Computing is being integrated into a comprehensive capital market, just like electricity in the 1990s.

Written by: Vaidik Mandloi

Translated by: Block unicorn

Google is one of the top three cloud service providers globally, and currently, it purchases computing resources worth $920 million monthly from SpaceX (a rocket company).

This is the chaotic state of the GPU capacity market. There are no benchmarks for pricing, and lenders cannot hedge the risks of financing hardware; everything is based on blind capital allocation. But this is about to change, as the Chicago Mercantile Exchange (CME) and Intercontinental Exchange (ICE) have announced plans to launch GPU computing time futures contracts.

Computing is being integrated into a comprehensive capital market, just like electricity in the 1990s. Today, I will delve into this new liquidity forward curve driven by stablecoin settlement, exploring what transformations it can bring to the largest infrastructure build-out since the railways.

Making Computing Tradable

When I say that computing is entering capital markets along the trajectory of electricity, I mean it very specifically; understanding this will tell us how this market is actually constructed.

In commodity markets, traders make a significant distinction between stock commodities and fluid commodities. For example, oil is a stock commodity because you can store it in tankers until you find a buyer. You can stockpile crude oil when prices are low and sell it when prices soar. Computing power, however, is a fluid commodity because you rent GPUs for a period and pay for it. Any computing capacity not used during the rental period will disappear permanently.

GPUs sitting idle on racks do not equate to "stored computing," just as disconnected power plants do not equate to "stored electricity," because in both cases, the valuable product is the flow—GPU hours or kilowatt-hours, not the physical machines generating that flow.

This is crucial for pricing because stock commodities have an inherent stabilizer in inventory, whereas fluid commodities lack this stabilizer. Stock can be released during periods of sharp price fluctuations to offset rising prices. Fluid commodities do not have such a buffer; this is why the spot price of computing often fluctuates wildly.

In mid-2025, a surge in new supply due to the launch of Nvidia's next-generation Blackwell chips led to a drop in demand for H100 graphics cards, and the computing spot price plummeted by 70% within 18 months. However, this year, due to the mass production of HBM chips, demand skyrocketed, and with no inventory to absorb it, the price of H100 graphics cards soared by 48% in just four days. For AI companies (whose training operating costs can reach tens of millions of dollars) and lenders providing over $120 billion in data center credit for this hardware, this volatility without hedging tools is a life-or-death issue.

Additionally, there is a second issue. A barrel of crude oil is identical to any other barrel of crude oil anywhere in the world, which is why it can trade on exchanges without physical inspection. However, an H100 located in Virginia and an H100 located in Iceland are entirely different products, as chip, cluster configurations, and adjacent workloads affect their actual performance.

Benchmark testing data from global GPU suppliers shows that even nominally identical hardware can have performance differences of up to 38%. The electricity industry faced a similar problem in the 1990s: power from the Texas grid was drastically different from that of the Mid-Atlantic region because transmission and local demand created different conditions at each node in the grid. The only solution then was to set different prices for each node and quote prices based on reference benchmarks. This reference benchmark is precisely what the computing market currently lacks.

SF Compute has built a real-time order book for GPU time, where buyers and sellers can trade time just as they would any commodity in the spot market. The logic is that once a liquid spot market exists, trading activity can be used to derive index prices. This index price can then be used to build cash-settled futures contracts.

Once data centers can sell futures contracts and lock in revenue for months ahead, they can engage with lenders to show that their income is hedged, thus obtaining lower rates and expanding. This, in turn, can reduce overall computing costs for everyone.

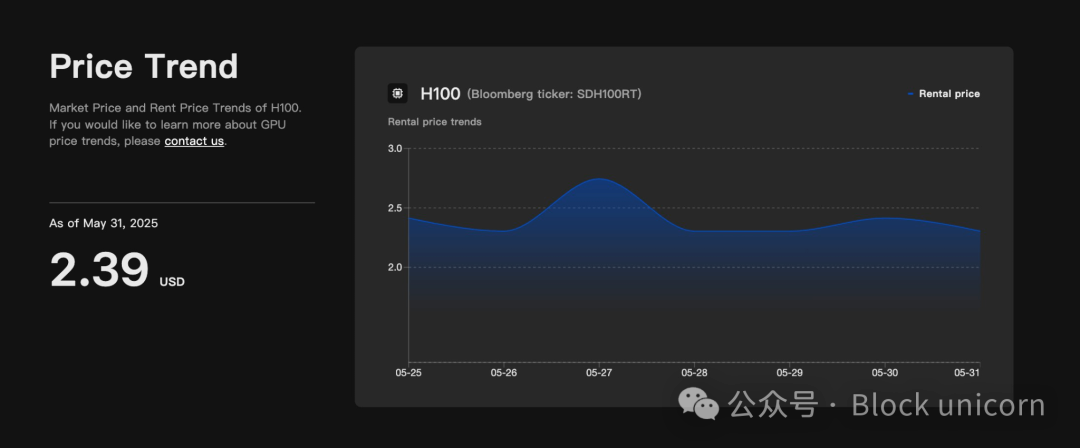

Another company, Silicon Data, has created a daily index called SDH100RT, which has been live on the Bloomberg terminal since May of last year, aggregating 3.5 million data points from global suppliers to form a single benchmark, with a cost equivalent to one hour of H100 GPU runtime. The newly announced futures contracts by the Chicago Mercantile Exchange (CME) will settle based on that index. Several companies are competing to create similar indices because becoming a reference price means they can capture a small portion of every trade in the market as long as the market exists.

