The booming tokenized stocks are actually just a way for traditional capital to take over?

Written by: Ignas | DeFi Research

Translated by: Saoirse, Foresight News

I think there is only one way to make big money with tokenized stocks.

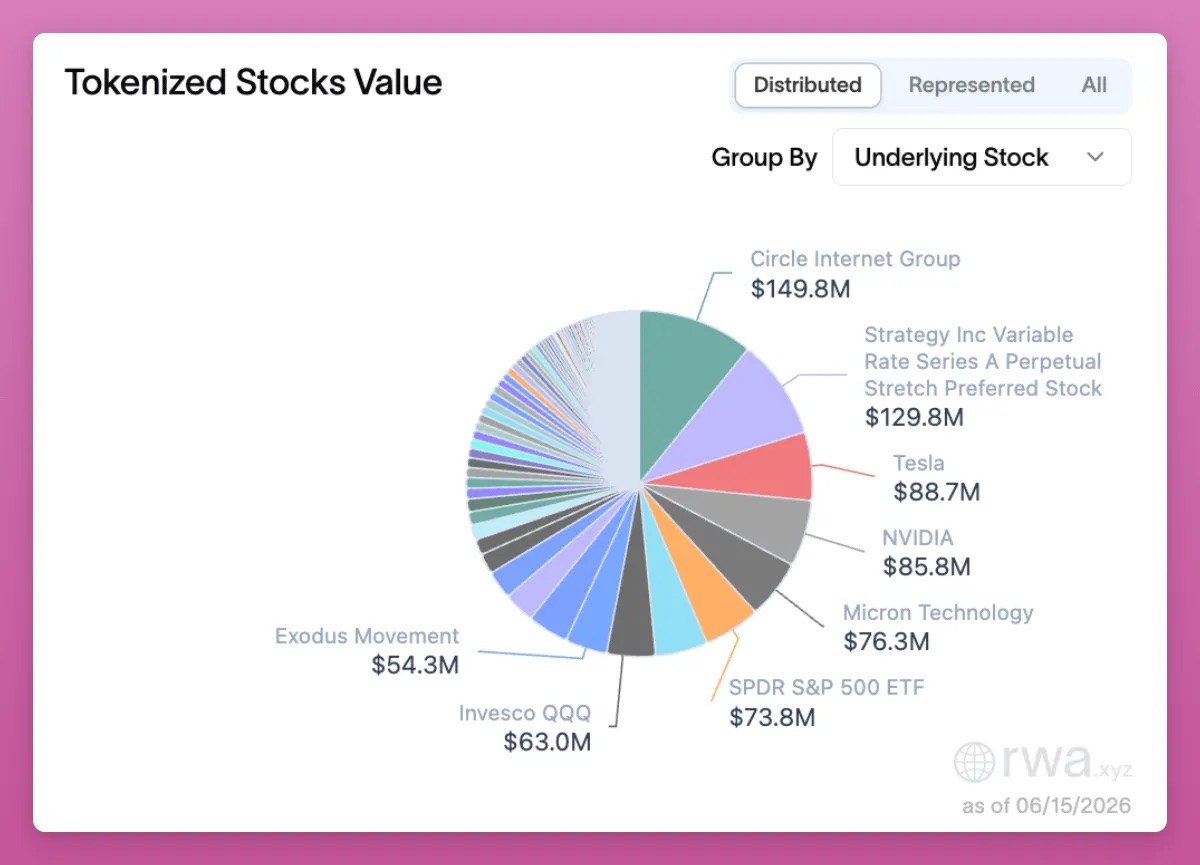

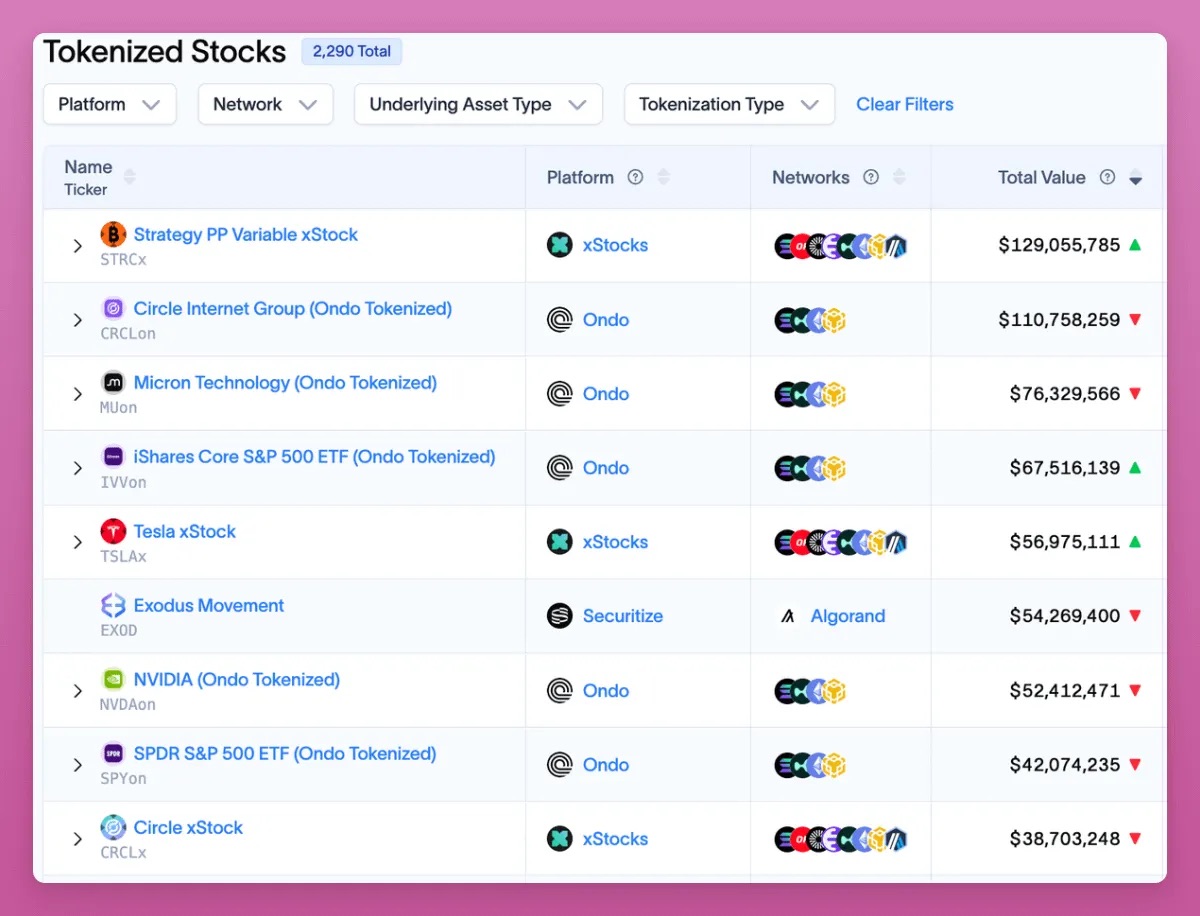

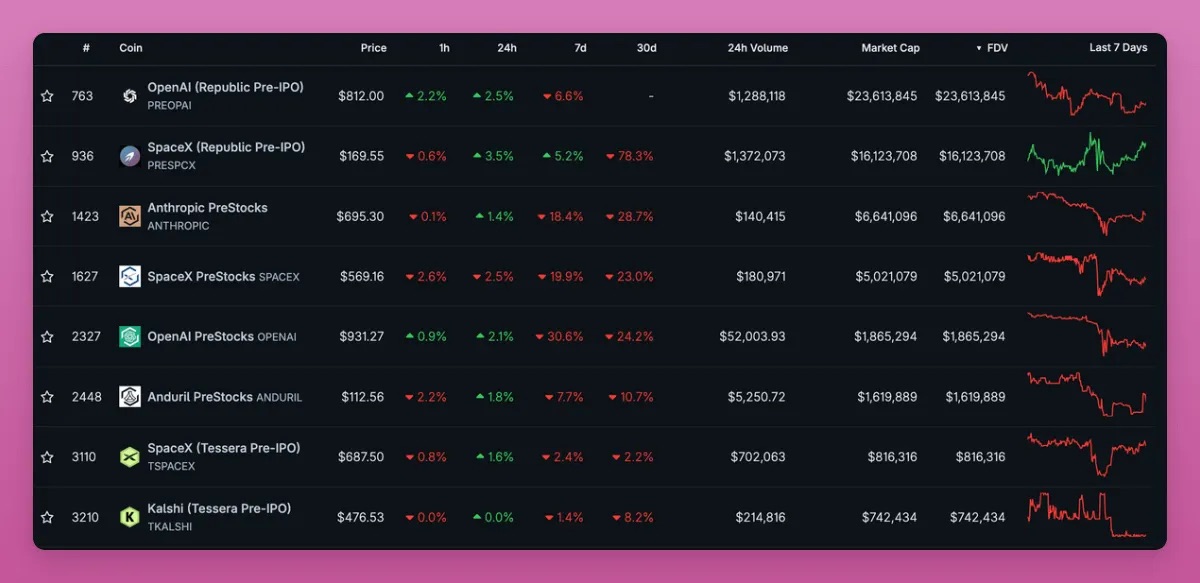

Of course, you can buy these tokens and bet on them skyrocketing tenfold, but apart from a few rare exceptions like Micron Technology (MU), the likelihood of getting rich this way is extremely slim. First, currently only 2,290 stocks have been tokenized, and only about 130 have a total market value exceeding $1 million, with the vast majority of tokenized stocks having almost no liquidity on-chain.

According to statistics from RWA data website rwa.xyz, Strategy is one of the largest targets, with a total value of $129 million.

