Everyone is closely watching the crypto boom in the United States, while emerging markets quietly begin the next phase of the industry.

Written by: Liam Akiba Wright

Translated by: Chopper, Foresight News

Compared to the bustling American crypto market, Israel and Pakistan staged a more low-key yet far-reaching test this month. The truly critical industry changes of 2026 may be occurring in places where digital assets are deeply integrated with local currencies and banking systems.

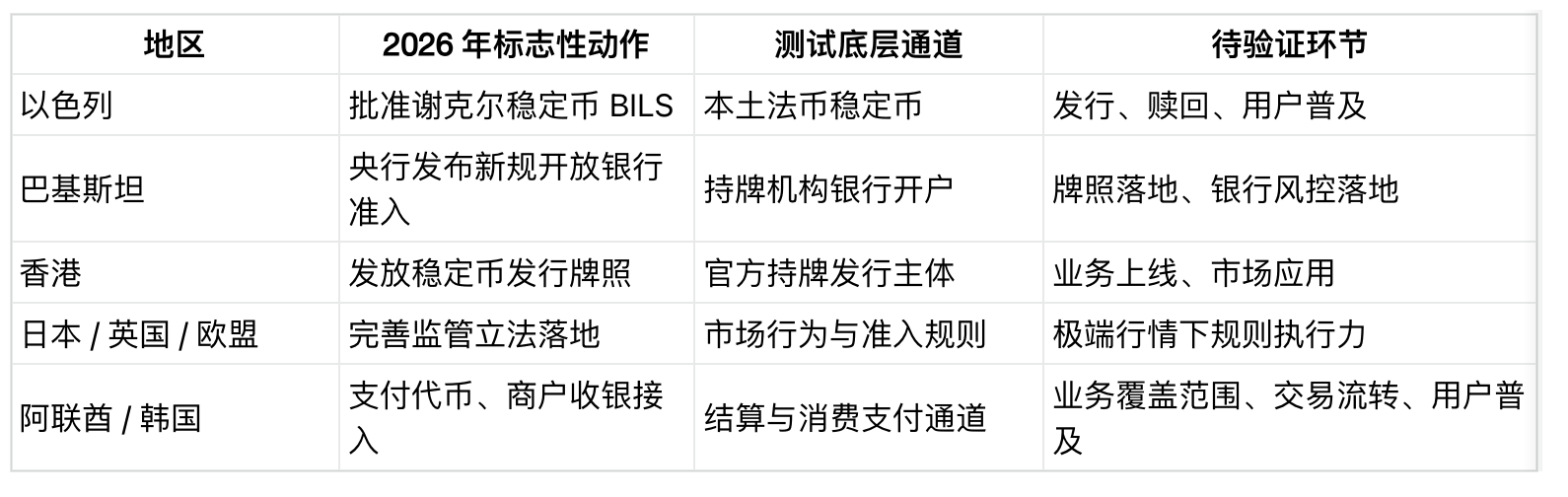

Israeli crypto firm Bits of Gold announced that after two years of pilot programs, the Israeli Capital Market Authority has approved the issuance and circulation of the stablecoin BILS, which is pegged to the shekel. Just a few days earlier, the State Bank of Pakistan issued notification number 10 of 2026, officially abolishing the cryptocurrency ban that had been in place since 2018.

The new regulations in Pakistan clarify that under a compliant regulatory framework, licensed Virtual Asset Service Providers (VASP) and approved operators can open bank accounts.

These two initiatives are entirely different from the U.S. spot ETF boom, but they point to the underlying logic that will determine the future of the crypto industry: whether cryptocurrencies can transcend their role as mere investment tools and truly integrate into mainstream financial infrastructure.

America has brought compliance endorsements, liquidity to the crypto industry, and ignited the debate over digital dollar discourse. Meanwhile, other countries and regions are testing a different set of underlying capabilities: whether cryptocurrencies can seamlessly connect with local fiat currencies, bank accounts, merchant payment settlements, and establish practical, executable market regulatory rules.

Perhaps we need to redefine the criteria for global cryptocurrency adoption. Bitcoin ETFs simply provide investors with another asset allocation channel, while compliance with local fiat currency stability allows users to directly hold their country's legal currency on-chain.

The central bank permitting crypto institutions to open compliant bank accounts creates a bridge for the industry to access the formal banking system. ETFs merely acknowledge cryptocurrencies as an asset category, while local stablecoins and bank access truly test whether cryptocurrencies can evolve into usable public financial infrastructure.

