Original author: The Flow Horse

Translation: Peggy, BlockBeats

Editor's note: In the context of super IPOs, AI narratives, and the repricing of risk assets, the market's discussion about SpaceX's listing is shifting from "how much is this company worth" to "how it will be traded after it goes public." However, as SpaceX becomes one of the most highly-watched tech assets, a more critical question arises: On the first trading day of a new stock with no historical prices, no mature options structure, and no clear chip distribution, should investors understand it through a valuation framework, or through market microstructure?

This article is a translation of The Flow Horse's video content focused on SpaceX's IPO trading strategies on its first day. The focus is not on discussing SpaceX's long-term fundamentals but rather on dissecting the cash flow, circulating shares, index inclusion, and lock-up pace that it may face in the early stages of trading. The video’s author is a market trader who has long focused on IPOs and order flow trading, whose perspective is closer to market levels and execution rather than traditional company valuation analysis.

In this content, SpaceX’s IPO is broken down into a set of more fundamental structural issues: It is not simply a "whether to buy or not" question, but rather a process of traders, retail investors, passive funds, and internal shareholders repricing around limited liquidity within different time frames.

First, retail investors are most likely to misjudge the opening day trading environment. In the past, when retail investors traded popular stocks, they often relied on trend lines, support and resistance, previous highs and lows, and opening momentum. However, SpaceX's IPO on the first day lacks historical charts, dense trading areas, and a mature options structure; prior to the first K-line, the market has no reusable price memory. What truly determines the short-term direction now are the order book, trades, VWAP, the opening range, and where buyers and sellers form genuine turnover. This means that if retail investors chase prices in the first wave of trading at the opening, or too early use technical analysis to find so-called trends, they might take on the highest risk before the structure is formed.

Second, past popular IPOs do not support the notion of "inevitably unidirectional rises in the initial listing period." Coinbase, Airbnb, and ARM all enjoyed high attention, yet they did not immediately provide a stable trend in their early days, instead first experiencing intense bidirectional volatility. In the past, the market often interpreted hot IPOs as a realization of emotional consensus; now it is more accurately understood that they often become places for short-term capital, profit-taking, and new buying to rotate. This means that even if SpaceX has a strong narrative and high subscriptions, it does not imply that it is suitable for trend followers in its first week. What is truly suitable for participating on the first day are traders who can quickly read order flows, manage positions, and accept bidirectional volatility.

Third, the strategy for the first day should shift from "predicting direction" to "waiting for structure." In the past, many traders were used to setting long or short viewpoints before the market opened, then validating their judgments with the first wave of prices. However, IPOs like SpaceX with low circulating shares need the market to first draw out the structure: Is there support around $135? Is the five-minute opening range effectively broken? Does VWAP bounce back and hold? Is there constantly refreshing hidden buying and selling power in Level 2? The core of trading now is not to jump to conclusions before everyone else but to assess who holds the upper hand once the market establishes the first batch of price coordinates. This means that the most important thing isn't to enter at the first minute, but to avoid being passively executed at the most chaotic, widest spread, and emotionally charged positions.

Fourth, investors must understand that different phases are dominated by different types of capital. In the first 15 trading days, SpaceX resembles a short-term trade driven by low circulating shares, emotional money, and order flow; around the 15th trading day, expectations for Nasdaq inclusion may bring in price-insensitive buy orders for a second phase; after the first earnings report, unlockings will begin to test the market's absorption; further down the line, the unlockings for major shareholders at 70 days, 90 days, 120 days, 180 days, and one year will gradually provide more reliable long-term signals. In the past, IPOs were often viewed as determining success or failure based on the price increase or decrease on the first day; now, SpaceX feels more like a series of continuous liquidity tests. This means that long-term judgments should not be based on first-day emotions but on whether the price can form a stable bottom following the entry of new supply into the market.

Fifth, trading in SpaceX may not only occur in SpaceX itself. Aerospace and space economy-related assets like Rocket Lab, LUNR, may become shadow stocks expressing the same theme during the listing period. In the past, IPO trading usually revolved around the main asset; now, when the main asset’s circulating shares are too low, volatility too high, and spreads too wide, related assets may instead provide a clearer trading structure. This means that market trading is not just about SpaceX's stock, but also about trading the industry narrative and liquidity spillover it activates.

