The report from Guotai Junan points out that the market has seriously overestimated the policy capacity boundaries of the Federal Reserve regarding Wo Sh's push for monetary easing and lowering U.S. Treasury yields. The U.S. is facing a triple structural constraint of sticky inflation, fiscal deficit, and an AI bubble; externally, it is continually eroded by global supply chain restructuring, the spillover of monetary easing from major trading partners, and the declining status of the dollar as a reserve currency. Regardless of how the Federal Reserve operates, an upward-sloping yield curve has become a high-probability path.

Written by: Li Jia

Source: Wall Street Watch

Inflationary pressures have reignited, driving global bond yields to multi-year highs. The yield on the U.S. 30-year Treasury bond reached 5.18%, the highest level since 2007; the 10-year yield also rose to 4.66%, a new high since January 2025.

The market had expected that Wo Sh would promote a shift towards easier monetary policy upon taking office as Federal Reserve Chair, thereby lowering U.S. Treasury yields. However, the latest report from Guotai Junan Securities indicates that this expectation has seriously overestimated the Federal Reserve's policy capacity boundaries.

The report posits that the U.S. currently faces three internal structural constraints: sticky inflation, expanding fiscal deficits, and an AI capital bubble, which leave the Federal Reserve with far less maneuvering room than the market anticipates. Meanwhile, three external pressures—global supply chain restructuring, the spillover effects of monetary easing from major trading partners, and the continued decline of the dollar's global reserve status—further erode the external conditions for decreasing U.S. Treasury yields.

Against this backdrop, regardless of who serves as Federal Reserve Chair, the room for long-term rate declines is extremely limited, and an upward-sloping yield curve has become a likely path.

Internal Constraints: The Triple Lock of Inflation, Fiscal Issues, and the AI Bubble

The United States is facing a significant narrowing of policy space due to its three structural constraints.

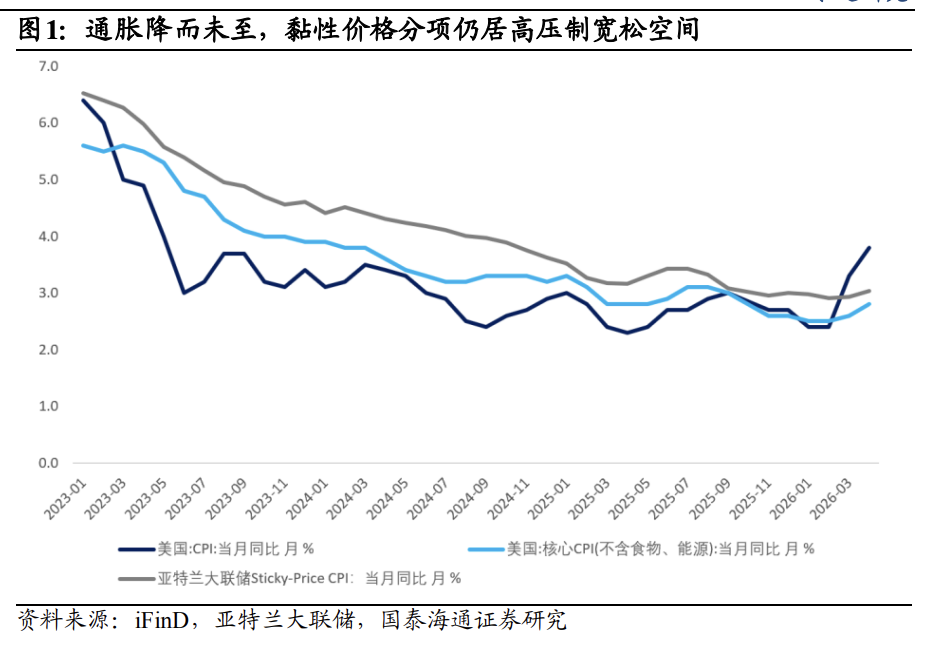

Sticky inflation continues to rise. In April 2026, the overall CPI in the U.S. rose 3.8% year-on-year, while the core CPI recorded a 0.4% month-on-month increase, the largest single-month gain this year. The sticky price CPI tracked by the Atlanta Federal Reserve has an annualized month-on-month rate of 4.6%, with the core measure surging to 4.8%, indicating that inflationary pressures have deeply penetrated areas like rent and services, which are typically slower to adjust. Market mainstream forecasts suggest that the May CPI may break above 4% year-on-year, making accelerated inflation increasingly the baseline scenario. In this context, rashly cutting interest rates will struggle to gain political support within the FOMC and will face credibility challenges.

