Written by: Rita

Trends Guide

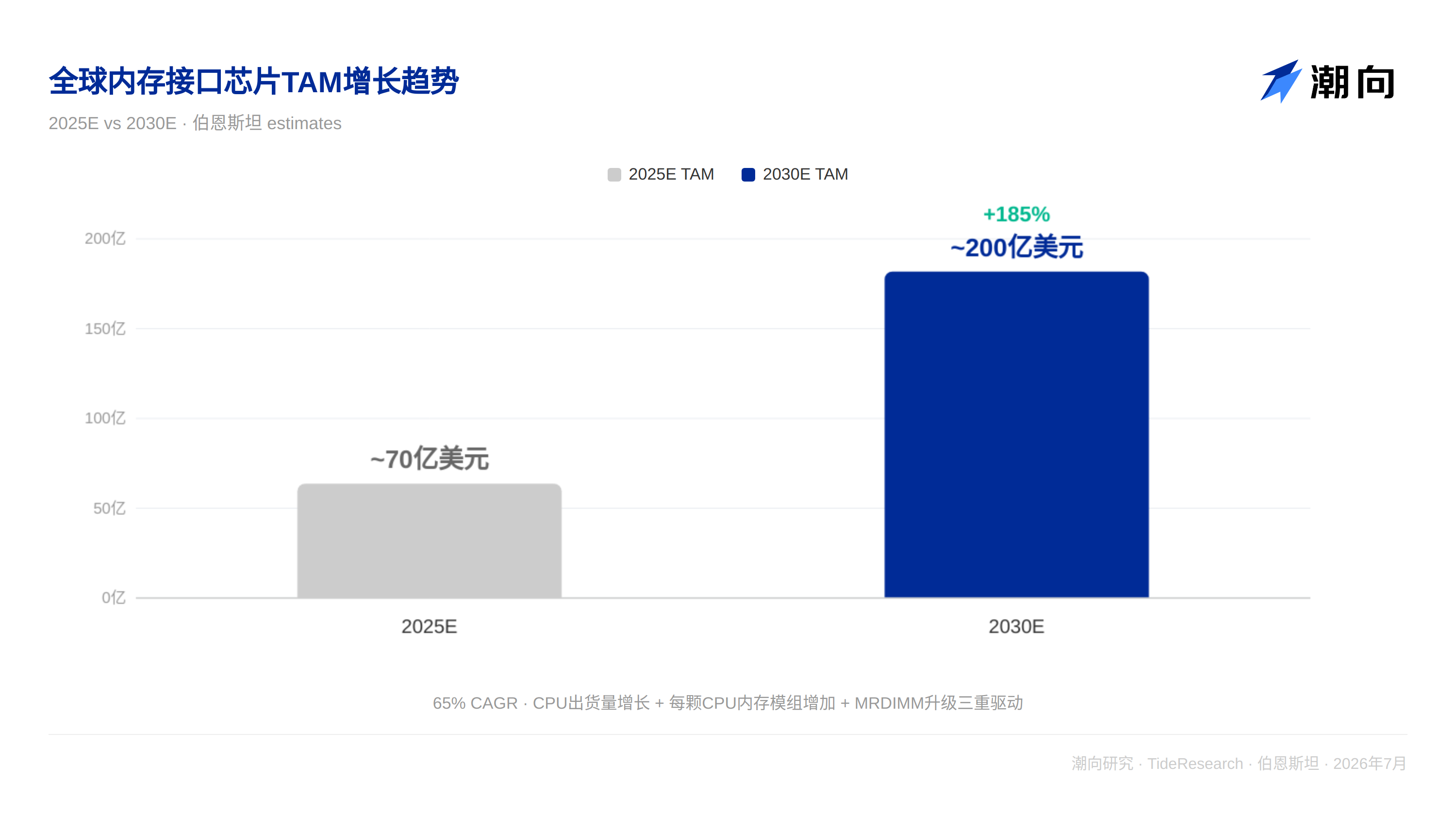

Bernstein released a deep dive report on storage interface chips on July 9, stating that AI is evolving from being training-intensive to being inference-intensive, with CPUs reassuming their role as the core orchestrators in AI workloads, driving structural growth in server CPU shipments. The report significantly raised the global memory interface chip Total Addressable Market (TAM) forecast to $20 billion by 2030 (previously around $7 billion), corresponding to a 65% five-year compound annual growth rate. The target price for Changxin Technology's A-shares was raised from 220 yuan to 400 yuan, and for H-shares from 320 Hong Kong dollars to 520 Hong Kong dollars, both maintaining an outperform rating. Renesas Electronics has a target price of 6,300 yen, also maintaining an outperform rating.

Three Major Drivers Combined, TAM Jumps from 7 Billion to 20 Billion

Bernstein judges that memory interface chips are encountering a rare window of triple structural benefits concurrently.

The first layer is the accelerated growth in server CPU shipments. In AI workloads, CPUs handle tasks such as scheduling, KV cache management, and real-time security checks, which can account for 50% to 90% of task completion time. AMD recently doubled its global x86 server CPU TAM forecast for 2030 to $120 billion, affirming this trend. Bernstein expects global server CPU shipments (excluding Nvidia's proprietary CPUs) to increase from 30.6 million units in 2025 to 89.3 million units by 2030, corresponding to a 24% annual compound growth rate.

The second layer is the continuous increase in the number of DRAM modules per CPU. AI servers typically raise DIMM slot utilization rates to 70% to 80% to maximize accelerator utilization, significantly higher than the approximately 50% of general servers. As the number of CPU channels evolves from 8 to 12 and 16 channels, the demand for memory interface chips per CPU directly doubles.