If this article could be compressed into one judgment, it would be: SpaceX's IPO on the first day belongs to traders; long-term judgments need to wait for supply tests. For traders, the first day may be the "Super Bowl" of order flow trading; for investors, the increase or decrease on the first day should not be overly interpreted. In this sense, the core issue of SpaceX's IPO is no longer just whether it should be bought on the first day, but whether participants can first judge which game they are entering: watching order flow on the first day, observing supply absorption in the long term. Mixing these two aspects is the reason why most retail investors are likely to lose money.

Below are the video contents (rearranged for easier reading comprehension):

Why Most Retail Investors Might Lose Money in SpaceX IPO

The most dangerous aspect of SpaceX's first day is that many people will treat it like a regular popular stock.

Regular stocks have historical price ranges, previous highs and lows, dense trading areas, and enough market memory. Traders can refer to past support and resistance, moving averages, options positions, and capital costs. But the IPO's first day presents a blank chart. Before the first K-line appears, there is no real trading history in the market.

This means that drawing trend lines too early makes no sense, and chasing the first wave after the opening can easily be pierced by reverse fluctuations. Especially in a low circulating share environment, prices may rapidly spike due to short-term buying or suddenly retreat due to profit-taking or institutional supply. If retail investors only focus on price increases and emotions, they are likely to enter the most chaotic positions.

The true trading logic on SpaceX's first day is the real-time formation of the auction mechanism (i.e., buyers and sellers seeking transaction balance at different prices). What traders need to observe is: Who is willing to raise the bid? At which price points do sellers continuously replenish their stock? At which price levels do many trades occur but the price can't progress? This order book information is more important than any technical patterns drawn in advance.

Trading Details: $75 Billion Financing, 3% Circulation, and High Retail Distribution