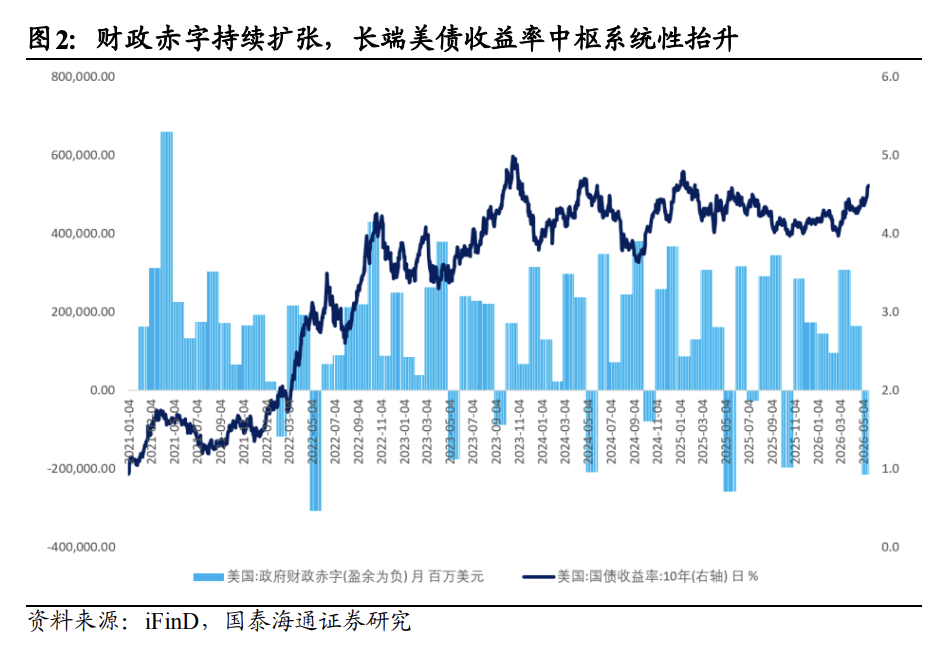

The expansion of fiscal deficits intensifies long-term pressures. The federal deficit for fiscal year 2025 has reached $1.8 trillion, with large-scale tax reforms and spending plans expected to increase the deficit by more than $3 trillion over the next decade. The Treasury has significantly ramped up Treasury bond issuance, with short-term Treasury bill supply possibly surging by more than $1 trillion in the second half of the year, causing subsequent pressure from long-term bond coupon supply to translate into long-term yields. Continued increases in supply amidst a lack of marginal demand result in structural upward pressure on long-term rates. Even if the Federal Reserve lowers rates, the 10-year Treasury yield may not fall in tandem, as the transmission of monetary policy has been significantly discounted in the face of fiscal pressures.

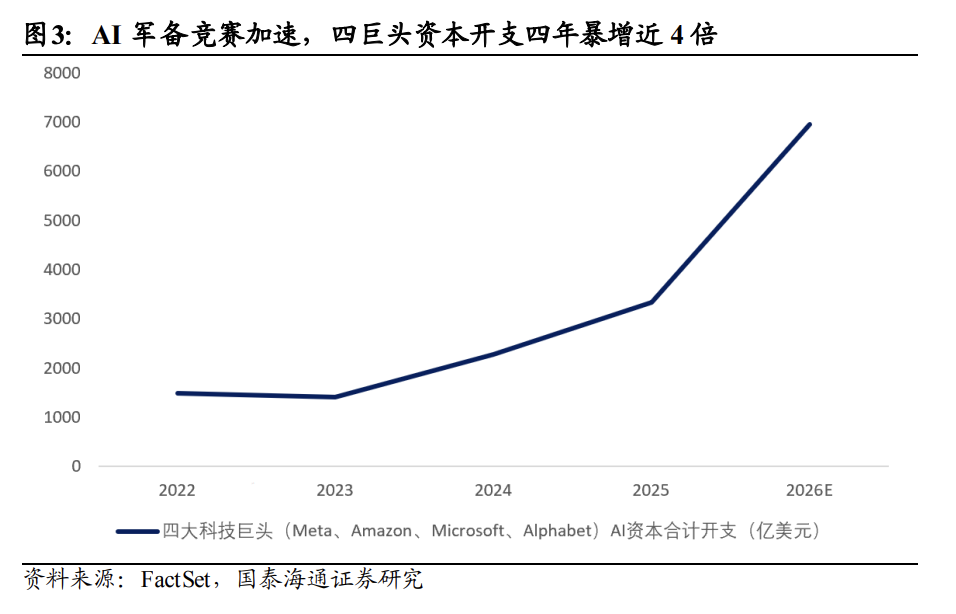

The AI bubble elevates inflation and market risks. The capital expenditure of the four major tech giants is projected to be around $410 billion in AI in 2025, accounting for about 1.3% of U.S. GDP, expected to rise to 1.6% in 2026. The enormous capital expenditure driven by the AI narrative has driven up prices for energy, land, and high-end manufacturing. The valuation of the S&P 500 is around 23 times forward earnings, reflecting a bubble level close to that of the early 2000s internet bubble. The ongoing boom in real investment continues to fuel inflation, and should the bubble burst, the Federal Reserve will find itself in a dilemma between stabilizing the market and containing inflation. Simply changing the Federal Reserve Chair is unlikely to achieve an overall downward shift in the interest rate curve.

External Erosion: Weakening U.S. Pricing Power Amid Global Supply Chain Restructuring

Global structural forces are also weakening the basis for the downward movement of long-term U.S. Treasury yields from three dimensions.

