S&P Warns Tether's Bitcoin Exposure Has Breached Safety Boundaries

Written by: KarenZ, Foresight News

On the evening of November 26, S&P Global Ratings released a stability assessment report on Tether's stablecoin, downgrading Tether (USDT) from a rating of 4 (restricted) to 5 (weak).

This rating is the lowest tier in S&P's 1-5 rating system, marking a new height of concern regarding the safety of this stablecoin, which has a circulation exceeding $180 billion.

Why the Downgrade?

The downgrade by S&P is not unfounded but is based on multiple risks associated with Tether's reserve asset structure and information disclosure.

1. Bitcoin Exposure Exceeds Safety Buffer

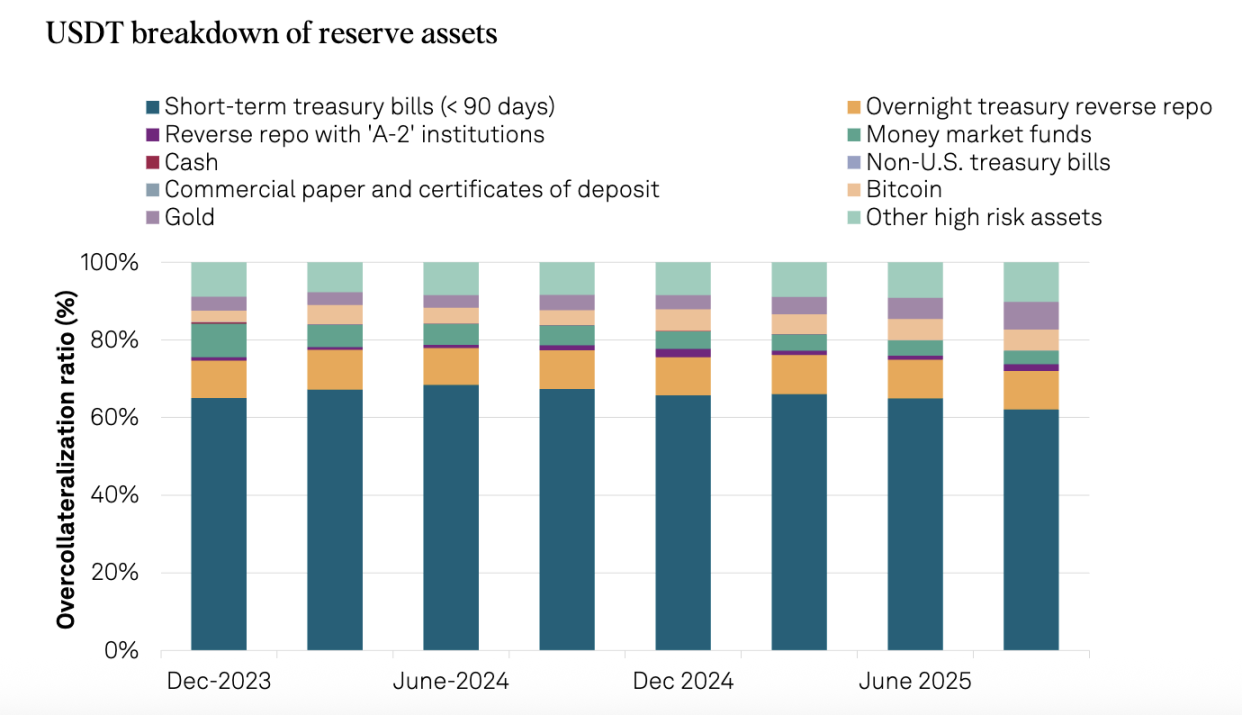

The core issue lies in the uncontrolled growth of Bitcoin exposure. As of September 30, 2025, the value of Bitcoin held by Tether accounted for 5.6% of the circulating USDT, exceeding the 3.9% excess collateral margin corresponding to its 103.9% collateralization ratio.

This comparison is particularly thought-provoking: one year ago, on September 30, 2024, the same metric was only 4%, below the 5.1% excess margin implied by the then 105.1% collateralization ratio. In other words, Tether's safety buffer is being eroded year by year.

When Bitcoin experienced significant monthly declines in October and November, this risk transformed from a theoretical threat into a real concern. If Bitcoin continues to undergo deeper declines, the value of Tether's reserves may fall below the total value of issued USDT, leading to under-collateralization. This is no longer a hypothetical scenario for S&P but a real risk that needs objective assessment.