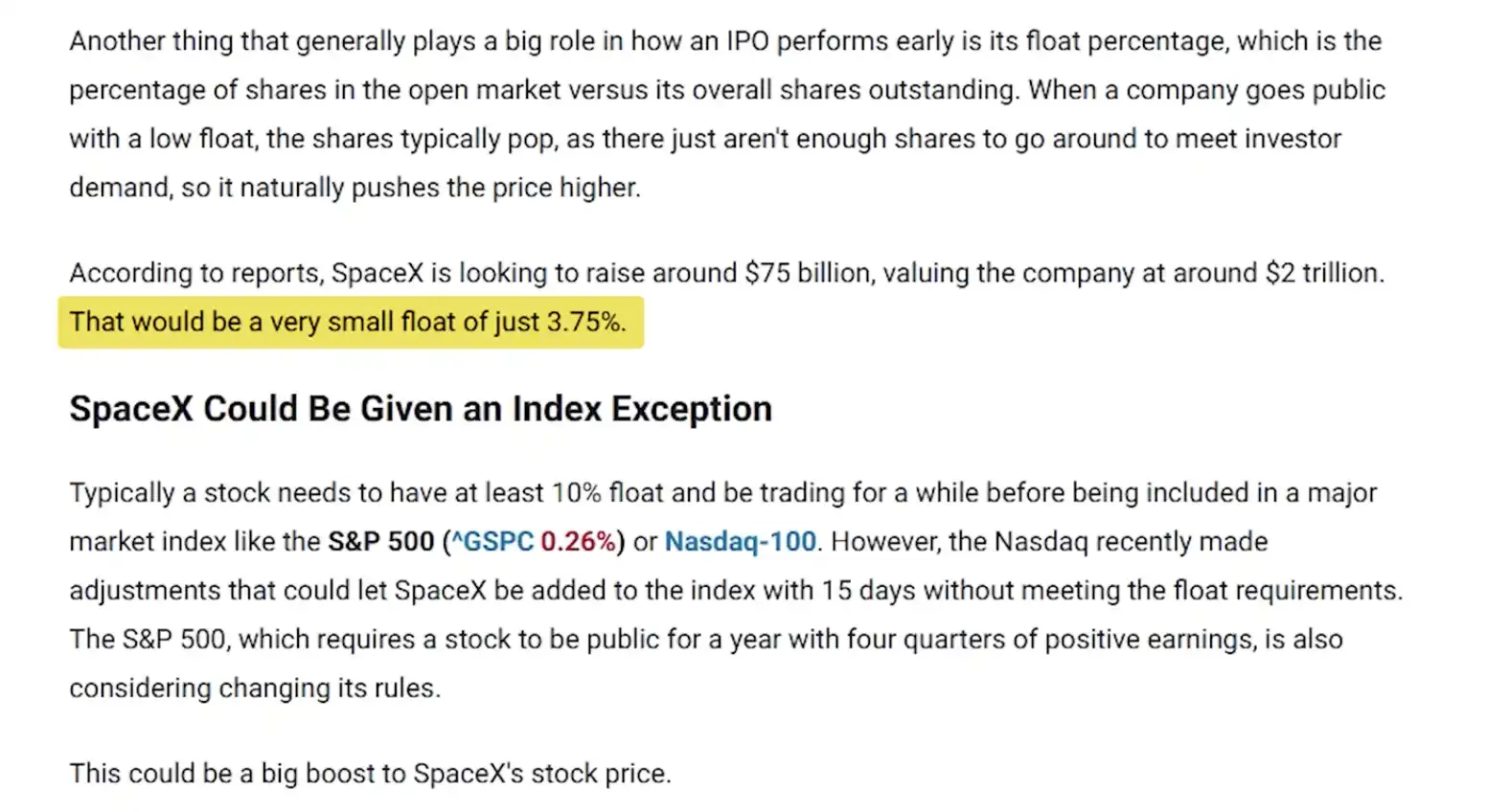

SpaceX's IPO plans to issue approximately 555 million shares, raising about $75 billion, with a pricing of $135 per share, bringing the overall valuation to approximately $1.7 trillion. This scale alone is enough to make it a market-level event.

However, what truly determines the volatility of the first day is not only the scale of financing, but also the circulating shares. Only about 3% of SpaceX's shares will be freely tradable at the beginning of its listing. This means that even moderate buying could have a significant impact on prices. Retail investors chasing prices, active funds building positions, and institutions buying small amounts could all cause the price to deviate from fundamentals in a short period.

Another special variable is the retail distribution. The retail distribution ratio in this offering could reach approximately 30%, which is about 3 to 4 times that of a typical IPO. This can make trading after the opening harder to judge. On one hand, more retail investors getting shares in advance could reduce the impulse to "chase after not being able to buy" on the first day; on the other hand, these investors who received shares in advance may also take profits right after the opening, forming the first wave of supply.

Therefore, the core of SpaceX's IPO is not simply to judge that "oversubscription equals good," but to understand the structure of the shares: an extremely low circulation will amplify both upward and downward movements, while high retail distribution may make both buying and selling on the first day more aggressive.

