Written by: Mike, Frank, MSX Maitong

If everything goes according to plan, SpaceX will go public on June 12 under the ticker SPCX on Nasdaq.

If all goes well, this will become the largest IPO in the history of global capital markets—according to the currently disclosed offering arrangements, SpaceX plans to raise approximately 75 billion USD, with a target valuation of about 1.75 trillion USD, which not only surpasses the fundraising scale of Saudi Aramco's IPO but also positions it as one of the most valuable publicly traded companies upon listing.

However, for the market, the significance of SpaceX goes far beyond "another star tech stock going public."

More importantly, the long-imagined and high-threshold field of commercial space has finally gained a genuine public market pricing anchor. Over the past few years, investors have recognized the appeal of the space economy, understanding that satellite internet, commercial launches, remote sensing data, and defense aerospace all have long-term potential, but it has been difficult to determine how much these assets should actually be valued.

Once SpaceX begins trading at a public market price, all publicly listed commercial space companies will be re-evaluated on the same valuation table, differentiating who is closer to SpaceX's capability frontier, who has real orders and revenue, and who is merely riding on a thematic wave.

Therefore, understanding commercial space before and after SpaceX's IPO should not focus on chasing short-term sentiment but instead on answering three questions: First, why is commercial space worth long-term attention? Second, which companies within the sector truly have sustainable business models? Third, after SpaceX goes public, will it siphon off funds or uplift the entire sector?

1. Commercial Space: From Government Projects to Commercial Assets

To understand why commercial space is worth long-term attention, one must grasp the historic transformation the industry is undergoing.

For decades, entering space has essentially been an extension of national capabilities. The United States has NASA, the Soviet Union had the Soviet space program, followed by the Russian Federal Space Corporation. Rocket development, satellite launches, and space exploration have fundamentally been large-scale projects led by governments; while commercial capital has participated, it has been difficult to become a leading force.

The reasons are simple: costs are too high, cycles are too long, and failure rates are too high. Traditional satellite launches often run into hundreds of millions of USD, with project construction cycles measured in years, and commercial return cycles could even extend to decades. For most enterprises, this is not a track that can accommodate standard business models, but rather resembles a part of national strategic investment.

It is because of this that the key to SpaceX's industry transformation lies not just in sending rockets into space, but in reshaping the cost curve of entering space.

Reusable rockets are at the heart of this change. The Falcon 9 first stage rocket can autonomously return and land after launch, and after refurbishment, it can execute missions again. This technology has transformed launches from single-use consumables into infrastructure that can be amortized multiple times. The previous launch cost of hundreds of millions of USD has been compressed to the tens of millions, and as new generation systems like Starship mature, costs may continue to decline.

Once the cost curve breaks downward, business models that were previously deemed unviable will start to take shape.

Satellite internet is the most direct example. In the past, launching thousands of satellites to form a low Earth constellation was nearly unimaginable economically; but with the reduced costs from reusable rockets, Starlink has the potential to transition from a grand vision to a subscription-based internet service for global users.

Remote sensing data services follow the same logic. Commercial satellites capturing Earth imagery, tracking crops, monitoring ports, and serving national defense and insurance industries faced significant challenges in scaling commercialization due to high satellite manufacturing and launch costs; but as satellite deployment costs decrease and data processing capabilities enhance, space data can evolve from "high-end customized services" to "continuously subscribed data products."

Looking further ahead, areas like space manufacturing, on-orbit services, lunar missions, and space AI data centers are still in early exploration stages, but the underlying logic is consistent: only with the continuous decline of marginal costs of entering space will new demands be unleashed.

Historical precedents of similar scenarios are not uncommon. Breakthroughs in shale gas technology lowered extraction costs, altering the U.S. energy landscape; smartphones reduced the threshold for mobile computing, leading to an explosion of mobile internet; and cloud computing transformed IT infrastructure from one-time capital expenditures to on-demand payments, enabling SaaS to truly become a major industry.