The power market also went through a similar phase: in 1993, Nord Pool opened the first power futures exchange, leading to the emergence of over 200 new power marketing companies. Industry professionals spent ten years arguing whether electricity legally constituted a commodity, but today it has become a market worth $6 trillion annually. The computing market is currently undergoing a similar journey.

Intermediaries

Thus, we now have the first computing spot market that can be called an early adopter of some form of price index, and exchanges have announced related intentions. However, there is a crucial link supporting all of this operation between the index prices on the Bloomberg terminal and a well-functioning capital market, and this link operates distinctly from traditional trading methods.

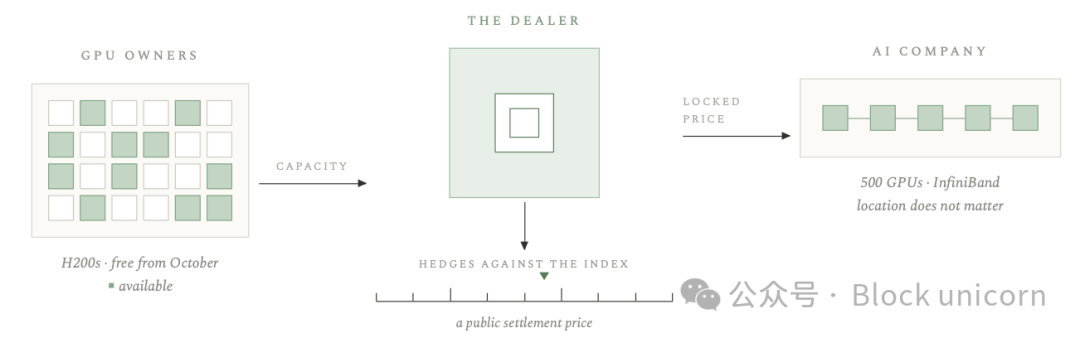

The way the computing futures market operates is entirely different from stock exchanges, where standardized stocks are traded between anonymous buyers. The computing futures market will be dominated by market makers that act as bridges between GPU owners (looking to lock in revenue) and AI companies (looking to lock in costs).

For example, imagine a data center in the U.S. has a large number of H200 servers available starting in October. A startup needs 500 GPUs but only cares whether the interconnect is InfiniBand (a type of GPU communication medium) and does not mind the specific location of the servers. This is a very specific requirement that needs someone to handle this custom order while hedging the risks posed by a standardized index.

This is not a new phenomenon; historically, each commodity has required such a link to enable parties to navigate the complex relationships of physical products and convert them into interchangeable units that can be traded on exchanges. An H100 contract on the shelf is just a custom contract that others cannot price. It can only generate revenue for one party based on a private agreement, inaccessible to other parts of the financial system. But if it can be combined with index prices and an open settlement layer, it can become a living commodity that lenders can hedge.

In 2023, CoreWeave borrowed $2.3 billion solely backed by Nvidia GPUs, marking the first time H100 hardware obtained loans. Its latest financing received an investment-grade rating from Moody's, based on Meta's credit status rather than CoreWeave's, as Meta signed a "pay without argument" contract requiring payment regardless of actual usage of computing resources.

This is also where the cryptocurrency ecosystem plays a vital role. Buyers and sellers of computing resources are spread across the globe, but they cannot obtain approval from the U.S. Commodity Futures Trading Commission (CFTC) to open U.S. commodity exchange accounts. However, cryptocurrency wallets can settle stablecoin payments, and any wallet can hold tokenized computing resources.

GPU export controls have revealed the geopolitical stratification of access to computing resources; for example, Nvidia cannot export cutting-edge chips to China and dozens of other countries. A computing futures market settled in stablecoins can provide researchers and startups outside the export-controlled areas with pricing for computing resources and hedge costs through infrastructure that bypasses restrictions, much like stablecoins have already done in Argentina and Nigeria.

Liquidity Forward Curve

Currently, constructing a GPU cluster means borrowing millions of dollars against un-lockable revenues because the global financial market lacks corresponding tools. However, a liquid forward curve allows companies to borrow against already hedged revenues at rates lower than unhedged positions. This means lower costs per computing hour. So, who will construct the settlement layer for the forward curve?

The only solution needed right now is to establish a settlement layer that allows anyone to verify collateral and treat the forward curve as a public product. Currently, we cannot verify the state of collateralized hardware, whether it has been double-pledged, or understand its actual utilization rates. But if GPUs and their yield streams can be tokenized as on-chain assets, every lender could verify collateral in real-time, making the forward curve publicly visible instead of mired in bilateral negotiations.

Moreover, future generations of AI agents will purchase computing resources by inference call counts, and they will not be able to open bank accounts. Cryptocurrencies are the only payment gateway capable of executing microtransactions between a Tokyo agent and a Virginia GPU rack in less than a second.

Currently, there are powerful checks and balances in place as GPU supply is highly concentrated. The top hyperscale data center operators control 78% of global IT computing power. Nvidia holds over 80% of the high-end AI chip market, and its product release plans can sway the entire market. Standardization presents a bottleneck, but financializing a certain asset category during a construction surge may make it more contagious.

Debt for AI infrastructure exceeding $120 billion has been transferred from balance sheets to Wall Street-funded special purpose vehicles (SPVs), much of which has entered corporate bond funds within target date retirement products, unbeknownst to the individuals holding those bonds. I believe the financing models used to construct this infrastructure likely contain assumptions about the hardware’s residual value, and existing data is insufficient to support these assumptions.

The power market does not stop at generators but runs through the entire system, up to wall sockets, affecting the prices of all electrical devices. The computing market still has many lines to lay!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。