Currently, most tokenized stocks are from mature listed companies. If you want to discover undervalued and less followed individual stocks, you may have more opportunities through traditional brokers like Interactive Brokers.

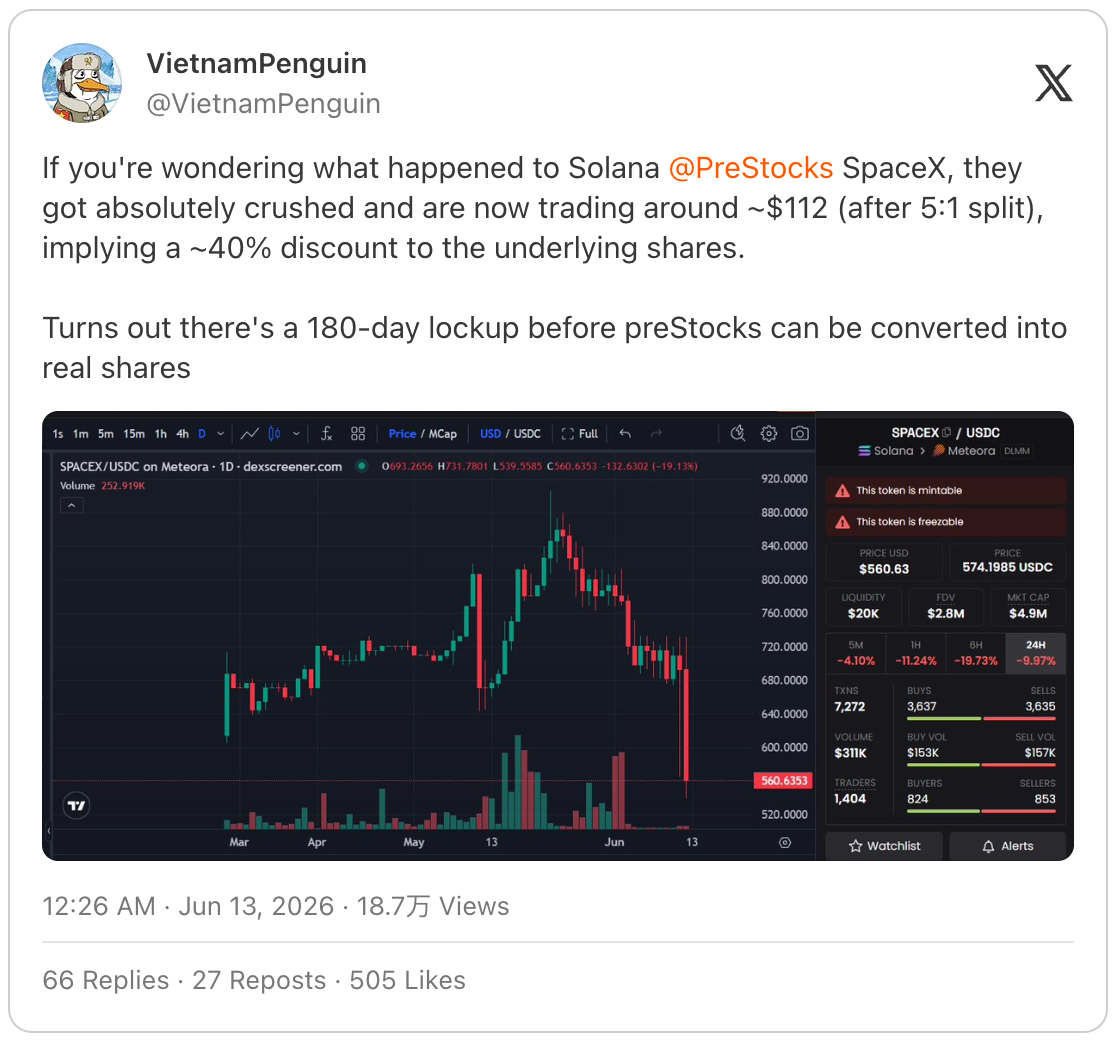

Secondly, holding tokenized stocks comes with many risks that traditional brokers do not have. For example, investors who purchased SpaceX's tokenized stock (SPCX) on the PreStocks platform found that these tokens need to be locked for 180 days in order to be exchanged for real stocks, a piece of news that led to a 40% drop in the token price.

Source: https://x.com/VietnamPenguin/status/2065470925252759680

Thus, investors not only have to bear the native risks of the crypto industry, such as smart contract risks and self-custody asset risks (without enjoying the convenience of self-custody), and liquidity risks but also have to take on additional risks brought by the issuer and asset custodian.

However, I do not entirely deny the tokenized stock sector. It is one of the most promising segments in the crypto industry: it can attract new users while retaining existing users who originally intended to liquidate crypto assets and shift to traditional financial markets. Tokenized stocks bring on-chain trading and fee income to blockchain, and can attract venture capital and developers to the industry, garnering market attention.

