Original | Odaily Planet Daily (@OdailyChina)

Author | Qin Xiaofeng (@QinXiaofeng888)

In the recently concluded first quarter, the cryptocurrency market performed poorly, affected by geopolitical tensions (such as the Iran conflict), macroeconomic uncertainties, and a decline in risk appetite. Bitcoin dropped from about $87,500 at the beginning of the year to about $66,700, a decline of approximately 23%, marking the worst start to a quarter since 2018, with other altcoins faring even worse. Aside from tokenization of traditional assets and the AI sector continuing to grow, the overall market narrative has fallen into a drought.

In contrast, the U.S. stock market seems to be following a different script. Even though all seven tech giants experienced double-digit declines, with Microsoft plummeting 23% for its worst quarterly performance since 2008, the profit-making effect has not disappeared. Some hot sectors have rotated quickly and achieved good results. These quality assets were promptly launched on the decentralized RWA trading platform, MSX.

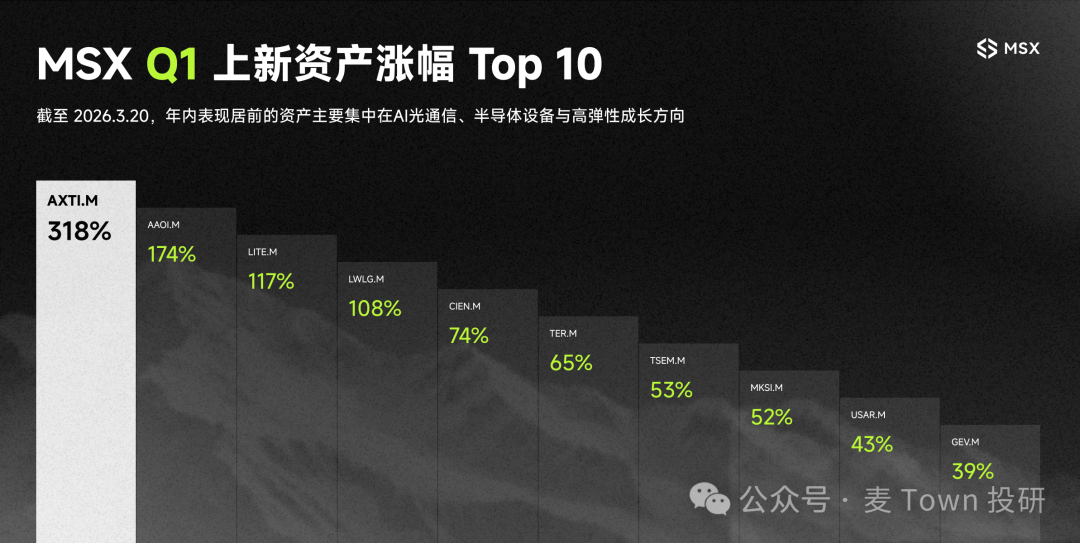

Data shows that in the first quarter of 2026, the MSX platform launched a total of 39 new U.S. stock token listings, covering individual stocks, industry ETFs, and macro tools, spanning five main lines of military aerospace, energy resources, AI hardware, optical communications, and regional allocation. The overall performance of this batch of listings has been impressive. As of the time of writing, only 1 of the 39 listings recorded a negative return (CRDO.M, -7.81%), while the rest had positive returns. Among them, 4 had gains exceeding 100%: AXTI.M (+318.59%), AAOI.M (+174.70%), LITE.M (+117.58%), and LWLG.M (+108.95%), all concentrated in the AI hardware and optical communications sectors. Additionally, there were 7 assets with gains exceeding 50%, accounting for nearly one-fifth of the total.

On the evening of April 2, Odaily Planet Daily invited Frank, a researcher from MSX, to review MSX's Q1 performance and make forward-looking predictions for new listings in Q2, helping listeners stay on top of the main line of the U.S. stock market and select stocks accurately.

