The current market consensus is built on the "four no's": the U.S. economy will not hard land, the Federal Reserve will not raise interest rates, AI spending will not be cut, and the Democratic Party will not sweep the midterm elections.

Written by: Li Jia, Wall Street Watch

The market has almost formed a "one-sided" bullish consensus, which has become precisely the risk signal most concerning to Bank of America.

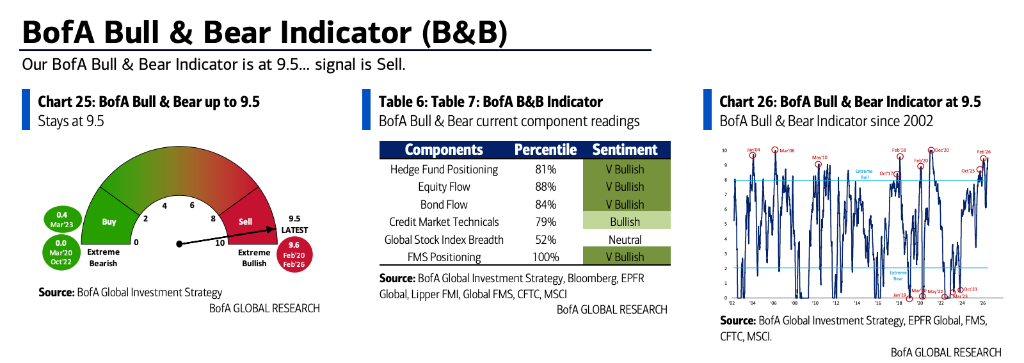

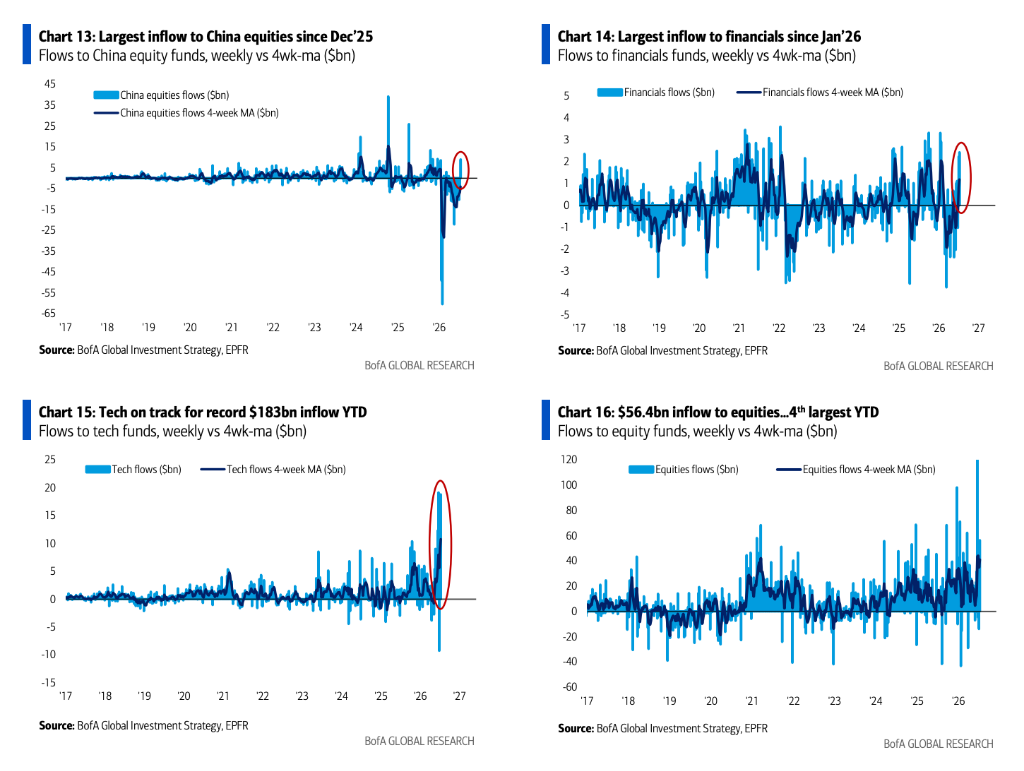

The latest edition of Bank of America's "The Flow Show" fund flow report shows that for the week ending July 8, global equity funds attracted a further $56.6 billion in inflows, with the inflow speed of technology stocks expected to set a new annual historical record; at the same time, Bank of America's Bull & Bear Indicator remains in the extremely optimistic range at 9.5, with "sell signals" having been triggered for several consecutive weeks.

