Every Monday, Wednesday, and Friday, we analyze the market through data retrospectives and capture opportunities through trends, covering macroeconomics, U.S. stocks, precious metals, crude oil, and crypto assets, providing insights into key global market changes, produced by PANews.

Macroeconomic Market

The main line of global macro trading is shifting from "geopolitical shocks" to "policy and liquidity reassessments." The core driver comes from the promotion of a temporary peace framework between the U.S. and Iran, with a memorandum of understanding expected to be formally signed on June 19. The core of the agreement is to immediately lift sanctions on Iranian oil exports and gradually restore shipping order in the Strait of Hormuz.

WTI crude oil has dropped nearly 6% to around $75, and Brent crude has fallen below $80 for the first time in over three months. Traders generally believe this round of adjustments is not due to a deterioration in demand, but rather a "decreased probability of war → return of supply expectations" driven by pure speculation. Meanwhile, there are still evident divergences in the oil market structure: On one hand, the market expects maritime transport to return to normal within 30 days, but on the other hand, the navigation rules in the Strait of Hormuz, potential "navigation fee disputes," and the $300 billion reconstruction funding mechanism have yet to materialize, making "peace narrative ≠ full restoration of supply."

In the precious metals sector, gold maintains slight fluctuations, while silver follows suit but lacks a trend breakthrough. The market sees it more as a "tail protection asset" against FOMC and geopolitical execution risks rather than a trending safe-haven situation.

The current market focus has shifted to the "debut" interest rate decision meeting of the new Federal Reserve Chair Powell. Although the market widely expects the benchmark interest rate to remain unchanged at 3.5% to 3.75%, significant policy signals may be about to change. Due to inflation surpassing 4% and demand pressure from AI investments, discussions regarding interest rate cuts within the Federal Reserve have basically disappeared, focusing instead on whether to raise rates. Key highlights include: the post-meeting statement may remove "easing bias" wording and the quarterly "dot plot" expectations may shift from rate cuts to maintaining or raising rates.

Before the FOMC meeting, the market has entered a liquidity contraction window, with the 10-year U.S. Treasury yield fluctuating around 4.3%, and risk assets are generally in a deleveraging state. Due to the U.S. stock market being closed on June 19, June 18 has become the only complete trading window before the major pricing center globally briefly steps back, with the market passively entering an early adjustment and concentrated volatility release phase.

Next, we need to focus on:

June 18 at 02:00 U.S. FOMC rate decision + 02:30 Powell press conference: If the dot plot is weakened or there are incomplete disclosures in the framework, or if Powell releases hawkish signals, it will directly raise the pricing of real interest rates, reshape the global interest rate curve, and compress the valuation center of NASDAQ and high beta AI assets, triggering systemic deleveraging.

June 19 U.S.-Iran agreement signing date: If the pace of lifting sanctions exceeds expectations, oil may enter the next round of rapid repricing range, further approaching the $70 center.