15th Trading Day: Nasdaq Inclusion May Change the Nature of Capital

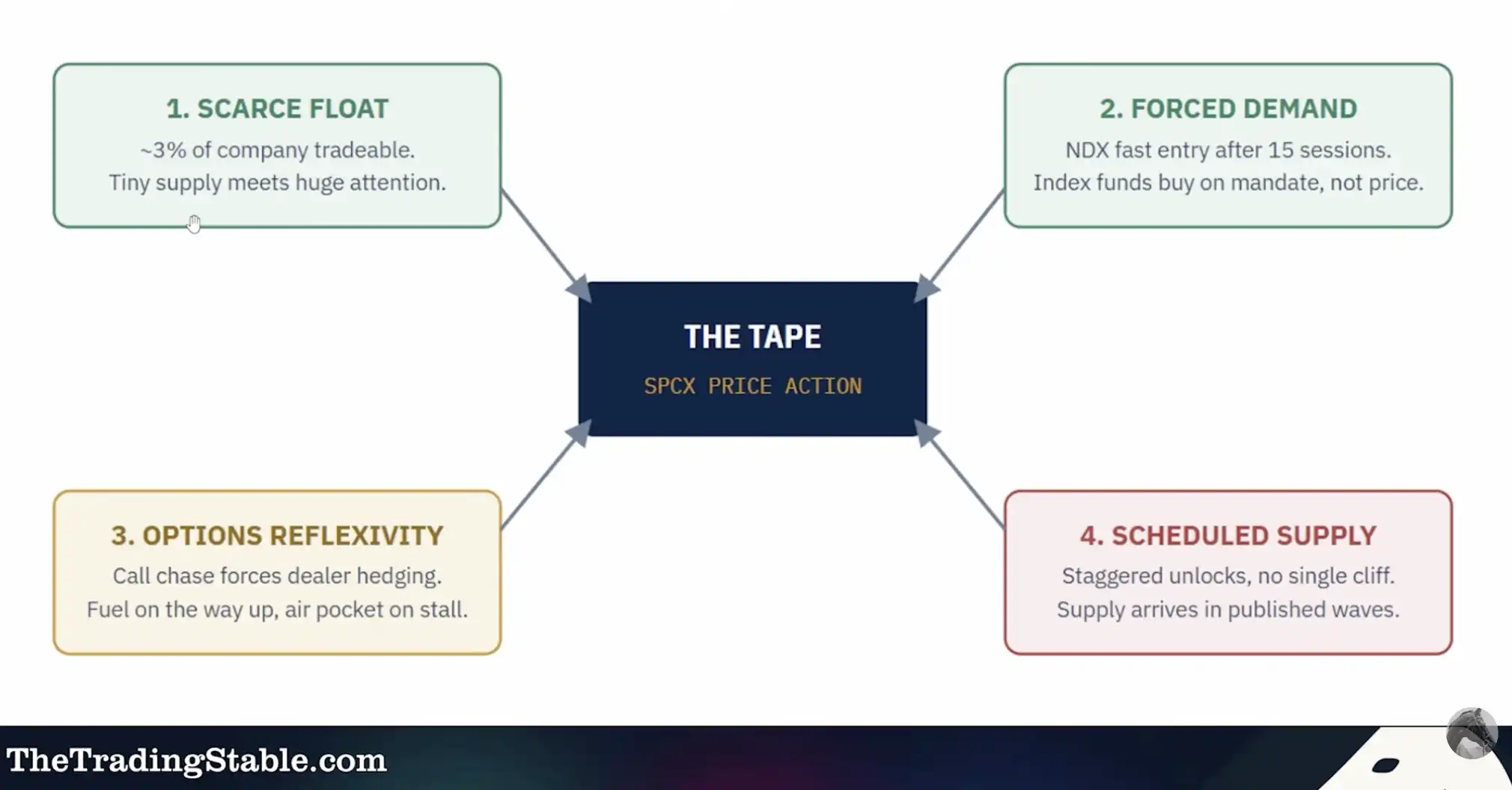

Another key time point is the 15th trading day after listing. According to its setting, SpaceX may be included in the Nasdaq 100 Index (NDX). This arrangement still needs to rely on final rules and actual results, but the corresponding trading logic is very important.

In the early stages of listing, the drivers of price are mainly fast money, retail investors, active funds, and emotional capital. These funds are sensitive to price, entering and exiting based on volatility. However, after index inclusion, another type of capital will be introduced to the market: passive funds.

The characteristic of passive funds is price insensitivity (i.e., they are bought not because they are cheap, but because of index rules or portfolio requirements). Index funds, ETFs, and related tracking products need to allocate component stocks according to rules; this type of buying is often more mechanical and easier to be anticipated by the market.

Therefore, before the 15th trading day, active funds may attempt to front-run (i.e., buying in advance before certain buying orders arrive). If SpaceX has already formed upward momentum in the early listing stages, the mechanical buying brought by index inclusion may further amplify the trend; but if the performance in the first two weeks is weak, this buying may not be enough to independently reverse the situation.

This makes the SpaceX IPO different from ordinary first-day trading: it is not a single-point event but a series of capital flow nodes.