Bank of America's Chief Investment Strategist Michael Hartnett believes that the current market bets on the "four no's" — the U.S. economy will not hard land, the Federal Reserve will not raise interest rates, AI capital expenditures will not be cut, and the Democratic Party will not sweep the midterm elections. It is precisely these four consensus points that support the continuous rise of risk assets, but any one of these expectations falling short could become the catalyst for the market's transition from boom to bust.

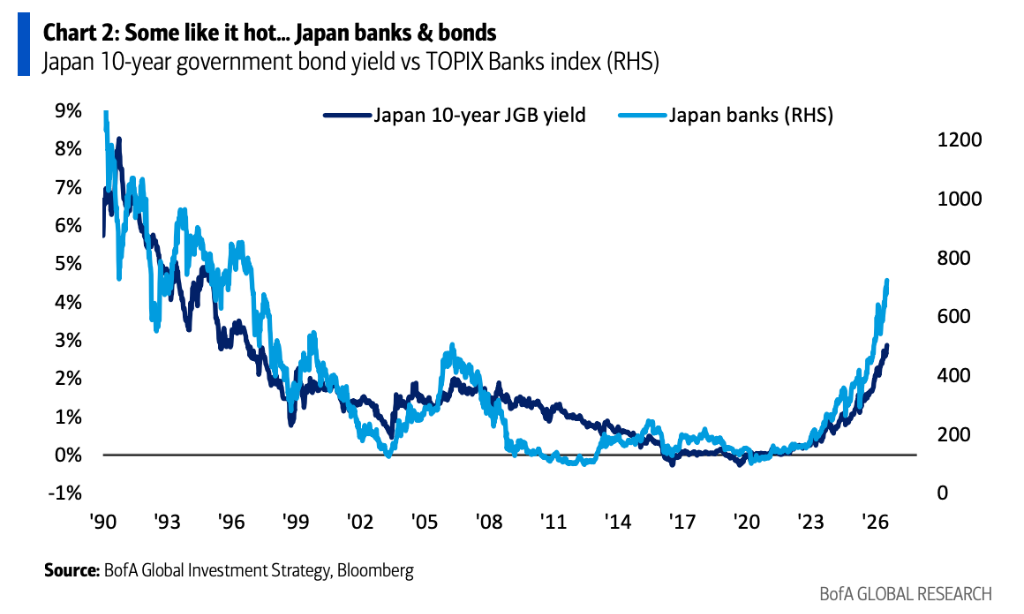

Among all risk observation indicators, Hartnett specifically mentions the Japanese market. He believes that Japanese bank stocks remain the "canary" of global risk appetite: if Japanese government bond yields rise further and rapidly, leading to a decline in bank stocks, it could signify that global risk assets are beginning to enter an adjustment cycle.

The Bull & Bear Indicator continues to flash red: "Everyone is heavily long"

The Bull & Bear Indicator from Bank of America maintained at 9.5 this week, far above the alert line of 8 that triggers a "sell signal." Historical data shows that in the past 24 years, this indicator has issued 17 sell signals, after which the global ACWI index averaged a decline of 2%-3% in the following 2 to 3 months, with an accuracy rate of about 60%, and in extreme cases, the maximum drawdown has reached 15%-20%.

From various sub-indicators, market sentiment is almost entirely in an extreme optimistic state: hedge fund positions are at the 81st percentile; global equity fund flows are at the 88th percentile; bond fund flows are at the 84th percentile; and fund manager positions have even reached the 100th percentile. The only indicator still in a neutral state is the global stock market breadth.

