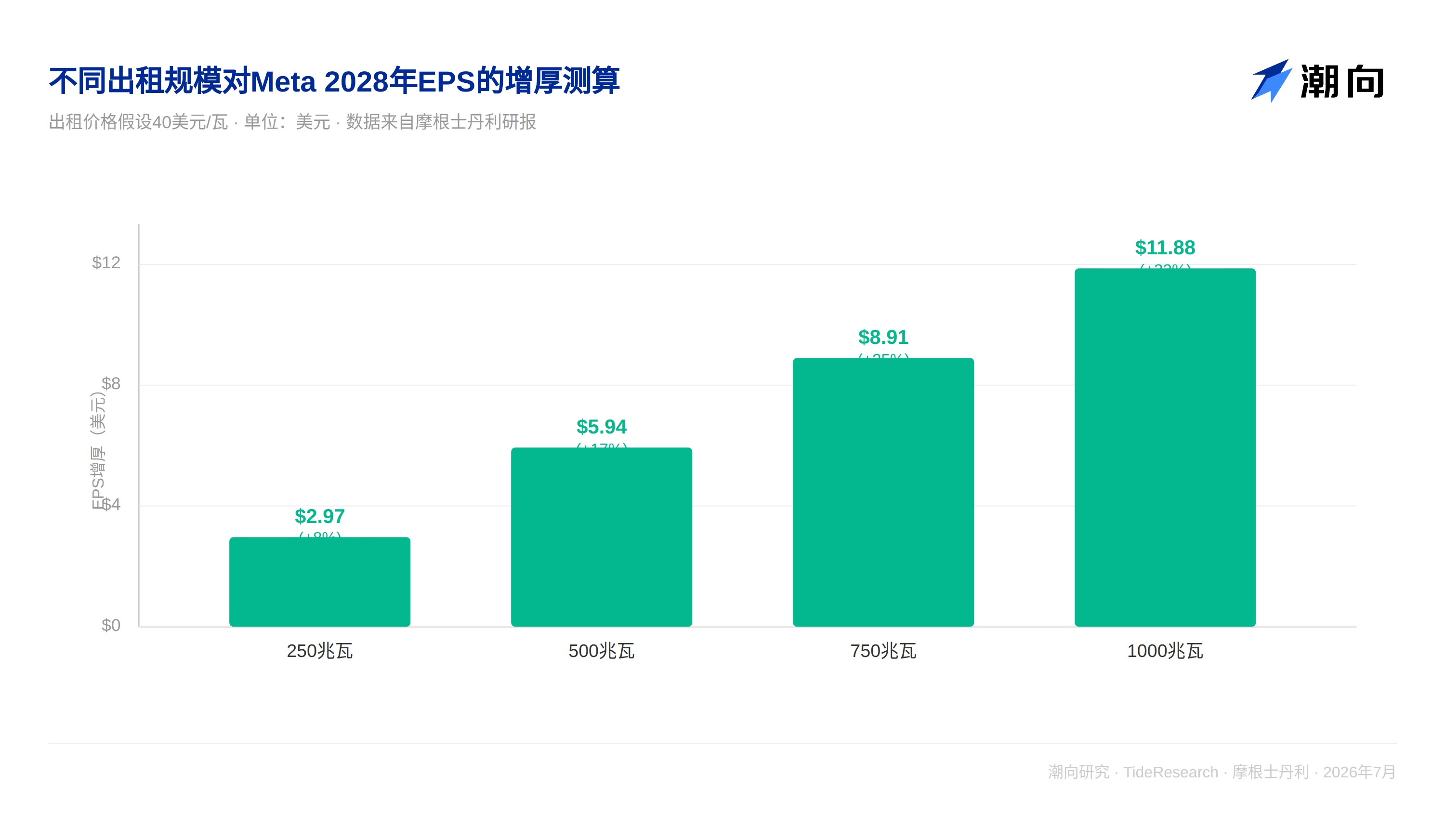

The numbers are more critical. Renting 250 megawatts of power at $40 per watt for a year could increase earnings per share by approximately 8% by 2028, and if the scale enlarges to 1000 megawatts, the increase could jump to 33%. However, Morgan Stanley made it clear that the upgrade rating for Meta is not based on optimism about its cloud venture; the core logic supporting the $775 target price remains the structural improvement in efficiency and user engagement.