Commercial space is following a similar path. It is not linear growth of an existing market, but rather a re-opening of new markets following a breakthrough in the cost curve.

This is why the global space economy is transitioning from a niche tech narrative to a long-term industrial narrative. Several institutions predict that the global space economy is poised to grow from approximately 630 billion USD in 2023 to around 1.8 trillion USD by 2035, driven primarily by commercial pivot points propelled by the interplay of launch costs, satellite manufacturing, data processing, and defense needs.

2. Looking at SpaceX from the Prospectus: What Is It Doing Now

The high market attention on SpaceX is because it is far more than a simple rocket company.

From the currently disclosed information, SpaceX's business structure can be roughly divided into three layers: launch and space infrastructure, Starlink satellite internet, and AI and computational power business formed after the incorporation of xAI.

The first layer is launch services and space systems.

This is SpaceX's foundational capability and the basis for all other businesses. The Falcon 9, Falcon Heavy, Starship, and the launch system developed around NASA, the U.S. Department of Defense, and commercial clients collectively form SpaceX's engineering barrier. Reusable rockets not only allow for lower costs but also enable a higher frequency of mission execution.

In the aerospace industry, high frequency itself is a barrier. The more launches, the more data, the quicker engineering iterations, and the more mature cost control become. This positive cycle is difficult for traditional aerospace companies to catch up to in the short term.

The second layer is Starlink.

If the rocket business validates SpaceX's engineering capabilities, then Starlink demonstrates SpaceX's commercialization ability. Low Earth orbit satellite internet is essentially a global communication network; the broader the coverage, the more users, and the more mature the terminals, the better opportunity there is to continuously dilute marginal costs.

This is also SpaceX's biggest difference from most commercial aerospace companies: it does not only sell one-off projects but also has ongoing subscription revenue. Starlink targets a variety of scenarios including individual consumers, enterprises, aviation, maritime, government, and defense, transforming a capital-intensive space project into a revenue model more akin to a telecommunications operator and internet infrastructure. For the capital market, this layer of business is also the most easily understood and modeled part of SpaceX's valuation.

The third layer is AI and computational power business.

This aspect represents the most imaginative and controversial part of SpaceX's current valuation. With xAI's incorporation into SpaceX, the company's narrative has extended further from "rockets + satellite internet" to "space infrastructure + AI infrastructure." Whether it's a large ground-based computational cluster or future orbital AI data centers, SpaceX is attempting to position itself in the competitive landscape of AI era infrastructure.

However, this layer of business also introduces new uncertainties. According to disclosed data, Starlink already possesses strong profitability, but the overall SpaceX group is still burdened by high capital expenditure and losses in the AI business. In other words, SpaceX is not a purely "already stable and profitable" company, but rather one that, after proving commercialization in its core business, continues to invest cash flow and capital market expectations into the next round of super narratives.

This is also why its valuation is so complex.

It possesses both the certainty brought by NASA and defense contracts, the growth fueled by Starlink's subscription revenue, along with the long-term potential of AI, Starship, Mars missions, and space data centers. It is neither a traditional aerospace stock nor a purely internet stock, but a composite giant formed by engineering capabilities, communication networks, government orders, and AI infrastructure.

This very complexity is why the market is willing to assign it a valuation in the trillion-dollar range, and also why investors must remain cautious.

3. Within the Sector: Siphoning or Uplifting?

After understanding the long-term logic of commercial aerospace, the real question begins: which companies within the commercial space sector are worth long-term attention?