The third layer is the leap in single-module value brought by MRDIMM upgrades. MRDIMM uses a "1 MRCD + 10 MDBs" architecture, while traditional RDIMM requires only 1 RCD. The value of single-module memory interface chips skyrockets from about $7 to $70 to $80, improving nearly tenfold. Bernstein expects the penetration rate of MRDIMM to increase from about 3% in 2026 to 25% by 2030.

The three major driving forces create a multiplier effect rather than simply adding together. Bernstein adjusted the 2030 TAM from about $7 billion to $20 billion.

Why Can MRDIMM Succeed? Three Structural Differences

The most frequently asked question in the market is: Why did LRDIMM in the DDR4 era never exceed 1% penetration, and what makes MRDIMM different?

Bernstein provided three structural differences. First, LRDIMM addresses error issues; it increases capacity but not bandwidth, while capacity was not a bottleneck during the DDR4 era. MRDIMM solves both capacity and bandwidth dimensions, with its reuse architecture doubling the single-module bandwidth, directly addressing the bandwidth bottleneck in AI workloads. Second, RDIMM was "good enough" during the DDR4 era, but it cannot maintain signal integrity at speeds above 8800MT/s in DDR5; the transition to MRDIMM is driven by physical laws rather than marketing push. Third, neither Intel nor AMD has released product roadmaps for DDR5 LRDIMM, while MRDIMM has clear support from both CPU platforms.

Additionally, AI servers have created a customer base that did not exist during the DDR4 era; these servers fill DIMM slots to capacity and push every specification to the limit, making them the most natural customer group for the bandwidth-focused MRDIMM. Rising DRAM prices are also narrowing the cost gap between MRDIMM and RDIMM, further reducing migration resistance.

Oligopoly Structure: Three Companies Control Over 90% of Market Share, Significant Barriers

The memory interface chip market is a textbook case of oligopoly. Changxin Technology (about 37%), Renesas (about 36%), and Rambus (about 20%) together account for approximately 92% of the global market share.

The entry barrier is extremely high. JEDEC standard certification requires chips to pass validation from multiple parties including DRAM manufacturers, CPU platforms, module manufacturers, CSPs, etc., with the entire process typically taking 18 to 24 months. Any design flaw or interoperability failure can lead to the complete elimination of suppliers. Moreover, RCD and MRCD are the most technologically complex components in the DIMM chip set, using the most advanced CMOS processes; DDR4 RCD began on a 40nm platform while the first-generation DDR5 RCD started at 28nm, with future advancements heading below 10nm. All three suppliers are deeply involved in the formulation of JEDEC standards; Changxin and Renesas are also board members of JEDEC, setting the benchmarks that new entrants must cross while defining the standards.

In the MRDIMM sector, Changxin and Renesas jointly lead the first generation of products, while Rambus chose to skip the first generation and directly enter the second generation. The competition for the second-generation MRDIMM (12,800MT/s) will be more balanced.

Changxin Technology: AI Scarcity Target, H-shares Enjoy a Premium

Bernstein raised the target price for Changxin's A-shares to 400 yuan (previously 220 yuan), based on a 50 times rolling price-to-earnings ratio for Q3 2027 to Q2 2028; the target price for H-shares is 520 Hong Kong dollars (previously 320 Hong Kong dollars), implying about a 15% premium over A-shares.

The H-share premium reflects global investors viewing Changxin as a scarce exposure to Chinese AI, unlike other Chinese semiconductor companies, which face direct geopolitical risks from entity lists or export controls. The limited circulation of H-shares due to lock-up periods indicates that the premium is likely to be maintained in the short term.

Changxin's growth drivers are threefold: the increasing penetration of MRDIMM leading to volume growth in interface chips, growing memory interface demand driven by rising CPU shipments, and contributions from new businesses such as PCIe Retimer. Bernstein predicts Changxin's EPS will reach 5.68 yuan and 10.82 yuan in 2027 and 2028, respectively.

Trends Perspective

The core judgment of Bernstein’s report is that memory interface chips are transitioning from a supporting role of "following the DRAM cycle" to being a direct beneficiary of "AI computing power expansion." The reassessment of CPUs' role in the era of AI, shifting from being "observers" during training to "conductors" during inference, is the starting point of the entire logic. The multiplier effect of the three driving forces allows the TAM to jump from about $7 billion to $20 billion, an increase of this magnitude is exceptionally rare in the semiconductor sector.

Whether MRDIMM can succeed is a key variable in validating the whole narrative. The lessons from LRDIMM's failure indicate that technological upgrades must simultaneously address real bottlenecks (bandwidth rather than capacity), secure clear support from CPU platforms, and have a sufficiently large customer base. The explosion of AI servers precisely meets these three conditions.

The premium of Changxin's H-shares relative to A-shares deserves attention. The premium due to limited circulation in the Hong Kong market may be sustained in the short term; however, there is a risk of narrowing after the lock-up period ends. For A-share investors, the scarcity logic of Changxin and the premium logic of H-shares are completely opposite; A-shares do not suffer from geopolitical discounts but also miss out on the scarcity premium of H-shares. The dynamic changes in the price difference between the two markets themselves serve as a transaction signal worth tracking continuously.

Disclaimer

This article is a compilation and interpretation by Trends Research of a third-party brokerage report (Bernstein, July 9, 2026). The ratings, target prices, earnings forecasts, and related judgments quoted in the text represent the views of the brokerage's analysts, reflecting the stance of their institution and not the views of Trends Research, nor does it constitute any investment advice.

The market is risky, and decisions should be made independently. This article should not be used as a basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。