The result depends on where the liquidity of the tokenization wave ultimately flows.

Written by: Liam Akiba Wright

Translated by: Luffy, Foresight News

TL;DR:

- According to reports, Standard Chartered has released a research report on Uniswap, setting a target price of $100 for the UNI token by 2030.

- The core logic of Standard Chartered is that tokenized assets will generate demand for open DeFi liquidity, and Uniswap is expected to handle a large number of transactions and earn fees.

- However, most institutional-level tokenization products employ access controls, and BlackRock's BUIDL product has also proven that there are still entry barriers in the DeFi field.

Standard Chartered has set a target price of $100 for the UNI token by the end of 2030, a prediction that means this leading decentralized exchange governance token's price will far exceed current market levels.

The argument from Standard Chartered is that various types of tokenized assets will require decentralized trading platforms, transforming fragmented on-chain financial tools into tradable liquidity.

Standard Chartered estimates that by 2028, the total size of global tokenized assets could reach $40 trillion; and by 2030, the share of tokenized assets flowing into the DeFi market is expected to increase from the current approximately 3.5% to 30%. Based on this calculation, the asset size supported by the DeFi market is likely to exceed $20 trillion by 2030.

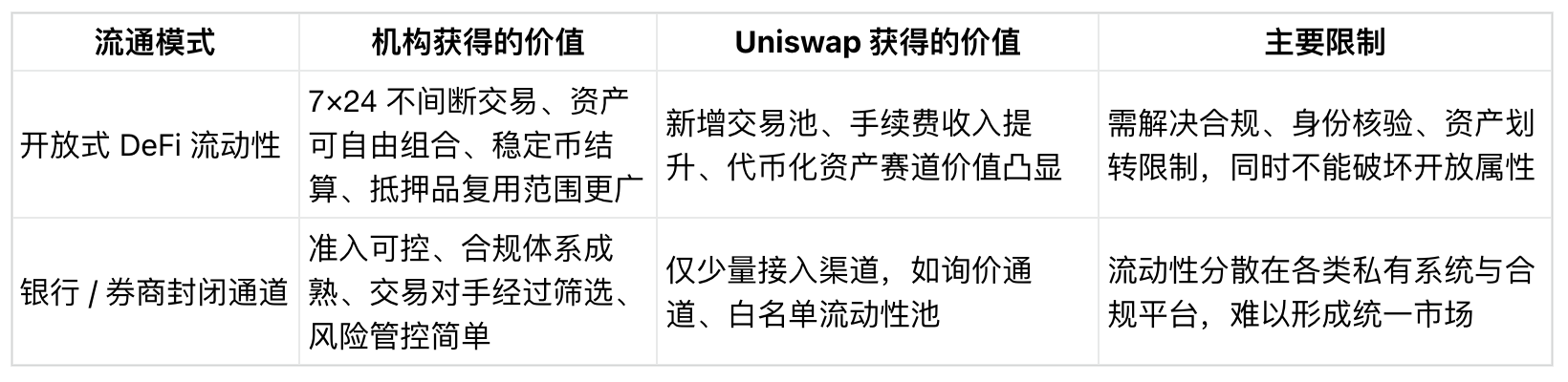

Currently, banks, asset management institutions, transfer registration service providers, and compliance platforms are all positioning themselves in the asset tokenization field. However, if these assets require 24/7 trading, flexible collateralization, and cross-product portfolio capabilities, and a single institution's proprietary system cannot meet these needs, then open decentralized protocols will capture the liquidity dividends.

Given the current market environment, core industry questions have emerged: Will tokenized on-chain assets such as treasury token, fund tokens, stock tokens, and stablecoins become liquidity targets of the open decentralized market, or will they always be restricted within a closed system, which has strict access controls and complete management of settlements?

Growth prospects depend on open liquidity

The valuation target provided by Standard Chartered is built on several assumptions: First, the market size for tokenized assets significantly expands; second, a considerable portion of tokenized assets is no longer purely dormant on-chain, merely acting as compliant packaging for ownership registration, but is actually active in the DeFi market; and finally, Uniswap must capture a sufficient share of related trading to boost the value of the UNI token. The core of this entire logic has shifted focus from the asset issuance stage to the liquidity trading stage.

Standard Chartered has long regarded asset tokenization as a significant long-term opportunity. In a report jointly published in 2024 with consulting firm Synpulse, the bank predicted that by 2034, the global tokenization of real-world assets could reach $30.1 trillion, with trade finance being one of the core application tracks. The report also mentioned that tokenization will spur entirely new DeFi applications and business models.

Citi's tokenization report released in June 2026 has a similar assessment of the market size but also presents counteracting factors: their baseline scenario forecasts a tokenized asset scale of $5.5 trillion by 2030, and the optimistic scenario predicts $8.2 trillion. The report also points out that a hybrid model may dominate, where institutions control the issuance, distribution, and settlement channels.

The divergence between these two paths directly determines the development space for Uniswap. If the size of tokenized assets continues to grow but their value remains locked within bank platforms, transfer service providers' systems, broker networks, and compliant trading markets, then the development space for open DeFi will be quite limited.

Conversely, if various tokenized financial instruments, stablecoins, and collateral assets require free trading across categories, the industry position of protocols like Uniswap will be greatly enhanced.

Data from DeFiLlama confirms that Uniswap has the foundation to meet this demand. As of the time of writing, the protocol's total locked value across multiple chains is approximately $2.89 billion, with fees exceeding $50 million in the past 30 days.