At the same time, Bank of America's global fund flow trading model has also maintained a sell signal for 8 consecutive weeks.

Global funds continue to flood into stocks, tech stocks expected to set historical records

Funds are still continuously chasing risk assets. For the week ending July 8, global equity funds had a net inflow of $56.6 billion, marking the fourth-largest single-week inflow this year; among them, tech funds attracted $18.8 billion in a single week, and if this pace is maintained, the net inflow of tech funds in 2026 will reach $183 billion, setting a new historical high.

Regional fund flows also reflect a rebound in risk appetite: U.S. equity funds regained a net inflow of $25.1 billion; China equity funds saw an inflow of $9 billion, the largest since December of last year; while European equity funds experienced capital outflows for the 13th consecutive week. At the same time, investment-grade bonds have seen net inflows for 14 consecutive weeks, and bank loan funds recorded the largest single-week inflow since February of last year.

It is worth noting that cash has not exited the market. The size of money market funds has risen to $7.9 trillion, setting a new historical high, and still attracted $39.5 billion in inflows during the week, indicating that a large amount of capital is chasing risk assets while retaining ample "ammunition" for new allocation opportunities.

Japanese bank stocks serve as the most important warning signal for the global market

Compared to U.S. tech stocks, Bank of America pays more attention to the Japanese market. Hartnett points out that over the past three years, the yield on Japanese 10-year government bonds has risen from about 0.5% to nearly 3%, and Japanese bank stocks have increased by about three times during the same period, becoming one of the strongest performing sectors globally.

In his view, Japanese bank stocks actually reflect the global liquidity and yield environment. If Japanese government bond yields continue to rise rapidly and begin to pressure bank stock performance, this change may signify a reversal in global risk appetite and become the earliest "canary" signal for a global stock market adjustment.

Supporting the market rise are the "four no's"

Hartnett summarizes the current market's optimistic expectations as the "four no's."

First, the U.S. economy will not hard land, meaning corporate profits still have support, and funds continue to choose to "stay away from bonds and embrace stocks."

Second, the Federal Reserve will not raise interest rates again at least until after the midterm elections, and central banks globally continue to maintain an accommodative stance. Since the beginning of this year, global central banks have cut interest rates a total of 34 times, surpassing 21 rate hikes.

Third, AI capital expenditures will not be cut. The market widely expects that global tech giants will have AI capital expenditures of about $80 billion in 2026, further rising to about $1 trillion in 2027, which remains the most important support for tech stock valuations.

Fourth, the Democratic Party will not sweep the U.S. midterm elections, meaning that fiscal and tax policies will not see drastic changes.

If the four major consensus points break, the market will usher in reverse trading opportunities

Hartnett simultaneously emphasizes that the truly worthy focus is not what the market currently believes, but which consensus is most likely to be broken.

If the U.S. economy ultimately shows significant cooling, with non-farm employment continuing to weaken, long-term government bonds, defensive consumption, high-dividend stocks, and large tech stocks may outperform the market again.

If the Federal Reserve is forced to raise interest rates again, then trades involving the dollar and yield curve flattening will become the main beneficiaries. Hartnett points out that the current U.S. CPI and unemployment rate are both about 4.2%; this combination has only occurred a few times in the past century, and almost all accompanied interest rate hikes and market turmoil.

If AI capital expenditures begin to contract, it will directly impact the current market's core investment logic. At that time, the software sector and large tech platforms may relatively outperform, while the Philadelphia Semiconductor Index (SOX) faces greater valuation pressure. Bank of America believes that narrowing debt financing space, deteriorating cash flows, and continued layoffs by tech giants may all become precursors to a cooling of AI investments.

Political risk is also not to be ignored. If the Democratic Party ultimately sweeps the midterm elections and the Republican Party loses control of the Senate, the market may once again trade scenarios of limited fiscal expansion, a weaker dollar, and declining U.S. Treasury yields.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。