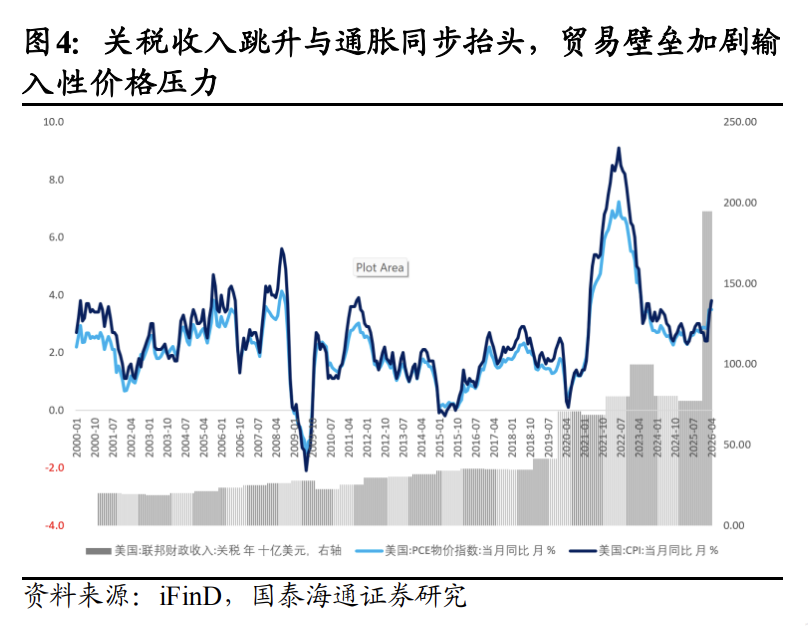

Tariffs are reshaping supply chains and raising the inflation baseline. Excluding low-cost supply sources from the global supply chain has forcibly increased the central production costs globally. Data from the Federal Reserve Bank of St. Louis shows that from June to August 2025, tariffs contributed approximately 0.5 percentage points to the annualized PCE inflation in the U.S.; over the 12-month period up to August 2025, tariffs accounted for 10.9% of the overall PCE inflation. The transmission mechanism of "tariffs equal inflation" has been fully validated by data.

Exchange rate fluctuations amplify the risk of reflation. Major manufacturing countries use monetary easing to respond to trade frictions, and a weakening currency exports exchange rate fluctuations and commodity price pressures globally. The construction cycle for alternative supply domestic capacity is longer and more costly, thereby magnifying the global risk of reflation in the short term. The International Monetary Fund points out that tariffs constitute a supply shock for the U.S. but a demand shock for other economies, further diversifying the inflation landscape and significantly increasing the difficulty of global central bank policy coordination.

The weakening of the dollar's reserve status leads to declining external demand for U.S. Treasuries. The dollar's share in global official foreign exchange reserves has fallen from about 71% at the beginning of this century to about 56% currently, hitting a nearly 20-year low. Central banks are accelerating diversification of their allocations, steadily increasing the strategic weight of gold, euros, and emerging market currencies. There is weakening marginal buying pressure from foreign central banks, leading to a diminishing support for long-term U.S. Treasuries. The Federal Reserve's own research also acknowledges that if confidence in the U.S.'s ability to repay debt or manage currency falters, the demand for dollar assets will face deeper erosion.

TACO Does Not Change the Major Direction of Interest Rates; An Upward-Sloping Curve is Probable

The so-called "TACO" (Trump Always Chickens Out) describes the regularity where markets plummet after Trump announces radical tariff measures, only for the White House to soften its stance, leading to rebounds in risk assets. After a delay in tariffs on Europe in 2025, the S&P 500 saw a daily increase of over 2%, but the yield on the 30-year Treasury bond concurrently approached 5%. The message from the bond market is clear: tariff concessions cannot resolve fiscal deficits, sticky inflation, and supply pressures; these are the core variables determining long-term pricing.

Regardless of what policy path the Federal Reserve under Wo Sh takes, an upward-sloping yield curve is a likely outcome.

Path One: Continue to lower rates. Short-term rates will decline in line with federal funds rates, while long-term rates will be constrained by fiscal supply and inflation premiums, resulting in a clearly blunted trajectory that forms a bull-steep structure. Since the Federal Reserve began its rate-cutting cycle in September 2024, the 10-year Treasury yield has risen from 3.65% to a peak of 4.79% in January 2025.

Path Two: Accelerate easing. If the Federal Reserve hastens its pace of easing under political pressure, the market will call into question its independence, and inflation expectations will be re-priced, inevitably raising the long-term yield's term premium further. The current 10-year term premium has reached its highest level since 2011.

In summary, making a one-sided bet that the 10-year Treasury yield will significantly decline is extremely low in cost-effectiveness under the current macro framework. In contrast, the trading logic of the 2s10s or 5s30s steepening curve is more advantageous—supported by short-term rate cut expectations and bolstered by long-term supply pressures and inflation premiums, resulting in a significantly better risk-reward ratio. Trump's TACO characteristics may create a short-term window for bullish trades, but this is a tactical game rather than a strategic shift.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。