Tokenized stocks inherently hold many opportunities: you can deposit them into decentralized exchange (DEX) liquidity pools to earn yields or use them as collateral for loans; you can also hold SPCX spot on-chain while shorting corresponding perpetual contracts to earn delta-neutral income, along with earning points on perpetual contract DEX platforms.

Speaking of hedging strategies, you can buy tokenized stock spots while shorting on the Variational platform. The native token VAR of this platform is likely the best airdrop opportunity right now:

- 50% of the total token supply will be allocated to the community;

- Point activities will end on September 30, leaving about 3.5 months of mining window;

- After the token is launched, the team plans to take 30% of the platform revenue for buybacks and burns;

- The platform is currently still in closed beta testing.

Tokenized stock does not belong to the early investment arena

But my biggest concern with tokenized stocks is that this sector essentially makes crypto investors the handover point for traditional financial assets.

The reason why the crypto industry previously produced a large number of millionaires is that we proactively entered new sectors: Bitcoin, smart contract public chains, various project airdrops, NFTs, Hyperliquid airdrops, and countless others. The tokenized listing process of SpaceX made me see this problem clearly.

Its sales model and hype are identical to hot crypto layer two token issuances: with a small circulation, extremely high fully diluted valuation, and the price fluctuations are completely disconnected from the company's fundamentals. In the short term, the traditional financial market is currently in a phase where "high fully diluted valuation is just a gimmick," exactly like the crypto industry two years ago.

It is undeniable that rockets, artificial intelligence, and Starlink businesses sound promising, but corporate valuations, lock-up timelines, revenue data, and governance mechanisms do not inspire optimism.

The core value of tokenization lies in broadening asset distribution channels: any user with Phantom, Metamask, or Rabby wallets can hold such tokens. Its volatility is lower than Bitcoin and altcoins, while not being pegged to the dollar like stablecoins, making its risk-reward ratio sit somewhere in between. For investors outside of developed markets, or users who do not wish or cannot liquidate crypto assets into the traditional financial system, tokenized stocks provide an attractive solution.

However, this does not mean we have grasped early investment opportunities. The previous appeal of the crypto industry was giving ordinary retail investors the chance to invest in revolutionary enterprises at the startup stage. A $2 trillion IPO project cannot be considered early-stage investment.

The real future of the crypto industry with long-term upside potential lies in enterprises achieving on-chain equity token issuance from inception. ICOs and fair sales were once good attempts, but in the last bull market cycle, the industry increasingly harvested retail investors: early private placement valuations were inflated, TGE further increased, but the allocation for the general public was pitifully small. Cobie analyzed this point thoroughly in his blog post.

Even now, I am still participating in investments on the Echo platform launched by Cobie, because this platform genuinely provides early project investment opportunities: I have already seen a 3.85-times return from my investment in the MegaETH round, even though the market has continued to be sluggish post-token launch.

Apptronic is a humanoid robotics company, and although it is highly valued, I have also participated in its Series B strategic financing. Such investment opportunities are not open to ordinary retail investors on traditional financial platforms.

By the way, besides Echo, I am also very optimistic about the Legion platform, but this platform still needs to find quality investment targets with reasonable valuations, which is not easy.

