JP Morgan, Goldman Sachs, HSBC, and Bank of New York Mellon have each taken completely different approaches.

Written by: Taioo

Translated by: Luffy, Foresight News

Currently, the four major banks dominate the vast majority of on-chain institutional businesses with actual operational scale, showing significant differences in their strategies and taking completely different development paths.

JP Morgan, Goldman Sachs, HSBC, and Bank of New York Mellon have all invested heavily in tokenized infrastructure, but they differ in terms of strengths, product concepts, and market competitive positions. This article will horizontally compare the four institutions across four dimensions: transaction scale, product breadth, compliance regulation layout, and underlying infrastructure model, to outline the true competitive landscape of institutional tokenization.

Evaluation Framework: Four Assessment Dimensions

To evaluate institutional tokenization businesses, this article employs a set of practical assessment standards: focusing on real operational implementation rather than conceptual promotion. The entire assessment system includes four core dimensions:

- Launch verified transaction volume in production systems

- Diversity of tokenized asset product offerings

- Completeness of regulatory qualifications and compliance system construction

- Underlying infrastructure model (self-built private chain network, joining public blockchain network, or dual-line parallel)

These dimensions correspond to different strategic advantages:

- Transaction volume: rewards institutions that quickly implement commercial systems and seize business opportunities

- Product breadth: institutions that serve diverse client types and cover all asset categories have an advantage

- Compliance qualifications: institutions that proactively build compliance systems before global regulatory details are implemented have first-mover barriers

- Infrastructure model: intuitively reflects how institutions assess the long-term strategic landscape of the future institutional blockchain market

The following sections will break down each of the four banks according to this framework.

JP Morgan Kinexys: Absolute Leader in Transaction Volume

The most critical indicator for evaluating institutional blockchain infrastructure is the real transaction scale that has been implemented, where JP Morgan far outpaces its peers.

The Kinexys system has accumulated a settlement transaction volume exceeding $1 trillion, with core business focused on tokenized collateral management and intraday repurchase settlements.

$1 trillion is a key watershed; surpassing this scale, regulators, counterparties, and institutional asset managers will view this financial infrastructure as a mature commercial tool rather than an experimental project.

JP Morgan's product layout deliberately takes a refined approach, with Kinexys focused on three major scenarios: JPM Coin cash settlement, collateral management, and repurchase clearing. The advantage of deepening a single track is that the functions of detailed scenarios are extremely well-rounded, rather than being broad but superficial, making shallow attempts at covering all asset categories.

JP Morgan's shortcoming lies in its closed private network model, as the Kinexys ecosystem is only open to JP Morgan's own institutional clients. Counterparties that have not established a banking relationship with JP Morgan cannot access its clearing system. Even though the existing internal transaction volumes are impressive, the overall market reach still has evident limitations.

Goldman Sachs Digital Assets: Leading in Product Diversity

Among the four banks, Goldman Sachs has the most diverse array of products for its institutional blockchain business.

The Goldman Sachs Digital Asset Platform (GS DAP) has completed tokenized bond issuances for multiple sovereign institutions and supranational organizations, with partners including the European Investment Bank and the Hong Kong Monetary Authority. It has also launched tokenized money market funds aimed at corporate treasury management institutions, and is a founding core member of the Canton Network, collaborating with several large financial institutions to build a shared network.

This diversified product layout matches Goldman Sachs' client structure: servicing sovereign issuers, corporate finance departments, asset management institutions, and various capital market participants. As an investment bank covering the widest array of institutional capital clients, Goldman Sachs requires an infrastructure capable of supporting various tokenization businesses rather than being limited to a single application scenario.

The Canton Network builds a shared underlying support for licensed financial institutions, with Goldman Sachs as a founding member, allowing it to lead network development while enjoying liquidity benefits from other institutional participants.