Currently, everything is still in the early pilot stage. BILS still needs to complete formal issuance and actual implementation; Pakistan still needs to cultivate licensed service providers and establish stable banking partnerships. Other regions are also progressing with their layouts: newly licensed stablecoin organizations in Hong Kong await official business launch; the UAE, South Korea, Japan, the UK, and the EU are each working on different segments of a comprehensive crypto adoption system, including payment tokens, merchant cash register settlements, market behavior regulation, access licenses, and risk compliance rules.

The UAE still needs to clarify the relationship between the issuance of dirham tokens and central bank records. But the trend is becoming increasingly clear: in 2026, the actual focal point of the crypto industry will be increasingly centered on the deep integration of digital assets with fiat currencies, banks, merchants, and clearing settlement systems.

Local Legal Currency and Banking Services

Bits of Gold has stated that the approved BILS will initially be issued based on Solana, with pilot partners including Fireblocks, QEDIT, Ernst & Young, and the Solana Foundation.

The greatest significance of the policy level is the on-chainization of local fiat currency. BILS brings the shekel into an on-chain market still dominated by USD stablecoins, raising the question: can a national currency achieve a programmable version without ceding the entire payment layer to USD tokens?

At the core is the game of monetary sovereignty. USD stablecoins have become the primary medium of settlement in the crypto market; and once the shekel stablecoin is successfully issued and adopted, Israel can establish a national currency payment channel within the same set of on-chain infrastructure. Its value lies not in market heat but in whether wallets, exchanges, payment institutions, and compliance organizations are willing to actively integrate and use it long-term.

Pakistan, on the other hand, has filled this crucial gap in bank connectivity. The new regulations from the Central Bank of Pakistan replace the old ban from 2018, allowing institutions regulated by the central bank to open bank accounts for compliant virtual asset businesses and their users. At the same time, all banks must meet requirements for risk control reviews, documentation filing, fund monitoring, and user risk screening, and strictly adhere to the country's virtual asset regulatory framework.

This has fundamentally changed the living environment for licensed crypto institutions. Bank accounts are the most basic underlying facilities of the financial system, directly determining whether compliant entities can hold client funds, complete fund reconciliations, fulfill due diligence obligations, and bring transactions into the regulatory monitoring system.

In Pakistan, which has long been among the world leaders in on-chain crypto adoption, bank access will determine whether the industry remains in informal circulation or enters a traceable, institutionalized stage of formal development.

Hong Kong is also following the path of first issuing licenses and then launching businesses. On April 10, the Hong Kong Monetary Authority granted stablecoin issuance licenses to two institutions: Antrix Financial and HSBC Hong Kong, with the licenses officially taking effect on the same day. This marks Hong Kong's move from policy planning to the implementation phase of licensed institutions, with further waiting for business launch and market user adoption.

The global landscape of crypto infrastructure in 2026 is clearly visible:

Brazil, Singapore, Thailand, and the Philippines are also advancing crypto compliance, from virtual asset licenses and stablecoin regulation to tokenized clearing, cross-border travel payments, and banking custody services blooming in multiple areas.

Regulatory Rules Are Becoming New Financial Infrastructure

The regulatory framework itself is evolving into a foundational infrastructure for the industry.

The Financial Services Agency of Japan plans to upgrade crypto assets from regulation under the Payment Services Act to standards under the Financial Instruments and Exchange Act, strengthening information disclosure, institutional risk control, market manipulation oversight, insider trading constraints, regulatory authority, and user protection mechanisms. This means that crypto assets will be included in a strict financial regulatory system, with entry qualifications tied to behavioral compliance, ongoing supervision, and accountability.

This also confirms that regulatory design itself is a form of foundational infrastructure. The market relies on laws to define access permissions, asset custody qualifications, marketing boundaries, and legal liabilities of trading behavior.

The UK is also steadily building its regulatory system. From September 30, 2026, to February 28, 2027, a new application for crypto business licenses will be open, and the new regulations will officially take effect on October 25, 2027, simultaneously pushing forward access authorization, ongoing supervision, consumer rights, asset custody, prudential operation, and market anti-manipulation guidelines.

The EU's MiCA regulation has been fully implemented, establishing a unified framework of crypto rules covering information transparency, mandatory disclosure, institutional access, daily supervision, consumer protection, market fairness, and financial stability.