2. Surge in High-Risk Asset Proportion

From September 30, 2024, to September 30, 2025, the proportion of high-risk assets in Tether's reserves surged from 17% to 24%. These high-risk assets include corporate bonds, precious metals, Bitcoin, secured loans, and other investments, which face credit, market, interest rate, and foreign exchange risks, yet relevant information disclosure remains limited.

Meanwhile, the proportion of low-risk assets (short-term U.S. Treasury bills and overnight reverse repos) decreased from 81% to 75%, while high-risk assets expanded accordingly. This intuitively reflects a significant increase in the market volatility sensitivity of Tether's reserve portfolio.

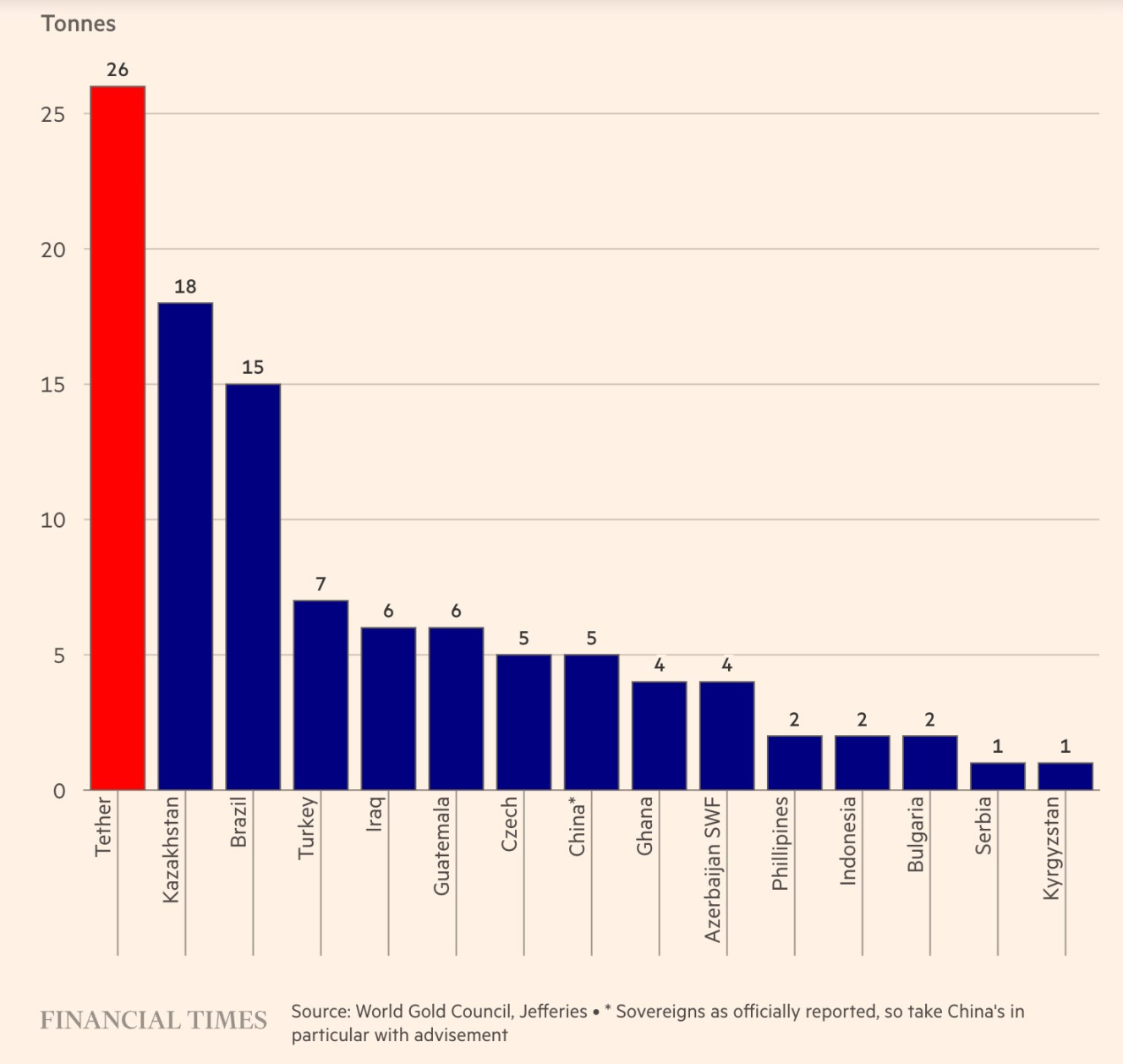

Notably, Tether's enthusiasm for gold is particularly noteworthy. The company purchased 26 tons of gold in the third quarter of 2025, holding approximately 116 tons by the end of September. Surprisingly, the gold reserves ($12.9 billion) have surpassed Bitcoin reserves ($9.9 billion), becoming its largest non-U.S. Treasury asset. This rapid expansion reflects Tether's strategic intent to hedge against fiat currency devaluation and seek value preservation and appreciation.