The existing data only represents the basic operational scale, but it does indicate that Uniswap is positioned as a liquidity infrastructure.

For institutions, there are clear operational differences between the two. Issuing fund tokens is a process, while building a trading venue that allows for free conversion of tokens with stablecoins, collateral, and other token assets is a separate operational business.

The gap between the two determines whether automated market maker Uniswap can become a necessary infrastructure or merely serve as a marginal supportive channel.

Thus, it is evident that the choice of trading channels is as important as asset issuance. Liquidity determines whether tokenized products can form a tradable market, reusable collateral, and settle assets; otherwise, they will merely become static ownership certificates within a compliance system.

BlackRock BUIDL: Connecting DeFi, but building access gates

BlackRock’s BUIDL institutional digital liquidity fund is a real case that evidences this contradiction. In February of this year, Uniswap Labs and compliance platform Securitize jointly announced that BlackRock's dollar institutional digital liquidity fund BUIDL would be accessible on the UniswapX trading channel.

This integration uses a request-for-quote trading mechanism that is only open to whitelisted users and pre-approved participants.

CryptoSlate’s previous reporting on BUIDL highlighted the core contradiction: although BUIDL holders can exchange USDC through UniswapX, the trading rights come with strict access thresholds.

The trading process relies on DeFi technology, but the asset circulation range is limited to approved institutional participants.

The initial issuance rules of BlackRock BUIDL fully reflect this control model: the product is only targeted at qualified investors, with a minimum investment amount of $5 million, assets can only be transferred to pre-approved parties, and it is not traded on any exchanges.

RWA.xyz data shows that on June 16, the total assets of BUIDL were approximately $2.37 billion, with only 108 holders.

Combining the access rules, it is not difficult to see the current state of the tokenization industry. Large-scale tokenized products can be born on-chain, but participation rights are highly concentrated with comprehensive access controls.

Standard Chartered's investor roadshow materials from May 2026 also once used BUIDL's access to Uniswap as an example to argue that decentralized platforms can be used for asset distribution and trading.

Even though a complete UNI valuation research report has not been publicly released, this roadshow material has categorized Uniswap as a foundational infrastructure for institutional digital assets, which underpins the $100 target price.

The BlackRock BUIDL model is between the two, utilizing Uniswap's technology at its core, but retaining institutional access control throughout. This design builds a bridge to DeFi infrastructure while not placing tokenized assets completely into an unrestricted open liquidity pool.

Liquidity solutions accepted by institutional assets are likely to initially adopt this compromise model: leveraging DeFi infrastructure for trades and settlements while imposing rigid restrictions on user identities, asset transfers, transaction counterparties, and self-controlled secondary market layouts.

UNI still lacks value capture mechanism

Even if Uniswap handles more real-world tokenized asset transactions, it does not mean that UNI holders will directly benefit, as the protocol still lacks a stable value capture mechanism.

Previously, proposals passed by the community on the Tally platform for the UNI token economics upgrade outlined the distribution of protocol fees and the UNI burn mechanism, while also proposing that Uniswap should become the default trading hub for tokenized assets.

This plan provides a path for valuation logic to land, but it comes with multiple prerequisites: community governance decisions, fee adjustments, institutional commercial collaborations, and real trading volume growth, all of which are essential.

Standard Chartered's $100 target price not only far exceeds the current market situation but even surpasses UNI’s historical peak in 2021. This target cannot be supported solely by asset issuance growth; it must rely on real continuous trading flow, stable fee income, and a clear mechanism linking protocol development with token value.

The core contradiction in the institutional tokenization track is that banks and asset management institutions require decentralized capabilities such as on-chain settlement, 24/7 transfers, programmable collateral, and stablecoin payments, while insisting on KYC identity verification, asset transfer restrictions, designated counterparties, and self-control over secondary market layouts.

The Financial Stability Board's research report on tokenization also confirms this cautious stance. The report notes that the overall scale of current tokenization is still small and that the industry faces multiple issues, such as closed access, insufficient cross-platform interoperability, limited settlement assets, and fragmented trading platforms.

These frictions are at the core of the barriers preventing tokenized assets from becoming general liquidity targets in DeFi.

If these industry barriers persist long-term, Uniswap will merely become a marginal supportive channel within the institutional tokenization ecosystem; if the related pain points gradually ease, the protocol will become the core trading venue for token funds, stablecoins, and native crypto assets.

Ultimately, the core of Standard Chartered's valuation prediction depends on where the liquidity of tokenization ultimately flows. The $100 target price represents considerable upward potential, while the more critical signal is that a traditional Wall Street investment bank has recognized the opportunity for DeFi protocols to partake in the institutional tokenization wave.

The BlackRock BUIDL case has already demonstrated that asset management institutions can utilize DeFi technology while maintaining strict circulation control; Citi's outlook on the tokenization industry also suggests that Wall Street is likely to build a hybrid system that firmly controls issuance, distribution, and settlement within institutions; while various industry pain points raised by the Financial Stability Board highlight that interoperability and settlement systems remain core challenges in the industry.

Future market signals will come from more cases of tokenized assets being integrated. If new assets adopt isolated whitelisting request channels, open DeFi can only capture a small share of the market; if unified cross-asset liquidity pools gradually come into play with reduced custom management rules, Uniswap's positioning in the tokenization track will no longer be limited to native cryptocurrency exchanges.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。