The First Day is Order Flow Trading, Not Chart Trading

The most important judgment about SpaceX on the first day is: do not treat it as chart trading.

Ordinary traders are accustomed to asking: Where is the support? Where is the resistance? Where is the previous high? Where is the dense trading area? Where is the options' maximum pain point? But on the IPO's first day, most of these questions have no answers. Without historical charts, there is no reliable technical structure; without a mature options market, there are no reference options open interest.

The real issue on the first day is: Where do buyers and sellers reach an agreement? Where is there significant turnover? After the price breaks below the offering price, is there any buying support? When the price rises, is there continuous replenishment from sellers? This is the core of order flow trading.

The initial key price levels must be drawn by the market itself on that day. First is $135, the set offering price in the video. Traders must observe how prices perform relative to $135: Can it quickly regain after breaking below? Can it sustain after going above? If there is buying support each time the price is under $135, it suggests that this level may become an early cost anchor; conversely, if the price is sold off each time it goes above $135, it indicates stronger supply above.

Second is VWAP (Volume Weighted Average Price, representing the market's average transaction cost for the day). After the listing hour, whether the price remains above VWAP or below, and whether it can gain support when retesting VWAP will directly reflect who holds the active power between buyers and sellers.

Lastly, the high and low points of the first day. After the close, the highest and lowest price on the first day will become the most critical structural references for the next few days. For a stock without a historical chart, the price range on the first day serves as the first set of coordinates established by the market.

Four Types of Capital Flows Driving Prices

Price fluctuations during the early stages of SpaceX's IPO can be divided into four types of capital flows.

The first type is the scarcity buying brought by the extremely low circulation. A 3% circulation means that very few shares are available for trading; if demand is slightly concentrated, the stock price could rise rapidly. This is why blindly shorting on the first day is very dangerous. Low-circulation stocks do not necessarily keep rising, but they are most likely to "squeeze" shorts in a short time.

The second type is the passive buying from Nasdaq index inclusion. If SpaceX is included in the NDX on the 15th trading day, index funds and related products need to buy according to rules; this type of capital does not order based on valuation but based on index weight. For bulls, this is an ideal mechanical demand; for short-term traders, it is a time window that can be traded in advance.

The third type is options reflexivity (i.e., the options market affecting the underlying stock price). Once the options are listed, significant buying of call options by retail investors may force market makers to buy the underlying stock to hedge, thereby forming a gamma cycle (i.e., the buying of options pushes market makers to buy the stock to hedge, further amplifying the upward movement). However, this mechanism may not emerge immediately on the first day of listing, and it may not mature in the initial week.

The fourth type is unlocks (i.e., shares that were restricted from sale gradually entering the market). This brings new supply and is a risk point that all long-term investors must pay attention to. The unique aspect of SpaceX is that it may not wait for a one-time unlock after 180 days but may release chips in stages.