Two paths for the cloud plan, differing in difficulty

The Meta cloud plan that has emerged is placed under the newly established Meta Compute department as of this January, comprising two pieces: one is model hosting API services for developers, similar to AWS's Bedrock, covering models like Muse Spark; the other is a bare metal service closer to computing power rental. Meta officials have not commented on this currently.

The report points out that the model hosting API business has higher requirements for technology, recruitment, and execution capability. Meta's Muse series models performed modestly in key tests assessing programming and third-party calling capabilities, such as TerminalBench and SWE Bench Verified, and there is still distance to catch up with cutting-edge models like Gemini. Additionally, Meta lacks a mature enterprise-level sales team like those of AWS, Azure, and GCP. Morgan Stanley believes that a comprehensive API service combining models and applications resembles a self-proof, with risks clearly higher than established cloud suppliers that have already refined their processes. In contrast, short-term rental of idle computing power does not require extensive hiring or forming new teams, making it a path with much less resistance.

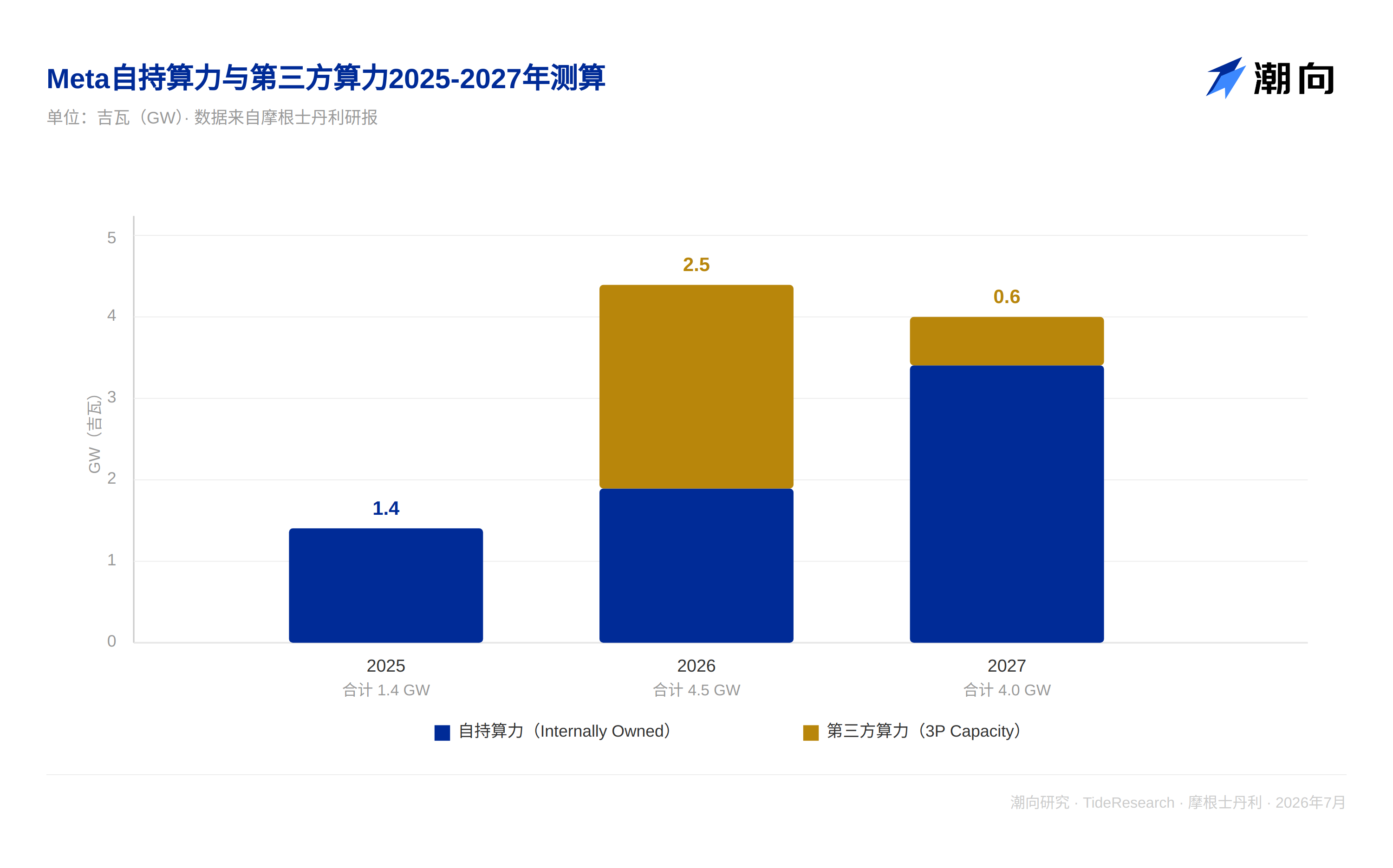

The window for excess computing power lies within these two years

Morgan Stanley estimates that Meta's owned computing power will expand from 1.4 gigawatts in 2025 to 1.9 gigawatts in 2026, and 3.4 gigawatts in 2027. In comparison, Amazon and Google are expected to each add 5 gigawatts and 9 gigawatts of computing power by 2027, which also theoretically gives Meta space to rent out. The report estimates that about 2.5 gigawatts of Meta's current computing power is rented from third parties such as Coreweave, Nebius, GCP, and Oracle. By 2026, this portion of third-party power will enable Meta's total usable capacity to reach 4.5 gigawatts, while by 2027, the third-party portion will narrow to 0.6 gigawatts, giving a total capacity of approximately 4.0 gigawatts. Morgan Stanley believes that the third-party computing power Meta rents cannot be resold, but this also indicates that the company retains more flexibility in computing power allocation and has the conditions to temporarily rent out part of its owned capacity.

Impact of computing power rental on earnings per share

The sensitivity analysis provided by Morgan Stanley shows that renting 250 megawatts of power for a year at $40 per watt can bring about $3 to earnings per share for 2028, nearly an 8% boost. If the rental scale expands to 1000 megawatts, the boost could reach $11.88, equating to a 33% upside potential. The higher the price and the larger the scale, the more evident the elasticity becomes; even at a lower price point of $20 per watt, renting 250 megawatts can still yield approximately $1.49, or a 4% increase.

How to calculate capital expenditure

Morgan Stanley's current model assumes that Meta's capital expenditure will rise from $145 billion in 2026 to $175 billion in 2027, and $205 billion in 2028, corresponding to the addition of about 3.5 gigawatts of new computing power in 2027, provided that this computing power is mainly used for Meta's own business and not for building a complete cloud service system. The report mentions that if Meta does scale its computing power rental business, there is potential for further upward revision of capital expenditures.