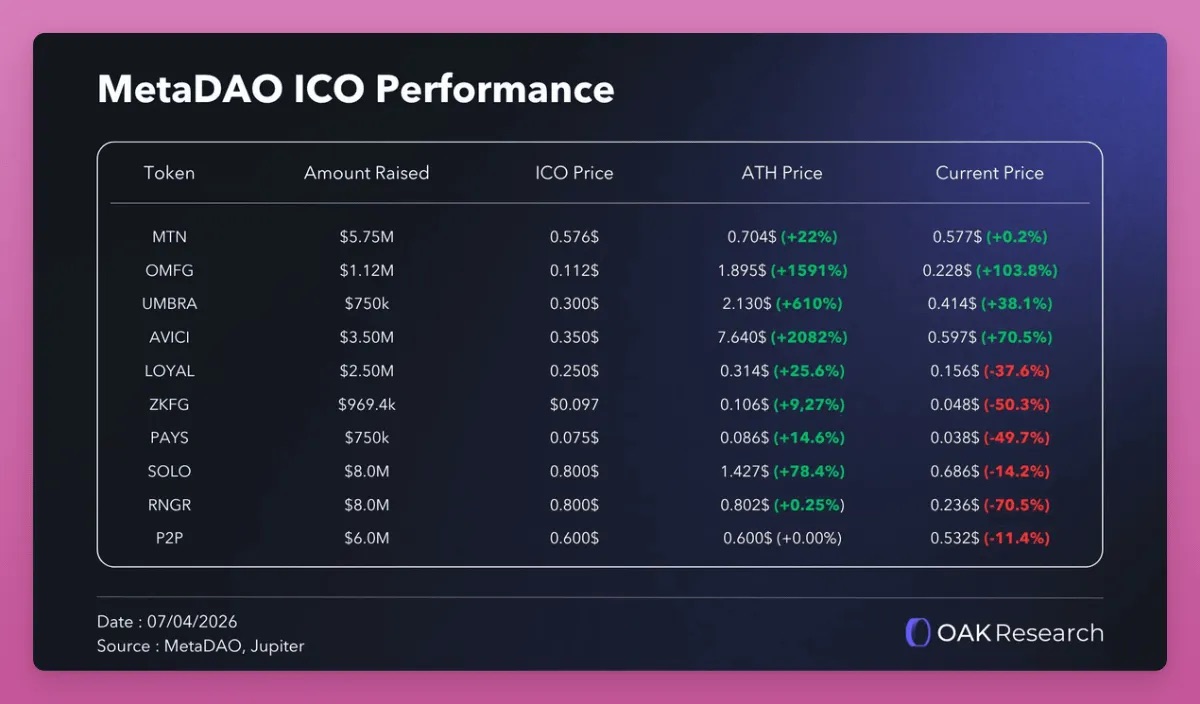

MetaDAO's model is outstanding: the ownership tokens issued by the platform grant holders legitimate equity, monitor the treasury fund expenditures through quota controls, and unlock tokens based on corporate performance, perfectly solving the core issues exposed by the early token issuance. Therefore, considering the current market environment, the various ICO projects launched by MetaDAO have performed better overall.

Source: X platform OAK Research

Additionally, there are native on-chain issuance models, such as the Opening Bell product line launched by Superstate, with the first target being Galaxy stocks, where corporate equity is issued compliantly on-chain.

Imagine if large enterprises did not complete the listing process offline, but instead issued equity directly on Ethereum or Solana public chains, rather than just using blockchain to encapsulate offline legal equity certificates. At that point, the immutability and security of blockchain will become the core competitive advantage of the industry, and the value of the tokens we hold will also rise.

MetaLeX is adopting this solution: it is creating fully programmable on-chain enterprises, with capital, equity, and ownership duration all managed on-chain.

To get back on track, currently, top centralized exchanges like Binance, Coinbase, and Kraken are heavily investing in traditional financial businesses, launching stocks, bonds, and ETF token products. However, the xStocks platform cannot deliver underlying physical stocks, resulting in Binance, Bybit, and Bitget all delisting the SpaceX tokenized stock products, with over $1 billion in user orders unable to be fulfilled. In contrast, trading orders from traditional brokers are much more stable.

Stablecoins were initially only used for short-term asset storage while waiting to enter the crypto-native assets; today, stablecoins have become the liquidity outlet for middle-aged investors from traditional finance.

Some might say that tokenized stocks before the IPO allow ordinary people to get in early on top-tier companies like OpenAI and Anthropic. Indeed, in terms of market capitalization, these two are currently the hottest tokenized targets in the primary market, but both companies are valued close to a trillion dollars.

This hardly counts as early investment: Anthropic's latest Series H strategic financing has reached a valuation of $965 billion. Rounds of financing: Series A, B, C, D, E, F, G, H (most recent round)

The tokenized equity sector is still in an extremely early stage

Standard Chartered has given a target price of $100 for Uniswap's token UNI, indicating a potential increase of 40 times! The underlying logic is as follows: the bank predicts that by 2030, the scale of tokenized assets circulating in decentralized finance will grow 37 times (currently only accounting for 3.5% of total assets, it will increase to 30% by 2030); the total on-chain tokenized asset scale will exceed $40 trillion by 2028.