Unlocking Schedule: Not a One-Time Cliff After 180 Days

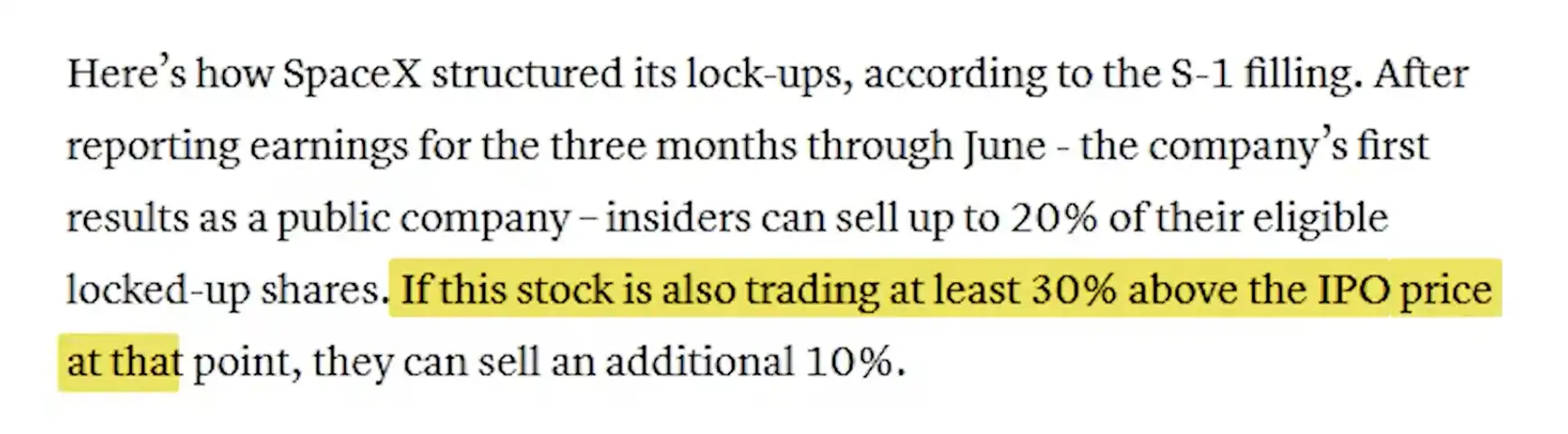

A common risk point in traditional IPOs is that after the end of the 180-day lock-up period, early investors' and employees' shares are concentrated in unlockings, suddenly flooding the market with significant supply. However, the unlocking structure given in the video for SpaceX is more complex: it may not be a one-time cliff, but rather a series of phased liquidity events.

First, after the first earnings report, up to 20% of qualified shares may unlock within 2 days. This means that the earnings report itself is not only a performance event but also a supply event. If the stock price is pushed up by emotions before the report, the new supply after the earnings report may suppress momentum.

Second, unlocks may also be tied to price performance. If in the 10 trading days before the earnings report, the stock price remains above $135 for more than 5 days by more than 30%, an additional 10% may be unlocked. This arrangement means that the increase itself triggers more supply, forming a dynamic balance: the stronger the price increase, the more shares may be available for sale later.

Subsequent nodes are equally important. The video mentions that on the 70th, 90th, and 120th days, approximately 7% of shares may unlock, with a further complete unlock after 180 days. For employee shares, approximately 5% may be sold immediately after the first earnings report, without needing additional performance or price conditions. Elon Musk and the largest shareholders may need to wait for more than a year, around 366 days.

These dates are especially important for long-term investors. To judge whether SpaceX forms a true bottom, one should not only look at the first-day increase or decrease but at how well buying can absorb new supplies each time they enter the market.

Lessons from Past IPOs: Coinbase, Airbnb, and ARM Did Not Provide a Unidirectional Trend from the Start

Popular IPOs easily create an illusion: since there is high market attention, the stock should rise steadily after listing. However, the early trading of Coinbase, Airbnb, and ARM shows that high temperature does not equate to a unidirectional trend.

The video mentions that these hot IPOs experienced significant volatility in their early days. Coinbase's early volatility reached approximately 119 points, Airbnb about 53 points, and ARM approximately 22 points. The key is not the specific numbers themselves but what they indicate: the first few days and weeks of popular IPOs are often characterized by intense bidirectional trading rather than stable trends.

This type of environment is more suitable for day scalpers (i.e., traders who profit by frequently entering and exiting based on short-term small fluctuations) and order flow traders rather than ordinary trend followers. Trend traders need structure, but what is most lacking in the early stage of an IPO is structure.

SpaceX may be more extreme. It has been highly oversubscribed and may allow more retail investors to receive allocations in advance. This means that after the opening, there will be both chasing funds and profit-taking funds; some want to buy in expectation of the index inclusion on the 15th day, while others see high momentum itself as an opportunity to sell. Both long and short forces being crowded together often results in not clean trends but high turnover, high volatility, and high noise.

First-Day Trading Strategy: Wait for the Market to Draw Structure Before Acting

The first rule for trading SpaceX on the first day is: do not chase the first wave at the opening.

The opening moment is usually the noisiest, with the widest spreads and the most extreme emotions. Especially in a low liquidity environment, the first wave of upward movement may simply be a brief sweep, and the first wave of downward movement may just be a drop caused by insufficient liquidity. The truly tradable structure needs to wait for the market to form.