In a larger industry context, Morgan Stanley estimates that the combined capital expenditure of cloud companies and emerging cloud computing firms will grow from $246 billion in 2024 and $433 billion in 2025, to $834 billion in 2026 and $1.2 trillion in 2027. By 2027, the breakdown is expected to be Amazon around $225 billion, Google around $350 billion, Meta around $175 billion, Microsoft around $276 billion, Oracle around $108 billion, Coreweave around $41 billion, and Nebius around $31 billion.

Valuation perspective

The report indicates that Morgan Stanley has given Meta an upgrade rating, supported by the fact that the company is structurally shifting towards long-term user engagement and efficiency improvements, with cloud computing itself not being the core reason for the rating. Renting out computing power seems more like a transitional buffer for earnings per share; what truly supports the valuation is whether new products like MetaAI, business intelligence agents, private messaging, and diffusion models can continuously scale, and whether subscription revenue can open a new growth curve. The $775 target price corresponds to a 23.1 times multiple of the expected earnings per share of $34.16 for 2027, representing approximately 37.6% upside from the closing price of $563.29 on June 30. The bull market scenario target price is $1000, corresponding to 28 times; the bear market scenario is $450, corresponding to 14 times. The report also notes that Meta's current price-to-earnings ratio is about 35% discounted compared to Google's, sitting about 2 standard deviations below the long-term average, close to multi-year lows.

Perspective on Trends

The weakest link in Morgan Stanley's calculations is assuming that renting out computing power will be a temporary business that Meta will consistently execute long-term, while Bloomberg's news has not yet been officially confirmed by Meta; key variables such as rental price, rental period, and specific clients are still hypothetical values. Despite detailed sensitivity tables, the underlying assumptions have yet to materialize. For investors, it's more worthwhile to pay attention to this underlying line of capital expenditure; once Meta really turns cloud computing into a serious business instead of merely renting out idle computing power, the currently given range of $175 billion to $205 billion for capital expenditure is likely to be broken, which would simultaneously impact free cash flow expectations and the market's judgment on whether Meta's valuation discount can narrow.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by Trend Research. The ratings, target prices, earnings forecasts, and related judgments cited in the article are solely the views of the brokerage analysts and represent the positions of their respective institutions, not the views of Trend Research, and do not constitute any investment advice.

The market carries risks; decisions should be made independently. This article should not serve as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。