Odaily Planet Daily: MSX launched 39 listings in Q1, of which 38 had positive returns, with an average increase of 37.6%. Such a win rate is quite rare in the current volatile market. What is the core stock selection framework behind this "honor roll"?

Frank: I actually want to correct a statement first. Q1 was not "volatile," but a true decline.

Throughout the first quarter, both the S&P 500 (-4%) and Nasdaq (-7%) were not moving sideways, but were truly declining, especially as the heavyweight tech stocks faced significant pressure. Core assets like Microsoft, Tesla, Meta, Google, Nvidia, Amazon, and Apple generally experienced varying degrees of pullback, even falling below their 200-day moving average.

This means that the backdrop of MSX's "Q1 39 launches, 38 positive returns, 8 with gains over 50%" report card was produced in an environment where the broader market was falling, and valuations were being killed.

If we break down the logic behind these results, frankly, timing the market correctly is certainly one reason. The launch timing of certain listings indeed fell just before market initiation. But beyond luck, more importantly, MSX has always followed a relatively stable principle in stock selection:

We avoid those stocks that seem to have large potential but have unclear industry directions, and we do not gamble on when large-cap blue chips will hit their bottom; instead, we prefer to find mid and small-cap stocks with clear industry trends, a transparent capital transmission chain, and performance likely to be gradually realized.

In simple terms, we are not betting on whether a major trend will suddenly reverse, but rather digging down along the most certain value chains. Who is receiving orders, who is undertaking capital expenditures, and who genuinely benefits from industry expansion are our focal points.

To put it more directly, we are not betting on whether a grand narrative will suddenly reverse but following the most certain value chains down. Who is getting orders, who is seeing capital expenditures, and who genuinely benefits from industrial expansion are more likely to enter the observation and listing vision of MSX. It’s also because of this that we can still produce a relatively impressive "honor roll" report card in an environment where indices and heavyweight stocks are generally under pressure.

Odaily Planet Daily: You organized the Q1 listings into five main lines: AI hardware, optical communications, energy resources, military aerospace, and regional allocation tools. How were these five lines identified and established as "tradable directions" at the beginning of the quarter? Were there any quantitative or macro indicators as support?

Frank: Actually, these five lines were not "planned" at the beginning of the quarter. More accurately, they gradually emerged during the continuous tracking of industry dynamics, financial report data, and market movements.

The research team at MSX has a core action every day, which is to keep an eye on the financial reports of large tech companies, capital expenditure guidance, data from the supply chain, as well as the latest hot narratives and capital movement sectors.

For instance, when Meta, Microsoft, Google, and Amazon continuously raised capital expenditures related to AI infrastructure, these figures in financial reports may seem like cold budgets, but essentially, they will inevitably flow down along the supply chain—toward chips, optical modules, power equipment, and thermal management and testing processes.

So rather than making macro judgments, we are more like tracking capital flows and paths of industry realization. The actual money that big tech spends is often more explanatory than many abstract macro indicators—PMI, interest rate expectations, macro scales are certainly important, but the actual solid signals are those that come from signed contracts, orders placed, and capacity expansions.

On this basis, we further distinguish which companies in various tracks are genuinely receiving orders, and where income and profits are beginning to manifest, versus those that are merely ahead in concept and sentiment.

As for energy resources and military aerospace, their driving forces are not entirely the same as the AI supply chain, leaning more towards policy, geopolitics, and cyclical logic, but essentially still meet MSX's same filtering criteria, which is first to look at whether the motivations are real, then to see if the benefits are specific, and lastly to assess whether tradability is established.

Odaily Planet Daily: Among them, AI hardware and optical communications have become the strongest dual main lines in Q1. At what point did you confirm that these two lines possessed "systematic opportunities" rather than merely short-term trading themes?

Frank: The AI hardware line is actually something our research institute began focusing on in Q2 and Q3 of last year. During that phase, almost all market attention was on Nvidia, but MSX had already started looking upstream and downstream in the supply chain to find out who was engaged in packaging, who was managing thermal solutions, who was involved in power management, and who was tackling more segmented requirements.