U.S. Stock Market Dynamics

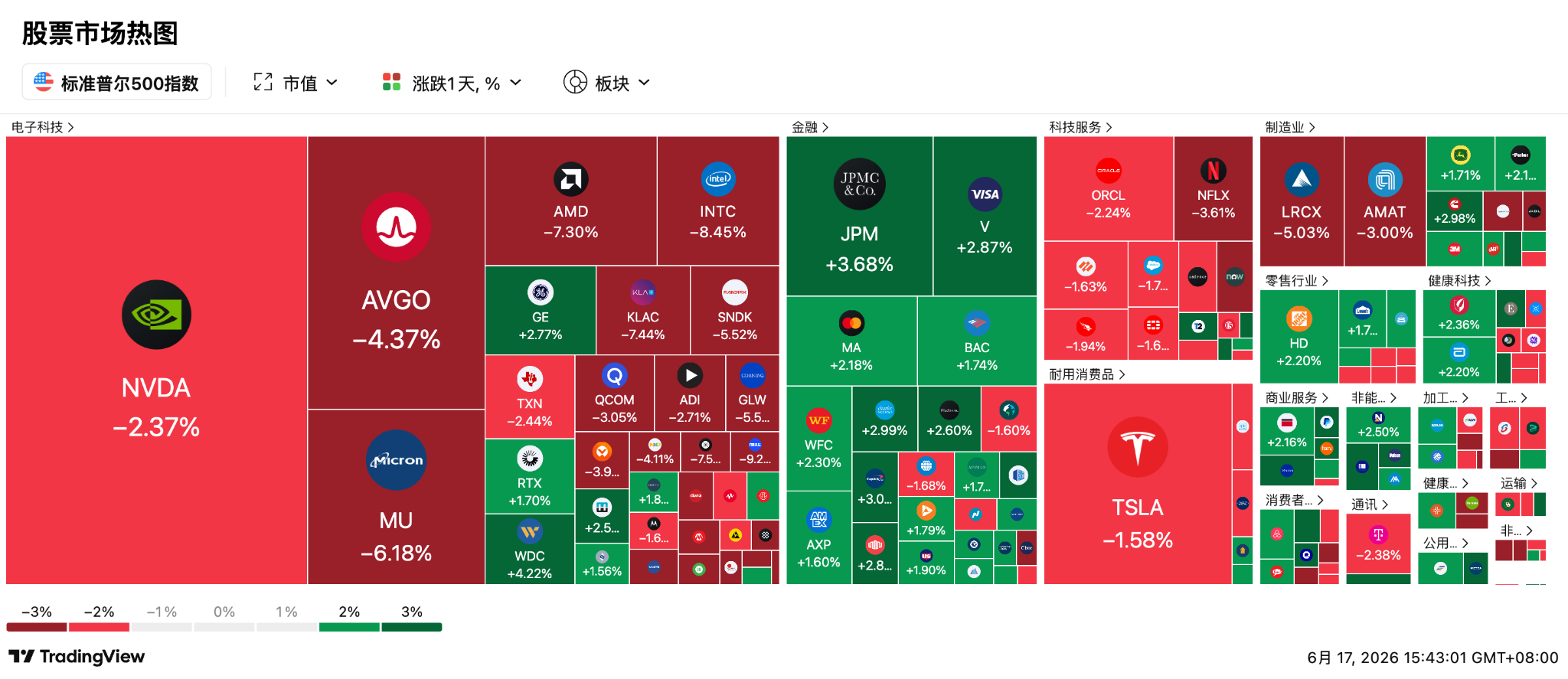

The Dow Jones Industrial Average has set a historical high for the fourth consecutive day, surging 0.64% to 51,999.67 points. However, the collapse of tech stocks has dragged the NASDAQ index down sharply by 1.15%, and the S&P 500 index fell by 0.57%. Academy Securities' Peter Tchir pointed out that the market is being forced to digest a large volume of IPO supply; should the S&P 500 break below 7,530 points in the short term, it will directly probe into the deep water area of 7,480-7,450.

The Philadelphia Semiconductor Index plummeted by 5.71%, with Marvell Technology down 9.8%, and Intel and AMD dropping 8.5% and 7.3%, respectively. Keyence Semiconductor fell over 7%, and Micron dropped 6.2%, with even Nvidia (down over 2%) and TSMC ADR (down over 3%) failing to escape the downturn.

The primary reason for this large drop is Microsoft's decision; Microsoft not only canceled a $3 billion Oracle cloud leasing agreement, but its vice president Charles Lamanna also indicated that Copilot will move to "pay-as-you-go" billing, considering replacing expensive closed-source models with open-source models like DeepSeek V4. Additionally, OpenAI's net loss of up to $38.53 billion last year further exposes the financial stress facing AI infrastructure.

SpaceX options officially launched trading on Tuesday, igniting the market on the first day, with call option trading volume nearing 1 million contracts, ranking fifth among all U.S. options types. SpaceX stock surged nearly 5% to $201.80 that day, hitting an intraday high of $225.64, now up about 50% from its IPO price of $135, with a market valuation reaching $2.65 trillion, successfully surpassing Amazon. Many large funds are frantically buying call options, betting on further price surges. Meanwhile, some institutions are more cautious, buying put options to "buy insurance," preventing potential declines after future stock unlockings.

Next, we need to focus on:

June 18 SpaceX weekly options are expected to go live: The launch of more derivatives may further attract retail speculative funds in the tech sector.