Source: Financial Times

3. Relatively Weak Regulatory Framework

After moving from the British Virgin Islands to El Salvador, Tether is regulated by the National Digital Assets Commission of El Salvador (CNAD). Although CNAD requires a 1:1 minimum reserve ratio, S&P believes this framework has critical flaws.

First, the rules are defined too broadly. CNAD allows the inclusion of relatively high-risk instruments such as loans and Bitcoin in reserve assets, as well as gold with significant price volatility. Second, there is a lack of requirements for the isolation of reserve assets.

4. Lack of Transparency in Management and Information Disclosure

S&P once again emphasized the age-old issues:

Lack of credit rating information regarding custodians, counterparties, and bank account providers.

Limited transparency in reserve management and risk preferences.

Limited public disclosure regarding governance, internal controls, and the isolation of these activities after the company's expansion into finance, data, energy, and education.

No public information regarding the isolation of USDT assets.

Tether CEO's Rebuttal

In response to the downgrade, Tether CEO Paolo Ardoino displayed his usual "combative stance," arguing that S&P's rating model is designed for a broken traditional financial system.

He pointed out, "We take your disdain as an honor. The classic rating models designed for old financial institutions have historically misled private and institutional investors into putting wealth into companies—despite being rated investment grade, they ultimately collapsed. This situation has forced global regulators to question these models and the independence and objectivity of all major rating agencies. Tether has built the first over-capitalized company in the history of finance, maintaining extremely high profitability. Tether is living proof that the traditional financial system has broken down to the extent that those hypocritical rulers feel threatened."

This rebuttal is not without merit. In the past, Tether has survived every FUD event. In the first three quarters of 2025, Tether's net profit reached $10 billion, making it one of the largest holders of U.S. Treasuries globally, with over $135 billion in U.S. government bonds—this scale itself serves as a credit endorsement.

Deep Reflection

What Are Stablecoins Stabilizing?

Tether's strategy of increasing exposure to Bitcoin and gold is essentially betting on "fiat currency devaluation." If future dollar inflation spirals out of control, this diversified reserve structure may provide greater purchasing power stability than a stablecoin solely backed by U.S. Treasuries.

However, under the current dollar-pegged accounting standards, this approach is destined to be rated as "high risk." This exposes a fundamental question: what exactly should stablecoins stabilize? The nominal value of the currency or the actual purchasing power?

The traditional rating system has chosen the former, while Tether is pursuing the latter. The evaluation criteria of the two are inherently misaligned.

Confusion of Roles Between Private Enterprises and Central Banks

When a private company attempts to play the role of a central bank, it inevitably faces the dilemmas that central banks encounter. Tether needs to maintain the safety of its reserves while also pursuing profitability.

Tether's accumulation of Bitcoin and gold is both a rational choice to hedge against fiat currency risks and a commercial consideration for asset appreciation. However, this mixed motivation contradicts the stablecoin commitment to "ensure principal safety."

Parallel Worlds of Institutions and Retail Investors

For retail investors, S&P's rating may just be another fleeting FUD; but for traditional institutions, this could be an insurmountable compliance red line.

Large funds and banks pursuing compliance may turn to USDC or PYUSD, as the latter's assets are primarily composed of cash and short-term U.S. Treasuries, aligning with traditional risk control models. S&P's criticism of USDT aligns closely with the requirements of the emerging U.S. stablecoin regulatory framework. This difference in standards is directly reflected in the rating differences: S&P assigned a "strong" (2) rating to USDC in December 2024.

Generational Differences in Rating Standards

The crypto world places greater emphasis on "liquidity and network effects"—this is the logic of 21st-century digital finance. USDT has proven the resilience of its network effects through 10 years of operation. However, whether a rating system more suited to the characteristics of crypto-native assets will emerge is an open question worth exploring.

Conclusion

S&P's downgrade of Tether's rating serves as a warning about the future risks of Tether. As the "liquidity pillar" of the crypto market, if USDT faces risk exposure, it not only concerns its own survival but also affects the healthy development of the entire industry.

However, this will not collapse Tether in the short term, as its massive network effect has created a moat. But it also buries a long-term concern for the market: when a private company attempts to support a global value-pegged tool with excessive risk assets, can it still ensure the absolute safety of the principal for holders?

This question not only pertains to Tether's future but also involves the sustainability of the entire stablecoin ecosystem. The answer can only be revealed with time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。