This stems from a very simple reasoning: Nvidia's market value is already in the trillions; although its certainty is high, its elasticity is limited, while its Tier 2 and Tier 3 suppliers are still in the early stages of performance explosion. There exist two transmissions: one is the real flow of orders, income, and profits along the supply chain; the other is the transmission of market attention, capital preferences, and narrative heat, with the former determining the fundamentals and the latter determining the pricing reassessment, both necessitating time.

As for optical communications, confirmation occurred somewhat later, probably between Q4 of last year and January of this year. The critical turning point came after the Q3 and Q4 financial reports of big tech were released, with capital expenditure guidance becoming increasingly aggressive. If you tally this up, you'll find that data centers need to expand, and computational density needs to be increased, thereby creating a real demand for the infrastructure, including optical modules, optical fibers, and switching and interconnection links.

Thus, the core standard for MSX to judge whether a line has systematic opportunities has never been about whether the concept is trending; instead, it has been whether there are real orders being transmitted within this industrial chain, whether real money is flowing, and whether companies stuck at key points have already demonstrated revenue growth.

Only when these conditions are met can it be regarded not as a short-term trading theme but as a systematic opportunity worthy of continuous allocation and listing. We generally prefer to avoid concepts that are purely narrative-driven.

Odaily Planet Daily: In contrast, military aerospace and regional allocation tools did not exhibit substantial rises but are still included in the system. How do you assess their true value within the portfolio?

Frank: The modest rise precisely indicates that their role was never meant to be "forward thrust."

A mature platform product logic cannot place all its bets on high-elasticity tracks. For example, if users' portfolios consisted entirely of AI hardware and optical communication stocks, back-testing would show that Q1 would have been quite rewarding, but once a major line adjusts, it could become very passive, akin to the article I just saw about Cathie Wood. Her investment style is quite aggressive, though she operates in secondary markets; she follows the fundamental logic of venture capital for aggressive investment.

This approach easily becomes a double-edged sword; when hitting the left side, it can surge dramatically, as with the tech stock frenzy during the 2020-2021 easing, propelling Wood to be revered as the "female Buffett," managing assets worth up to $59 billion. Yet, it can also plunge tremendously; as seen now, it has dropped 70%, resulting in hundreds of billions evaporated...

Ultimately, high elasticity is an advantage, but without structural hedging and diversification, it can likewise turn into a double-edged sword.

Hence, the value of military aerospace and regional allocation tools lies in providing a form of "varying directional exposure"; after all, military aerospace has its independent driving factors, corresponding very little with the AI cycle—upgrades in geopolitical rivalry and increased national defense budgets represent a logic that is entirely asynchronous with tech cycles. Regional allocation tools emphasize functionality, such as enabling users to conveniently allocate some exposure outside the U.S. market.

This type of asset may not be meant to deliver the maximum increase, but they allow users to construct a more complete and resilient portfolio on the MSX platform. We don't aim to deliver only the assets that can best appreciate but rather to provide enough usable configuration tools to help users respond to different market environments.

This is also something MSX has consistently adhered to in its listing framework: it must have offensive elasticity and structural integrity.

Odaily Planet Daily: The new listings in Q1 presented a clear phased progression: January focused on macro fundamentals, February delved into AI infrastructure, and March supplemented tools and materials. How do you understand this dynamic and responsive mechanism? Was this rhythm the result of proactive design, or a dynamic adjustment influenced by market sentiment and capital flows?

Frank: Both aspects are present, but if we had to assign weight to each, dynamic adjustment would likely weigh more heavily.

In January, the focus was on macro frameworks because the most heated areas initially were energy, resources, and geopolitical cues, with the market’s feedback coming from these directions first. By February, as big tech financial reports began to surface and Capex data increasingly exceeded expectations, a more informed digging into AI infrastructure's finer segments could take place—who is producing optical modules, who handles liquid cooling, who provides electric power solutions, and who authentically receives orders linked to expansion logic.