In comparison to JP Morgan, Goldman Sachs' shortcoming lies in the verified public trading volume. The Goldman Sachs Digital Assets Platform has conducted multiple real bond issuances, but the overall clearing scale of its blockchain infrastructure has not disclosed complete data as JP Morgan Kinexys has.

HSBC Orion: Leader in Cross-Border Business and Sustainable Finance

HSBC, through the Orion platform, has differentiated itself by targeting cross-border tokenized securities issuance and the sustainable finance product sector.

In November 2023, HSBC launched a tokenized gold product, "HSBC Gold Token," for institutional clients, which corresponds to physical gold stored in the London vault; this product is planned to expand to the Hong Kong retail market in March 2024.

The Orion platform has repeatedly launched benchmark tokenized bond projects, with notable projects including the Hong Kong Monetary Authority's digital green bonds issued in February 2024 and November 2025, the latter being the largest digital bond in the world.

HSBC's global positioning advantage, which local banks in New York and London do not possess, acts as a natural barrier. The client resources developed over many years in Asia, the Middle East, and emerging markets provide a natural distribution channel for tokenized securities, while regulatory frameworks for digital assets in these regions are rapidly improving.

The HSBC Gold Token is a unique innovation that extends tokenized services from institutional clearing infrastructure to ordinary retail users.

Overall, HSBC's institutional blockchain business scale is not as large as JP Morgan's, and the completeness of its products is weaker than Goldman Sachs', but its global network layout creates a unique competitive barrier in overseas markets where the other three banks are underrepresented.

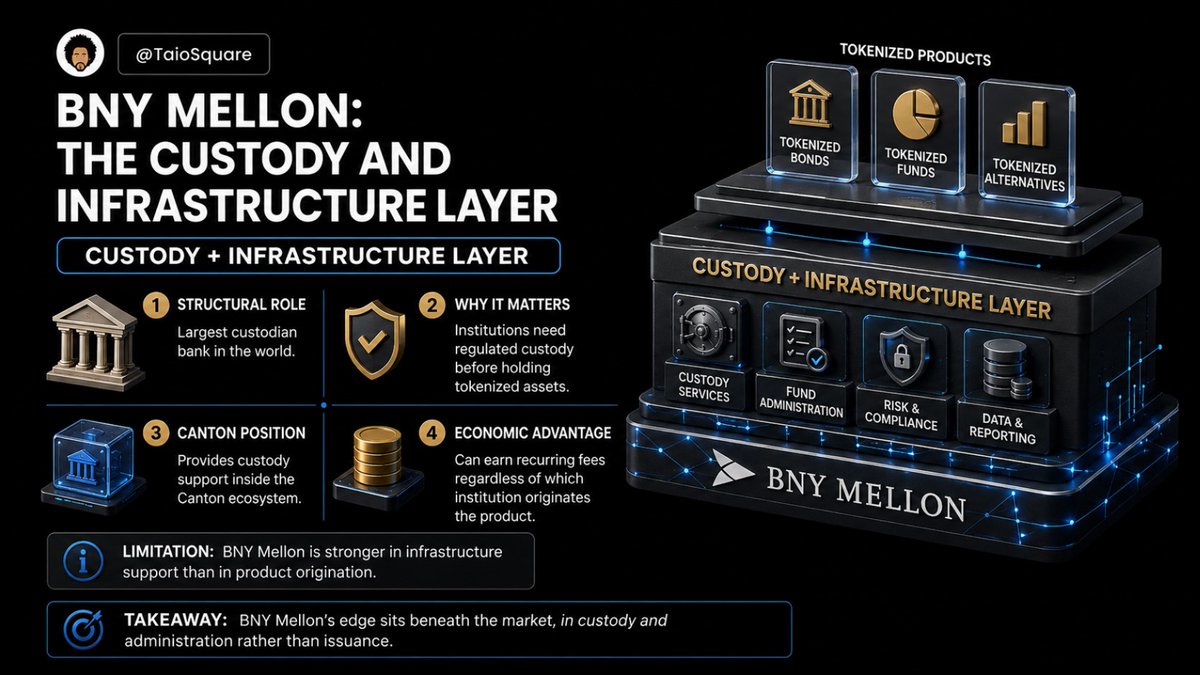

Bank of New York Mellon: Custody and Underlying Infrastructure Service Provider

Bank of New York Mellon's positioning in the institutional tokenization sector is completely different from that of the other three banks: whereas the others are primarily investment banks or large commercial banks with extensive institutional credit operations, Bank of New York Mellon primarily serves as a custodian and asset servicing institution.