July 7 NASDAQ-100 officially includes SpaceX: If the passive investment scale reaches $8-18 billion, it will create a stage demand-supply mismatch with the extremely low float, amplifying price volatility.

Late July SpaceX Q2 earnings report and unlocking period: A 10-15% early unlocking stock sell pressure will test the floor of institutions like Ron Baron in terms of market support.

Cryptocurrency

Bitcoin maintains a range fluctuation structure, with the market forming a short-term bullish-bearish boundary around $64,000. Analysts generally believe that the current structure lacks trend-driving forces, as the overall market enters a macro waiting phase.

Structurally, resistance is concentrated at $68,500 (weekly 200EMA), and support is at $62,000 (weekly 200MA), forming a typical mid-range fluctuation structure.

At the same time, risk signals from institutions are frequently emerging. Strategy Preferred Stock STRC plummeted to $91.79, raising market concerns about debts, and Strive SATA faced heavy losses due to zero debt issues.

Analysts warn that if Bitcoin breaks below $64,000, it may retest the $60,000 support level, while $48,300 is seen as a structural iron bottom.

Points for today:

Binance Wallet's eighth Prime Sale Pre-TGE will launch Re (RE)

Spark (SPK) will unlock about 900 million tokens on June 17, valued at approximately $17.8 million

YZY (YZY) will unlock about 20.83 million tokens on June 17, valued at approximately $6.2 million

Upbit 24-hour trading volume ranking: WLD, XRP, XLM, SPX, JTO

Bitcoin spot ETF: +$10.0643 million

Ethereum spot ETF: +$9.5876 million

HYPE spot ETF: +$8.6205 million

Today, the top gainers among the top 100 cryptocurrencies by market cap: LAB up 36%, SPX up 24%, UNI up 22%, AERO up 11%, H up 6.9%.

Asia-Pacific Market

The Asian market is in a "holding breath mode" amid uncertainties regarding U.S. and European policies. The Nikkei 225 index rebounded quickly after a lower start, eventually rising and re-standing above 70,000 points, setting a new historical high. Despite the poor performance of the U.S. semiconductor industry causing a 5% drop in SoftBank Group's stock price, the sharp decline in oil prices due to the U.S.-Iran peace treaty draft has reduced Japan's manufacturing dependency on energy imports, leading to high expectations for subsequent guidance from the Bank of Japan.

The South Korean market, however, is under significant pressure, with the KOSPI index falling about 1%. The Middle East conflict has led to a sudden drop of 40,000 jobs in May, creating the lowest record in 17 months. Technology stocks suffered severe damage, with Samsung Electronics falling over 3%, and Samsung Electro-Mechanics and Hyundai Motor both dropping over 2%. In response, the South Korean Ministry of Finance has urgently pledged to take employment revival measures to address the current predicament. However, on the other hand, South Korean retail investors, referred to as "Western Ants," have displayed extreme investment enthusiasm, buying $795.93 million worth of SpaceX stocks in a single day, setting a historical high, betting real capital on the future of Musk-related stocks.

The Chinese market shows characteristics of "policy-driven + structural rotation," with the Shanghai index turning red after probing the bottom, while the Shenzhen Component Index and the ChiNext index rose. A-shares in AI hardware, PCBs, and copper-clad laminates strengthened, with leading companies like BOE Technology Group hitting the ceiling; however, the consumer and automotive sectors are under pressure. Hong Kong stock movements are similarly mixed, with the Hang Seng Index slightly down, but technology stocks performing strongly, with Kuaishou rising over 3% and MINIMAX surging over 8%.

Positive policy news has emerged, with the Lujiazui Forum releasing multiple measures for financial openness and reform of the technology capital market, including expansion of the Sci-Tech Innovation Board to AI large models, pilot foreign exchange futures for RMB, and expansion of REITs, enhancing expectations for the dual main line of "technology + capital market."

Next, we need to focus on:

June 19 China A-shares and Hong Kong stocks will be closed: The Asia-Pacific market may bear "unilateral pricing volatility," with increased volatility in the Nikkei and Korean stocks.

The pace of landing specific details of China's policies: If AI and REITs accelerate, it will strengthen the structural market conditions for risk assets in the medium term, rather than index-type markets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。