In March, when supplementing tools and materials, it primarily stemmed from the leading securities already having run through a wave of performance, prompting funds to naturally look for peripheral segments that had yet to be fully priced in, rebounding assets, and relatively lower beneficiaries. Additionally, the emergence of events like GTC and major optical communication industry conferences catalyzed further market attention moving from the leaders to supporting and application levels.

Thus, you could interpret MSX's listing rhythm as having a forward-looking judgment on the broad direction, but the specifics of which assets to list, how many to list, and which categories to prioritize are dynamically pushed forward along with the rhythm of industry data release and market capital preferences.

This does not resemble a last-minute decision-making monthly plan, but rather resembles a mechanism dubbed "advance when the signal is received," which is why MSX's listings do not appear mechanical, but rather reflect a continuous high-frequency interaction with the market.

Odaily Planet Daily: In the context of tightening global liquidity, the cost-effectiveness of U.S. stocks and Crypto is being reassessed. How do you see this "capital dual-choice" trend continuing into Q2?

Frank: Altcoins are indeed entering a "sage period." In the past two years, many stocks in the U.S. have doubled, even increased tenfold over months; for example, LITE launched in Q1 more than doubled in just one to two months.

So, I don't think this is merely "dual-choice." Instead, it is capital reallocating priorities; in the past two years, crypto users have distinctly experienced a learning curve, gradually shifting from pure MEME and on-chain speculation to focusing on macro elements, the Federal Reserve, and big tech earnings reports.

This cognitive upgrade, once it occurs, is irreversible. When they discover that there are higher certainty opportunities in U.S. stocks with relatively manageable volatility, a portion of their positions will naturally shift over.

Will this trend continue into Q2? I believe there is a high probability, and it could even accelerate. The reason is simple: the crypto market currently lacks new high-level narratives, and on-chain activity is decreasing, while AI industry performance verification in U.S. stocks is just beginning. Intelligent capital will gravitate toward areas with higher certainty.

Based on this trend judgment, MSX has recently launched a content initiative called "Investing in U.S. Stocks" (for those interested, it can be found in the "Newbies and Education" section on the official website), aimed at helping users from a crypto background understand the basic logic of U.S. stocks—how to view financial reports, how to interpret valuations, and how to analyze supply chains. This effort is to systematically bolster the foundational skills of "reading financial reports, assessing valuations, and understanding supply chains."

This content is not merely for spreading awareness; it derives from our recognition of changing user demands. Users are not looking to "abandon crypto"; rather, they seek to allocate funds to more efficient and profitable avenues in the current market environment, necessitating the learning of U.S. stocks and actively enhancing their own arsenal.

This change is what truly warrants attention as a trend.

Odaily Planet Daily: After the landing of securities tokenization, the "entry barrier" for U.S. stocks is lowering. How do you think this will change the structure of retail investors in the future?

Frank: The most intuitive change is that as the barrier lowers, the people entering will naturally change.

In the past, for an Asian retail investor to participate in U.S. stocks, they often had to go through a series of frictions such as traditional brokerage accounts, fund transfers, account systems, and minimum funding requirements; however, with the gradual implementation of securities tokenization, users can participate in relevant listings through a more lightweight on-chain方式, enabling more flexible and fragmented holdings.

Essentially, this does not just move the trading interface on-chain but unlocks a batch of new users who were previously blocked by infrastructure barriers.

From a structural change perspective, we at MSX research institute identify two clear trends.

First, the proportion of retail investors from the Asia-Pacific region and emerging markets will increase. They haven't been lacking in demand; instead, they were impeded by channels, costs, and processes. With these constraints weakened, new users will naturally join.

Second, the trading methods of this new batch of users will likely be more "thematically driven" rather than the traditional index-based passive configuration, because they are inherently accustomed to track thinking, narrative thinking, and thematic investment thinking. Their focus in crypto has been on new narratives and new tracks, so when they enter the tokenized securities market, they are likely not to simply buy the index and lay low for the long term but actively seek out segmented opportunities that are more elastic within the supply chain.