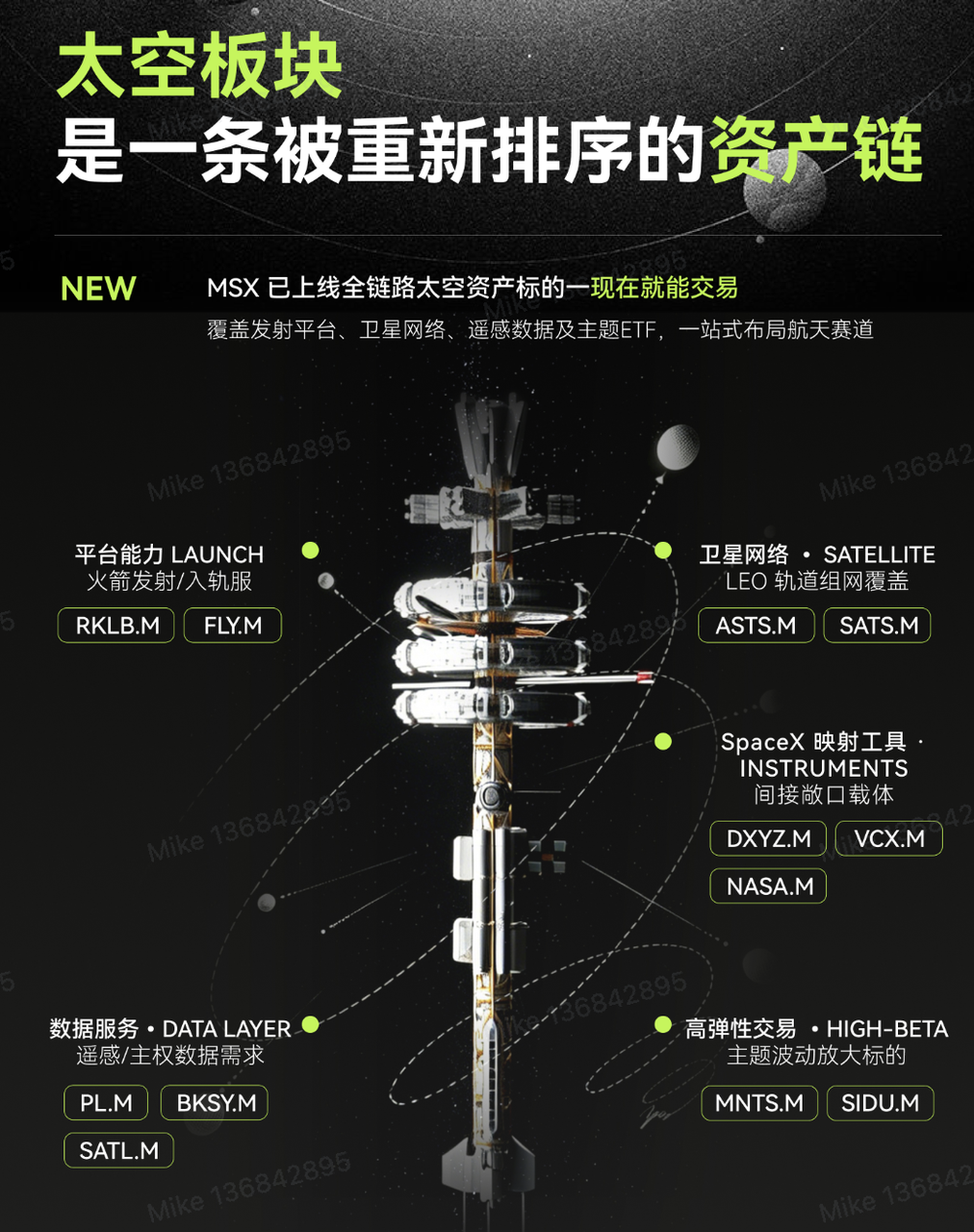

Here, it is necessary to establish a basic judgment, namely that commercial space is not a homogenous sector; it contains platform companies comparable to SpaceX, satellite network companies, data services companies, highly elastic small-cap companies, and those providing indirect exposure through ETFs or closed-end tools. Thus, the valuation logic for different assets varies significantly, as do their risk-reward ratios.