Global regulation is no longer a single country’s action but is being promoted through multi-regional collaboration. The biggest change in 2026 is that regulatory rules are starting to directly determine whether crypto products can enter mainstream formal financial channels.

The UAE has launched a regulatory framework for payment tokens, and the central bank has published a list of licensed institutions; at the same time, multiple financial institutions have been approved to issue the dirham stablecoin DDSC for institutional payments, clearing, fund pool management, and cross-border trade settlements. Currently, this is limited to institutional scenarios, and widespread retail adoption still requires further verification.

South Korea is completing the merchant payment link. In March of this year, Crypto.com partnered with KG Inicis to integrate crypto payments into a vast merchant network, serving outbound tourists and local e-commerce users, allowing merchants to choose to receive settlement in fiat or digital assets. Korea's K Bank has also partnered with Ripple to test cross-border payments, exploring the integration model between the banking system and crypto payment channels. The core value of such layouts is to extend crypto applications from mere investments to real scenarios such as cash register settlements, cross-border remittances, and daily consumption.

Implementation Is the Final Test

The U.S.-centric narrative remains strong, given its sufficiently large scale. As of April 29, the total crypto market capitalization is close to $2.59 trillion, with Bitcoin's market cap around $1.56 trillion. USD stablecoins continue to monopolize market liquidity, with USDT 24-hour trading volume around $111.5 billion and USDC at about $47.84 billion.

Such a large scale ensures that U.S. policies and the dollar settlement system always capture global attention. The stablecoin game behind the CLARITY Act is fundamentally a struggle for economic dominance over the digital dollar. USD liquidity remains the core pillar of global crypto infrastructure, and this is irreplaceable.

However, actual usage data is rewriting the criteria for evaluation. Chainalysis data indicates that by 2025, the actual economic flow of global stablecoins will reach $28 trillion, and by 2035, it is expected to increase to $71.9 trillion, with an optimistic scenario possibly approaching $150 trillion. Although these predictions are model extrapolations, they indicate a trend: the value of stablecoins has extended from trading margins to three core scenarios: payment infrastructure, corporate fund pools, and cross-border clearing.

Emerging markets are the central stage for this transformation. The Chainalysis global crypto adoption rankings show that India is at the top, followed by the U.S., Pakistan, Vietnam, and Brazil, with adoption covering all income levels. The key to lasting adoption lies in deposit channels, clarity of regulation, and the completeness of financial and digital infrastructure, which are precisely the core issues being tested by the bank access in Pakistan and local stablecoin in Israel.

The International Monetary Fund has also pointed out risks: cross-border flow of stablecoins can affect exchange rate deviations, domestic currency devaluations, dollar premiums, and overall financial stability. Simply put, when stablecoins are deeply integrated into the foreign exchange market, their influence will significantly rise, also bringing new policy battles.

Contradictions arise. Local fiat stablecoins can maintain the status of national currency in on-chain finance; bank access brings crypto institutions into the regulatory system; and merchant payment access allows cryptocurrencies to step out of their investment attributes into daily settlements. But each new channel also imposes higher demands for reserve fund regulation, redemption mechanisms, anti-money laundering, market manipulation, and exchange rate risk management.

The current pattern is already clearly differentiated: U.S. ETFs and Wall Street's entry have completed the financial investment of cryptocurrencies, lowering the threshold for public asset allocation; while the truly more difficult and core challenge of adoption is unfolding under the push of regulatory authorities across the region: whether crypto can truly connect with local fiat, bank accounts, merchant consumption, and the foreign exchange market.

Currently, everything is still in its early stages. BILS awaits formal issuance and user implementation; Pakistan awaits licensed institutions to genuinely integrate into the banking system; new licensed organizations in Hong Kong await business launch; Japan, the UK, and the EU await the regulatory rules to undergo extreme market tests; the UAE needs to完善 rules related to issuance and record keeping; and South Korea needs merchant payments to reach real transaction scales.

If all these pilot projects go smoothly, the global crypto landscape will no longer be dominated by the U.S. investment product cycle, but instead become a regional financial ecology where various areas absorb and integrate crypto assets within their own local regulatory frameworks. If the pilots do not meet expectations, the dollar and the U.S. capital market will continue to dominate the industry’s direction.

The next round of true competition will not be about market hype but about the actual rate of adoption in real usage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。