The first observation point is $135. If the price briefly breaks below $135 and quickly regains, returning to the opening range and VWAP, it indicates there is real buying support below. Conversely, if the price repeatedly tries to hold above $135 but is sold back, it indicates that sellers may be in control.

The second observation point is the five-minute opening range (i.e., the high and low point range formed in the first five minutes after opening). Filtering noise using a five-minute or thirty-minute opening range can help avoid getting trapped in back-and-forth losses too early. If the opening range is narrow, subsequent breakouts become more significant, as many short-term positions are concentrated within a limited price range, leading to easier triggers for stop-losses and chasing orders once the price moves away from the range.

The third observation point is VWAP. After the first hour post-listing, if the price is operating above VWAP and quickly gains buying support while retesting VWAP, it may be a signal of bullish dominance. If the price stays consistently below VWAP, unable to rebound, it suggests the average transaction cost for the day is turning into resistance.

The fourth observation point is the "ghost level" (i.e., a position where there is hidden buying or selling power consistently absorbing trades). If a certain price level seems to have low orders but has continuous volume, and the price cannot break through, it may suggest there is hidden selling power consistently replenishing. Conversely, if a low level consistently executes trades but the price does not drop further, it may suggest hidden buying support is involved.

These temporary price levels may not be significant for the next few months, but they are crucial on the first day. Because in the absence of historical charts, they are the first markers generated by the market.

Position Control and Risk Management: Do Not Trade Low-Circulating New Stocks as Blue-Chip Stocks

SpaceX may have a large company size, but the trading characteristics in the early listing period do not necessarily resemble those of large blue-chip stocks.

If the circulation is only 3%, the order book may be thin, spreads may be wide, and prices may rapidly fluctuate due to successive sweeps. Combined with a potentially immature options market at the beginning, traders lacking hedging tools may amplify losses due to position size being too large, slippage, and halting risks.

Therefore, one cannot trade SpaceX with the position methods used for mature large cap stocks like Apple, Microsoft, or NVIDIA. New traders who simply want to learn about order flow should start with very small positions or even just observe without trading. For most people, the most significant issue is not missing the first-day opportunity but rather being driven by FOMO to enter heavily at the most chaotic positions, which is the greatest risk.

Short-term traders must accept one reality: the most important thing on the first day is not to profit from every fluctuation but to avoid being "washed out" by the market at positions without structure. Long-term investors should focus more on subsequent supply nodes rather than rushing to prove they were right about SpaceX on the first day.

Four Things You Must Understand

First, the first 15 trading days are likely driven by emotions. Extremely low circulating shares, enormous attention, and lack of technical standard points will make prices mainly rely on order flow and short-term capital pushes.

Second, the 15th trading day may be a node for changes in the nature of capital. If SpaceX is included in the Nasdaq 100, price-insensitive mechanical buying may enter the market, and active funds may trade this expectation in advance.

Third, the first earnings report is not only a performance event but also a point of supply pressure. Some shares may begin to unlock after the earnings report, and the market needs to prove it can absorb the new supply.

Fourth, unlocking is not a one-time event but multiple liquidity tests stretched over the next year. The unlocking events at 70 days, 90 days, 120 days, 180 days, and even a year later will all re-examine the true buying foundations of SpaceX.

Noteworthy Shadow Stocks of SpaceX

During SpaceX's listing period, related industry proxy stocks (i.e., alternatives used to express similar themes or risk exposures when the core assets cannot be traded directly) are also worth attention.

Aerospace, defense, rocket launches, satellite, and space economy-related stocks may receive capital spillover due to SpaceX's market heat. Examples mentioned in the video include Rocket Lab (RKLB) and other space-related assets.

The opportunity of these shadow stocks lies not in their guaranteed benefits but in their potential to serve as alternative pathways for capital expressing the SpaceX theme. Especially when the spreads, volatility, and circulation of SpaceX itself are too large, some related assets with better liquidity may provide clearer trading structures.

However, proxy trading must be based on market verification. If related assets only temporarily trend upward without volume, continuity, or relative strength, one cannot forcefully apply the SpaceX logic to them.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。