If one does not differentiate and simply uses the term "space stocks," it is very easy to buy the weakest comparable assets during the hottest emotional moments. A more reasonable approach is to break commercial space into five layers:

First Layer: Platform Space Infrastructure

This layer is closest to the public market comparable logic of SpaceX. For example, what SpaceX lacks is not just rockets, but rather its full-stack capabilities spanning from launch, satellites, ground stations, communication networks, government contracts to long-term AI infrastructure. In publicly listed companies, the ones most closely aligned with this positioning are RKLB.M (Rocket Lab) and FLY.M (Firefly Aerospace).

Rocket Lab is currently the most typical platform-type candidate among publicly listed space companies. It has the Electron small rocket launch business, satellite and space system business, and is extending toward medium reusable rockets with Neutron. By 2025, Rocket Lab is expected to achieve annual revenue of 602 million USD, with a year-end backlog of 1.85 billion USD, putting its revenue visibility relatively ahead of other commercial space public companies.

On the surface, Rocket Lab's current valuation does not seem cheap. However, the market's willingness to give it a premium is essentially pricing for a shift in identity, as it transitions from merely a "small rocket company" to a space infrastructure platform driven by three engines: "launch + satellites + defense orders."

The biggest catalyst in 2026 is the maiden flight of the medium reusable rocket Neutron. The management's latest guidance points to the fourth quarter; if Neutron successfully launches, Rocket Lab will first possess medium lift capability comparable to Falcon 9 in some mission scenarios, transitioning from the small payload market into the larger main track; simultaneously, Rocket Lab's defense attributes are also strengthening. The company has secured the SDA Tranche 3 project, involving 18 satellites worth approximately 816 million USD, progressively converting orders into revenue.

Additionally, with mergers and integrations in areas like laser communication, space robotics, and satellite components, Rocket Lab's narrative has evolved from "can they launch" to "can they become the second space infrastructure platform in the public market."

Firefly resembles a second-tier company in the ascent of platform capabilities. This company went public in August 2025 with an issuance price of 45 USD, raising approximately 868 million USD, covering launch, lunar missions, and defense directions, and already has clients like NASA and Lockheed Martin. However, it is still in a high growth, non-profitable, and high volatility phase.

The advantage of companies like this lies in their high elasticity, but the drawbacks are also very clear; once a mission fails, orders are delayed, or market risk appetite decreases, the valuation pressure will be more severe than for mature platforms.

Thus, Rocket Lab is more suitable as a core sample of the platform logic in commercial space, while Firefly leans more towards a high-elasticity growth sample.

Second Layer: Satellite Networks and Connectivity Services

The second layer focuses on coverage, access, and long-term service revenue.

The most representative company in this layer is ASTS.M (AST SpaceMobile). Its core is not satellite manufacturing but building a satellite communication network aimed at ordinary mobile phones, commonly referred to as "direct connect mobile."

If this model can succeed, the potential for ASTS is very large. It targets global mobile communication blind spots, connecting remote areas, disaster communications, defense communications, and more, theoretically possible to collaborate with existing mobile operators rather than completely replacing them. However, ASTS's challenges are also evident: commercial validation is still underway, satellite deployment pace, capital consumption, spectrum coordination, and operator cooperation progress, all impact valuation realization speed.

SATS.M (EchoStar), on the other hand, is more like a mature satellite operation platform; while its growth potential is less than ASTS, its assets and businesses are more developed, and volatility is relatively controllable. For investors, such assets are more suitable as a stable observation sample in the direction of satellite communication infrastructure rather than purely chasing high elasticity.

Third Layer: Space Data Services

The third layer is the easiest in the space economy to shift from "concept stock" to "operating asset."

The representative company is PL.M (Planet Labs), and the logic is clear: selling continuously updated Earth observation data, with agriculture, insurance, energy, ports, national defense, and government management becoming potential usage scenarios for its data.