The entry of the world's largest custodian institution into digital asset custody has significant implications for the landing of institutional RWA (real-world assets); for institutional asset managers to hold tokenized assets in compliant accounts, mature custody infrastructure must be in place.

Bank of New York Mellon collaborates with Goldman Sachs in the Canton Network, providing custody support for all transactions within the network. For example, when Goldman Sachs' clients issue tokenized bonds through the Goldman Sachs Digital Asset Platform and other Canton institutions participate in subscriptions, the custody services can be undertaken by Bank of New York Mellon. Regardless of which institution initiates the transaction, Bank of New York Mellon can continuously earn stable custody service fees.

The shortcoming of Bank of New York Mellon lies in its focus on providing underlying infrastructure services without actively issuing products. It does not engage in large-scale issuance of tokenized bonds or tokenized money market funds like Goldman Sachs does.

Its core competitiveness is in custodianship and asset servicing; all tokenized products held in institutional compliant accounts rely on this underlying service.

Conclusion

The horizontal comparison results of the four banks are as follows:

- Transaction scale: JP Morgan Kinexys can verify a settlement total exceeding $1 trillion, leading substantially; Goldman Sachs, HSBC, and Bank of New York Mellon have not disclosed complete transaction data of comparable magnitude.

- Product breadth: Goldman Sachs leads distinctly, launching sovereign tokenized bonds, tokenized money market funds, and co-building the Canton Network; JP Morgan has fewer products but excels in depth of segmented scenarios; HSBC has the unique gold token, tapping into the retail sector; Bank of New York Mellon focuses on underlying custodianship and does not issue front-end products.

- Regulatory compliance: all four have proactively built compliance systems before global regulatory details are implemented; JP Morgan and Goldman Sachs have the deepest communication with regulators in various countries; HSBC, rooted in Hong Kong, has a geographical advantage in the regulation of digital assets in Asia.

- Infrastructure model: JP Morgan has built a closed private network; Goldman Sachs employs a dual-line strategy, combining its own platform with a shared network; HSBC and Bank of New York Mellon mainly join shared networks and have not scaled up their own dedicated underlying network. The shared network model reduces infrastructure investment costs but also loses the unique competitive advantage offered by a private network.

The most critical finding from this comparison is that the institutional tokenization market will not converge to a single infrastructure model but will instead have multiple development paths running in parallel to match the needs of different institutional clients.

Parallel development on multiple paths conceals risks of market fragmentation. If each institution's blockchain infrastructure becomes an isolated island with insufficient interoperability between networks, rather than a unified mutual clearing system, the efficiency improvements brought by blockchain technology will be confined within individual bank client ecosystems, unable to benefit the entire market.

The future risk of industry fragmentation will depend on two major variables: the progress of interoperability standards for the Canton Network and other institutional networks, and the speed of developing a unified regulatory framework for tokenized securities in various countries.

My basic view is that over the next 5 to 10 years, major institutional networks will gradually enhance interoperability. Institutions have a business incentive to share liquidity pools, but the journey to full interoperability will be lengthy and fraught with uncertainty.

The four institutions have taken four completely different strategic routes: JP Morgan boasts transaction volume, Goldman Sachs has the most extensive product matrix, HSBC has a unique global location advantage, and Bank of New York Mellon dominates the underlying custodianship sector. In the institutional tokenization race of the next decade, who will build the most lasting competitive barriers? We will wait and see.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。