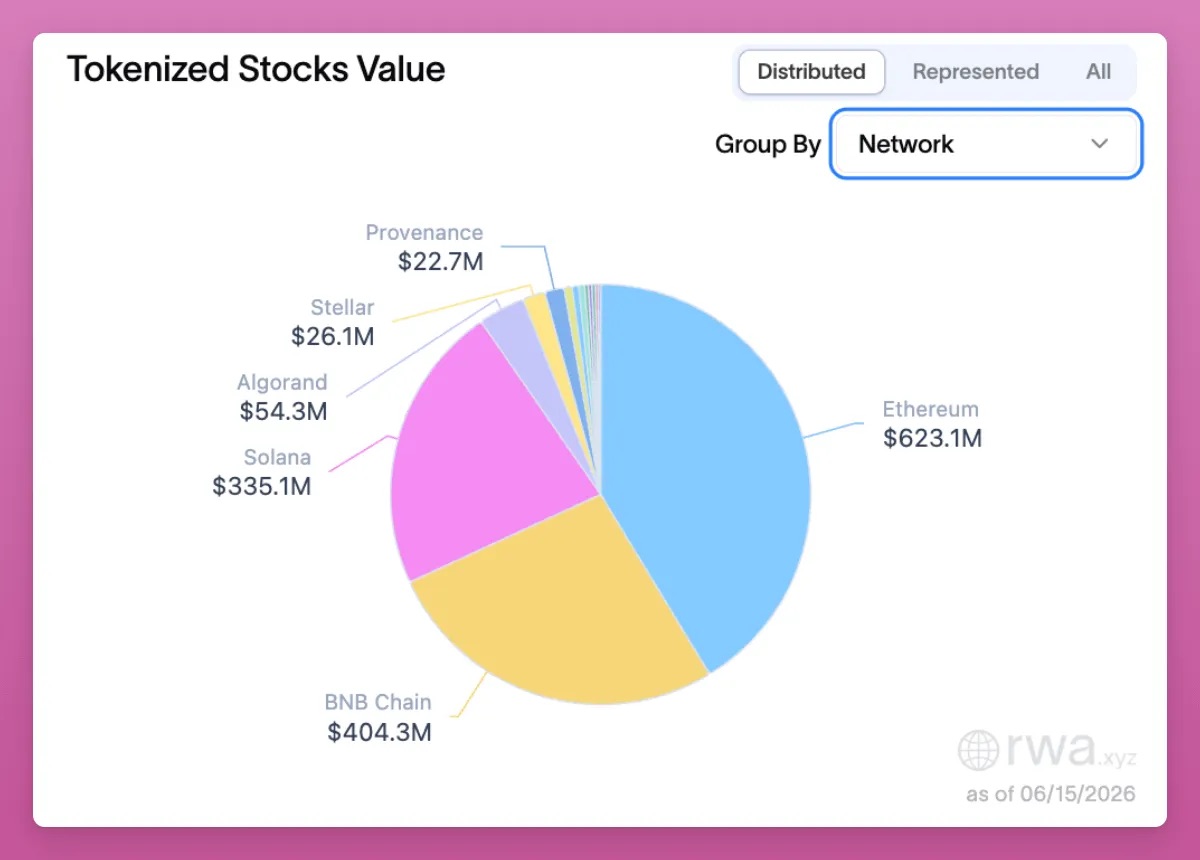

So far, the total value of tokenized equity freely circulating across platforms is $1.5 billion (these assets can detach from the issuing platform and conduct peer-to-peer transfers between different wallets), mainly deployed on Ethereum, BNB Smart Chain, and Solana public chain. However, the overall size of the sector is still very small: $1.5 billion is even lower than UNI's own market capitalization of $1.9 billion.

Standard Chartered has always given extremely optimistic price predictions (once predicting $40,000 for Ethereum and $500,000 for Bitcoin by 2030), but the logic behind supporting UNI is very sound: the value locked in tokenized equity continues to rise, which will drive on-chain trading volumes up, and platform fees will simultaneously increase, with current fees being used for buybacks and token burns of UNI.

Not only Uniswap stands to benefit. Once the tokenized equity sector experiences a boom, the entire crypto supply chain will profit: lending protocols like Aave, Fluid, Kamino, and decentralized exchanges across various public chains, including Pancakeswap and Jupiter, will also share the dividends.

The development of tokenized equity will give the crypto industry counter-cyclical properties: currently, when Bitcoin and Ethereum prices are falling, there is a large-scale deleveraging in decentralized lending, with revenues from various protocols shrinking and platform tokens being under pressure. Decentralized exchanges for perpetual contracts will be among the first to benefit from tokenized stocks, while spot exchanges will be the next wave of beneficiaries.

After the report from Standard Chartered was released, the UNI token rose 13% in one day, but there are more investment opportunities within the sector. Over the past two weeks, the platform token BP of Backpack has surged by 200%.

Backpack, as a centralized exchange, has previously struggled to find a core business that truly meets market demand, facing competition from established exchanges like Binance and also vying for users with the Hyperliquid decentralized perpetual contract platform. The tokenized asset business seems to have finally provided it with a core growth trajectory.