In the 2026 fiscal year, Planet Labs achieved revenue of approximately 308 million USD, with a year-end backlog of 900 million USD, and it has for the first time turned Adjusted EBITDA positive; this is important as it indicates the company has progressively transitioned from "burning money to tell a story" to the "business self-sustaining" stage.

In contrast, BKSY.M (BlackSky) is more focused on space intelligence and defense subscription logic. The core points of interest are high-frequency remote sensing, AI analysis, international clients, and government contracts, with the business model closer to "space intelligence service provider," supported significantly by defense and sovereign needs.

SATL.M (Satellogic) is smaller in scale, with higher elasticity, but also weaker in certainty, making it more suitable as a high-elasticity supplementary sample rather than a core asset of the sector.

Fourth Layer: Highly Elastic Small Caps

Companies like MNTS.M (Momentus) and SIDU.M (Sidus Space) fall into the fourth layer.

They share common traits of being small-cap, early-realizing, and high-volatility, pricing more reliant on events, themes, and technology validation. When themes heat up, these assets often respond first because a small transaction volume can push prices; but as soon as the market shifts from sentiment to valuation comparisons, they are also the easiest to reassess.

Fifth Layer: SpaceX Exposure Instruments

Before SpaceX officially goes public, another type of choice has emerged in the market: obtaining indirect exposure to SpaceX through ETFs, closed-end funds, or pre-IPO tools.

For instance, tools like DXYZ.M, VCX.M, and NASA.M have all, to varying degrees, absorbed the scarce trading before SpaceX goes public.

The core logic behind DXYZ is "SpaceX expectation trading + scarce private equity tech assets." It provides public market investors with a channel to indirectly trade a private giant.

VCX resembles a basket of unlisted tech assets, containing not only SpaceX but also other AI and pre-IPO tech companies, making its pricing logic closer to the overall risk appetite for unlisted tech assets.

NASA.M combines the space-themed ETF with SpaceX exposure tools. It went public at the end of March 2026, quickly attracting funds based on the anticipation of SpaceX's IPO, becoming one of the most sought-after space-themed tools in the market.

However, this type of tool also faces a very practical issue: once SpaceX's main entity goes public, the scarcity of substitutes will weaken.

When SpaceX cannot be purchased directly, the market is willing to pay a premium for alternative exposure; but when SPCX can be traded directly, some funds may flow from alternative tools to the main entity. This does not mean these tools will necessarily lose value, but their pricing logic will change: from "unique entry" to "combinatorial allocation."

This is also an important reason why diversification may occur in the space sector after the SpaceX IPO.

Lastly, it is worth mentioning that as core targets of MSX Q2 Top Picks, RKLB.M, YSS.M, BKSY.M, and PL.M all recorded positive returns, with an average gain exceeding 100%.

In Conclusion

Of course, while commercial space is worth long-term attention, it does not mean that any price is worth chasing.

SpaceX's current target valuation of approximately 1.75 trillion USD corresponds to a price-to-sales ratio close to one hundred times its revenue in 2025. This valuation suggests that the market has already factored in growth expectations for many years to come, including Starlink expansion, Starship maturity, AI computational power business emergence, and the future commercialization of space infrastructure.

If, after the IPO, performance growth slows below expectations, or Starlink user growth decelerates, or capital expenditures in the AI business continue to expand, valuation corrections could be very severe.

High valuation, in itself, is one of the greatest risks for SpaceX.

However, the real significance of the SpaceX IPO lies in its ability to help the market more clearly differentiate between core assets, comparable assets, and merely emotional assets.

For investors, what is most worth long-term focus in commercial space is not just the term "space" itself, but which companies can turn imagination into orders, orders into revenue, and revenue into cash flow after the cost curve declines.

Moving forward, the true watershed within the commercial space sector will no longer be about how grand the story is told, but rather who can prove their standing based on what.

The answer will soon be revealed.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。