This point is very much in alignment with MSX's asset selection logic because we are not merely providing a generalized entry point focused on broad tools but are striving to construct a thematic and structured trading platform that is more suited for a new generation of on-chain users to understand and operate.

In other words, the changes brought about by securities tokenization are not only about "how to buy," but also about "who buys, what is bought, and why it is bought."

Odaily Planet Daily: From the Q2 starting point, how do you view the continuity and switching risks of the current main line of U.S. stocks? Are AI hardware and optical communications still the core offensive areas? Are there new main lines entering the new listings realm of MSX?

Frank: I believe the AI narrative will likely continue, but its form is already changing.

In Q1, the market has indeed begun to move away from the singular mindset of "as long as Nvidia rises, it’s an AI market," and instead is beginning to observe who truly benefits from the incremental gains post-AI infrastructure expansion. This suggests that AI hardware and optical communications will still be the core offensive direction in Q2, but the trend may progressively shift from "broad-based increases" to "differentiated selection."

In other words, the direction may not weaken, but stock picking will evidently become more difficult. The future will not compete on whether there is AI exposure, but on who stands at more critical, quickly fulfilling segments.

Additionally, there are two directions that we at MSX research institute believe are worth paying close attention to.

The first is aerospace. This is not entirely a new main line, but as we enter Q2, its certainty is higher than in Q1. The underlying reason is that the geopolitical environment is still continuously changing, and the timing of national defense budgets and associated contracts is becoming clearer, with certain companies in niche segments showing increased visibility of their performance.

Recently, MSX keenly captured this trend and pre-launched several mid and small-cap commercial aviation listings, generally receiving double-digit increases. Particularly in the past few days, when the market has been overall weak, these stocks have shown relatively independent performance, which indicates that this direction possesses continued observation and layout value.

The second area is software SaaS, which has been unjustly penalized by Q1 sentiment. In Q1, software stocks were often indiscriminately cut down. The market initially priced them using risk appetite before differentiating their fundamentals. However, there will surely be a group of companies with high customer retention, healthy cash flow, and clear competitive moats that have been pulled down just because of the pressures in the sector. Once such assets enter the valuation recovery phase, their elasticity is often considerably significant.

Therefore, MSX's understanding of Q2 can be summarized as follows: the main line is still present, but the style will shift from "broad net" to "deep selection," continuing to capture high-certainty main lines like AI hardware and optical communications while also starting to explore new structural opportunities in aerospace and software recovery.

Odaily Planet Daily: In the current macro context (interest rate trajectory, geopolitical environment, profit cycle), do you lean towards offensive targets or allocation tools? How do you balance elasticity and defense?

Frank: I believe the key to this question lies not in simply answering whether to lean towards offense or defense but in how to understand the macro environment at this phase.

•First, on the interest rate path, the market's expectations for rate cuts have been revised multiple times, so strategies overly based on the assumption that "cutting rates at a certain point is guaranteed" can indeed be dangerous;

•Second, there remains a high level of uncertainty in geopolitical aspects;

•Third, while capital expenditures in big tech are still expanding, the speed of revenue realization has not completely synchronized, indicating that the market will increasingly care about "when the money spent translates into real profits."

Thus, in this backdrop, MSX is more inclined not towards full offense or full defense,but rather towards offense with defense.

Specifically, core positions will still prioritize the most certain AI infrastructure chains because these companies have more legitimate orders and revenue growth logic backing them; at the same time, a portion of defensive exposure that is less correlated with the tech cycle, including energy, military, and a certain proportion of tool-focused configurations, will be retained.

This approach also represents MSX's overall thinking in platform new listings: we will not place all resources on high-elastic offensive stocks but will continuously supplement some defensive and tool-type assets, allowing users to find suitable strategies in different market environments.

Ultimately, a truly long-term effective system does not rely solely on identifying the hottest main line at any given time, but rather maintains the ability to balance offense, certainty, and portfolio stability. The Q1 report card fundamentally reflects this logic's phase manifestation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。