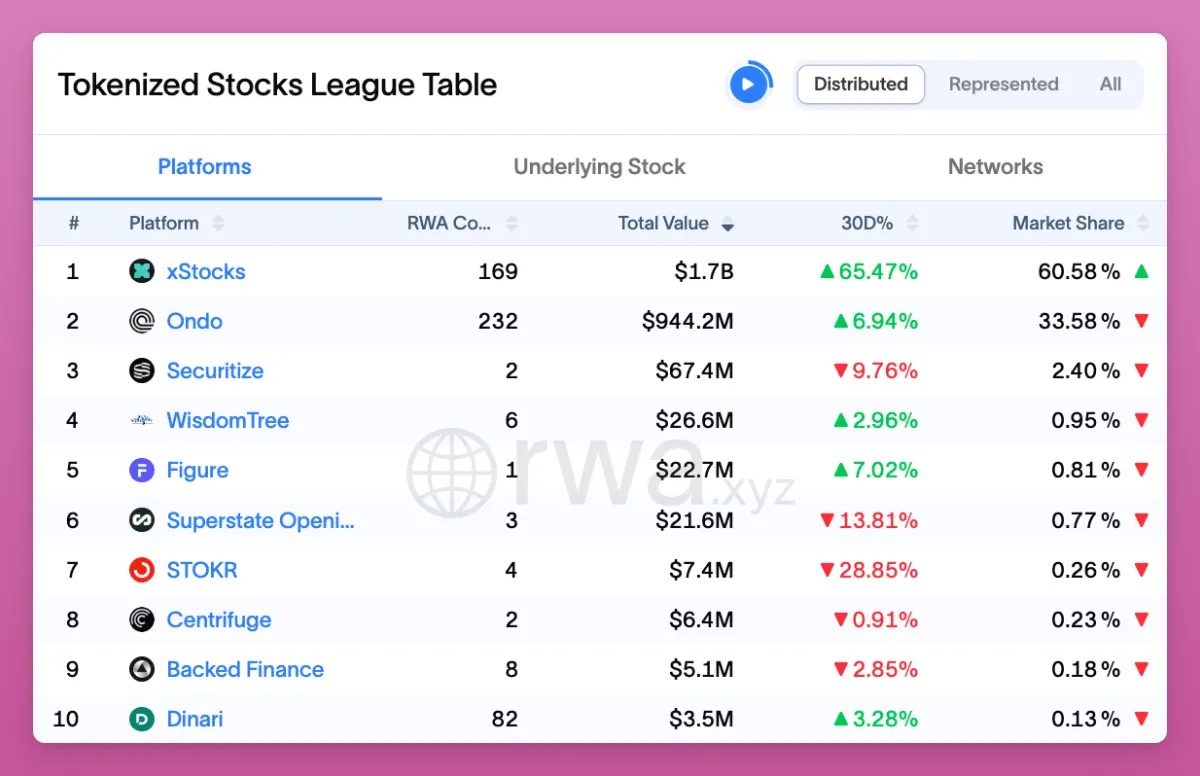

The vast majority of tokenized stocks on the market (xStocks, Ondo) belong to a custodial packaging model: the issuing institution holds the physical stocks, minting tokens that track stock prices, and users can only achieve price returns without holding real equity. However, Backpack achieves native on-chain issuance through the Opening Bell product line under Superstate: the tokens are formally registered equity with the U.S. Securities and Exchange Commission, fully consistent with the equity rights of NASDAQ-listed stocks, granting holders dividends and voting rights, with the platform holding a complete set of compliance licenses (the founding team of Backpack comes from the original FTX Europe branch).

This logic also extends to the platform's native token BP: staking BP for one year will allow for redeeming it for the company's physical equity upon IPO or acquisition (with a seven-day redemption window each year).

The tokenized equity sector also has many direct trading opportunities: Ondo ranks second in the industry by total circulating value, with the platform having issued its native token ONDO.

However, ONDO only possesses governance functionality, having almost no capacity for value capture, as all platform revenues belong to the company and will not be shared with token holders. Although the market is discussing the commencement of a fee-sharing mechanism, implementation still carries uncertainties. Additionally, the pressure from token dilution is significant, with nearly 50% of tokens still awaiting unlocking by 2029.

If sentiment in the tokenized equity market heats up, there may be short-term speculation opportunities for ONDO, but I will not hold it long-term.

The industry leader xStocks occupies 60% of the market share, with a total scale of about $1.7 billion. Backed Finance will purchase real stocks and ETFs, held in reserve by custodial institutions on a 1:1 basis, and then mint tokens that track asset prices. Products are deployed on Solana and Ethereum (with some on Arbitrum layer two), and users can trade on Kraken five days a week or trade on-chain around the clock, covering about 60 targets. The number of targets is less than Ondo, but capital liquidity is better.

Holding xStock tokens does not equate to holding the underlying physical stocks; it is merely a creditor's rights against the issuing organization. Once the platform encounters risk, investors will only belong to the unsecured creditors of a cross-jurisdictional packaging service provider, completely different from the model of holding real equity like that of Backpack.

Ironically, weeks before Kraken acquired Backed Finance, it had just submitted its own IPO application, initially valued at $20 billion. This has raised market questions about whether the platform would issue an independent token.

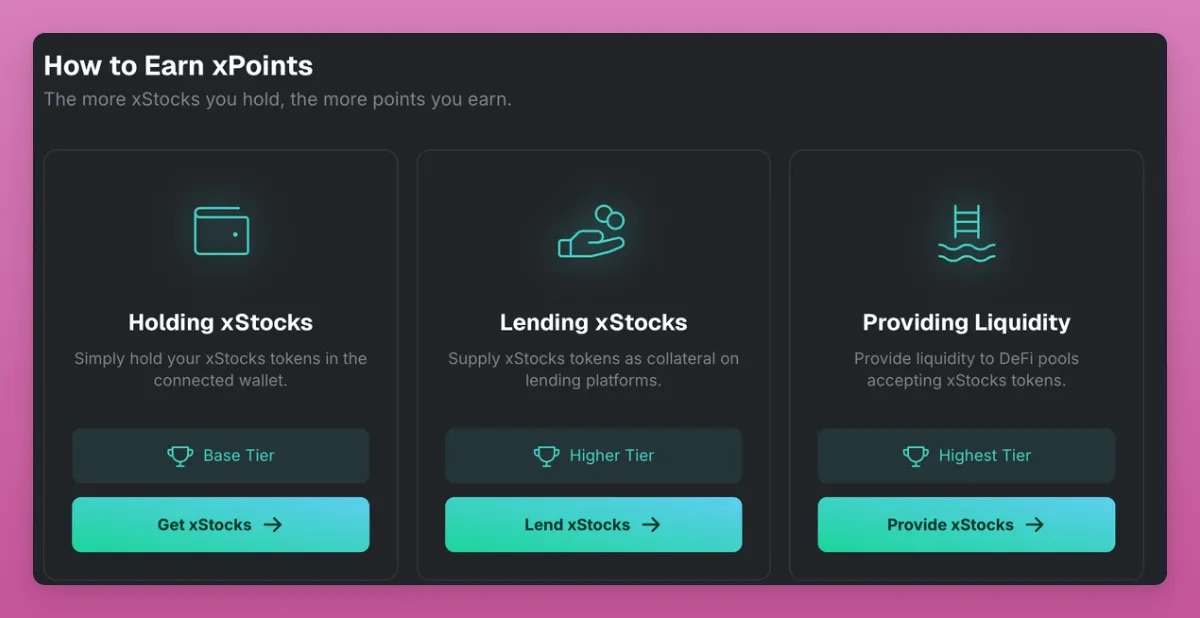

After the acquisition, xStocks launched the xPoints reward program in March, which is usually a precursor to token issuance, but the platform has yet to confirm if it will launch a token.

xPoints activity official website

This matter is quite strange: Kraken itself could issue its equity through traditional channels; why would it need to issue a separate token for the xStocks platform?

A more reasonable explanation for launching the reward program is that Kraken has reached a cooperative agreement with NASDAQ to tokenize stocks, and the platform requires trading volumes and liquidity to support business scale, thereby boosting Kraken's overall performance data.

I do not wish to become just another handover point in the sector, but if you are willing to participate in the points mining, the rules for earning points are as follows:

- Providing liquidity: 7x points (highest tier, supporting Raydium, Orca, Byreal)

- Asset lending: 5x points (Kamino platform)

- Simply holding tokens: 1x base points

- Trading on Kraken centralized exchange does not earn points, only on-chain operations can accumulate points

The third largest in the industry is Securitize, and I do not plan to participate in its rewards mining. The company will go public via a SPAC merger with Cantor Equity Partners, with an overall valuation of about $1.25 billion, and BlackRock leading a $47 million financing round. The platform has no native token, and mining offers no returns.

As mentioned above, various arbitrage plays exist within the sector: for example, when perpetual contract funding rates are negative, you can short on Hyperliquid (also mine trade.xyz points) and buy the spot tokens simultaneously; or you can compare funding rates among various exchanges on the Ostium platform (this platform currently does not have a token).

If manual position management is too cumbersome, consider the Nado platform: it is an order book-based decentralized exchange that supports unified margin accounts for spot, margin, and perpetual contracts; the development team previously built Kraken and launched the INK product. The platform will support tokenized stock spots and perpetual contracts, achieving delta-neutral strategies—a relatively low-profile opportunity worth participating in for points mining.

But be vigilant: the primary market token platform Ventuals has just announced its shutdown, notifying users that all platform points will be rendered worthless. Participating in token airdrop mining now requires more effort, significantly increasing the uncertainty of returns.

The story is far from over

The term "crypto" now covers a very wide range, including perpetual contracts, NFTs, prediction markets, meme coins, and more; the RWA sector is also continuously expanding in size, and detailed breakdowns of the segmented tracks deserve individual deep dives.

Stablecoins, money funds, credit, private equity, and tokenized stocks belong to different segments, each with vastly different risk and reward logic.

The unique advantage of tokenized stocks lies in asset turnover efficiency: stocks inherently carry price volatility, enabling arbitrage and trading opportunities that passive real-world assets do not possess.

I believe this will rejuvenate public chains focused on trading, with Solana particularly benefiting (I see Ethereum as a storage public chain for high-value assets, more suitable for passive investment).

Previously, the Solana ecosystem relied heavily on meme coins, but the new narrative of "everything can be traded on-chain" through tokenized equities may strengthen the public chain market. For example, trading volume in tokenized equities may soon dominate the total transaction volume on the Solana chain: transfer fees are low, and confirmation speed is quick, providing a better user experience than Ethereum-based public chains.

In the future, millions of ordinary retail investors may hold and trade tokenized equities on their mobile devices rather than simply storing stablecoins, which will boost the ecosystem income of mainstream layer one public chains and subsequently elevate public chain token valuations.

In summary, to genuinely achieve wealth growth through the tokenized stock sector, the core idea is to bet on the widespread implementation of on-chain asset tokenization: which issuers and platforms will dominate the sector in the next year, three years, or five years? Which platforms will issue tokens and initiate airdrops? The investment targets are right in front of you: you can position in UNI, BP, ONDO, or wait for Kraken to go public.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。